Global Smart Prosthetics Market Size, Growth & Revenue 2024-2034

Global Smart Prosthetics Market is segmented by Product Type (Myoelectric Prosthetics, Bionic Prosthetics, Sensor-Integrated Prosthetics, Body-Powered Prosthetics, Hybrid Prosthetics), Application (Upper Limb Prosthetics, Lower Limb Prosthetics, Cosmetic Prosthetics, Pediatric Prosthetics, Sports Prosthetics), End-Use Industry (Healthcare Facilities, Rehabilitation Centers, Sports Institutions, Home Care Settings), Distribution Channel (Direct Sales, Third-Party Distributors, Online Sales Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Smart Prosthetics Market represents a dynamic and rapidly evolving segment of the medical device industry, focused on the development and deployment of technologically advanced prosthetic limbs that enhance patient mobility and quality of life. These smart prosthetics incorporate sensors, robotics, and AI-driven control systems to provide intuitive movement, improved durability, and customization options tailored to individual needs. The market scope includes various prosthetic types such as myoelectric, bionic, sensor-integrated, body-powered, and hybrid models, catering to diverse applications including upper and lower limb replacements, cosmetic enhancements, pediatric care, and sports performance. Global demand is driven by an aging population, increasing prevalence of diabetes and vascular diseases leading to amputations, and heightened awareness of rehabilitation technologies. Moreover, advancements in materials science and connectivity further expand the functional capabilities of smart prosthetics. The market is characterized by significant innovation, extensive research collaborations, and increasing investments from both public and private sectors. As a result, stakeholders ranging from manufacturers to healthcare providers find strategic importance in this segment for future growth and patient-centric care.

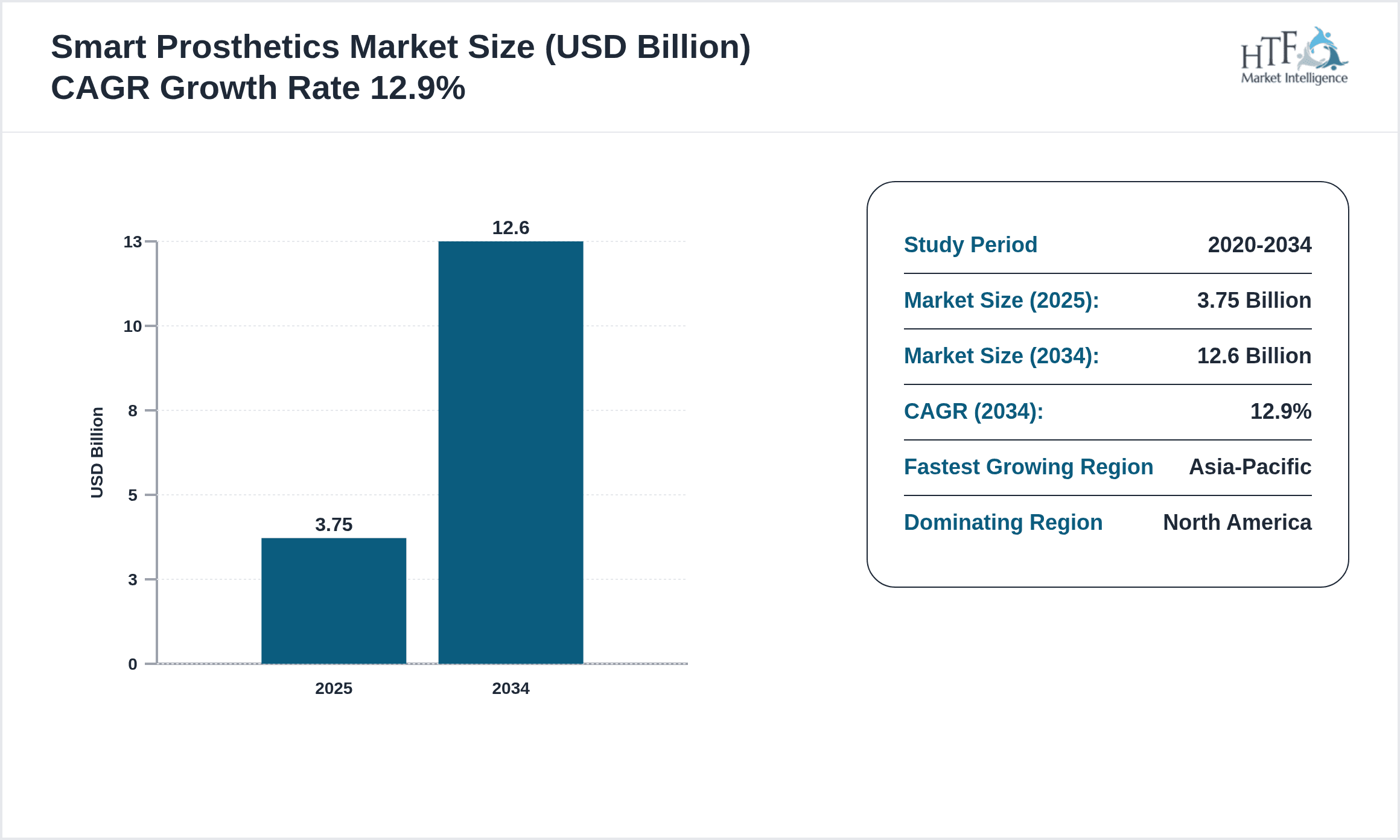

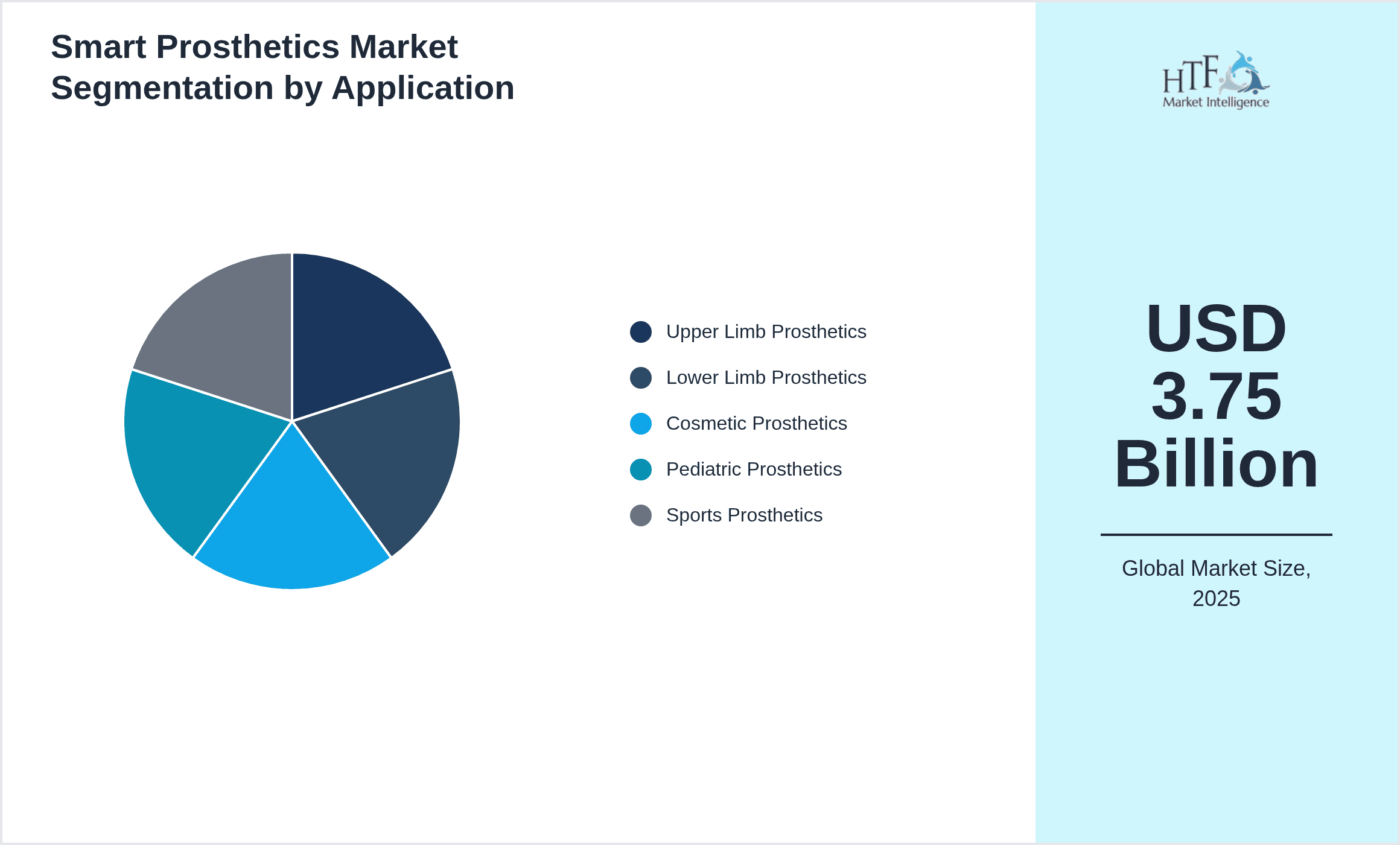

- •Key market highlights include a base market size of USD 3.75 Billion in 2024 with projections reaching USD 12.6 Billion by 2034, illustrating a robust compound annual growth rate (CAGR) of 12.9%. The market's rapid expansion is bolstered by technological breakthroughs such as sensor integration and AI-enabled control systems, which enhance prosthetic responsiveness and user experience. North America currently dominates the market, driven by advanced healthcare infrastructure and high adoption rates, while Asia-Pacific is identified as the fastest-growing region due to increasing healthcare investments and rising awareness. Myoelectric prosthetics hold the leading product type position, with sensor-integrated prosthetics exhibiting the fastest growth trajectory. Applications focusing on upper and lower limb prosthetics dominate in terms of volume and revenue share, reflecting the prevalence of limb loss in these categories.

- •The Global Smart Prosthetics Market offers significant value proposition through improved patient mobility, reduced rehabilitation time, and enhanced customization, making it strategically important across medical, sports, and cosmetic industries. The integration of advanced technology not only elevates patient outcomes but also opens new avenues for manufacturers and service providers to innovate and expand their portfolios. Healthcare providers benefit from improved treatment protocols and patient satisfaction, while investors witness promising returns fueled by continuous R&D and expanding end-user base. The evolving regulatory landscape further supports market growth by ensuring safety and efficacy standards, thus fostering confidence among stakeholders and facilitating global market penetration.

Competitive Landscape

The competitive landscape of the Global Smart Prosthetics Market is marked by intense rivalry among established multinational corporations and emerging innovative startups. Market participants prioritize continuous innovation, focusing on integrating advanced sensor technologies, AI, and robotics to differentiate their offerings. Strategic partnerships, collaborations with research institutions, and mergers & acquisitions are common approaches to enhance product portfolios and expand geographic reach. Companies invest heavily in R&D to develop lightweight, durable, and highly responsive prosthetics that cater to diverse patient needs. Pricing strategies and reimbursement frameworks also play critical roles in shaping competitive positioning. Furthermore, regional players leverage local market insights to tailor products for specific demographics, increasing their competitive edge. The market entry barriers include high technological complexity, regulatory compliance, and substantial capital requirements, which protect incumbent firms but also encourage strategic alliances to navigate these challenges. Looking ahead, competition is expected to intensify with the advent of disruptive technologies and growing demand for personalized prosthetic solutions.

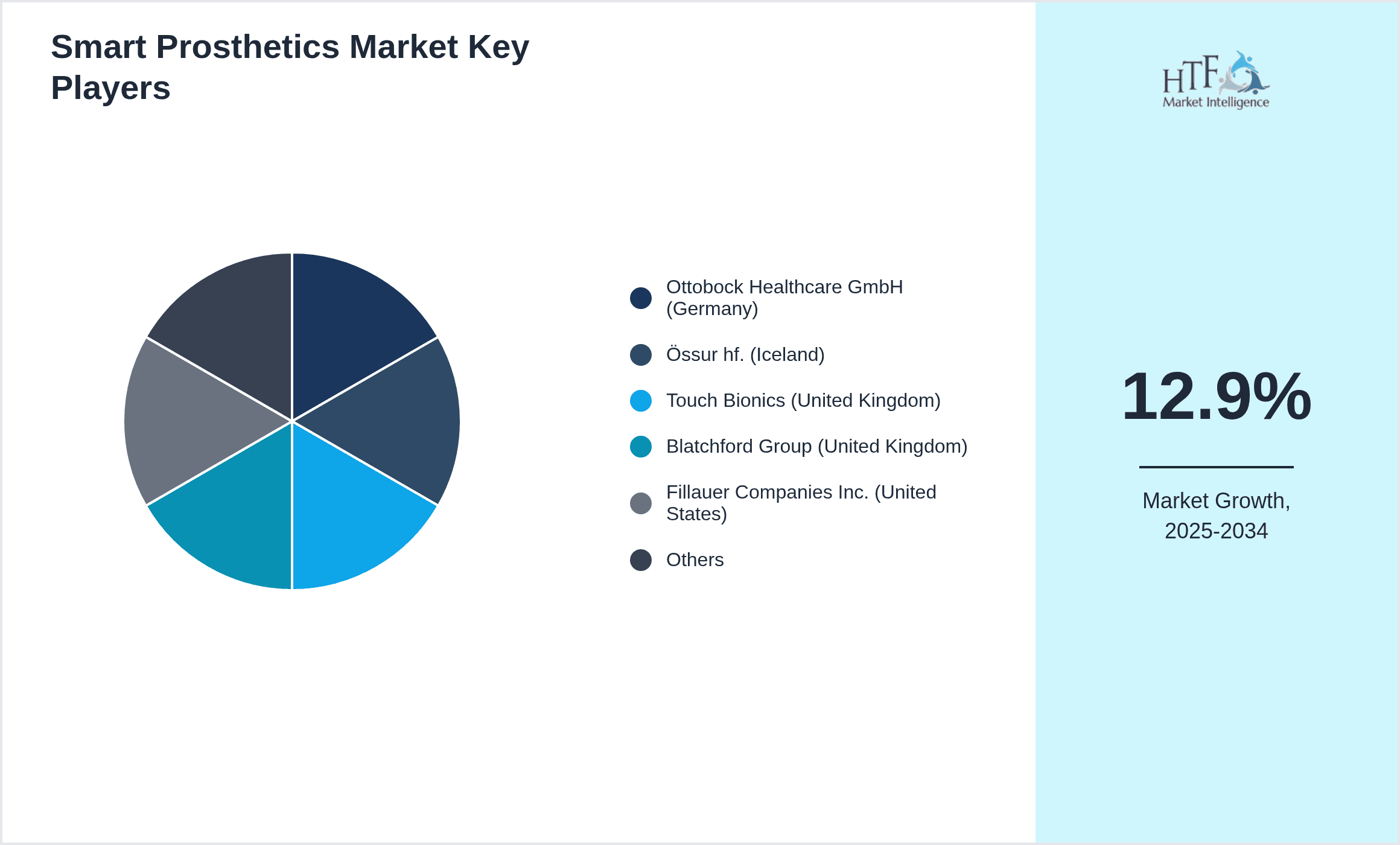

Prominent Players in Smart Prosthetics Market

- •Ottobock Healthcare GmbH (Germany)

- •Össur hf. (Iceland)

- •Touch Bionics (United Kingdom)

- •Blatchford Group (United Kingdom)

- •Fillauer Companies Inc. (United States)

- •Mobius Bionics (United States)

- •RSLSteeper (United Kingdom)

- •Endolite (United Kingdom)

- •Freedom Innovations (United States)

- •Hanger, Inc. (United States)

- •Blatchford (United Kingdom)

- •Rheo Knee (United States)

- •Coapt LLC (United States)

- •BeBionic (United Kingdom)

- •Infinite Biomedical Technologies (United States)

- •BionX Medical Technologies (Canada)

- •Endo Prosthetics LLC (United States)

- •Coyote Design (United States)

- •Taska Prosthetics (United Kingdom)

- •Liberating Technologies, Inc. (United States)

- •Proteor (France)

- •Gulick Group (United States)

- •Medicare Prosthetics (Canada)

- •Athletics Prosthetics Corp. (United States)

- •Trulife Ltd. (United Kingdom)

Market Breakdown

- •By Product Type

- ◦Myoelectric Prosthetics

- ◦Bionic Prosthetics

- ◦Sensor-Integrated Prosthetics

- ◦Body-Powered Prosthetics

- ◦Hybrid Prosthetics

- •By Application

- ◦Upper Limb Prosthetics

- ◦Lower Limb Prosthetics

- ◦Cosmetic Prosthetics

- ◦Pediatric Prosthetics

- ◦Sports Prosthetics

- •By End-Use Industry

- ◦Healthcare Facilities

- ◦Rehabilitation Centers

- ◦Sports Institutions

- ◦Home Care Settings

- •By Distribution Channel

- ◦Direct Sales

- ◦Third-Party Distributors

- ◦Online Sales Platforms

Growth Dynamics

- •Rising incidence of limb loss due to diabetes, accidents, and vascular diseases globally propels demand for advanced smart prosthetics offering enhanced mobility and user comfort. For example, increasing diabetic amputations in Asia-Pacific necessitate sophisticated prosthetic solutions tailored to patient needs.

- •Technological advancements such as integration of AI, machine learning algorithms, and sensor technology in prosthetics enable intuitive control and adaptability, significantly improving user experience and expanding market adoption worldwide.

- •Growing geriatric population with increasing prevalence of age-related limb amputations fuels demand for durable and efficient smart prosthetic devices, especially in North America and Europe where aging demographics are prominent.

- •Government initiatives and reimbursement policies in developed economies encourage adoption of smart prosthetics by reducing treatment costs and promoting innovation through funding and grants, thereby boosting market growth.

- •Increasing awareness and social acceptance of prosthetic technologies coupled with rising sports participation among amputees create new opportunities for specialized sports prosthetics, driving segment growth.

- •Investment in R&D by leading companies to develop lightweight, durable materials and improve battery efficiency enhances product attractiveness and market penetration across diverse applications.

- •Emergence of tele-rehabilitation and remote monitoring technologies integrated with smart prosthetics provides improved patient outcomes and lowers healthcare burdens, acting as a key growth catalyst.

Market Trends

- •The market is witnessing a trend towards miniaturization and enhanced portability of prosthetic devices, with companies focusing on compact sensor systems and lightweight materials that increase user convenience and functionality.

- •Adoption of 3D printing technology for customized prosthetic components allows rapid prototyping and cost-effective production, enabling personalized solutions to meet unique patient requirements.

- •Integration of wireless connectivity and IoT capabilities in smart prosthetics enables real-time data transmission for monitoring and adjustment, improving rehabilitation and device performance.

- •Sustainability considerations influence material selection and manufacturing processes, with increased focus on eco-friendly and recyclable components in prosthetic production.

- •Collaborative ecosystems involving manufacturers, healthcare providers, and technology firms foster innovation and accelerate market development through shared expertise and resources.

- •Segmentation of the market based on application is becoming more granular, with specialized devices for pediatric and sports use gaining traction due to tailored design and functionality.

- •Future directions include development of neural interface prosthetics that directly connect with the nervous system, promising unprecedented control and sensory feedback capabilities.

Market Opportunities

- •Expanding markets in emerging economies present substantial growth potential due to rising healthcare infrastructure investments and increasing awareness about advanced prosthetic solutions.

- •Development of smart prosthetics tailored for pediatric patients offers untapped opportunities by addressing growth-related challenges and unique functional requirements.

- •Integration of AI-driven predictive maintenance and self-diagnostic features in prosthetics opens avenues for service innovation and enhanced customer satisfaction.

- •Collaborations between technology companies and healthcare providers can accelerate development of next-generation prosthetics with enhanced sensory feedback and control mechanisms.

- •Opportunities exist in the sports prosthetics segment as rising participation of disabled athletes and para-sports events drive demand for high-performance devices.

- •Geographic expansion into underpenetrated regions supported by government healthcare initiatives can significantly boost market share for leading manufacturers.

- •Innovative financing models such as leasing and pay-per-use can improve affordability and accessibility of smart prosthetics, broadening consumer base.

Market Challenges

- •High costs associated with advanced smart prosthetic technologies pose affordability challenges for patients, especially in developing markets where healthcare coverage is limited.

- •Complex regulatory approval processes across different regions can delay product launches and increase time-to-market, impacting competitive positioning.

- •Technical limitations such as battery life, reliability of sensors, and durability under strenuous conditions remain critical hurdles for widespread adoption.

- •Lack of awareness and trained healthcare professionals to fit and maintain smart prosthetics restricts market penetration in some regions.

- •Supply chain disruptions and dependence on specialized components can affect manufacturing continuity and cost structures.

- •Competition from low-cost traditional prosthetics and counterfeit products undermines market growth and brand reputation.

- •Ethical and privacy concerns related to data collected through connected prosthetics may impact user acceptance and regulatory scrutiny.

Regulatory Framework

- •Between 2019 and 2024, regulatory agencies such as the FDA and EMA have strengthened approval requirements for smart prosthetics, mandating rigorous clinical testing to ensure safety and efficacy, which has elevated market standards.

- •New regulations introduced in 2021 emphasize cybersecurity protocols for connected prosthetic devices, requiring manufacturers to implement robust data protection measures to safeguard patient information.

- •Safety standards updated in 2020 mandate compliance with electromagnetic compatibility and biocompatibility for sensor-integrated prosthetics, impacting design and manufacturing processes.

- •Region-specific mandates, such as the EU Medical Device Regulation (MDR) implemented in 2021, require enhanced post-market surveillance and traceability for smart prosthetics sold in Europe.

- •Government initiatives launched between 2019 and 2024 provide funding and incentives to encourage innovation and adoption of advanced prosthetic technologies, supporting market expansion globally.

Market Intelligence

- •15th February 2025, Ottobock Healthcare GmbH launched the latest generation of their Sensor-Integrated Prosthetics featuring advanced AI-driven motion recognition and adaptive grip strength, targeting upper limb amputees seeking enhanced dexterity and control. This product aims to reduce rehabilitation time and improve user comfort through seamless integration with mobile applications for personalized adjustments. The launch is expected to strengthen Ottobock's market leadership and expand its footprint in Asia-Pacific and Europe. Source: Official Ottobock Press Release

- •10th January 2025, Össur hf. introduced a new hybrid prosthetic combining myoelectric and body-powered technologies to offer both power and reliability for lower limb amputees. The device incorporates lightweight materials and enhanced battery efficiency, improving mobility and endurance. This innovation aligns with growing demand for versatile and durable prosthetics in sports and rehabilitation sectors globally, particularly in North America and Europe. Source: Össur Corporate Announcement

- •8th March 2025, Touch Bionics announced a strategic partnership with a leading AI firm to co-develop neural interface prosthetics capable of direct brain-computer communication. This collaboration aims to pioneer next-generation prosthetic control systems, providing unprecedented sensory feedback and movement precision. The initiative is expected to position Touch Bionics at the forefront of smart prosthetics innovation over the coming decade. Source: Company Website

- •5th April 2025, Fillauer Companies Inc. completed the acquisition of a startup specializing in 3D-printed customized prosthetic sockets, enhancing its portfolio with cost-effective, patient-specific solutions. This strategic move expands Fillauer's distribution channels and technological capabilities, facilitating market penetration in emerging regions such as Latin America and Middle East & Africa. The acquisition supports Fillauer’s growth ambitions and addresses increasing demand for personalized prosthetics. Source: Industry Publication

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.75 Billion |

| Forecast Year Market Size | USD 12.6 Billion |

| CAGR | 12.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.3% |

| Scope of Report | Market is segmented by Product Type (Myoelectric Prosthetics, Bionic Prosthetics, Sensor-Integrated Prosthetics, Body-Powered Prosthetics, Hybrid Prosthetics), Application (Upper Limb Prosthetics, Lower Limb Prosthetics, Cosmetic Prosthetics, Pediatric Prosthetics, Sports Prosthetics), End-Use Industry (Healthcare Facilities, Rehabilitation Centers, Sports Institutions, Home Care Settings), Distribution Channel (Direct Sales, Third-Party Distributors, Online Sales Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Ottobock Healthcare GmbH (Germany), Össur hf. (Iceland), Touch Bionics (United Kingdom), Blatchford Group (United Kingdom), Fillauer Companies Inc. (United States), Mobius Bionics (United States), RSLSteeper (United Kingdom), Endolite (United Kingdom), Freedom Innovations (United States), Hanger, Inc. (United States), Blatchford (United Kingdom), Rheo Knee (United States), Coapt LLC (United States), BeBionic (United Kingdom), Infinite Biomedical Technologies (United States), BionX Medical Technologies (Canada), Endo Prosthetics LLC (United States), Coyote Design (United States), Taska Prosthetics (United Kingdom), Liberating Technologies, Inc. (United States), Proteor (France), Gulick Group (United States), Medicare Prosthetics (Canada), Athletics Prosthetics Corp. (United States), Trulife Ltd. (United Kingdom) |

Global Smart Prosthetics Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.