Global Rugged Smartphones Market Size, Growth & Revenue 2024-2034

Global Rugged Smartphones Market is segmented by Product Type (Waterproof Rugged Smartphones, Shockproof Rugged Smartphones, Dustproof Rugged Smartphones, Freezeproof Rugged Smartphones, Other Rugged Smartphones), Application (Field Services, Military & Defense, Outdoor Recreation, Transportation & Logistics, Construction), End-Use Industry (Oil & Gas, Mining, Public Safety, Manufacturing), Distribution Channel (Online Retail, Specialized Distributors, Direct Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global rugged smartphones market comprises durable mobile devices engineered to operate reliably in harsh environments such as extreme temperatures, water exposure, dust, and mechanical shocks. These devices are widely used in sectors like field services, military, construction, outdoor recreation, and logistics, where conventional smartphones cannot withstand operational stresses. The market includes product types like waterproof, shockproof, dustproof, and freezeproof smartphones, each designed to meet specific environmental challenges. Growing demand from industries requiring robust communication tools, technological advancements in mobile durability, and increasing adoption in developing regions are significant drivers. The market's scope also covers innovations in battery technology, secure communication features, and enhanced user interfaces tailored for challenging conditions. Rising infrastructure development, government initiatives in defense and public safety, and expanding outdoor recreational activities globally further fuel the market growth. Overall, the rugged smartphones market represents a critical segment of the mobile device industry focused on resilience, longevity, and specialized usability.

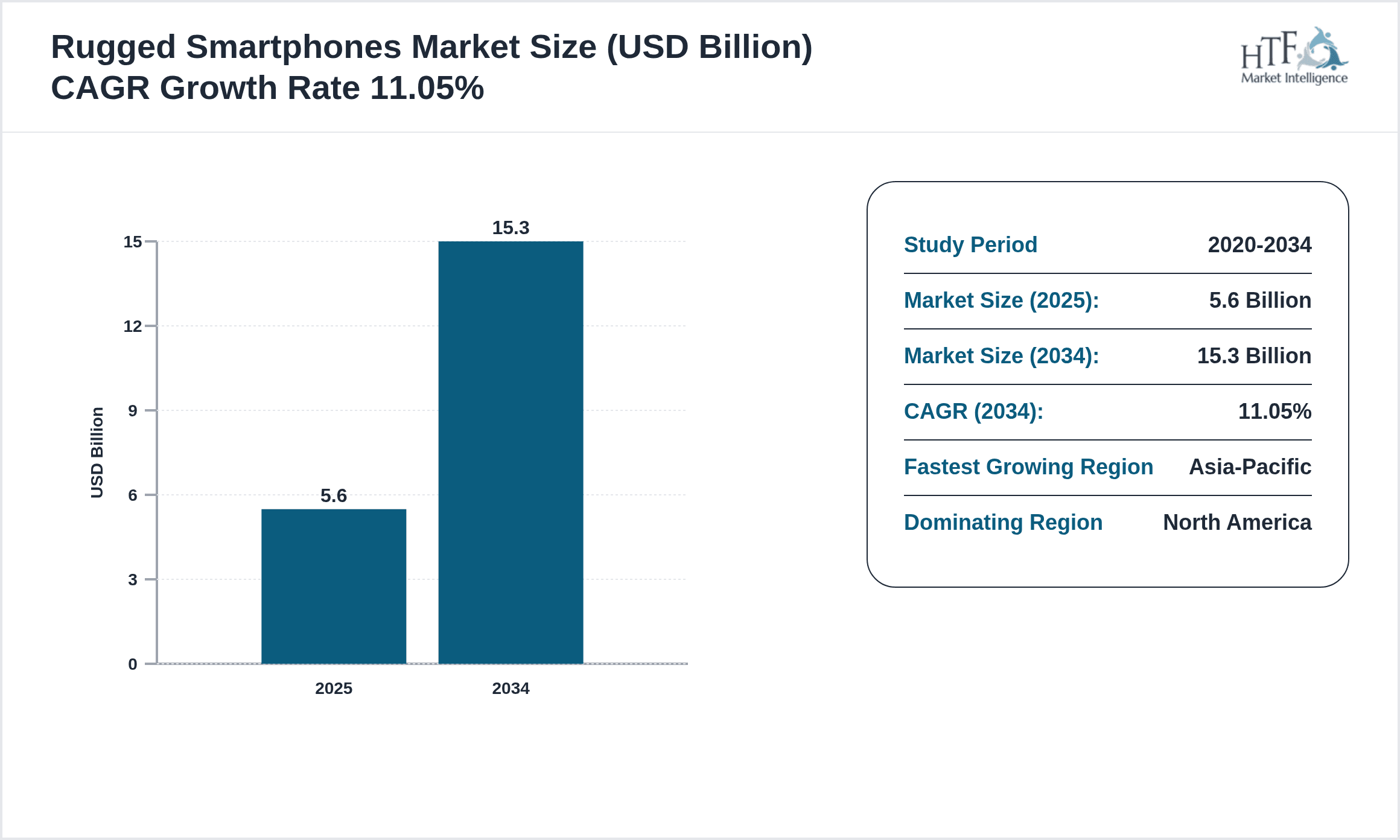

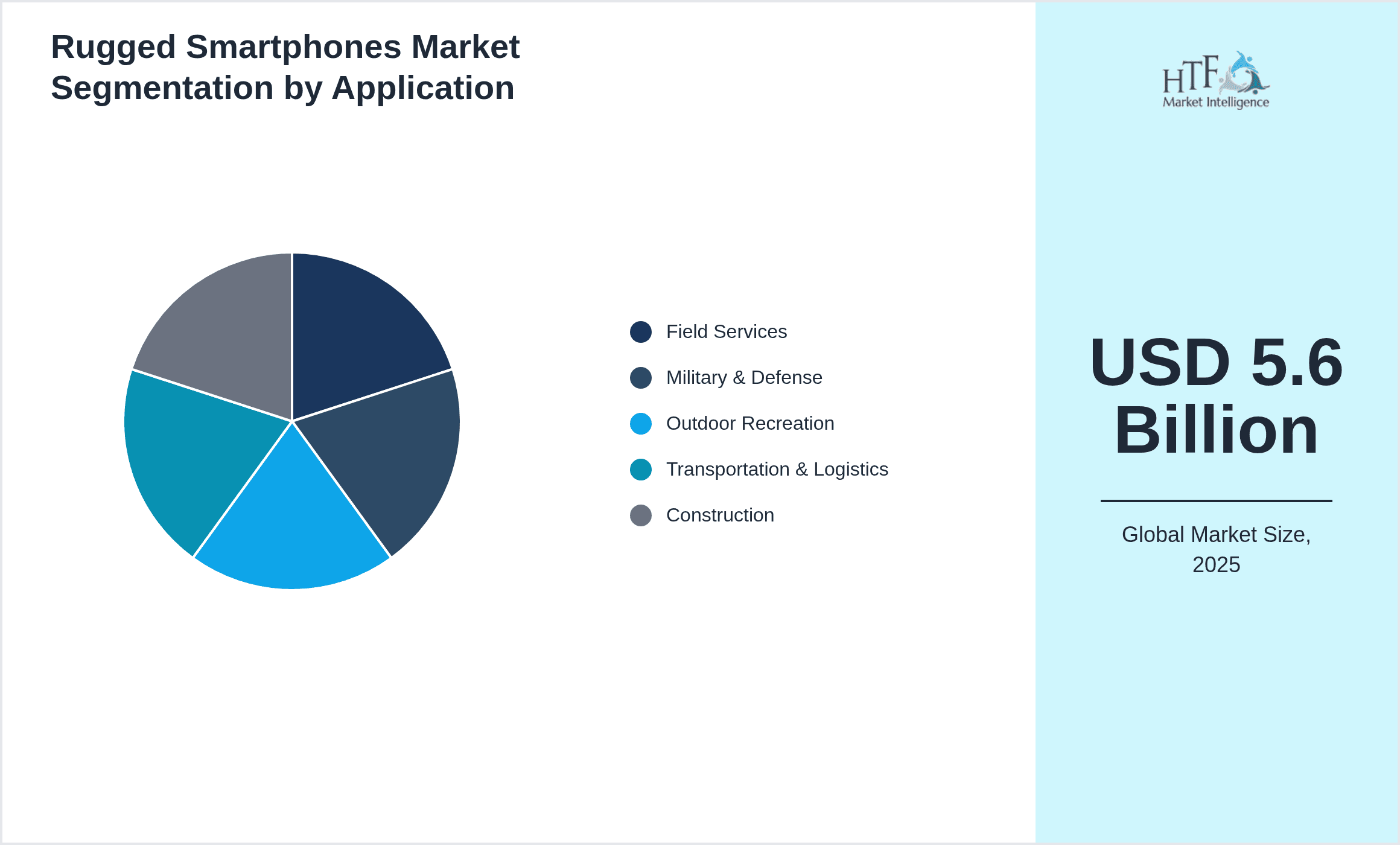

- •Market highlights include a projected CAGR of 11.05% from 2024 to 2034, with the market size expected to grow from USD 5.6 Billion in 2024 to USD 15.3 Billion by 2034. North America currently dominates the market, driven by advanced industrial sectors and military applications, while Asia-Pacific is the fastest-growing region due to increasing infrastructure projects and expanding outdoor industries. Waterproof smartphones lead the product segment, accounting for the largest revenue share, whereas freezeproof types are witnessing the fastest growth. Field services remain the dominant application area, complemented by rising usage in transportation and construction sectors. Innovations in rugged smartphone technology and strategic partnerships among key players are shaping competitive dynamics and market expansion.

- •The rugged smartphones market offers high value propositions to industries requiring durable communication devices that perform reliably under adverse conditions. For stakeholders including manufacturers, distributors, and end-users, the market delivers opportunities to leverage rugged technology advancements and meet stringent operational demands. The strategic importance lies in enabling uninterrupted communication in critical environments, reducing device replacement costs, and enhancing workforce productivity. Additionally, the market supports sustainability through devices designed for longevity and reduced electronic waste. Overall, rugged smartphones represent an essential technology segment with expanding relevance across defense, industrial, and consumer outdoor applications worldwide.

Competitive Landscape

The rugged smartphones market exhibits intense competition characterized by a blend of global technology leaders and specialized regional manufacturers. Companies focus on innovation in durability features, battery efficiency, and integration of advanced communication protocols to differentiate offerings. Market positioning hinges on product reliability, brand reputation, and technological advancements such as 5G connectivity and enhanced security features. Rivalry drives frequent product launches, strategic alliances, and investments in R&D to capture niche segments. Pricing strategies vary with premium models targeting military and industrial clients, while cost-effective solutions cater to emerging markets. Distribution networks and after-sales service quality are pivotal competitive factors, alongside adherence to international ruggedness standards. Market entry barriers include high development costs and certification requirements, preserving competitive advantages for established players. Future trends indicate increased consolidation through mergers and acquisitions, fostering market leadership and expanded geographic reach.

Leading Companies in Rugged Smartphones Market

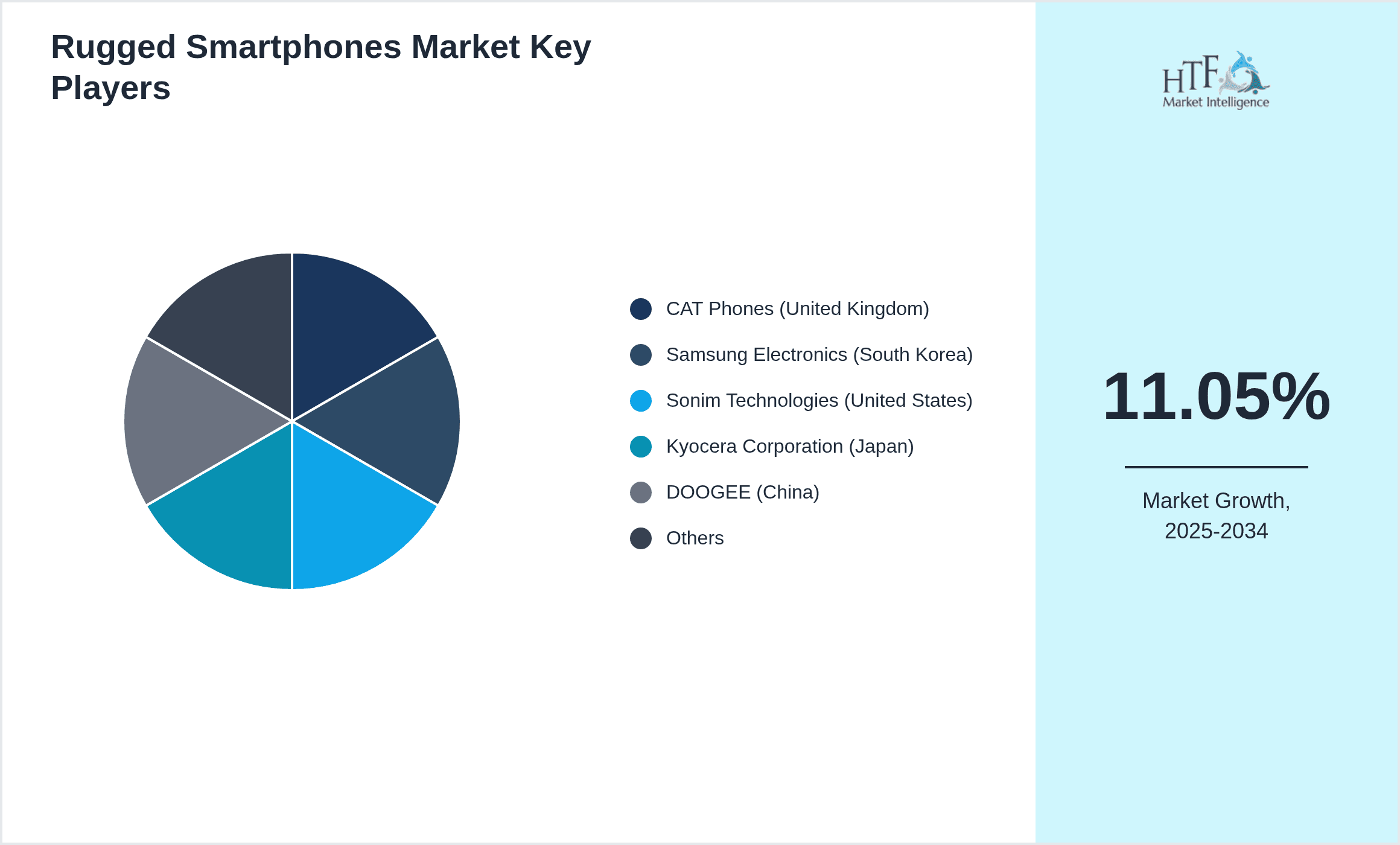

- •CAT Phones (United Kingdom)

- •Samsung Electronics (South Korea)

- •Sonim Technologies (United States)

- •Kyocera Corporation (Japan)

- •DOOGEE (China)

- •Blackview (China)

- •Ulefone (China)

- •AGM Global Vision (China)

- •RugGear (Hong Kong)

- •Unihertz (China)

- •Crosscall (France)

- •Ecom Instruments (Germany)

- •i.safe MOBILE (Germany)

- •Panasonic Corporation (Japan)

- •Bullitt Group (United Kingdom)

- •Honeywell International (United States)

- •Zebra Technologies (United States)

- •Kyocera Communication Systems (Japan)

- •CATL (China)

- •General Dynamics Mission Systems (United States)

- •Tough Mobile Solutions (Australia)

- •Archer Mobile (United States)

- •Sonim Technologies Europe (Germany)

- •Spice Mobility (India)

- •DOOGEE Europe (France)

Market Breakdown

- •By Product Type

- ◦Waterproof Rugged Smartphones

- ◦Shockproof Rugged Smartphones

- ◦Dustproof Rugged Smartphones

- ◦Freezeproof Rugged Smartphones

- ◦Other Rugged Smartphones

- •By Application

- ◦Field Services

- ◦Military & Defense

- ◦Outdoor Recreation

- ◦Transportation & Logistics

- ◦Construction

- •By End-Use Industry

- ◦Oil & Gas

- ◦Mining

- ◦Public Safety

- ◦Manufacturing

- •By Distribution Channel

- ◦Online Retail

- ◦Specialized Distributors

- ◦Direct Sales

Growth Dynamics

- •Rising demand for durable communication devices in harsh industrial and outdoor environments significantly drives market growth. Increasing infrastructure projects in emerging economies necessitate reliable smartphones that can endure extreme conditions, fueling sales globally.

- •Technological advancements such as integration of 5G connectivity, enhanced battery life, and improved rugged casing materials contribute to expanding application scope and adoption among professional users.

- •Government initiatives and defense spending focused on upgrading communication equipment boost demand, especially for military-grade rugged smartphones with specialized features.

- •Growth in outdoor recreational activities and sports increases consumer interest in rugged smartphones, expanding market penetration beyond industrial sectors.

- •Collaborations between smartphone manufacturers and software developers to provide custom solutions for field operations enhance product attractiveness and market differentiation.

- •Increasing awareness of total cost of ownership encourages enterprises to invest in rugged devices that reduce repair and replacement expenses over time.

- •Emerging markets in Asia-Pacific and Latin America present significant growth opportunities due to expanding construction, transportation, and mining industries requiring rugged communication tools.

Market Trends

- •The market is witnessing a trend toward multi-functional rugged smartphones combining durability with high-end features like AI-enabled cameras, biometric security, and enhanced user interfaces, catering to diverse user needs.

- •Sustainability is gaining importance, with manufacturers focusing on eco-friendly materials and longer device lifecycles to reduce environmental impact.

- •Adoption of modular designs allowing customization and easy repair is increasing, enabling users to upgrade specific components without replacing entire devices.

- •Integration of IoT and smart sensor technologies in rugged smartphones supports real-time data collection and monitoring for industrial applications, enhancing operational efficiencies.

- •Growing partnerships between rugged smartphone makers and telecom providers facilitate enhanced network coverage and service quality for end users in remote areas.

- •Shift towards online retail channels is accelerating due to convenience and wider product availability, impacting traditional distribution models.

- •Emergence of foldable and flexible display technologies adapted for rugged environments presents future innovation prospects.

Market Opportunities

- •Expansion into untapped emerging markets with growing industrialization offers substantial revenue potential for rugged smartphone manufacturers.

- •Development of specialized devices tailored for niche sectors such as emergency services and extreme sports can create new revenue streams.

- •Investment in R&D for integrating advanced technologies like augmented reality (AR) and virtual reality (VR) in rugged smartphones opens avenues for innovative applications.

- •Strategic alliances with software providers to deliver integrated communication and management solutions enhance product value proposition.

- •Leveraging government subsidies and defense contracts can accelerate market penetration and product adoption.

- •Rising consumer demand for rugged smartphones in outdoor recreation presents opportunities for targeted marketing and product diversification.

- •Adoption of e-commerce platforms for direct-to-consumer sales expands market reach and reduces distribution costs.

Market Challenges

- •High manufacturing costs and complex certification processes limit the entry of new players and restrict price competitiveness in some segments.

- •Rapid technological changes necessitate continuous innovation, imposing significant R&D expenses on market participants.

- •Limited consumer awareness in certain regions about rugged smartphones’ benefits hampers market expansion.

- •Competition from rugged smartphone alternatives like protective cases for conventional phones poses substitution threats.

- •Supply chain disruptions and raw material shortages can affect production schedules and product availability.

- •Balancing device ruggedness with user-friendly features remains a design challenge impacting customer satisfaction.

- •Navigating diverse regulatory standards across regions complicates product certification and market entry.

Regulatory Framework

- •Between 2019 and 2024, global regulatory agencies have enforced stricter standards related to environmental durability and safety certifications for rugged smartphones. Compliance with IP (Ingress Protection) ratings and MIL-STD-810G military standards became mandatory for devices marketed to defense and industrial sectors, ensuring reliability and user safety. These regulations have increased the emphasis on robust testing, impacting product design and manufacturing costs. In addition, data security regulations such as GDPR and CCPA have influenced the integration of secure communication features in rugged smartphones. Region-specific mandates, including FCC certification in North America and CE marking in Europe, require manufacturers to adhere to electromagnetic compatibility and wireless communication standards. Governments have also introduced incentives to promote rugged device adoption in public safety and emergency services, further shaping market dynamics.

- •Regulatory compliance has driven manufacturers to adopt transparent supply chains and sustainable materials to meet environmental directives, enhancing corporate responsibility and market acceptance.

- •Ongoing updates to wireless communication standards necessitate continuous product adaptation to maintain market eligibility and competitive advantage.

- •Certification timelines and costs remain a challenge, particularly for smaller manufacturers aiming at global market penetration.

- •Public safety communication regulations have led to specialized rugged smartphone features, such as push-to-talk functionality, being incorporated to meet emergency responder requirements.

Market Intelligence

- •15th January 2025, CAT Phones launched the CAT S63 rugged smartphone featuring enhanced thermal imaging capabilities and upgraded battery life designed for field service professionals operating in extreme conditions. The device incorporates advanced durability certifications including IP69 and MIL-STD-810H, making it suitable for military and industrial applications. This launch signifies CAT’s commitment to innovation and addressing specific user needs in demanding environments, strengthening its market position globally. The new model also integrates 5G connectivity, improving communication speed and reliability for end users. Source: Official CAT Phones website

- •10th March 2025, DOOGEE unveiled the DOOGEE V30 Pro, a freezeproof rugged smartphone targeting outdoor enthusiasts and extreme weather workers. The device offers a reinforced frame, ultra-low temperature battery performance, and advanced GPS tracking, enhancing operational safety and efficiency. The launch highlights growing consumer interest in specialized rugged smartphones supporting outdoor recreation and harsh climate applications. DOOGEE’s strategic focus on niche rugged types supports market diversification and competitive differentiation. Source: DOOGEE corporate press release

- •7th June 2024, Sonim Technologies announced a strategic partnership with a leading telecom provider to expand 5G network coverage for rugged smartphone users in remote industrial regions. This collaboration aims to enhance connectivity and service reliability for field operators and public safety officials. The initiative underscores the importance of integrated solutions combining rugged hardware and robust network infrastructure to meet evolving market demands. The partnership is expected to accelerate rugged smartphone adoption in underserved areas, offering new growth avenues. Source: Sonim Technologies press statement

- •22nd November 2024, Samsung Electronics released the Galaxy XCover Pro 2, an upgraded shockproof rugged smartphone featuring modular accessories and enhanced user interface tailored for logistics and transportation sectors. The device’s versatility and durability cater to enterprise needs for adaptable communication tools in dynamic work environments. Samsung’s focus on modularity and ease of repair addresses growing customer preferences for sustainable and customizable rugged smartphones. This product launch reinforces Samsung’s competitive stance in the rugged smartphone market. Source: Samsung Electronics official announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 5.6 Billion |

| Forecast Year Market Size | USD 15.3 Billion |

| CAGR | 11.05% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.53% |

| Scope of Report | Market is segmented by Product Type (Waterproof Rugged Smartphones, Shockproof Rugged Smartphones, Dustproof Rugged Smartphones, Freezeproof Rugged Smartphones, Other Rugged Smartphones), Application (Field Services, Military & Defense, Outdoor Recreation, Transportation & Logistics, Construction), End-Use Industry (Oil & Gas, Mining, Public Safety, Manufacturing), Distribution Channel (Online Retail, Specialized Distributors, Direct Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | CAT Phones (United Kingdom), Samsung Electronics (South Korea), Sonim Technologies (United States), Kyocera Corporation (Japan), DOOGEE (China), Blackview (China), Ulefone (China), AGM Global Vision (China), RugGear (Hong Kong), Unihertz (China), Crosscall (France), Ecom Instruments (Germany), i.safe MOBILE (Germany), Panasonic Corporation (Japan), Bullitt Group (United Kingdom), Honeywell International (United States), Zebra Technologies (United States), Kyocera Communication Systems (Japan), CATL (China), General Dynamics Mission Systems (United States), Tough Mobile Solutions (Australia), Archer Mobile (United States), Sonim Technologies Europe (Germany), Spice Mobility (India), DOOGEE Europe (France) |

Global Rugged Smartphones Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.