Global Gaming Consoles Market Size, Growth & Revenue 2024-2034

Global Gaming Consoles Market is segmented by Product Type (Home Consoles, Handheld Consoles, Hybrid Consoles, Microconsoles, Retro Consoles), Application (Home Gaming, Portable Gaming, Online Gaming, VR/AR Gaming, Esports), End-Use Industry (Consumer Entertainment, Esports and Competitive Gaming, Educational and Training, Virtual Reality Experiences), Distribution Channel (Offline Retail, Online Retail, Direct-to-Consumer Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global gaming consoles market is a dynamic sector involving the development and commercialization of electronic devices tailored for interactive gaming experiences. Spanning multiple console types such as home, handheld, hybrid, microconsoles, and retro consoles, the market serves diverse applications including home gaming, portable usage, online gaming, VR/AR immersion, and esports competitions. This market is characterized by rapid technological innovation, increasing consumer demand for high-quality gaming content, and widespread digital connectivity. Key players continuously invest in hardware enhancements, software compatibility, and ecosystem development to capture a broad user base globally. The market's growth is fueled by the rising popularity of immersive and competitive gaming formats, alongside expanding internet penetration and mobile device integration. Major regions such as North America, Europe, and Asia-Pacific dominate the market, with Asia-Pacific exhibiting the fastest growth due to rising gamer populations and technological adoption. This report provides a detailed analysis of market segmentation, competitive landscape, growth drivers, trends, challenges, and strategic opportunities projected over the next decade.

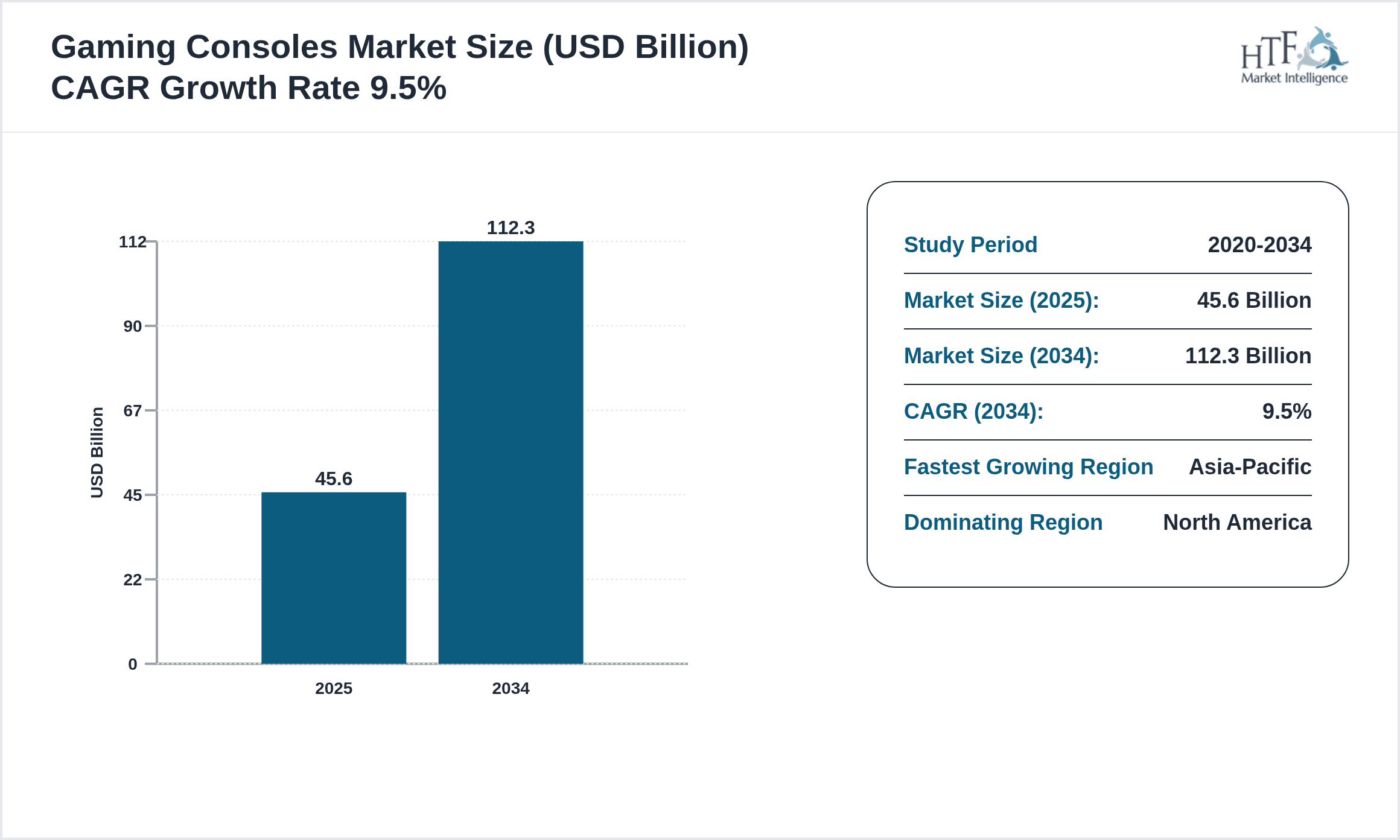

- •In 2024, the global gaming consoles market was valued at USD 45.6 billion and is forecasted to reach USD 112.3 billion by 2034, exhibiting a robust CAGR of 9.5%. The market is primarily driven by technological advancements such as hybrid consoles that combine portability with home gaming capabilities, and the integration of VR/AR technologies enhancing user engagement. North America leads in market size due to established gaming culture and advanced infrastructure, while Asia-Pacific is the fastest growing region owing to expanding middle-class consumers and increasing esports participation. Home consoles remain the dominant product type, with hybrid consoles following closely, reflecting shifting consumer preferences towards versatile gaming solutions. The market also benefits from increasing online gaming adoption and the surge in esports viewership, supporting new monetization models and content delivery mechanisms.

- •Gaming consoles hold strategic importance across entertainment, media, and technology industries, offering significant value to manufacturers, game developers, and content providers by enabling new revenue streams and user engagement metrics. The market's continuous innovation fosters ecosystem development involving hardware manufacturers, software publishers, and online service platforms, creating competitive advantages and broadening consumer reach. Stakeholders capitalize on rising demand for immersive gaming experiences, portability, and online connectivity by investing in next-generation consoles and cloud-based gaming. This growth supports ancillary sectors including digital content distribution, esports event management, and gaming accessories, underscoring the market's pivotal role in the digital entertainment economy globally.

Competitive Landscape

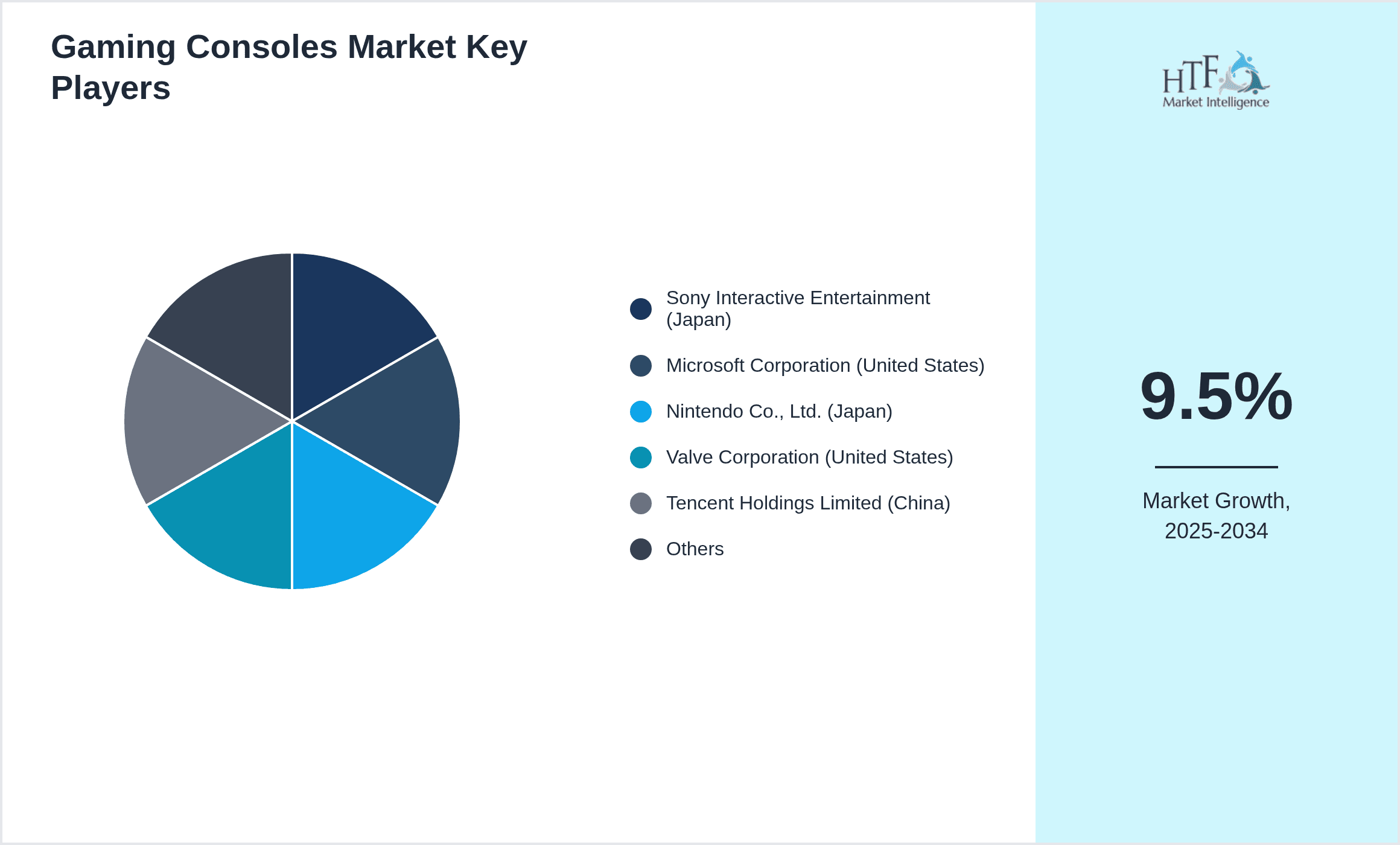

The global gaming consoles market is highly competitive, with leading companies adopting aggressive innovation strategies to maintain and grow their market positions. Competition centers on hardware performance, exclusive game titles, and ecosystem integration including online services and subscription models. Market players engage in continuous product development cycles to introduce cutting-edge consoles that support high-definition graphics, VR/AR capabilities, and hybrid functionalities. Strategic partnerships, mergers, and acquisitions are common to expand technological expertise and content libraries, enhancing customer retention. Pricing strategies vary to capture diverse consumer segments, from premium home consoles to affordable handheld devices. Regional competition is influenced by localized consumer preferences and regulatory frameworks, compelling companies to tailor offerings accordingly. The market's competitive dynamics are further shaped by rapid technological shifts and the emergence of cloud gaming platforms, which challenge traditional console paradigms and require adaptive approaches from industry players.

Leading Companies in Gaming Consoles Market

- •Sony Interactive Entertainment (Japan)

- •Microsoft Corporation (United States)

- •Nintendo Co., Ltd. (Japan)

- •Valve Corporation (United States)

- •Tencent Holdings Limited (China)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Google LLC (United States)

- •Amazon.com, Inc. (United States)

- •Razer Inc. (United States)

- •ASUStek Computer Inc. (Taiwan)

- •Mad Catz Global Limited (United States)

- •NVIDIA Corporation (United States)

- •Apple Inc. (United States)

- •Sony Corporation (Japan)

- •Logitech International S.A. (Switzerland)

- •Corsair Gaming, Inc. (United States)

- •SteelSeries ApS (Denmark)

- •Ubisoft Entertainment SA (France)

- •Electronic Arts Inc. (United States)

- •Activision Blizzard, Inc. (United States)

- •Capcom Co., Ltd. (Japan)

- •Bandai Namco Holdings Inc. (Japan)

- •Sega Corporation (Japan)

- •Zynga Inc. (United States)

- •Epic Games, Inc. (United States)

Market Breakdown

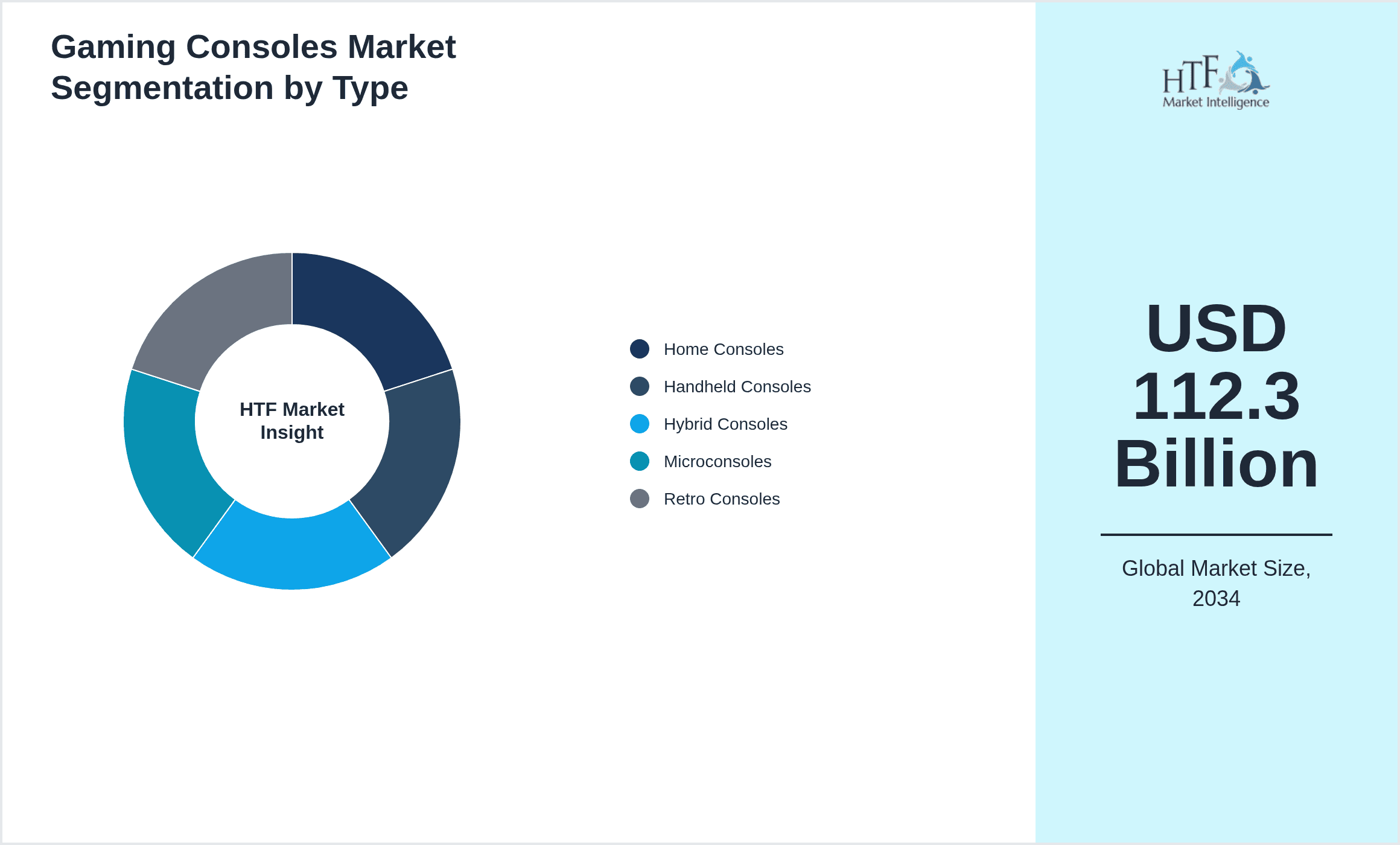

- •By Product Type

- ◦Home Consoles

- ◦Handheld Consoles

- ◦Hybrid Consoles

- ◦Microconsoles

- ◦Retro Consoles

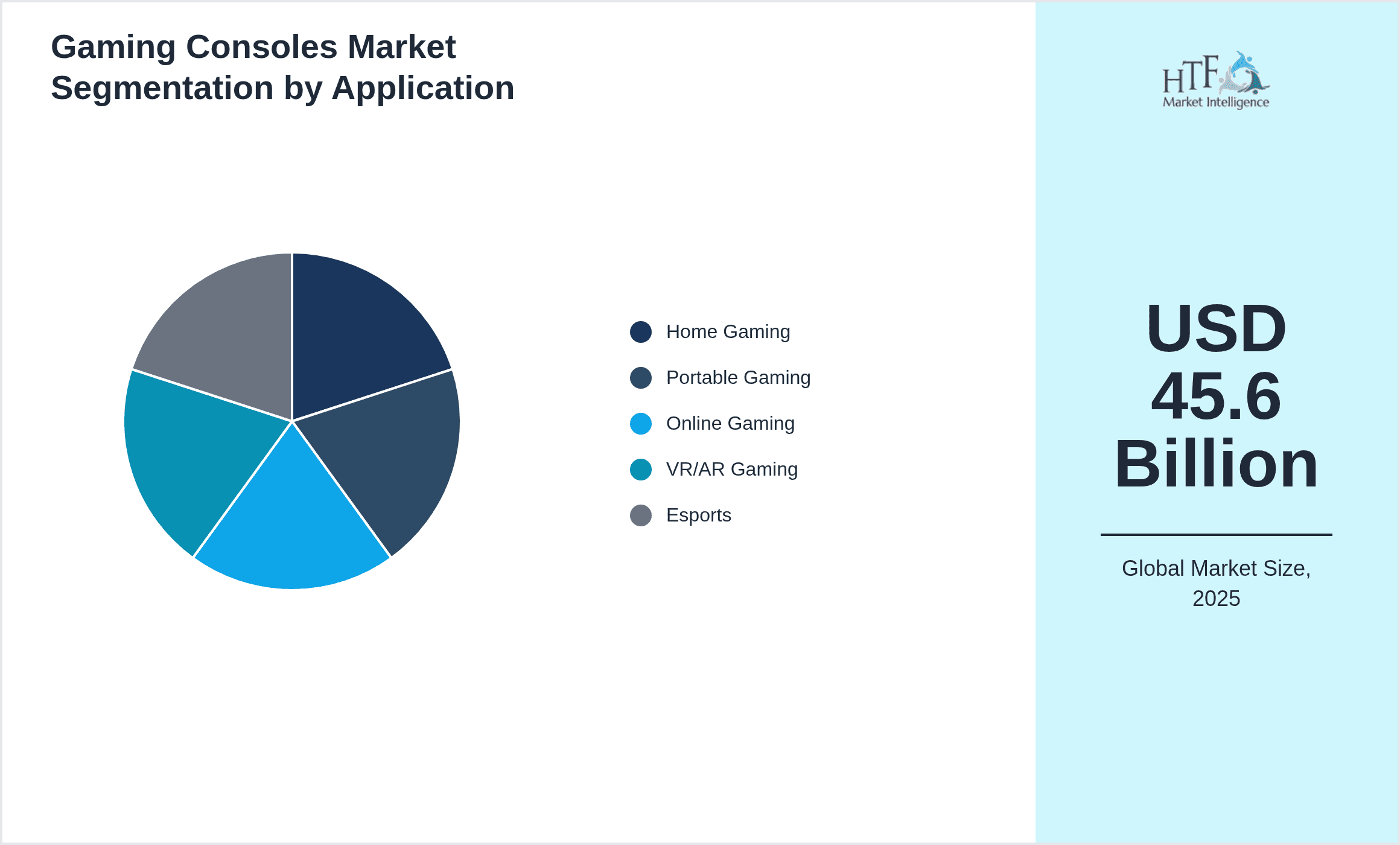

- •By Application

- ◦Home Gaming

- ◦Portable Gaming

- ◦Online Gaming

- ◦VR/AR Gaming

- ◦Esports

- •By End-Use Industry

- ◦Consumer Entertainment

- ◦Esports and Competitive Gaming

- ◦Educational and Training

- ◦Virtual Reality Experiences

- •By Distribution Channel

- ◦Offline Retail

- ◦Online Retail

- ◦Direct-to-Consumer Platforms

Growth Dynamics

- •The rising adoption of hybrid consoles that offer both portable and home gaming experiences is significantly driving market expansion. Consumers increasingly prefer devices that enable seamless transition between different modes, enhancing usability and engagement.

- •Technological advancements such as integration of VR and AR are expanding gaming functionality, attracting new user segments and creating immersive experiences that stimulate market growth.

- •The growth of esports as a mainstream entertainment form is boosting demand for high-performance gaming consoles designed for competitive play, fueling sales and innovation.

- •Increasing internet penetration and digital infrastructure improvements worldwide facilitate online gaming and content streaming, supporting market uptake of connected gaming consoles.

- •Strategic partnerships between console manufacturers and game developers enable exclusive titles and bundled offerings, enhancing product appeal and driving consumer loyalty.

- •Rising disposable incomes and expanding middle-class populations in emerging markets, particularly in Asia-Pacific and Latin America, are creating new growth opportunities for gaming consoles.

- •The expansion of subscription-based gaming services integrated with consoles is transforming revenue models and encouraging higher market penetration among casual and hardcore gamers alike.

Market Trends

- •The market is witnessing a shift towards cloud gaming integration, allowing consoles to stream high-quality games without reliance on extensive local hardware, thereby lowering entry barriers.

- •Sustainability is emerging as a key focus, with manufacturers adopting eco-friendly materials and energy-efficient designs to meet regulatory standards and consumer expectations.

- •Customization and modular console designs are gaining popularity, enabling users to upgrade components and personalize aesthetics, enhancing user engagement and product lifespan.

- •Cross-platform compatibility is increasingly demanded, allowing gamers to play titles seamlessly across consoles, PCs, and mobile devices, driving ecosystem expansion.

- •Esports sponsorship and integration with gaming consoles are intensifying, fueling brand visibility and influencing console design to meet competitive gaming standards.

- •Emerging markets are witnessing localized content and regionalized marketing strategies from manufacturers to capture diverse gaming cultures and preferences.

- •Artificial intelligence enhancements are being embedded within consoles for adaptive gameplay, personalized experiences, and improved system performance.

Market Opportunities

- •Developing cloud-based gaming platforms integrated with consoles presents significant growth potential by reducing hardware costs and expanding accessibility to high-end games.

- •Expanding esports infrastructure globally creates opportunities for consoles optimized for competitive performance, tapping into a rapidly growing audience and revenue stream.

- •Innovations in VR/AR gaming accessories and content offer pathways for consoles to deliver unique immersive experiences, attracting new consumer segments.

- •Penetrating emerging markets through affordable console variants and localized content can unlock considerable market expansion and brand loyalty.

- •Collaborations between console manufacturers and content creators for exclusive titles can drive product differentiation and consumer demand.

- •Subscription-based models and digital marketplaces integrated with consoles offer recurring revenue opportunities and enhanced customer retention.

- •Adoption of sustainable manufacturing practices can position companies favorably amid increasing regulatory and consumer focus on environmental responsibility.

Market Challenges

- •High production costs of advanced consoles incorporating VR/AR and hybrid technologies limit accessibility for price-sensitive consumer segments, constraining market penetration.

- •Rapid technological obsolescence demands continuous R&D investment, imposing financial strain on manufacturers and complicating inventory management.

- •Complex regulatory landscapes across countries related to digital content, privacy, and online gaming create compliance challenges for global console distributors.

- •Intense competition from mobile and PC gaming platforms offering flexible and cost-effective alternatives pressures console market growth.

- •Supply chain disruptions and component shortages, especially semiconductors, hamper manufacturing schedules and product availability.

- •Piracy and unauthorized software pose risks to revenue and intellectual property, requiring robust security measures and enforcement.

- •Balancing innovation with backward compatibility and legacy support remains a technical and strategic challenge for developers and manufacturers.

Regulatory Framework

- •Between 2019 and 2024, several regions implemented digital content protection regulations requiring enhanced DRM (Digital Rights Management) compliance for gaming consoles, impacting software development and licensing agreements.

- •The European Union introduced stricter data privacy laws affecting online gaming features on consoles, mandating transparent user data handling and consent protocols.

- •North American regulatory bodies updated consumer protection guidelines to address in-game purchases and loot box mechanics, influencing console platform policies and parental controls.

- •China enforced cybersecurity standards for gaming devices that require manufacturers to integrate content filtering and age verification systems, affecting hardware and software design.

- •Government incentives promoting sustainable electronics manufacturing have encouraged console producers to adopt eco-friendly materials and energy-efficient technologies since 2022.

Market Intelligence

- •15th January 2025, Sony Interactive Entertainment launched the PlayStation 6, featuring next-generation VR integration, ultra-fast SSD storage, and backward compatibility with previous generations. The new console targets enhanced immersive gaming and streamlined online experiences, aiming to consolidate Sony's leadership in home consoles. The launch includes exclusive game titles and subscription service enhancements, aligning with evolving consumer preferences for hybrid gaming. This strategic release is expected to significantly boost market growth in North America and Europe. Source: Sony Official Press Release

- •10th March 2025, Microsoft Corporation introduced an upgraded Xbox Series X+ model optimized for cloud gaming with enhanced AI-driven graphics rendering. The device supports seamless integration with Xbox Game Pass and expands accessibility across online platforms. Microsoft’s investment in hybrid console technology and subscription services reflects its focus on competitive esports and online community building. This innovation is poised to capture increasing market share in the Asia-Pacific region. Source: Microsoft Newsroom

- •22nd February 2025, Nintendo Co., Ltd. announced a strategic partnership with a leading VR technology firm to develop immersive gaming content for its Switch hybrid console. This collaboration aims to blend portable gaming with virtual reality experiences, targeting younger demographics and esports enthusiasts. The initiative includes exclusive titles and augmented reality features designed to enhance user engagement and diversify Nintendo’s product portfolio. This move is expected to drive growth in emerging markets such as Latin America and Southeast Asia. Source: Nintendo Corporate Announcement

- •5th April 2025, Valve Corporation expanded its Steam Deck handheld console lineup with a new model incorporating improved battery life, higher processing power, and expanded game compatibility. The upgrade focuses on portability and online gaming capabilities to meet growing consumer demand for versatile devices. Valve’s innovations support the increasing trend of cross-platform gaming and cloud streaming, further intensifying competition in the hybrid console segment. This launch is anticipated to strengthen Valve’s position in North America and Europe. Source: Valve Official Blog

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.6 Billion |

| Forecast Year Market Size | USD 112.3 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Scope of Report | Market is segmented by Product Type (Home Consoles, Handheld Consoles, Hybrid Consoles, Microconsoles, Retro Consoles), Application (Home Gaming, Portable Gaming, Online Gaming, VR/AR Gaming, Esports), End-Use Industry (Consumer Entertainment, Esports and Competitive Gaming, Educational and Training, Virtual Reality Experiences), Distribution Channel (Offline Retail, Online Retail, Direct-to-Consumer Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Sony Interactive Entertainment (Japan), Microsoft Corporation (United States), Nintendo Co., Ltd. (Japan), Valve Corporation (United States), Tencent Holdings Limited (China), Samsung Electronics Co., Ltd. (South Korea), Google LLC (United States), Amazon.com, Inc. (United States), Razer Inc. (United States), ASUStek Computer Inc. (Taiwan), Mad Catz Global Limited (United States), NVIDIA Corporation (United States), Apple Inc. (United States), Sony Corporation (Japan), Logitech International S.A. (Switzerland), Corsair Gaming, Inc. (United States), SteelSeries ApS (Denmark), Ubisoft Entertainment SA (France), Electronic Arts Inc. (United States), Activision Blizzard, Inc. (United States), Capcom Co., Ltd. (Japan), Bandai Namco Holdings Inc. (Japan), Sega Corporation (Japan), Zynga Inc. (United States), Epic Games, Inc. (United States) |

Global Gaming Consoles Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.