Global Automated Drilling Systems Market Size, Growth & Revenue 2024-2034

Global Automated Drilling Systems Market is segmented by Product Type (Fully Automated Systems, Semi-Automated Systems, Remote-Controlled Systems, Robotic Drilling Systems, Hybrid Systems), Application (Oil & Gas Exploration, Mining, Construction, Geothermal Drilling, Water Well Drilling), End-Use Industry (Energy, Mining & Minerals, Construction & Infrastructure, Water Resource Management), Distribution Channel (Direct Sales, Distributors & Dealers, Aftermarket Services), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Automated Drilling Systems market represents a transformative sector that integrates cutting-edge automation technologies to streamline drilling operations across multiple industries including oil & gas, mining, construction, geothermal, and water well drilling. This market covers a broad spectrum of drilling solutions ranging from fully automated and semi-automated systems to remote-controlled, robotic, and hybrid configurations. These systems are designed to enhance operational efficiency, precision, and safety while minimizing human error and environmental impact. As industries face increasing demands for cost reduction, improved productivity, and compliance with stringent safety regulations, the adoption of automated drilling technologies has accelerated globally. The market’s scope includes hardware components, software platforms enabling real-time data analytics and control, and services for maintenance and system integration. Key applications span from upstream oil and gas exploration to deep mining and geothermal energy extraction. The global market is characterized by rapid innovation, with significant investments in AI, IoT, and robotics to advance drilling automation capabilities and expand applicability across diverse geographies and challenging environments.

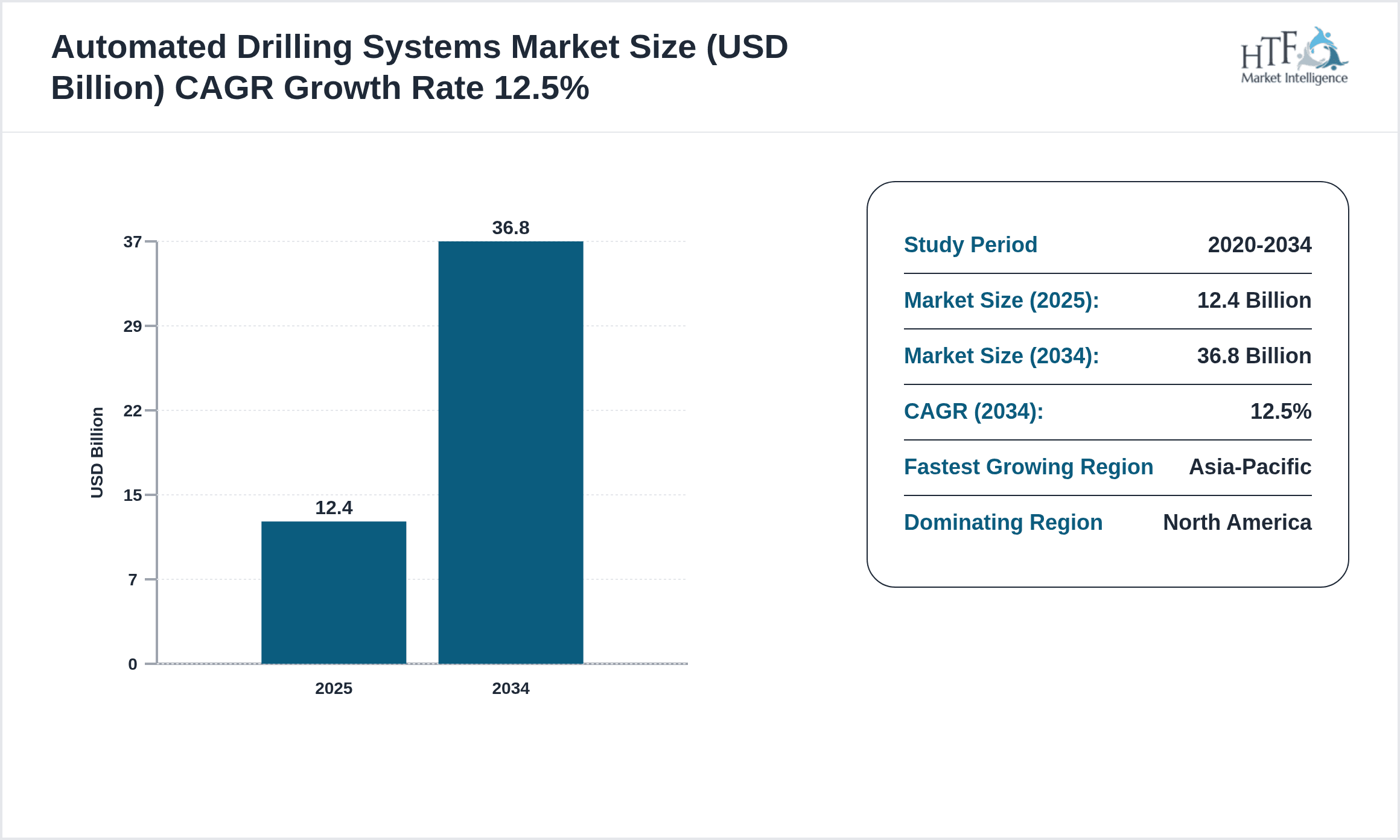

- •Market highlights reveal a robust growth trajectory driven by rising demand for operational efficiency and safety in hazardous drilling environments. The market size stood at USD 12.4 Billion in 2025 and is forecasted to reach USD 36.8 Billion by 2034, exhibiting a CAGR of 12.5%. Key regions such as North America dominate market revenues owing to mature infrastructure and technology adoption, while Asia-Pacific is the fastest-growing region propelled by expanding mining and energy sectors. Fully automated systems lead product adoption due to their comprehensive control capabilities, whereas robotic drilling systems represent the fastest-growing segment fueled by advancements in robotics and AI integration. Application-wise, oil & gas exploration holds the largest market share, followed by mining, reflecting ongoing global energy needs and mineral extraction activities.

- •The market’s strategic importance is underscored by its ability to revolutionize drilling processes, reduce operational risks, and enable data-driven decision-making. Automated drilling systems enable stakeholders—from equipment manufacturers to end-users in oil, mining, and construction sectors—to optimize resource utilization, minimize downtime, and comply with environmental standards. The integration of advanced sensors, AI-driven analytics, and remote operation capabilities offers competitive advantages in cost-effectiveness and safety enhancements. Investment in automated drilling technology also aligns with global sustainability goals by reducing emissions through improved precision and efficiency. Consequently, this market serves as a critical enabler for the energy transition, infrastructure development, and resource security worldwide, fostering innovation and collaboration among technology providers, industrial operators, and regulatory bodies.

Competitive Landscape

The global Automated Drilling Systems market is characterized by intense competition among established multinational corporations and emerging technology firms. Market players focus on innovation-driven strategies, including continuous R&D investments in robotics, AI, and IoT-integrated solutions to achieve superior drilling precision and operational efficiency. Competitive dynamics also revolve around strategic partnerships, technology licensing, and collaborations with drilling contractors and end-users to co-develop tailored systems addressing specific industrial needs. Companies differentiate through proprietary software platforms offering real-time analytics, remote monitoring, and predictive maintenance capabilities. Pricing strategies vary from premium advanced system offerings to cost-effective modular solutions catering to diverse market segments. Market entry barriers include high capital expenditure requirements, stringent regulatory compliance, and the necessity for robust after-sales services and training. Regional competition is notable, with North American and European firms dominating technologically advanced segments, while Asia-Pacific players are rapidly expanding through localized manufacturing and service networks. Future trends indicate consolidation via mergers and acquisitions alongside increased focus on sustainable and digital-enabled drilling technologies.

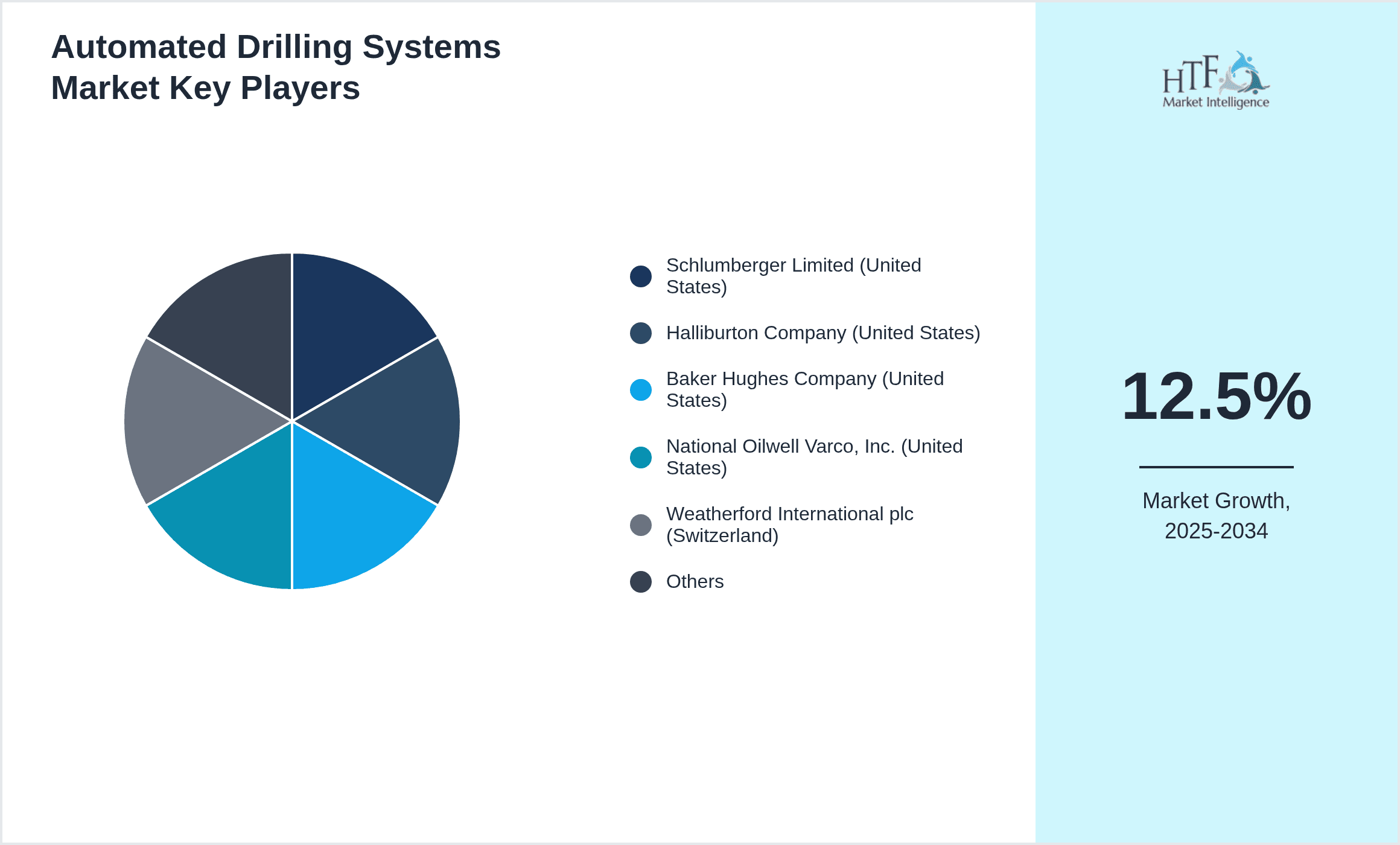

Major Automated Drilling Systems Industry Players

- •Schlumberger Limited (United States)

- •Halliburton Company (United States)

- •Baker Hughes Company (United States)

- •National Oilwell Varco, Inc. (United States)

- •Weatherford International plc (Switzerland)

- •FMC Technologies, Inc. (United States)

- •Atlas Copco AB (Sweden)

- •Sandvik AB (Sweden)

- •Komatsu Ltd. (Japan)

- •Caterpillar Inc. (United States)

- •Geoservices Group (France)

- •NOV Grant Prideco (United States)

- •FAMUR Group (Poland)

- •Furukawa Rock Drill Co., Ltd. (Japan)

- •Herrenknecht AG (Germany)

- •Epiroc AB (Sweden)

- •Dando Drilling International (United Kingdom)

- •Geotec S.A. (Brazil)

- •Sandvik Mining and Rock Technology (Sweden)

- •KOMATSU Mining Corp. (Japan)

- •Acteon Group (United Kingdom)

- •Boart Longyear (United States)

- •Trelleborg AB (Sweden)

- •Husqvarna AB (Sweden)

- •Fugro N.V. (Netherlands)

Market Breakdown

- •By Product Type

- ◦Fully Automated Systems

- ◦Semi-Automated Systems

- ◦Remote-Controlled Systems

- ◦Robotic Drilling Systems

- ◦Hybrid Systems

- •By Application

- ◦Oil & Gas Exploration

- ◦Mining

- ◦Construction

- ◦Geothermal Drilling

- ◦Water Well Drilling

- •By End-Use Industry

- ◦Energy

- ◦Mining & Minerals

- ◦Construction & Infrastructure

- ◦Water Resource Management

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Dealers

- ◦Aftermarket Services

Growth Dynamics

- •The Automated Drilling Systems market experiences strong growth driven primarily by the increasing demand for enhanced operational efficiency and safety in drilling activities. Industries such as oil & gas and mining face challenges of complex terrains and hazardous environments where automation reduces human exposure to risks. Additionally, the integration of AI and IoT technologies has enabled predictive maintenance and real-time analytics, optimizing drilling performance and reducing downtime. Government initiatives promoting digital transformation and environmental compliance further accelerate technology adoption. Expanding infrastructure projects worldwide fuel the demand for advanced drilling solutions, especially in developing regions. Together, these factors create a favorable environment for rapid market expansion and technological innovation.

- •Advancements in robotic drilling and remote operation capabilities are reshaping market growth by enabling drilling in previously inaccessible or dangerous locations. The development of hybrid systems combining manual and automated controls offers flexibility for varied operational requirements, encouraging adoption across diverse industries. Increasing focus on reducing carbon footprint and minimizing environmental impact drives investment in precision drilling technologies that enhance resource efficiency. Furthermore, the rising trend of digital twin technology allows operators to simulate drilling processes, improving planning and execution. These technological trends collectively boost market growth and create new avenues for product development and service offerings.

- •Despite positive growth trends, market expansion faces challenges including high initial capital expenditure and integration complexities with legacy infrastructure. Technical limitations related to system interoperability and the need for skilled personnel to manage sophisticated automated platforms may restrain adoption, particularly among smaller operators. Regulatory uncertainties and evolving safety standards require continuous compliance efforts, increasing operational costs. Furthermore, market penetration in emerging economies is hindered by lack of infrastructure and technology awareness, slowing growth velocity. These restraints necessitate innovation in cost-effective automation solutions and comprehensive training programs to broaden market accessibility.

- •Significant opportunities arise from untapped markets in Asia-Pacific and Latin America where expanding mining and energy sectors seek modernization. The growing demand for geothermal energy and water well drilling in sustainable resource management presents new application areas for automated systems. Collaborations between technology providers and industrial operators to co-develop customized solutions offer potential for market differentiation. Additionally, the integration of cloud computing and edge analytics facilitates remote monitoring and control, enabling service-based business models and recurring revenue streams. Investment in product innovation focused on modularity and scalability can capture emerging customer segments and accelerate global adoption.

- •Market challenges include managing the complexity of integrating automated systems into diverse operational environments with varying regulatory frameworks. Cybersecurity risks associated with connected drilling platforms necessitate robust data protection measures, adding to development costs. Competition from low-cost manual drilling alternatives in cost-sensitive markets limits growth potential. Additionally, fluctuating commodity prices impact capital expenditure budgets of end-users, affecting procurement cycles. Addressing these challenges requires strategic investments in product reliability, cybersecurity, and cost optimization alongside proactive engagement with regulatory authorities to shape favorable policies.

Market Trends

- •The global Automated Drilling Systems market is witnessing a surge in adoption of AI and machine learning algorithms that enable autonomous decision-making and adaptive drilling strategies. Companies are increasingly deploying advanced sensor arrays and real-time data analytics to optimize drilling parameters dynamically, leading to enhanced precision and reduced wear on equipment. This trend is supported by growing investments in digital transformation initiatives within oil & gas and mining industries to improve operational transparency and reduce costs.

- •Robotic drilling platforms equipped with remote control and teleoperation features are gaining traction, allowing operators to manage drilling processes from safe, off-site locations. This innovation not only improves safety but also enables continuous operations in harsh or inaccessible environments. The integration of augmented reality (AR) for operator training and field support is further enhancing system usability and maintenance efficiency.

- •Sustainability-driven trends are influencing product development, with manufacturers focusing on energy-efficient drilling systems that lower fuel consumption and emissions. The deployment of hybrid automated systems combining electric and diesel power sources reflects the industry's commitment to environmental stewardship. Strategic partnerships between drilling system providers and renewable energy companies are emerging to address geothermal drilling demands.

- •Digital twin technology is becoming increasingly prevalent, enabling virtual simulations of drilling operations to predict outcomes and optimize processes before onsite execution. This digital replication facilitates scenario analysis, risk management, and cost control, providing competitive advantages to early adopters. Additionally, cloud-based platforms enhance data accessibility and collaboration across global operations.

- •The market is also witnessing consolidation as key players engage in mergers and acquisitions to expand technological capabilities and geographic presence. Collaborative ecosystems involving equipment manufacturers, software developers, and service providers are fostering innovation and comprehensive solution offerings. This collaborative trend is accelerating the development of integrated drilling automation ecosystems, enhancing customer value propositions.

Market Opportunities

- •Expanding infrastructure development initiatives in emerging economies present significant growth opportunities for automated drilling system providers. These regions require modern drilling technologies to support mining, construction, and energy projects, creating demand for scalable and cost-effective automation solutions. Market players can capitalize on this by establishing local partnerships and adapting products to regional operational conditions.

- •The increasing global emphasis on sustainable resource extraction and environmental conservation opens avenues for deploying precision automated drilling technologies that minimize ecological impact. Innovations in low-emission drilling systems and real-time environmental monitoring can attract clients focused on regulatory compliance and corporate social responsibility.

- •Integration of IoT and cloud computing into drilling systems enables new service models such as equipment-as-a-service and predictive maintenance subscriptions, offering recurring revenue streams and closer customer engagement. Providers focusing on these digital service offerings can differentiate themselves and build long-term client relationships.

- •Technological advancements in AI, robotics, and sensor technologies create opportunities for developing next-generation drilling systems capable of fully autonomous operations in complex environments. Early investment in such innovations can secure competitive advantages and market leadership in future automation waves.

- •Geothermal energy exploration and water resource management are emerging application areas where automated drilling can provide operational efficiency and safety benefits. Market entrants targeting these niche segments can leverage specialized expertise to capture untapped demand and diversify revenue sources.

Market Challenges

- •High upfront capital investment required for automated drilling systems remains a barrier for small and medium-sized enterprises, limiting widespread adoption in cost-sensitive markets. The complexity of system integration with existing infrastructure further escalates implementation costs and operational risks.

- •The need for skilled workforce to operate and maintain sophisticated automated drilling platforms presents a significant challenge, especially in regions with limited technical training and education facilities. This skill gap hampers market penetration and operational effectiveness.

- •Evolving regulatory requirements across different jurisdictions create compliance complexities for manufacturers and operators, necessitating continuous adaptation of system designs and operational protocols. Non-compliance risks can lead to financial penalties and reputational damage.

- •Cybersecurity threats targeting connected drilling systems pose risks to data integrity and operational continuity. Addressing these vulnerabilities demands substantial investments in security architectures and ongoing monitoring, increasing total cost of ownership.

- •Volatility in commodity prices influences capital expenditure budgets of end-users, potentially delaying or reducing investments in advanced automated drilling technologies. Market players must navigate these economic uncertainties by offering flexible financing and scalable solutions.

Regulatory Framework

- •Between 2020 and 2025, several countries implemented stringent safety and environmental regulations impacting automated drilling systems. These include mandatory compliance with international standards for equipment operation and emissions control, requiring manufacturers to enhance system reliability and reduce ecological footprint.

- •Regulations mandating real-time monitoring and reporting of drilling activities have been enforced globally, compelling system providers to integrate advanced sensor and communication technologies. These measures aim to improve transparency and risk management in drilling operations.

- •Data protection and cybersecurity regulations specific to industrial control systems have emerged, obliging companies to adopt robust security protocols to safeguard automated drilling platforms against cyber threats and unauthorized access.

- •Region-specific mandates in North America and Europe require automated systems to comply with occupational health and safety standards, including operator training certifications and emergency response capabilities, influencing system design and service offerings.

- •Government incentive programs promoting digital transformation and sustainable technologies in mining and energy sectors have been introduced, providing financial support and tax benefits for adoption of automated drilling solutions, thereby accelerating market growth.

Market Intelligence

- •15th January 2025, Schlumberger Limited launched the 'AutoDrill X' system featuring enhanced AI-powered drilling automation and integrated IoT connectivity. This advanced platform enables real-time data analytics and adaptive control algorithms to optimize drilling speed and accuracy, targeting oil & gas exploration markets globally. The product aims to reduce operational costs and improve safety by minimizing human intervention in hazardous environments. This launch reinforces Schlumberger’s leadership position and commitment to digital transformation in drilling technologies. Source: Official Schlumberger press release

- •3rd March 2025, Baker Hughes Company introduced a new robotic drilling rig equipped with remote operation capabilities and augmented reality support for field technicians. This innovation enhances drilling precision and allows operators to monitor and control operations from offsite locations, significantly improving safety and operational uptime. The system integrates predictive maintenance features leveraging machine learning to anticipate equipment failures. This product rollout targets mining and geothermal drilling segments, expanding Baker Hughes’ market reach. Source: Baker Hughes corporate announcement

- •22nd July 2024, Halliburton Company announced a strategic partnership with Epiroc AB to co-develop hybrid automated drilling systems combining Halliburton’s software expertise and Epiroc’s robotic hardware technology. The collaboration aims to create modular solutions adaptable to various drilling environments, enhancing flexibility and cost-effectiveness. This alliance is expected to accelerate innovation cycles and strengthen competitive positioning in global markets, particularly in Asia-Pacific and Latin America.

- •10th November 2024, Atlas Copco AB completed the acquisition of Dando Drilling International to broaden its portfolio in water well drilling automation. This acquisition enables Atlas Copco to offer comprehensive automated solutions tailored to water resource management and environmental drilling applications, tapping into emerging markets focused on sustainable development. The integration is projected to enhance service capabilities and drive revenue growth in the automated drilling systems market. Source: Atlas Copco official news release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.4 Billion |

| Forecast Year Market Size | USD 36.8 Billion |

| CAGR | 12.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.1% |

| Scope of Report | Market is segmented by Product Type (Fully Automated Systems, Semi-Automated Systems, Remote-Controlled Systems, Robotic Drilling Systems, Hybrid Systems), Application (Oil & Gas Exploration, Mining, Construction, Geothermal Drilling, Water Well Drilling), End-Use Industry (Energy, Mining & Minerals, Construction & Infrastructure, Water Resource Management), Distribution Channel (Direct Sales, Distributors & Dealers, Aftermarket Services) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Schlumberger Limited (United States), Halliburton Company (United States), Baker Hughes Company (United States), National Oilwell Varco, Inc. (United States), Weatherford International plc (Switzerland), FMC Technologies, Inc. (United States), Atlas Copco AB (Sweden), Sandvik AB (Sweden), Komatsu Ltd. (Japan), Caterpillar Inc. (United States), Geoservices Group (France), NOV Grant Prideco (United States), FAMUR Group (Poland), Furukawa Rock Drill Co., Ltd. (Japan), Herrenknecht AG (Germany), Epiroc AB (Sweden), Dando Drilling International (United Kingdom), Geotec S.A. (Brazil), Sandvik Mining and Rock Technology (Sweden), KOMATSU Mining Corp. (Japan), Acteon Group (United Kingdom), Boart Longyear (United States), Trelleborg AB (Sweden), Husqvarna AB (Sweden), Fugro N.V. (Netherlands) |

Global Automated Drilling Systems Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.