Global Leather Goods Market Size, Growth & Revenue 2024-2034

Global Leather Goods Market is segmented by Product Type (Genuine Leather, Synthetic Leather, Suede Leather, Nubuck Leather, Patent Leather), Application (Handbags, Footwear, Wallets, Belts, Accessories), End-Use Industry (Fashion & Apparel, Luxury Goods, Automotive Interiors, Sports & Leisure), Distribution Channel (Retail Stores, E-commerce, Wholesale), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

The Global Leather Goods market is a dynamic and diverse industry that includes products made from various leather types such as genuine, synthetic, suede, nubuck, and patent leather. It serves a wide array of applications including handbags, footwear, wallets, belts, and accessories. The market is characterized by its integration of traditional craftsmanship and modern technology, catering to fashion-conscious consumers globally. Key growth drivers include rising disposable incomes, increasing demand for premium and sustainable leather products, and expanding e-commerce platforms enabling wider reach. Geographically, North America dominates due to strong luxury brand presence and high consumer spending, while Asia-Pacific is the fastest-growing region fueled by urbanization and rising middle-class populations. The market faces challenges such as fluctuating raw material costs and stringent environmental regulations. However, opportunities abound in innovative product development, sustainable leather alternatives, and emerging markets. Strategic importance extends to fashion, automotive, and lifestyle sectors, making this market crucial for stakeholders aiming for long-term value.

Competitive Landscape

The competitive environment in the Global Leather Goods market is marked by intense rivalry among established luxury brands and emerging manufacturers focusing on innovation and sustainability. Companies compete on product quality, brand heritage, and design innovation, while also leveraging strategic partnerships and digital transformation to enhance market reach. Innovation in eco-friendly leather processing and synthetic alternatives is a significant competitive factor, as consumers increasingly demand sustainable products. Market leaders adopt diverse pricing strategies and omnichannel distribution to cater to both premium and mass markets. The industry experiences continuous M&A activities to consolidate market share and expand geographic presence. Barriers to entry include high capital investment, skilled craftsmanship requirements, and compliance with environmental regulations. Regional competition varies, with North America and Europe leading in luxury segments, while Asia-Pacific offers volume growth opportunities. Future competitiveness will hinge on agility in adapting to consumer trends and integrating technology with craftsmanship.

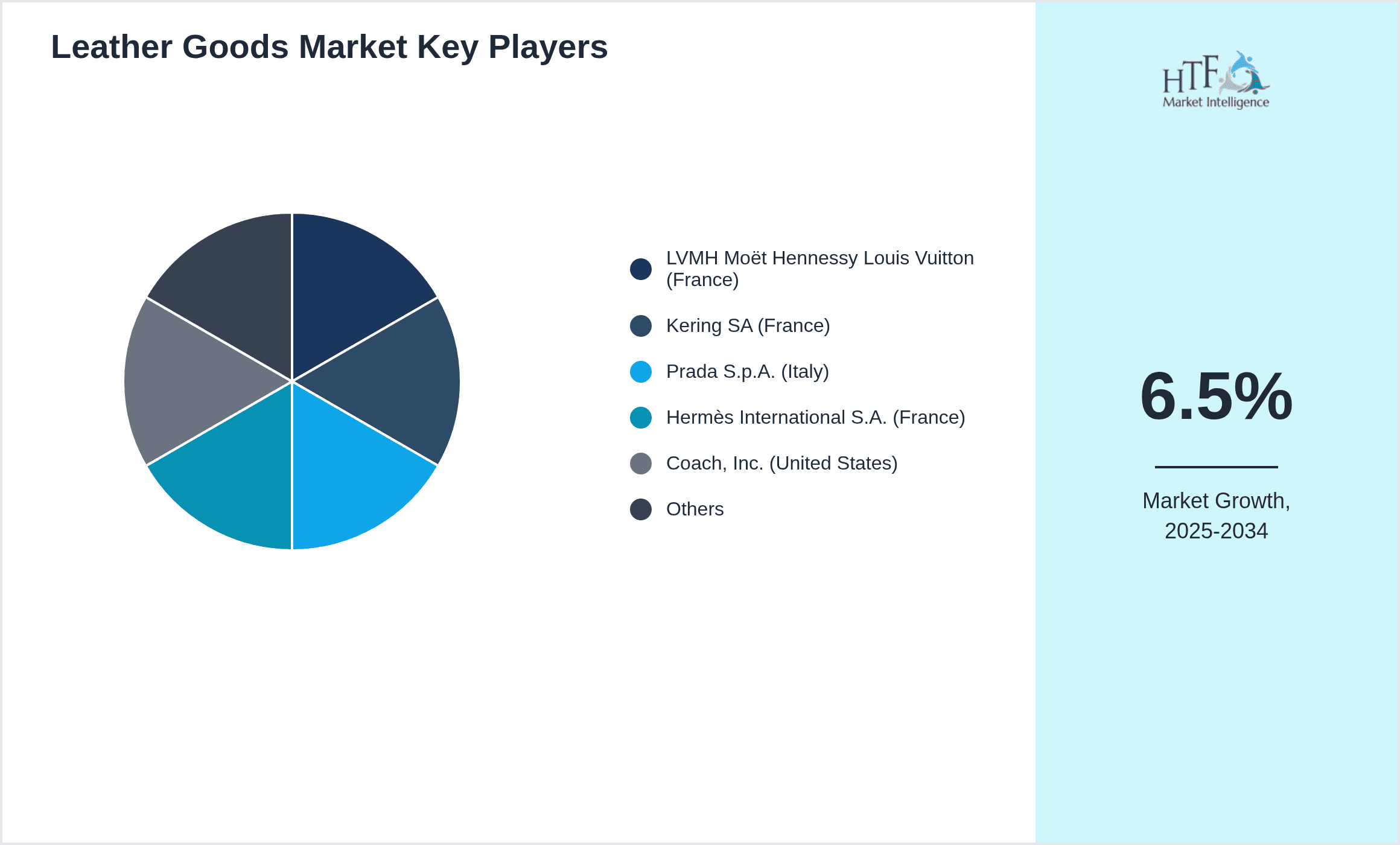

Leading Companies in Leather Goods Market

- •LVMH Moët Hennessy Louis Vuitton (France)

- •Kering SA (France)

- •Prada S.p.A. (Italy)

- •Hermès International S.A. (France)

- •Coach, Inc. (United States)

- •Fossil Group, Inc. (United States)

- •Tapestry, Inc. (United States)

- •Gucci (Italy)

- •Burberry Group plc (United Kingdom)

- •Michael Kors Holdings Limited (United States)

- •Salvatore Ferragamo S.p.A. (Italy)

- •Mulberry Group plc (United Kingdom)

- •Aspinal of London (United Kingdom)

- •Ralph Lauren Corporation (United States)

- •Tod's S.p.A. (Italy)

- •Skechers U.S.A., Inc. (United States)

- •VF Corporation (United States)

- •Salvatore Ferragamo S.p.A. (Italy)

- •Longchamp (France)

- •Hugo Boss AG (Germany)

- •Brunello Cucinelli S.p.A. (Italy)

- •Chanel S.A. (France)

- •Coach (United States)

- •Bally International AG (Switzerland)

- •Calvin Klein Inc. (United States)

Market Breakdown

- •By Product Type

- ◦Genuine Leather

- ◦Synthetic Leather

- ◦Suede Leather

- ◦Nubuck Leather

- ◦Patent Leather

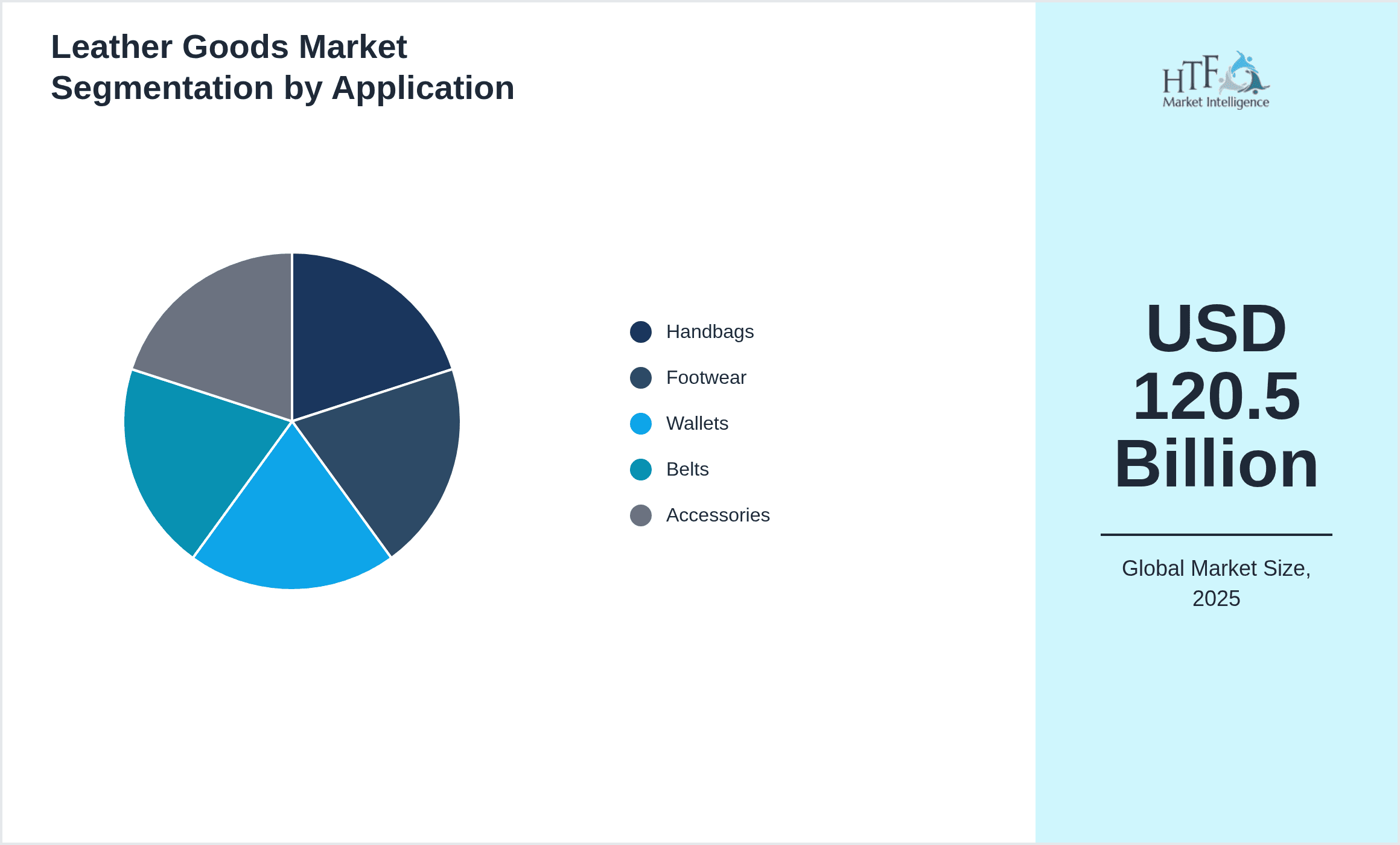

- •By Application

- ◦Handbags

- ◦Footwear

- ◦Wallets

- ◦Belts

- ◦Accessories

- •By End-Use Industry

- ◦Fashion & Apparel

- ◦Luxury Goods

- ◦Automotive Interiors

- ◦Sports & Leisure

- •By Distribution Channel

- ◦Retail Stores

- ◦E-commerce

- ◦Wholesale

Growth Dynamics

The Global Leather Goods market growth is primarily driven by increasing consumer preference for premium and sustainable leather products. Rising disposable incomes in emerging economies have expanded the customer base, particularly in Asia-Pacific, where urbanization and fashion consciousness are accelerating demand. Technological advancements in leather processing and synthetic alternatives have enhanced product quality and reduced environmental impact, fostering market expansion. Additionally, the proliferation of e-commerce platforms has broadened market accessibility, enabling brands to reach diverse demographics worldwide. Strategic collaborations between luxury brands and eco-conscious innovators are further stimulating growth. The shift towards personalized and customized leather goods also supports higher consumer engagement and loyalty. Collectively, these factors create a robust growth environment, positioning the leather goods market for sustained expansion through 2034.

Market Trends

Sustainability has emerged as a defining trend in the Global Leather Goods market, with manufacturers adopting eco-friendly tanning processes and sourcing certified raw materials. There is growing consumer demand for vegan leather alternatives and cruelty-free products, prompting innovation in synthetic leather technologies. Digital transformation is reshaping distribution channels, with omnichannel retailing and virtual try-ons enhancing customer experience. Additionally, collaborations between luxury brands and artists or designers are creating limited-edition collections that drive exclusivity and consumer interest. The rise of fast fashion has also led to increased demand for affordable leather goods, balancing luxury with accessibility. These trends collectively influence product design, marketing strategies, and supply chain operations, positioning the market to adapt to evolving consumer expectations and regulatory landscapes.

Market Opportunities

Expanding into untapped emerging markets, particularly in Asia-Pacific and Latin America, offers significant growth opportunities for leather goods manufacturers. The increasing middle-class population with rising purchasing power fuels demand for both luxury and affordable leather products. Innovations in sustainable and bio-based leather alternatives present avenues for product differentiation and compliance with stringent environmental regulations. Additionally, leveraging digital platforms for direct-to-consumer sales enhances market penetration and brand loyalty. Collaborations with fashion influencers and adoption of customization technologies can further attract younger demographics seeking unique products. Investments in supply chain transparency and ethical sourcing will also strengthen brand reputation and consumer trust. These opportunities position the leather goods market for long-term sustainable growth and competitive advantage globally.

Market Challenges

The Global Leather Goods market faces challenges including fluctuating raw material prices due to livestock availability and geopolitical factors impacting supply chains. Environmental regulations on tanning processes and waste management impose compliance costs and operational complexities for manufacturers. Additionally, competition from synthetic leather and alternative materials pressures market shares of traditional leather products. Counterfeit goods and brand infringement issues undermine profitability and consumer trust. The COVID-19 pandemic disrupted retail and manufacturing operations, causing demand fluctuations and logistical constraints. Furthermore, changing consumer preferences towards minimalist lifestyles and digital goods may reduce demand for physical leather products. Addressing these challenges requires innovation in sustainable practices, supply chain resilience, and strategic marketing to maintain market position and growth.

Regulatory Framework

Between 2019 and 2024, key environmental regulations affecting the Global Leather Goods market have focused on reducing pollution from tanning processes and promoting sustainable sourcing. The EU's REACH regulation mandates strict control on chemical usage in leather production, impacting manufacturers worldwide. North America has intensified regulations on waste disposal and water treatment facilities in leather manufacturing plants. Several countries have introduced guidelines to ensure animal welfare standards for raw material sourcing. Additionally, import-export policies have been updated to include stricter labeling and certification requirements to combat counterfeit products. Governments are also incentivizing adoption of eco-friendly technologies through subsidies and tax benefits, encouraging industry-wide shifts towards green manufacturing practices. Compliance with these regulations is critical for market access, influencing product development, operational costs, and competitive strategies globally.

Market Intelligence

- •15th January 2024, LVMH Moët Hennessy Louis Vuitton launched a new line of sustainable leather handbags made from bio-based materials, targeting environmentally conscious consumers. The product features innovative tanning techniques that reduce water consumption by 40% and eliminate the use of harmful chemicals. This launch aligns with LVMH’s strategic commitment to sustainability and expands its eco-friendly portfolio, positioning the company as a market leader in green luxury goods. The collection is available globally through flagship stores and e-commerce platforms, expected to drive significant market share growth in the premium segment. Source: Official LVMH Press Release

- •10th November 2023, Coach, Inc. introduced a new synthetic leather footwear collection that combines durability with vegan-friendly materials. The line incorporates advanced polymer composites that mimic the texture and longevity of genuine leather while reducing carbon footprint. This innovation addresses rising consumer demand for cruelty-free products and supports Coach's sustainability goals. Market analysts predict this launch will enhance Coach’s competitive positioning, particularly among younger demographics prioritizing ethical consumption. The collection rollout includes online exclusive releases and partnerships with major retailers in North America and Europe. Source: Coach Corporate Website

- •20th March 2024, Kering SA announced a strategic partnership with a biotechnology firm to develop lab-grown leather alternatives. This collaboration aims to revolutionize the leather goods industry by producing materials that offer the look and feel of traditional leather with zero animal impact. The initiative is expected to reduce environmental burdens associated with livestock farming and tanning. Kering plans to integrate these materials into its product lines by 2025, reinforcing its leadership in sustainability innovation and attracting eco-conscious consumers globally. Source: Kering Official Announcement

- •5th July 2023, Prada S.p.A. expanded its global retail footprint by opening flagship stores in emerging markets across Southeast Asia. The expansion supports growing regional demand for luxury leather goods fueled by increasing disposable incomes and fashion awareness. Prada’s stores feature digital integration and personalized shopping experiences, enhancing customer engagement. This strategic move is expected to strengthen Prada’s market share in Asia-Pacific, leveraging the region’s high growth potential. Source: Prada Corporate News

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

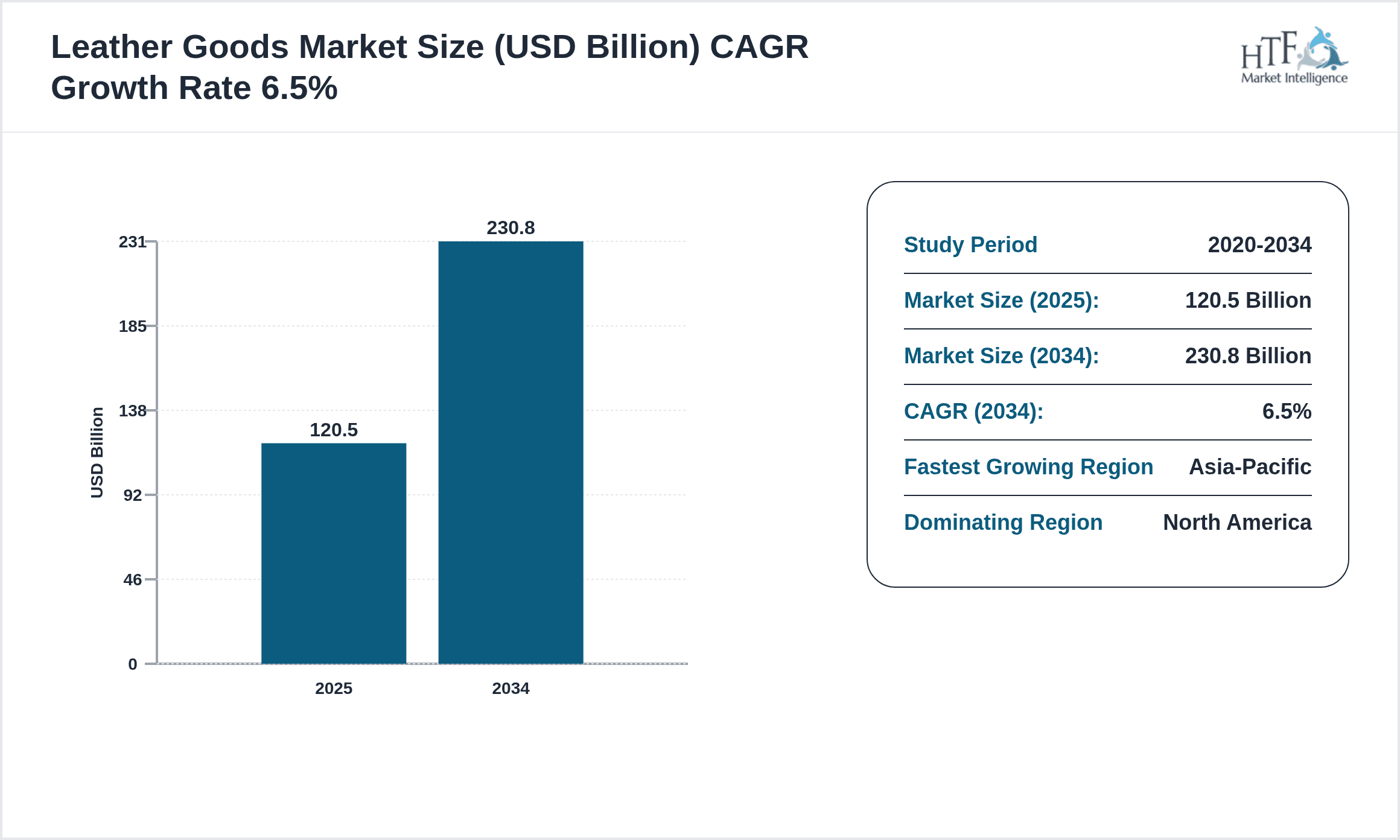

| Base Year Market Size | USD 120.5 Billion |

| Forecast Year Market Size | USD 230.8 Billion |

| CAGR | 6.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.3% |

| Scope of Report | Market is segmented by Product Type (Genuine Leather, Synthetic Leather, Suede Leather, Nubuck Leather, Patent Leather), Application (Handbags, Footwear, Wallets, Belts, Accessories), End-Use Industry (Fashion & Apparel, Luxury Goods, Automotive Interiors, Sports & Leisure), Distribution Channel (Retail Stores, E-commerce, Wholesale) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | LVMH Moët Hennessy Louis Vuitton (France), Kering SA (France), Prada S.p.A. (Italy), Hermès International S.A. (France), Coach, Inc. (United States) |

Global Leather Goods Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.