Global Orthopedic Bone Cement And Casting Materials Market Size, Growth & Revenue 2025-2034

Global Orthopedic Bone Cement And Casting Materials Market is segmented by Type (Polymethyl Methacrylate (PMMA) Bone Cement, Calcium Phosphate Cement, Bioactive Glass Cement, Composite Bone Cement, Others), Application (Joint Reconstruction, Trauma, Spine Surgery, Dental, Others), End-Use Industry (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Dental Clinics), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global orthopedic bone cement and casting materials market comprises biocompatible substances essential for bone repair and fixation during orthopedic surgical procedures. This market covers primary product types including polymethyl methacrylate bone cements, calcium phosphate cements, and bioactive glass cements, which are utilized across various applications such as joint reconstruction, trauma treatment, spine surgery, and dental procedures. The evolving scope includes innovations in material formulations enhancing mechanical strength, biodegradability, and osteoconductivity, which improve postoperative outcomes and patient safety. The market holds strategic importance due to the increasing incidence of orthopedic injuries, aging demographics, and the rising prevalence of chronic bone diseases globally. Furthermore, the advancement of minimally invasive surgical techniques and growing healthcare infrastructure in emerging economies propel market expansion. This market integrates multidisciplinary technologies and clinical expertise to address the rising demand for effective bone stabilization and regeneration, thus playing a pivotal role in the healthcare ecosystem worldwide.

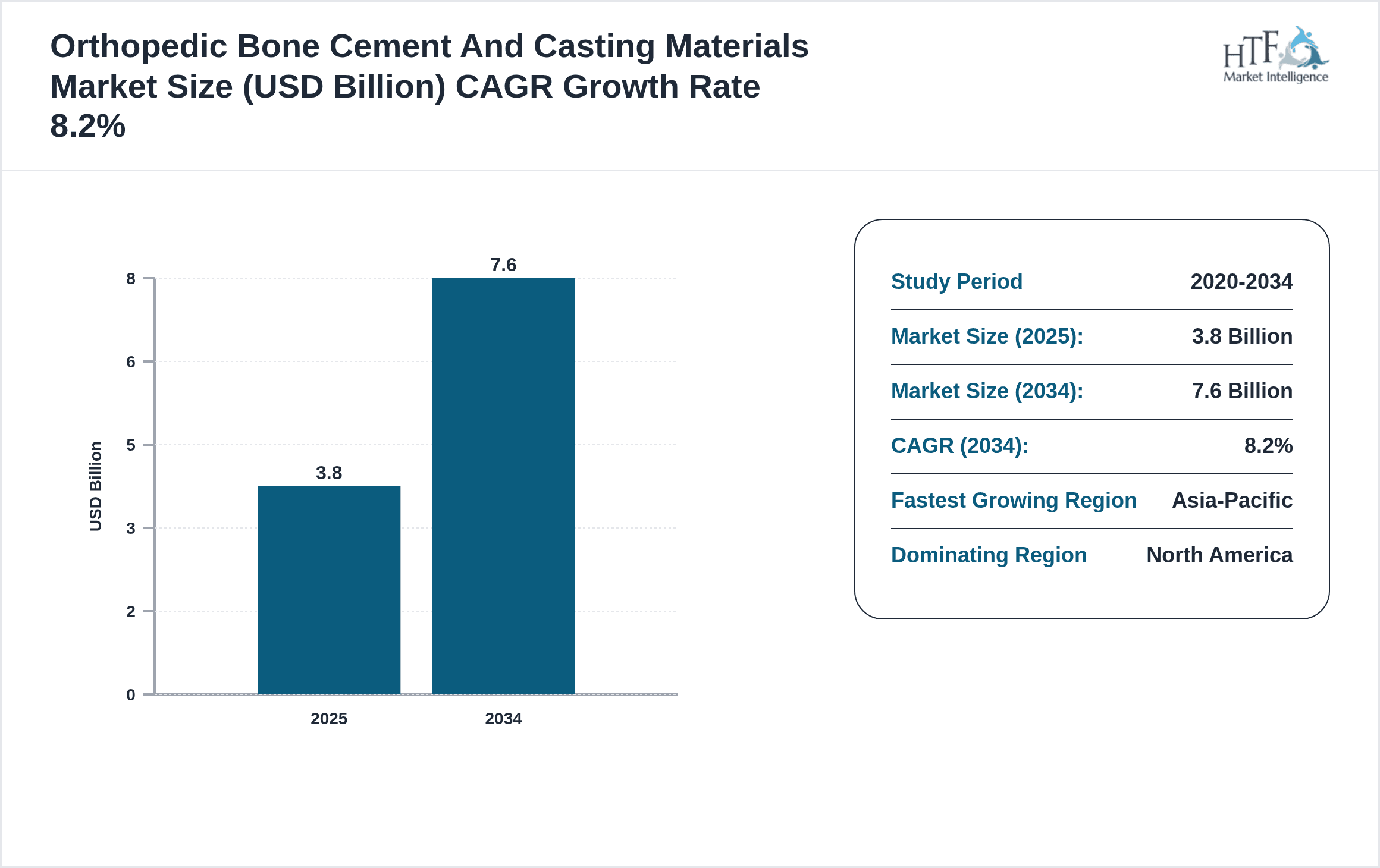

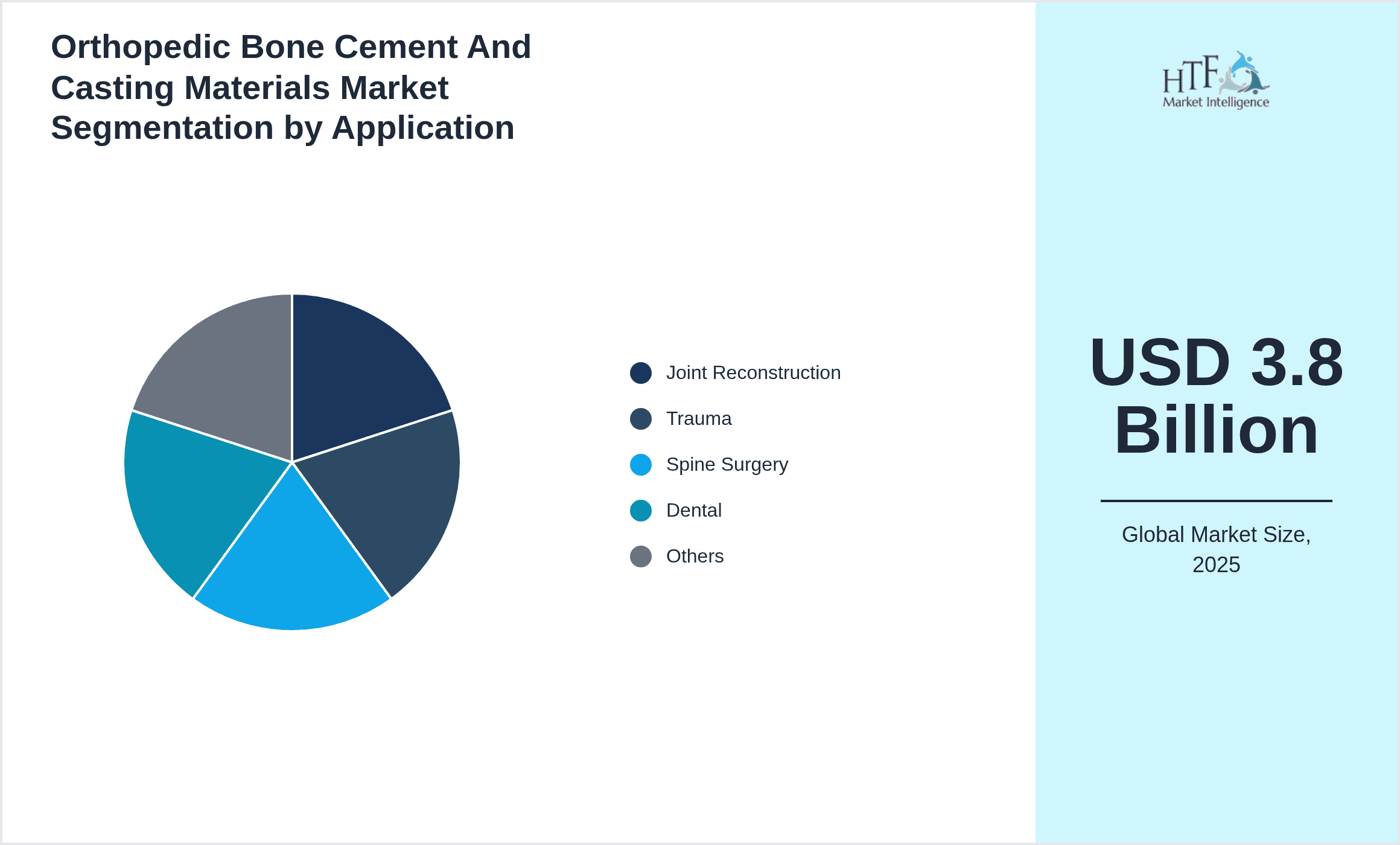

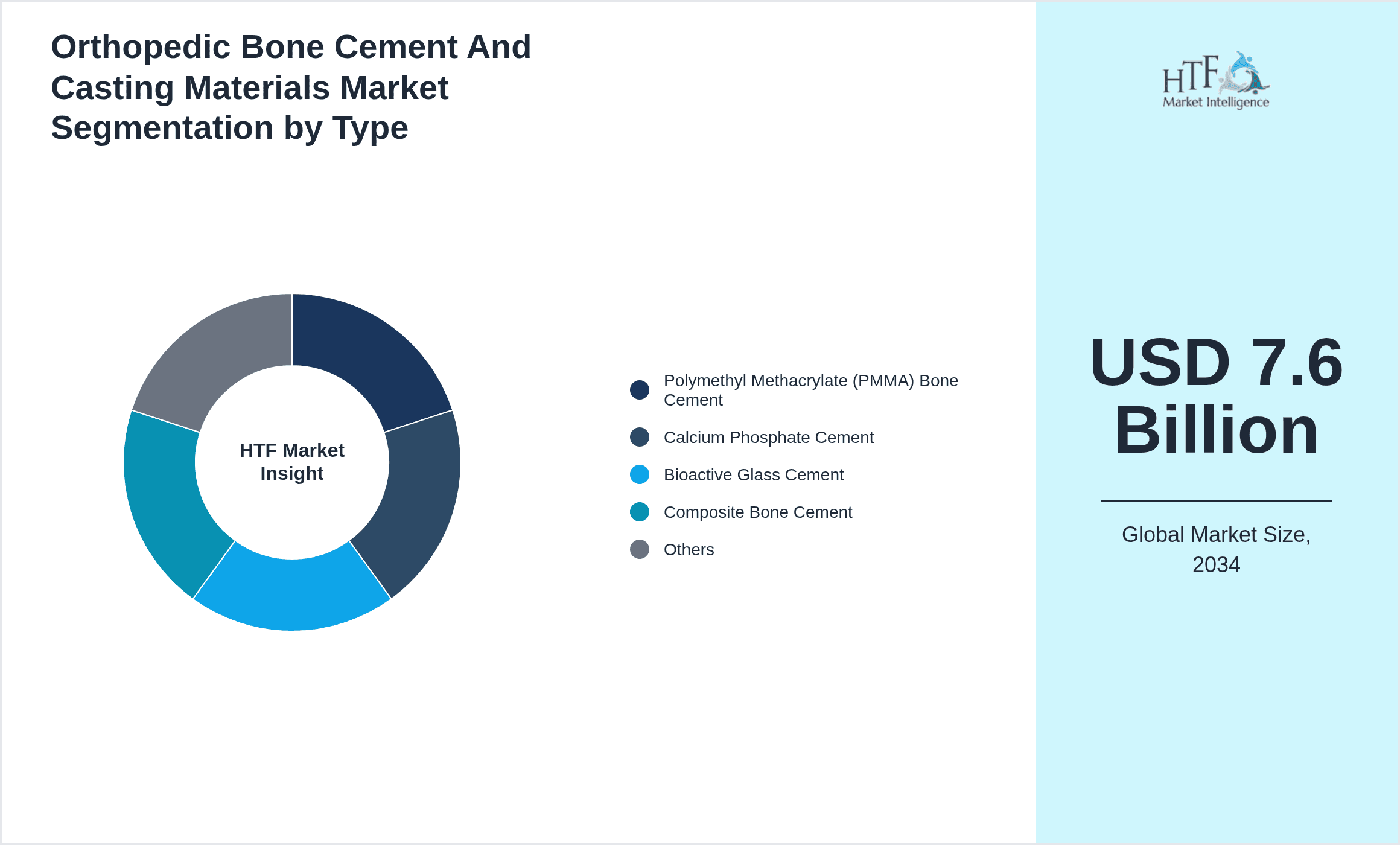

- •The market is projected to grow from USD 3.8 billion in 2025 to USD 7.6 billion by 2034, registering a robust CAGR of 8.2 percent. North America dominates with the largest market share, driven by advanced healthcare infrastructure and high adoption rates of innovative orthopedic materials. Asia-Pacific exhibits the highest growth rate fueled by expanding medical facilities and increasing orthopedic surgeries. PMMA bone cement remains the leading product type, while calcium phosphate cement shows the fastest growth due to its biocompatible properties and rising preference in minimally invasive procedures. Joint reconstruction leads application segments, with increasing cases of osteoarthritis and sports injuries globally. These data points highlight significant growth potential and emerging opportunities within the orthopedic bone cement and casting materials market.

- •This market offers a compelling value proposition to healthcare providers, manufacturers, and patients by delivering materials that enhance surgical precision, reduce recovery times, and improve patient quality of life. For orthopedic surgeons and hospitals, these materials provide reliable fixation solutions that adapt to various surgical needs and patient conditions. Manufacturers benefit from continual technological advancements and expanding global demand, enabling innovation in product portfolios and market penetration. Additionally, patients and caregivers gain from improved clinical outcomes and reduced postoperative complications. The strategic importance of this market is underscored by its direct impact on the efficacy of orthopedic treatments and its growing integration within multidisciplinary therapeutic approaches in the global healthcare industry.

Competitive Landscape

The competitive landscape in the orthopedic bone cement and casting materials market is characterized by strategic product innovation, expansion into emerging markets, and collaborative partnerships among industry players. Companies prioritize research and development to enhance material properties such as biocompatibility, mechanical strength, and delivery mechanisms, leading to differentiated product offerings. Global expansion strategies target regions with increasing orthopedic procedure volumes, notably Asia-Pacific and Latin America, to leverage growing healthcare infrastructure. Technological adoption includes integration of bioactive and resorbable materials to meet evolving clinical demands. Strategic alliances and mergers enable consolidation of expertise and market share, allowing players to broaden their portfolios and optimize supply chains. Pricing strategies focus on balancing affordability with advanced product features to capture diverse customer segments. Distribution channel diversification through direct sales, distributors, and e-commerce platforms enhances market reach. Companies invest substantially in regulatory compliance and quality certifications to maintain competitive advantage and ensure market access globally. The dynamic competitive environment fosters continuous innovation and adaptation to shifting market trends and regional demands.

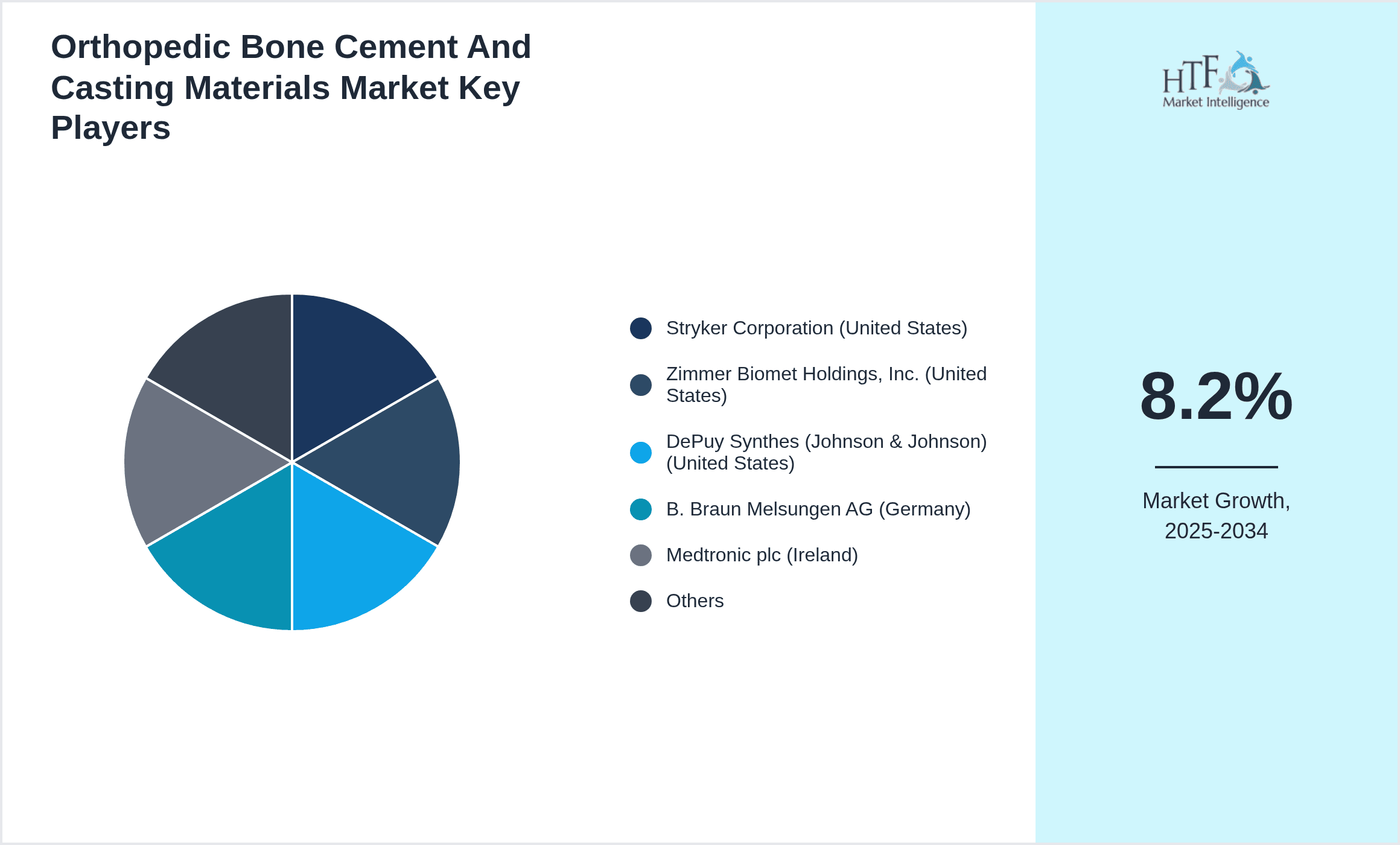

Leading Companies in Orthopedic Bone Cement And Casting Materials Market

- •Stryker Corporation (United States)

- •Zimmer Biomet Holdings, Inc. (United States)

- •DePuy Synthes (Johnson & Johnson) (United States)

- •B. Braun Melsungen AG (Germany)

- •Medtronic plc (Ireland)

- •Heraeus Holding GmbH (Germany)

- •Smith & Nephew plc (United Kingdom)

- •DJ Orthopedics (United States)

- •Cortec Corporation (United States)

- •Exactech, Inc. (United States)

- •Orthovita, Inc. (United States)

- •Mediwound Ltd. (Israel)

- •BIOCERAMENT, Inc. (United States)

- •KISCO International, Inc. (United States)

- •Stryker India Pvt Ltd (India)

- •Synthes GmbH (Switzerland)

- •Medline Industries, Inc. (United States)

- •Integra LifeSciences Corporation (United States)

- •Orthosolutions, Inc. (United States)

- •NuVasive, Inc. (United States)

Market Breakdown

- •By Type

- ◦Polymethyl Methacrylate (PMMA) Bone Cement

- ◦Calcium Phosphate Cement

- ◦Bioactive Glass Cement

- ◦Composite Bone Cement

- ◦Others

- •By Application

- ◦Joint Reconstruction

- ◦Trauma

- ◦Spine Surgery

- ◦Dental

- ◦Others

- •By End-Use Industry

- ◦Hospitals

- ◦Orthopedic Clinics

- ◦Ambulatory Surgical Centers

- ◦Dental Clinics

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

The global orthopedic bone cement and casting materials market growth is propelled by increasing prevalence of musculoskeletal disorders and the rising geriatric population requiring joint reconstruction and trauma treatment. Advancements in material science, such as enhanced bioactive and biodegradable bone cements, support improved surgical outcomes and patient recovery. Expanding healthcare infrastructure in emerging economies fosters greater accessibility and adoption of orthopedic procedures. Furthermore, growing awareness about minimally invasive surgeries drives demand for specialized bone cements with superior handling properties. Real-time instances include increased usage of calcium phosphate cement in Asia-Pacific due to its osteoconductive properties. Strategic collaborations between manufacturers and healthcare providers enhance product development and market penetration. Regulatory approvals for novel biocompatible materials further bolster growth. The cumulative impact of these factors establishes a robust growth trajectory, attracting investments and encouraging innovation across the industry landscape.

Market Trends

Emerging trends in the orthopedic bone cement and casting materials market include the integration of nanotechnology to improve material strength and bioactivity. Increasing adoption of 3D printing techniques facilitates the development of patient-specific casting materials and implants, enhancing surgical precision and customization. The shift towards resorbable and bioactive cements reflects growing emphasis on reducing long-term complications and promoting natural bone regeneration. Recent industry examples include the launch of bioactive glass-based bone cements offering enhanced bonding with bone tissue. Additionally, digitalization in supply chain management improves product availability and reduces costs. Growing collaborations between research institutions and manufacturers accelerate innovation cycles. These trends collectively indicate a market evolution focused on technological sophistication, patient-centric solutions, and operational efficiency, driving future opportunities and shaping competitive dynamics.

Market Opportunities

Significant opportunities in the orthopedic bone cement and casting materials market arise from unmet needs in emerging regions where orthopedic care infrastructure is rapidly developing. Expansion into Asia-Pacific and Latin America offers vast potential due to rising orthopedic surgery volumes and increasing healthcare expenditure. Innovation in bioactive and resorbable bone cement formulations presents avenues to capture market share by addressing concerns related to toxicity and implant longevity. The growing demand for minimally invasive procedures creates openings for advanced bone cements tailored to these techniques. Furthermore, partnerships between material scientists and orthopedic surgeons enable co-development of next-generation products that enhance clinical outcomes. Recent investments in digital health solutions and telemedicine also support remote surgical planning and material management. These factors collectively create a fertile landscape for market entrants and incumbents to capitalize on evolving clinical and technological demands.

Market Challenges

Challenges in the orthopedic bone cement and casting materials market include stringent regulatory approvals that delay product launches and increase development costs. Variability in clinical acceptance due to concerns regarding biocompatibility and long-term implant stability constrains market growth. High costs associated with advanced bone cement formulations limit accessibility in price-sensitive markets. Supply chain disruptions and raw material price volatility create operational uncertainties for manufacturers. Additionally, competition from alternative fixation technologies such as bioresorbable screws and plates impacts demand for traditional bone cements. Recent industry reports highlight difficulties faced by companies in obtaining timely certifications in emerging markets, further complicating expansion efforts. These challenges necessitate strategic risk management, continuous innovation, and effective stakeholder engagement to sustain and grow market presence.

Regulatory Framework

In the last five years, key regulatory developments have shaped the orthopedic bone cement and casting materials market globally. The U.S. Food and Drug Administration has enhanced scrutiny over biocompatibility and safety profiles of bone cements, requiring comprehensive clinical data for approvals. The European Medical Device Regulation introduced stricter classification and post-market surveillance mandates that impact product lifecycle management. In Asia-Pacific, regulatory agencies have accelerated harmonization efforts to align with global standards, facilitating faster market entry. These regulations emphasize robust quality management systems, traceability, and adverse event reporting to ensure patient safety. Compliance with these evolving frameworks necessitates substantial investment by manufacturers in clinical research, documentation, and manufacturing controls. Collectively, these regulations foster higher product quality and safety, influencing market dynamics and competitive positioning worldwide.

Market Intelligence

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Source: Official company announcements and industry reports

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 7.6 Billion |

| CAGR | 8.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.9% |

| Scope of Report | Market is segmented by Type (Polymethyl Methacrylate (PMMA) Bone Cement, Calcium Phosphate Cement, Bioactive Glass Cement, Composite Bone Cement, Others), Application (Joint Reconstruction, Trauma, Spine Surgery, Dental, Others), End-Use Industry (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Dental Clinics), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Stryker Corporation (United States), Zimmer Biomet Holdings, Inc. (United States), DePuy Synthes (Johnson & Johnson) (United States), B. Braun Melsungen AG (Germany), Medtronic plc (Ireland), Heraeus Holding GmbH (Germany), Smith & Nephew plc (United Kingdom), DJ Orthopedics (United States), Cortec Corporation (United States), Exactech, Inc. (United States), Orthovita, Inc. (United States), Mediwound Ltd. (Israel), BIOCERAMENT, Inc. (United States), KISCO International, Inc. (United States), Stryker India Pvt Ltd (India), Synthes GmbH (Switzerland), Medline Industries, Inc. (United States), Integra LifeSciences Corporation (United States), Orthosolutions, Inc. (United States), NuVasive, Inc. (United States) |

Global Orthopedic Bone Cement And Casting Materials Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.