Global Ophthalmic Surgical Systems Market - Outlook 2024-2034

Global Ophthalmic Surgical Systems Market is segmented by Product Type (Phacoemulsification Systems, Femtosecond Laser Systems, Vitrectomy Systems, Laser Systems, Microkeratomes), Application (Cataract Surgery, Glaucoma Surgery, Retinal Surgery, Refractive Surgery, Pediatric Ophthalmic Surgery), End-Use Industry (Hospitals, Specialty Eye Clinics, Ambulatory Surgical Centers, Research and Academic Institutes), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Ophthalmic Surgical Systems market comprises sophisticated medical equipment tailored for eye surgeries, including devices for cataract, glaucoma, retinal, refractive, and pediatric ophthalmic procedures. This market integrates cutting-edge technologies such as phacoemulsification, femtosecond lasers, and vitrectomy instruments, enabling precise and minimally invasive interventions. Rising incidences of ocular diseases, driven by aging populations and lifestyle factors, augment demand for advanced surgical solutions worldwide. Market growth is further propelled by technological innovation, expanding healthcare infrastructure, and increasing awareness about eye health. The market is segmented by product types, applications, end-user settings, and distribution channels, reflecting diverse demand dynamics across global regions. Regulatory compliance, reimbursement policies, and healthcare spending patterns critically influence adoption rates and market penetration. Overall, the ophthalmic surgical systems market represents a vital component of the global ophthalmology sector, offering significant opportunities for medical device manufacturers, healthcare providers, and technology innovators in enhancing patient outcomes and operational efficiency.

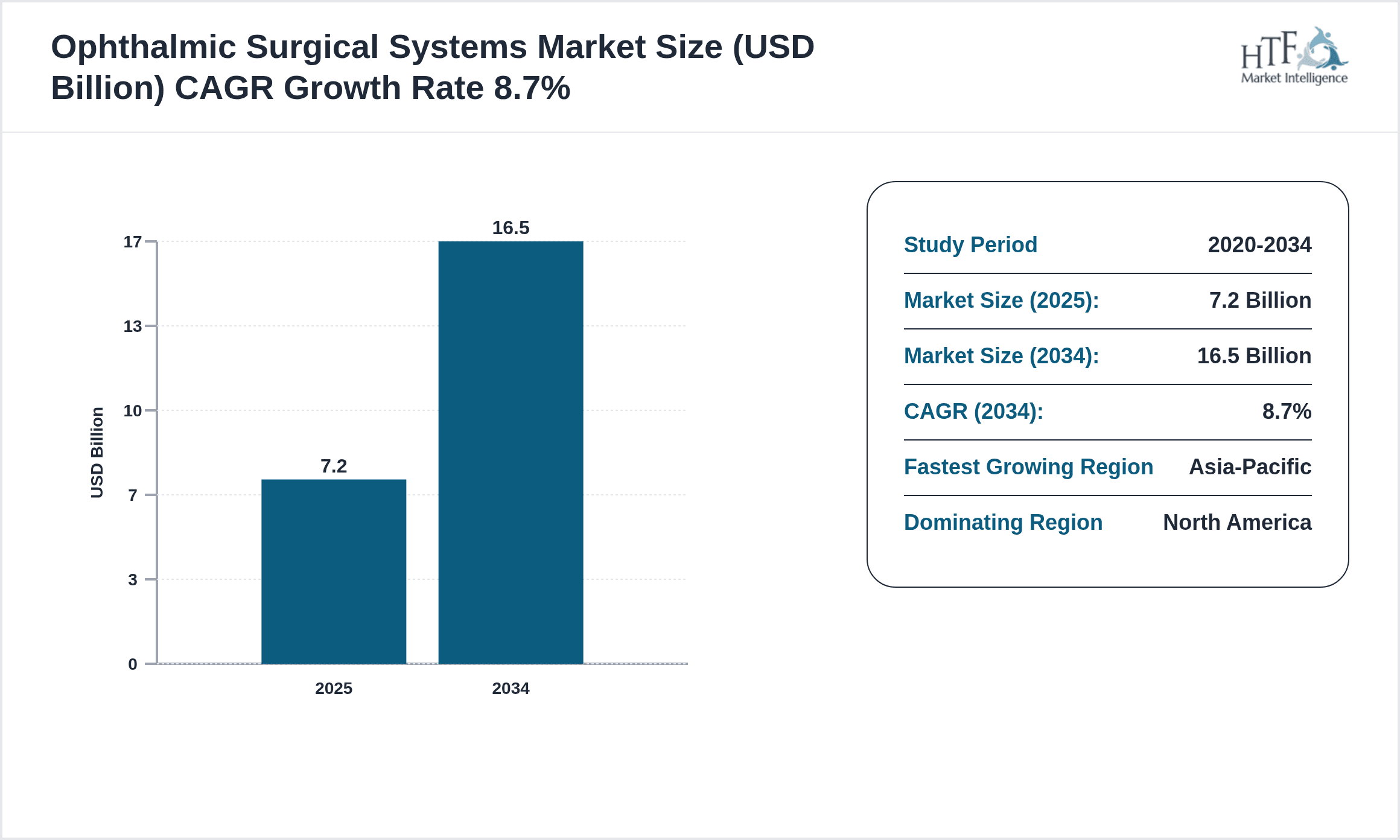

- •Key highlights include a base market valuation of USD 7.2 Billion in 2024, projected to reach USD 16.5 Billion by 2034, reflecting a robust CAGR of 8.7%. North America dominates the market due to advanced healthcare infrastructure and high adoption rates, while Asia-Pacific exhibits the fastest growth driven by expanding healthcare access and rising patient awareness. Phacoemulsification systems maintain leadership in product types, with femtosecond laser systems emerging as the fastest-growing segment owing to precision and safety benefits. Cataract surgery remains the predominant application, followed closely by glaucoma and retinal surgeries. The market landscape is shaped by continuous innovation, strategic collaborations, and evolving clinical practices, underscoring its dynamic nature and potential for substantial value generation across regions.

- •This market holds strategic importance for medical device companies, healthcare institutions, and investors focused on ophthalmology. Its growth trajectory offers opportunities for technological advancement, market expansion, and enhanced patient care. The integration of digital platforms, laser technologies, and minimally invasive surgical techniques aligns with the global shift towards precision medicine and value-based care. Stakeholders benefit from understanding market segmentation, competitive dynamics, and regulatory environments to effectively position their offerings and capitalize on emerging trends. Overall, the global ophthalmic surgical systems market is poised for significant expansion, driven by unmet clinical needs, increasing surgical volumes, and the pursuit of superior visual outcomes for patients worldwide.

Competitive Landscape

The global ophthalmic surgical systems market is highly competitive with numerous established players and emerging entrants striving for technological leadership and market share. Competition revolves around product innovation, clinical efficacy, pricing strategies, and geographic coverage. Leading companies invest heavily in R&D to develop next-generation surgical platforms integrating laser technology, robotics, and AI for enhanced precision. Strategic partnerships, acquisitions, and collaborations are common to expand product portfolios and distribution networks. Market rivalry is intensified by the need to address diverse patient populations and comply with stringent regulatory standards globally. Additionally, companies focus on after-sales service, training, and customer support to differentiate offerings. The competitive landscape reflects dynamic shifts as companies adapt to evolving clinical practices and emerging technologies, ensuring sustained growth and resilience in an expanding global market.

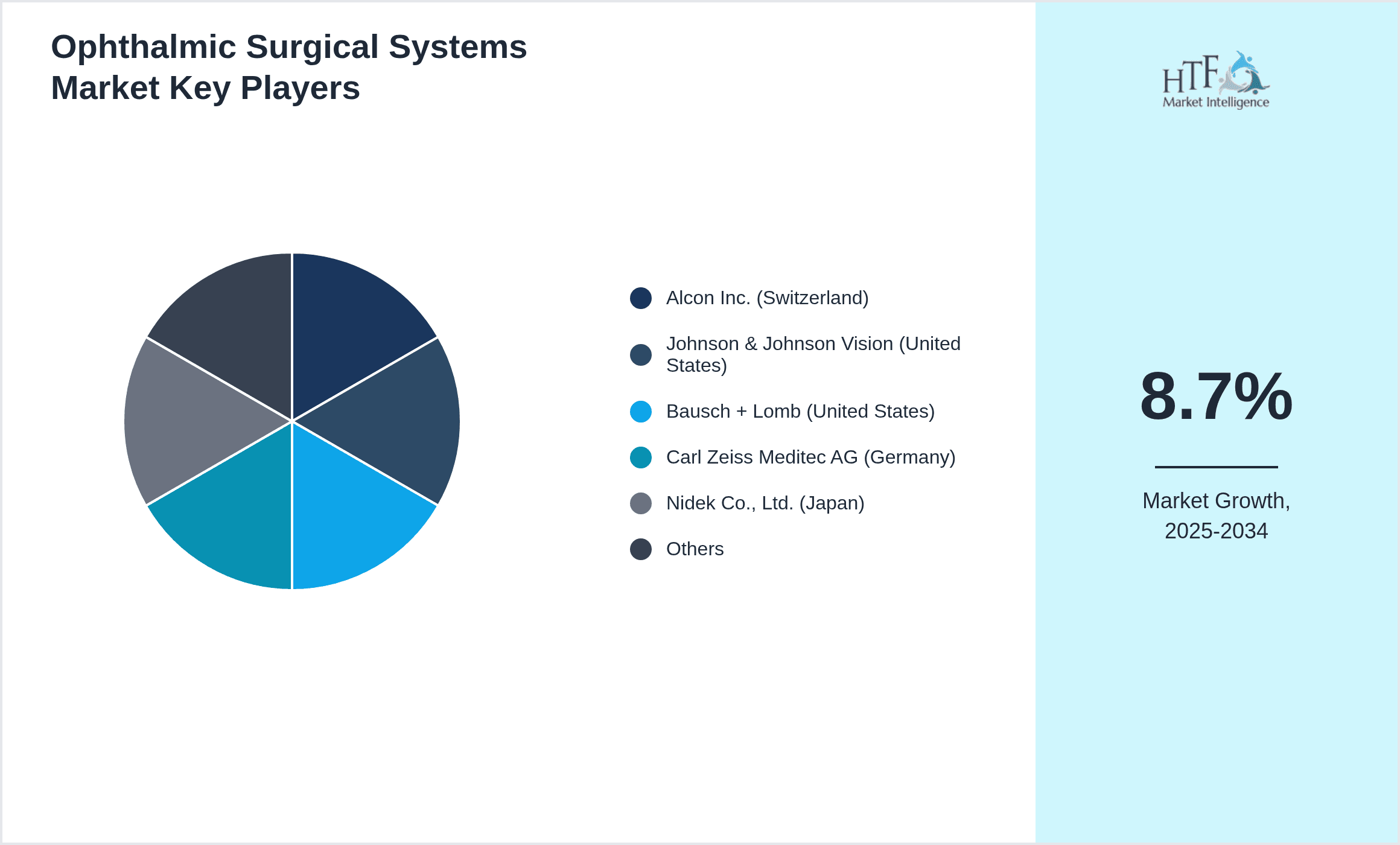

Prominent Players in Ophthalmic Surgical Systems Market

- •Alcon Inc. (Switzerland)

- •Johnson & Johnson Vision (United States)

- •Bausch + Lomb (United States)

- •Carl Zeiss Meditec AG (Germany)

- •Nidek Co., Ltd. (Japan)

- •HOYA Corporation (Japan)

- •Lumenis Ltd. (Israel)

- •Topcon Corporation (Japan)

- •Ellex Medical Lasers Ltd. (Australia)

- •Ziemer Ophthalmic Systems AG (Switzerland)

- •Synergetics USA, Inc. (United States)

- •Quantel Medical (France)

- •Surgical Innovations Group plc (United Kingdom)

- •DORC International (Netherlands)

- •Medennium Inc. (United States)

- •Ellex Medical Lasers Ltd. (Australia)

- •Optovue, Inc. (United States)

- •Iridex Corporation (United States)

- •Elbit Imaging Ltd. (Israel)

- •Avedro, Inc. (United States)

- •Keeler Ltd. (United Kingdom)

- •Asclepion Laser Technologies GmbH (Germany)

- •Haag-Streit AG (Switzerland)

- •Moria SA (France)

- •Quantel Medical (France)

Market Breakdown

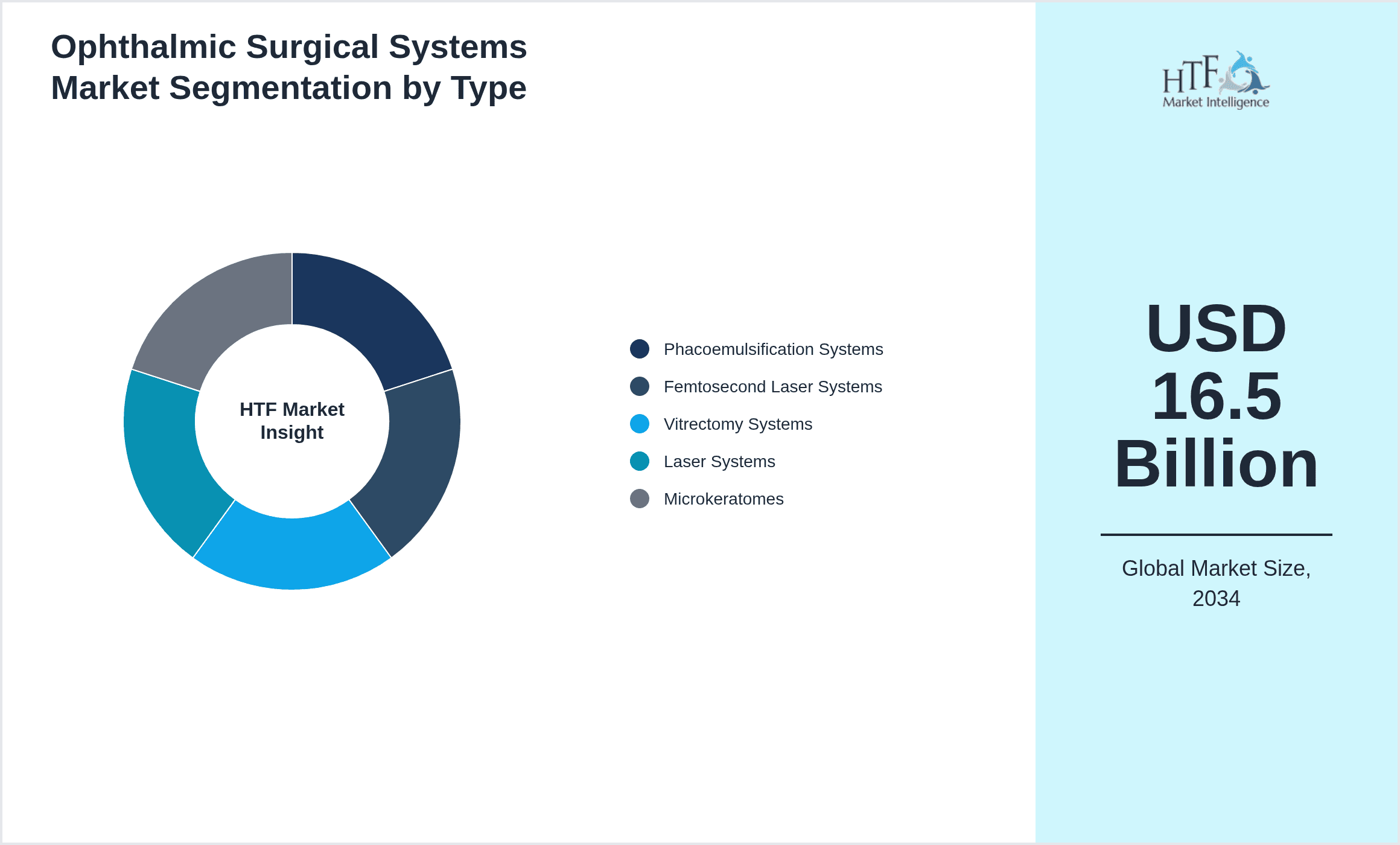

- •By Product Type

- ◦Phacoemulsification Systems

- ◦Femtosecond Laser Systems

- ◦Vitrectomy Systems

- ◦Laser Systems

- ◦Microkeratomes

- •By Application

- ◦Cataract Surgery

- ◦Glaucoma Surgery

- ◦Retinal Surgery

- ◦Refractive Surgery

- ◦Pediatric Ophthalmic Surgery

- •By End-Use Industry

- ◦Hospitals

- ◦Specialty Eye Clinics

- ◦Ambulatory Surgical Centers

- ◦Research and Academic Institutes

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

- •Rising prevalence of cataracts and other ocular disorders globally, driven by aging populations and increasing diabetes incidence, fuels demand for advanced ophthalmic surgical systems. Improved healthcare access in developing regions further expands the patient base and surgical volumes.

- •Technological advancements such as femtosecond lasers and robotic-assisted surgeries enhance precision and patient outcomes, attracting adoption among surgeons and healthcare facilities. These innovations also reduce intraoperative risks and recovery times, encouraging market growth.

- •Increasing government initiatives and reimbursement policies supporting eye care and surgical interventions promote wider acceptance of ophthalmic surgical systems, particularly in North America and Europe where healthcare infrastructure is well-established.

- •Growing awareness about eye health and vision correction, driven by public health campaigns and aging demographics, leads to higher demand for surgical treatments and related advanced devices.

- •Expansion of healthcare infrastructure and rising investments in emerging markets, especially in Asia-Pacific, facilitate market penetration and adoption of ophthalmic surgical technologies among a broader patient population.

- •Collaborations between medical device manufacturers and healthcare providers to develop customized solutions and training programs support market expansion and technology diffusion.

- •Increasing integration of digital technologies such as AI and imaging in surgical systems enables better diagnostics and surgical planning, fostering innovation-driven growth.

Market Trends

- •The adoption of femtosecond laser technology is accelerating, driven by its ability to perform precise corneal incisions and reduce surgical complications, making it a preferred choice in refractive and cataract surgeries.

- •Minimally invasive surgical procedures are trending globally, reflecting patient preference for faster recovery and reduced hospital stays, prompting manufacturers to develop compact and efficient ophthalmic systems.

- •Integration of AI and machine learning in ophthalmic surgical platforms is emerging, enabling enhanced image analysis, surgical navigation, and outcome prediction, thereby improving surgical accuracy and efficiency.

- •Sustainability initiatives are influencing product design with increased focus on energy-efficient devices and recyclable materials, aligning with global environmental goals and regulatory requirements.

- •Collaborative ecosystems involving technology firms, healthcare providers, and academic institutions are developing innovative solutions, accelerating product development cycles and clinical validation processes.

- •Expansion of telemedicine and remote diagnostics complements surgical systems, enabling preoperative assessments and postoperative follow-ups, thereby enhancing the continuum of ophthalmic care.

- •Emergence of portable and user-friendly devices allows wider adoption in outpatient settings and emerging markets, addressing accessibility challenges and decentralizing eye care services.

Market Opportunities

- •Untapped markets in Asia-Pacific and Latin America offer significant growth potential due to increasing healthcare investments and expanding middle-class populations demanding quality eye care services.

- •Development of multifunctional surgical platforms integrating diagnostics with treatment capabilities presents opportunities for enhanced clinical workflows and cost efficiencies.

- •Collaborations for localized manufacturing and distribution can reduce costs and improve market penetration in emerging economies, creating competitive advantages for manufacturers.

- •Innovations in laser-based technologies and robotic assistance open avenues for new product launches targeting complex and precision-demanding ophthalmic surgeries.

- •Growing geriatric population worldwide increases demand for cataract and glaucoma surgeries, creating sustained market expansion opportunities.

- •Integration of augmented reality and virtual reality in surgical training enhances surgeon skill levels and adoption of advanced systems, supporting market growth.

- •Emerging reimbursement schemes and government-sponsored eye health programs facilitate adoption of premium surgical systems among broader patient demographics.

Market Challenges

- •High cost of advanced ophthalmic surgical systems limits accessibility in low- and middle-income countries, constraining market growth despite clinical benefits.

- •Stringent regulatory approvals and prolonged clinical validation timelines increase time-to-market and development costs for new devices.

- •Lack of skilled surgeons trained in using sophisticated surgical systems poses a barrier to adoption in certain regions, affecting market penetration.

- •Competition from low-cost alternatives and refurbished equipment pressures pricing strategies and profit margins for leading manufacturers.

- •Supply chain disruptions and component shortages, exacerbated by global economic uncertainties, impact production and timely delivery of surgical systems.

- •Variability in reimbursement policies across countries complicates market access and influences purchasing decisions by healthcare providers.

- •Concerns regarding data security and patient privacy with integration of digital and connected surgical platforms require stringent compliance measures.

Regulatory Framework

- •Between 2019 and 2024, the U.S. FDA updated guidance on ophthalmic surgical devices emphasizing enhanced premarket data requirements and post-market surveillance to ensure patient safety and device efficacy.

- •The European Union implemented the Medical Device Regulation (MDR) in 2021, strengthening conformity assessment procedures and clinical evaluation criteria for ophthalmic surgical systems marketed within member states.

- •In Japan, the Pharmaceuticals and Medical Devices Agency (PMDA) revised approval pathways in 2022 to accelerate innovative ophthalmic device introductions while maintaining rigorous safety standards.

- •China's National Medical Products Administration (NMPA) introduced enhanced regulatory frameworks from 2020 to 2024 requiring localized clinical trials and stricter quality management for ophthalmic surgical devices.

- •Global harmonization efforts by the International Medical Device Regulators Forum (IMDRF) during this period aimed to unify standards for ophthalmic surgical systems, facilitating international market access and compliance.

Market Intelligence

- •15th February 2025, Alcon Inc. launched its next-generation phacoemulsification system featuring enhanced fluidics and improved surgeon ergonomics to optimize cataract surgery outcomes. The device integrates advanced software algorithms for real-time monitoring and adaptive energy delivery, aiming to reduce intraoperative complications and improve patient recovery. Targeted at hospitals and specialty eye clinics globally, this launch underpins Alcon's commitment to innovation and leadership in ophthalmic surgery technologies. Strategic objectives include expanding market share in emerging regions and reinforcing presence in mature markets through differentiated offerings. Source: Alcon Official Press Release

- •20th March 2025, Johnson & Johnson Vision unveiled the latest femtosecond laser platform designed for precision refractive and cataract surgeries. Incorporating AI-driven eye tracking and customizable treatment protocols, the system enhances surgical accuracy and patient safety. The launch aligns with growing demand for minimally invasive procedures and supports the company’s strategy to integrate digital solutions in surgical workflows. The system is being introduced initially in North America and Europe, with plans for phased rollout in Asia-Pacific. This innovation marks a significant advancement in ophthalmic surgical technology, targeting improved clinical outcomes and surgeon efficiency. Source: Johnson & Johnson Vision Corporate Announcement

- •5th January 2025, Bausch + Lomb announced a strategic partnership with a leading AI software firm to develop integrated diagnostic and surgical planning tools for retinal surgeries. This collaboration aims to leverage machine learning algorithms to enhance preoperative imaging, surgical navigation, and postoperative monitoring. The initiative reflects Bausch + Lomb’s focus on combining technology and clinical expertise to improve patient outcomes and streamline ophthalmic surgical procedures. The partnership is expected to accelerate innovation cycles and broaden the application scope of the company’s surgical systems across global markets. Source: Bausch + Lomb Industry Bulletin

- •10th April 2025, Carl Zeiss Meditec AG expanded its manufacturing capabilities with a new facility dedicated to femtosecond laser systems in Germany. This expansion aims to meet increasing global demand and shorten delivery lead times, enabling rapid deployment of advanced surgical technologies. The facility incorporates state-of-the-art automation and quality control processes to ensure product consistency and regulatory compliance. This strategic move supports Carl Zeiss Meditec’s growth ambitions in the ophthalmic surgical systems sector, particularly in Europe and Asia-Pacific regions. The investment underscores the company’s commitment to innovation and operational excellence. Source: Carl Zeiss Corporate News

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 7.2 Billion |

| Forecast Year Market Size | USD 16.5 Billion |

| CAGR | 8.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.4% |

| Scope of Report | Market is segmented by Product Type (Phacoemulsification Systems, Femtosecond Laser Systems, Vitrectomy Systems, Laser Systems, Microkeratomes), Application (Cataract Surgery, Glaucoma Surgery, Retinal Surgery, Refractive Surgery, Pediatric Ophthalmic Surgery), End-Use Industry (Hospitals, Specialty Eye Clinics, Ambulatory Surgical Centers, Research and Academic Institutes), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Alcon Inc. (Switzerland), Johnson & Johnson Vision (United States), Bausch + Lomb (United States), Carl Zeiss Meditec AG (Germany), Nidek Co., Ltd. (Japan), HOYA Corporation (Japan), Lumenis Ltd. (Israel), Topcon Corporation (Japan), Ellex Medical Lasers Ltd. (Australia), Ziemer Ophthalmic Systems AG (Switzerland), Synergetics USA, Inc. (United States), Quantel Medical (France), Surgical Innovations Group plc (United Kingdom), DORC International (Netherlands), Medennium Inc. (United States), Ellex Medical Lasers Ltd. (Australia), Optovue, Inc. (United States), Iridex Corporation (United States), Elbit Imaging Ltd. (Israel), Avedro, Inc. (United States), Keeler Ltd. (United Kingdom), Asclepion Laser Technologies GmbH (Germany), Haag-Streit AG (Switzerland), Moria SA (France), Quantel Medical (France) |

Global Ophthalmic Surgical Systems Market - Outlook 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.