Global Dendritic Cell Cancer Vaccine Market Size, Growth & Revenue 2024-2034

Global Dendritic Cell Cancer Vaccine Market is segmented by Product Type (Autologous DC Vaccine, Allogeneic DC Vaccine, Peptide-Pulsed DC Vaccine, RNA-Pulsed DC Vaccine, Fusion DC Vaccine), Application (Melanoma, Prostate Cancer, Lung Cancer, Breast Cancer, Other Cancers), End-Use Industry (Hospitals, Cancer Research Institutes, Clinical Laboratories, Biopharmaceutical Companies), Distribution Channel (Direct Sales, Specialty Clinics, Online Pharmacies), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global dendritic cell cancer vaccine market represents a cutting-edge segment in oncology therapeutics, focusing on the use of dendritic cells as antigen-presenting cells to elicit targeted immune responses against cancerous cells. These vaccines are developed by isolating dendritic cells from patients or donors, loading them with tumor-specific antigens, and administering them to stimulate the immune system to recognize and destroy malignant cells. The market spans a range of vaccine types including autologous, allogeneic, peptide-pulsed, RNA-pulsed, and fusion vaccines, each with distinct production methodologies and clinical applications. Predominantly utilized in treating melanoma, prostate, lung, and breast cancers, these vaccines offer promising alternatives to conventional therapies by leveraging personalized and precision medicine approaches. The industry is marked by significant research investments, regulatory developments, and growing clinical trial pipelines, reinforcing its strategic importance in immuno-oncology. With the rising incidence of cancer worldwide and increasing adoption of immunotherapeutic modalities, the market is poised for substantial growth and innovation over the coming decade.

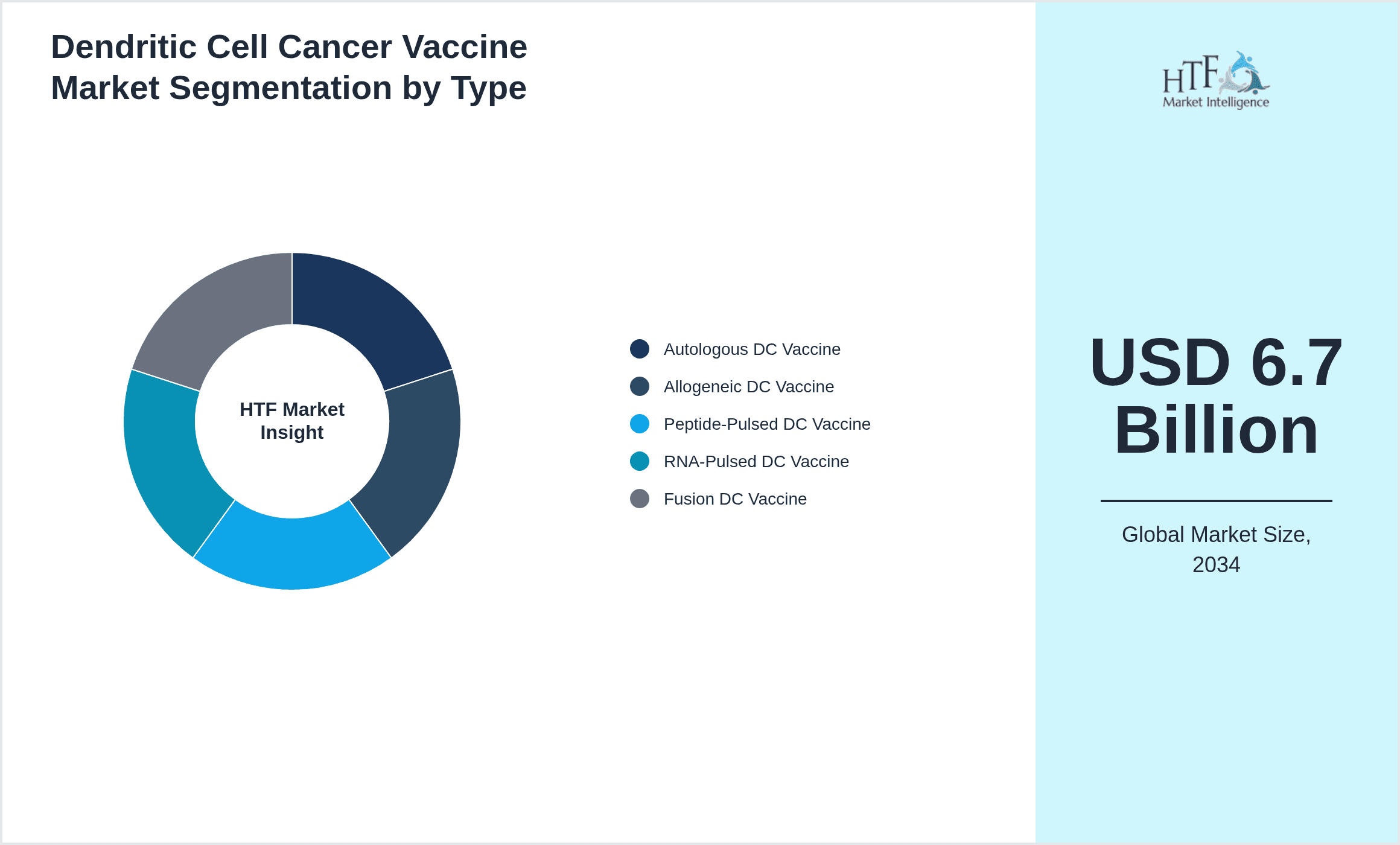

- •Key highlights of the market include a robust compound annual growth rate (CAGR) of approximately 13.6% projected through 2034, driven by technological advancements in dendritic cell manipulation and antigen presentation. The base market size was valued at USD 1.8 billion in 2024, with forecasts estimating growth to USD 6.7 billion by 2034, reflecting heightened adoption in both developed and emerging regions. North America holds a dominant share owing to advanced healthcare infrastructure, extensive R&D, and favorable reimbursement policies, while Asia-Pacific emerges as the fastest-growing region fueled by increasing cancer prevalence and expanding biopharmaceutical capabilities. The autologous dendritic cell vaccine segment leads the product spectrum due to personalized treatment efficacy, whereas RNA-pulsed vaccines exhibit the highest growth potential given their innovative design and scalable manufacturing. Market dynamics are also shaped by evolving regulatory frameworks, strategic partnerships, and rising patient awareness.

- •The strategic importance of the dendritic cell cancer vaccine market lies in its potential to revolutionize cancer treatment by offering highly specific, immune-mediated therapies that minimize systemic toxicity and improve long-term survival rates. This market is critical for pharmaceutical companies, biotechnology firms, healthcare providers, and policy makers aiming to address unmet clinical needs in oncology. By integrating cutting-edge technologies such as genetic engineering and personalized medicine, stakeholders can enhance therapeutic outcomes and drive sustainable growth. Moreover, the market offers significant value propositions through continuous innovation, expanded indications, and improved patient accessibility, positioning dendritic cell vaccines as a transformative force in global cancer care ecosystems.

Competitive Landscape

The competitive environment of the global dendritic cell cancer vaccine market is characterized by intense rivalry among biopharmaceutical innovators focusing on proprietary technologies, clinical trial advancements, and strategic collaborations. Market players employ differentiated approaches including personalized vaccine platforms, novel antigen-loading techniques, and combination therapies with immune checkpoint inhibitors to establish competitive advantages. Innovation in manufacturing scalability and regulatory compliance further influences market positioning, enabling companies to accelerate product approvals and commercial launches. Strategic partnerships, licensing agreements, and mergers & acquisitions are common, facilitating technology access and geographic expansion. Regional competition is marked by North American firms leading in R&D intensity and patent portfolios, while Asia-Pacific entities gain momentum through cost-effective production and growing clinical trial activities. Pricing strategies balance innovation costs with market penetration, supported by evolving reimbursement frameworks. The competitive landscape is expected to evolve with emerging players entering the market, emphasizing enhanced efficacy, safety, and patient-centric solutions, which collectively shape future market trajectories.

Companies Shaping the Dendritic Cell Cancer Vaccine Market

- •Dendreon Pharmaceuticals LLC (United States)

- •Argos Therapeutics, Inc. (United States)

- •Immunicum AB (Sweden)

- •Cellular Biomedicine Group, Inc. (United States)

- •Biontech SE (Germany)

- •Neon Therapeutics, Inc. (United States)

- •Cellectis SA (France)

- •Kite Pharma, Inc. (United States)

- •Immatics Biotechnologies GmbH (Germany)

- •Agenus Inc. (United States)

- •Medigene AG (Germany)

- •Immunocore Limited (United Kingdom)

- •Adaptimmune Therapeutics plc (United Kingdom)

- •MaxCyte, Inc. (United States)

- •OncoSec Medical Incorporated (United States)

- •Novartis AG (Switzerland)

- •Genentech, Inc. (United States)

- •Merck & Co., Inc. (United States)

- •Gritstone Oncology, Inc. (United States)

- •Neon Therapeutics, Inc. (United States)

- •ImmunoCellular Therapeutics, Ltd. (United States)

- •OncoImmunity AS (Norway)

- •BioNTech SE (Germany)

- •Arcellx, Inc. (United States)

- •Hoffmann-La Roche AG (Switzerland)

Market Breakdown

- •By Product Type

- ◦Autologous DC Vaccine

- ◦Allogeneic DC Vaccine

- ◦Peptide-Pulsed DC Vaccine

- ◦RNA-Pulsed DC Vaccine

- ◦Fusion DC Vaccine

- •By Application

- ◦Melanoma

- ◦Prostate Cancer

- ◦Lung Cancer

- ◦Breast Cancer

- ◦Other Cancers

- •By End-Use Industry

- ◦Hospitals

- ◦Cancer Research Institutes

- ◦Clinical Laboratories

- ◦Biopharmaceutical Companies

- •By Distribution Channel

- ◦Direct Sales

- ◦Specialty Clinics

- ◦Online Pharmacies

Growth Dynamics

- •The global dendritic cell cancer vaccine market is primarily driven by the increasing prevalence of cancer worldwide, which fuels demand for innovative and effective immunotherapies. Advances in biotechnology and personalized medicine have enabled the development of sophisticated dendritic cell vaccines that offer targeted treatment options, improving patient survival rates and quality of life. Additionally, supportive government initiatives and funding for cancer research bolster market growth by facilitating clinical trials and regulatory approvals. The rise in awareness among patients and healthcare providers about immunotherapy benefits further accelerates adoption. Technological improvements in dendritic cell isolation, antigen loading, and vaccine delivery methods enhance efficacy and scalability, contributing to market expansion. Collaborations between pharmaceutical companies and research institutions also play a pivotal role in advancing product pipelines and market penetration.

- •Emerging trends include the integration of dendritic cell vaccines with other immunotherapeutic agents such as checkpoint inhibitors and CAR-T therapies to create synergistic effects enhancing anti-tumor responses. Innovations in RNA-pulsed and peptide-pulsed vaccine platforms are gaining traction due to their customizable nature and potential for rapid development. Market players are increasingly focusing on off-the-shelf allogeneic vaccines to overcome challenges associated with autologous vaccine production. The adoption of artificial intelligence and machine learning in antigen identification and vaccine design is revolutionizing the development process. Furthermore, expanding clinical trial activities in Asia-Pacific and Latin America reflect growing regional interest and investment, signaling a shift toward more geographically diverse market growth.

- •Despite promising growth, the market faces restraints such as high manufacturing costs and complex production processes associated with dendritic cell vaccines, limiting widespread accessibility. Stringent regulatory requirements and the need for extensive clinical validation prolong product development timelines and increase financial risks for companies. The personalized nature of autologous vaccines poses logistical challenges, including the need for specialized facilities and trained personnel. Market penetration in low-income regions is hindered by infrastructure limitations and affordability issues. Additionally, variable patient responses and potential immune-related adverse events necessitate careful patient selection and monitoring, which can constrain adoption rates.

- •Opportunities abound in expanding indications beyond current cancers to include hematologic malignancies and rare tumors, broadening market scope. Advances in biomarker discovery and genomic profiling enable more precise patient stratification, enhancing vaccine efficacy and market appeal. Emerging economies present untapped markets with increasing healthcare expenditure and growing cancer awareness. The development of combination therapies integrating dendritic cell vaccines with chemotherapy, radiotherapy, or novel agents offers synergistic potential and new revenue streams. Licensing and strategic partnerships provide avenues for technology exchange, accelerated development, and geographic expansion. Furthermore, innovations in delivery platforms and manufacturing automation can reduce costs, improving market accessibility and scalability.

- •Challenges include navigating complex regulatory landscapes across multiple jurisdictions, which can delay market entry and increase compliance costs. Intellectual property disputes and patent expirations may impact competitive advantages and revenue streams. Ensuring consistent vaccine quality and potency amidst biological variability requires stringent quality control measures. Market fragmentation and competition from alternative immunotherapies such as checkpoint inhibitors and CAR-T cells intensify pressure on pricing and adoption. Additionally, educating healthcare professionals and patients about the benefits and limitations of dendritic cell vaccines remains essential to overcoming skepticism and achieving market acceptance.

Market Trends

- •A key trend in the dendritic cell cancer vaccine market is the increasing use of next-generation sequencing and bioinformatics to identify novel tumor antigens, enabling highly personalized vaccine development. This precision approach enhances immunogenicity and clinical outcomes, attracting significant research focus and investment. Concurrently, the market is witnessing a shift toward off-the-shelf vaccine products, improving manufacturing efficiency and reducing treatment delays. The integration of dendritic cell vaccines with immune checkpoint inhibitors is gaining popularity, reflecting a trend towards combination immunotherapies to overcome tumor immune evasion. Additionally, digital health technologies are being leveraged to monitor patient responses and optimize treatment regimens, improving clinical efficacy and patient engagement. These advancements collectively drive innovation and competitive differentiation in the market.

- •Biopharmaceutical companies are increasingly adopting collaboration models with academic institutions and contract research organizations to accelerate clinical development and regulatory approvals. This trend fosters knowledge sharing and resource optimization, reducing time-to-market. The rise of decentralized clinical trials and telemedicine has expanded patient access to dendritic cell vaccine therapies, particularly in remote regions. Sustainability considerations are influencing manufacturing practices, with companies exploring greener processes and supply chain transparency. Moreover, market players are focusing on expanding indications beyond solid tumors to hematologic cancers, reflecting evolving therapeutic landscapes and unmet medical needs. These trends point to a dynamic and adaptive market environment poised for sustained growth.

- •Strategic investments in artificial intelligence tools for antigen prediction and vaccine design are transforming research methodologies, enabling faster and more accurate vaccine candidates. Regulatory bodies are progressively establishing clearer guidelines for cell-based immunotherapies, facilitating smoother approval pathways. Emerging markets are witnessing increased government support and funding for cancer immunotherapies, catalyzing regional market expansion. Personalized medicine is becoming a central theme, with patient-specific vaccine formulations gaining traction. Furthermore, advancements in nanotechnology for vaccine delivery are enhancing dendritic cell targeting and antigen presentation efficiency, improving therapeutic outcomes. Collectively, these trends highlight the convergence of technology, regulation, and market demand shaping the future of dendritic cell cancer vaccines.

- •Digital platforms and social media are playing an influential role in disseminating information about dendritic cell vaccines, increasing patient awareness and demand. Market participants are harnessing real-world evidence and patient registries to demonstrate clinical value and support reimbursement negotiations. The adoption of standardized manufacturing protocols improves product consistency and regulatory compliance, fostering industry credibility. Collaborative ecosystems involving pharmaceutical firms, research centers, and healthcare providers are emerging to streamline vaccine development and commercialization. Moreover, pricing models are evolving towards value-based frameworks aligned with patient outcomes. These strategic trends underscore the market’s maturation and focus on sustainable growth.

- •Future directions include exploration of multi-antigen vaccines and neoantigen targeting to overcome tumor heterogeneity and immune escape mechanisms. Innovative adjuvant formulations are being developed to enhance dendritic cell activation and T-cell priming. The rise of personalized cancer vaccines incorporating patient-specific mutanomes reflects an advanced therapeutic frontier. Additionally, integration with emerging modalities such as oncolytic viruses and microbiome modulation is under investigation to potentiate immune responses. Regulatory harmonization efforts across regions aim to facilitate global clinical trial conduct and product approvals. These forward-looking trends position the dendritic cell cancer vaccine market for transformative growth and therapeutic impact.

Market Opportunities

- •Expanding the use of dendritic cell cancer vaccines into hematological malignancies presents a significant growth opportunity, leveraging the technology’s adaptability to various cancer types. This diversification can open new revenue streams and patient populations. Additionally, the rising adoption of combination therapies integrating dendritic cell vaccines with checkpoint inhibitors or chemotherapy enhances therapeutic efficacy, creating market demand for integrated treatment regimens. Emerging markets, especially in Asia-Pacific and Latin America, offer substantial growth potential due to increasing healthcare expenditure and cancer prevalence. Technological advancements enabling cost-effective manufacturing and off-the-shelf vaccine products improve accessibility and scalability. Strategic collaborations and licensing agreements facilitate entry into new geographic and therapeutic segments. Moreover, ongoing research into novel antigens and delivery platforms provides avenues for product innovation and differentiation, addressing unmet clinical needs and strengthening market positioning.

- •The integration of artificial intelligence and machine learning in vaccine design and patient selection enhances precision and accelerates development timelines, representing a lucrative opportunity. Government initiatives and funding aimed at cancer immunotherapy research create a favorable environment for market growth. Development of standardized manufacturing protocols and automation can reduce production costs and improve quality control, increasing profitability. Personalized medicine trends offer opportunities for tailored vaccine solutions, improving patient outcomes and satisfaction. Companies can capitalize on expanding indications beyond traditional solid tumors, exploring rare and refractory cancers. Furthermore, digital health platforms enable enhanced patient monitoring and engagement, supporting better clinical results and market differentiation. These opportunities collectively underscore the market’s potential for innovation-driven expansion.

- •Investment in educational campaigns targeting healthcare professionals and patients can increase market penetration by improving awareness and acceptance of dendritic cell vaccines. Leveraging real-world evidence and health economics data facilitates reimbursement negotiations and policy advocacy. Expansion into pediatric oncology and preventive cancer vaccines presents novel market segments. Partnerships with diagnostic companies can enable integrated cancer care solutions combining vaccines with biomarker-driven patient stratification. Additionally, exploring sustainable and eco-friendly manufacturing practices aligns with corporate social responsibility trends, enhancing brand reputation. The growing emphasis on global health equity opens avenues for deploying vaccines in underserved regions, supported by international health organizations and philanthropic funding. These strategic opportunities can drive long-term market growth and societal impact.

- •The development of multi-antigen and neoantigen vaccines addresses tumor heterogeneity challenges, enhancing clinical success rates and market differentiation. Advances in delivery technologies, including nanoparticles and electroporation, improve vaccine efficacy and patient compliance. The increasing prevalence of immune-related adverse event management protocols supports broader clinical adoption. Expanding clinical trial networks and decentralized trial models facilitate faster data generation and regulatory approvals. Additionally, leveraging big data analytics for patient response monitoring informs adaptive trial designs and personalized treatment adjustments. These opportunities foster innovation, competitive advantage, and enhanced patient-centered care in the dendritic cell cancer vaccine market.

- •Collaborations with academic institutions and government agencies can accelerate research and development efforts, reducing time-to-market. Licensing agreements for technology transfer enable market entrants to access cutting-edge platforms and expand product portfolios. Exploring biobanking and cell processing services offers ancillary revenue streams. The growing interest in immuno-oncology by venture capital and private equity investors provides financial resources for market expansion. Addressing regulatory harmonization challenges through proactive engagement can streamline approvals and market entry. These multifaceted opportunities position companies to capitalize on evolving market dynamics and technological advancements effectively.

Market Challenges

- •High production costs and complex manufacturing processes associated with dendritic cell cancer vaccines pose significant barriers to widespread adoption, limiting accessibility especially in low-resource settings. The personalized nature of autologous vaccines requires specialized facilities and skilled personnel, complicating scalability and supply chain logistics. Additionally, stringent regulatory requirements across multiple jurisdictions increase development timelines and compliance costs, impacting profitability. Market competition from alternative immunotherapies such as checkpoint inhibitors and CAR-T therapies intensifies pricing pressures and challenges differentiation. Variability in patient immune responses and potential adverse events necessitate careful patient selection and monitoring, complicating clinical management. Furthermore, limited awareness and skepticism among healthcare providers and patients hinder market penetration. Overcoming these challenges requires strategic investments in manufacturing innovation, regulatory navigation, education, and robust clinical evidence generation to ensure sustainable market growth.

- •Intellectual property disputes and patent expirations threaten competitive advantages and revenue streams, necessitating continuous innovation and portfolio diversification. The fragmented market landscape with numerous players creates high competition for clinical trial participants and reimbursement approvals. Inadequate reimbursement policies and healthcare infrastructure in emerging regions restrict market expansion. Challenges in standardizing vaccine quality and potency due to biological variability impact regulatory approvals and clinician confidence. Additionally, complex logistics involving cell collection, processing, and delivery increase operational risks and costs. The need for comprehensive patient data management and integration with healthcare systems adds further complexity. Addressing these multifaceted challenges is critical to unlocking the full commercial potential of dendritic cell cancer vaccines.

- •Rapidly evolving scientific knowledge and technological advancements require continuous adaptation of clinical protocols and manufacturing processes, which can strain resources. Limited long-term clinical data on efficacy and safety may impede regulatory approvals and physician acceptance. Market entry barriers due to high capital investment and expertise limit participation by smaller companies and startups. The ethical considerations surrounding personalized therapies and genetic manipulation necessitate transparent communication and regulatory oversight. Supply chain disruptions, particularly in the context of global health crises, pose risks to vaccine availability. Furthermore, reimbursement uncertainties and variable healthcare policies across regions complicate market forecasting and strategic planning. Navigating these challenges demands coordinated efforts among stakeholders to foster innovation and market sustainability.

- •Patient heterogeneity and tumor microenvironment complexity can reduce vaccine effectiveness, requiring combination therapies and personalized approaches that increase development complexity. Public perception and misinformation regarding immunotherapies may influence treatment acceptance. Data privacy and security concerns related to genetic and health information require robust safeguards. The competition from emerging therapeutic modalities, including gene editing and oncolytic viruses, adds to market rivalry. Additionally, achieving global regulatory harmonization is challenging due to diverse healthcare systems and standards. Addressing these challenges through multidisciplinary strategies and stakeholder collaboration is essential for the sustained success of the dendritic cell cancer vaccine market.

- •Logistical challenges related to cold chain management and timely vaccine delivery impact treatment continuity and patient outcomes. The necessity for personalized dosing and scheduling complicates clinical workflows and patient compliance. Limited availability of standardized biomarkers for patient stratification hampers optimal vaccine application. Financial constraints and reimbursement delays affect healthcare provider willingness to adopt these therapies. Adapting to evolving regulatory requirements and post-marketing surveillance obligations imposes additional operational burdens. Overcoming these challenges requires innovation in manufacturing, patient engagement, and policy advocacy to enhance market viability and therapeutic impact.

Regulatory Framework

- •Between 2019 and 2024, regulatory agencies globally have introduced comprehensive guidelines specifically addressing cell-based immunotherapies, including dendritic cell cancer vaccines. These regulations emphasize stringent quality control, safety evaluation, and efficacy demonstration through phased clinical trials. The FDA and EMA have implemented accelerated approval pathways and breakthrough therapy designations to expedite market access for promising therapies. Regulatory frameworks mandate detailed characterization of vaccine components, manufacturing consistency, and robust pharmacovigilance plans. Regional mandates require compliance with Good Manufacturing Practice (GMP) standards tailored to personalized therapies. Additionally, data protection and patient consent regulations have been reinforced to safeguard genetic and health information used in vaccine development. These evolving regulations have shaped clinical development strategies, ensuring patient safety while fostering innovation and market growth in the dendritic cell cancer vaccine sector.

- •The introduction of harmonized international guidelines by the International Council for Harmonisation (ICH) has facilitated global clinical trial conduct and regulatory submissions. Regulatory agencies increasingly encourage adaptive trial designs and real-world evidence to support approval decisions. Post-marketing monitoring requirements have been expanded to capture long-term safety and efficacy data. Countries in Asia-Pacific have strengthened their regulatory frameworks aligning with global standards, enabling faster entry of innovative vaccines. Orphan drug designations and incentives for rare cancer indications have been extended to include dendritic cell vaccines. The evolving policy landscape underscores the importance of regulatory intelligence and proactive engagement by market participants to navigate compliance and optimize product approvals.

- •Safety standards have been enhanced to address potential immunogenicity and autoimmunity risks associated with dendritic cell vaccines. Environmental and operational guidelines focus on minimizing contamination risks during cell processing. Specific requirements for labeling, packaging, and cold chain logistics ensure product integrity throughout distribution. Regulatory authorities have increased scrutiny on clinical trial patient selection criteria to ensure representative and ethical study populations. Government support programs and funding initiatives have been established to accelerate innovative cancer vaccine development and commercialization. These regulatory developments collectively provide a structured framework that balances innovation with patient protection, driving sustainable growth in the dendritic cell cancer vaccine market.

- •Region-specific mandates include the FDA’s guidance on individualized cellular therapy products and the EMA’s advanced therapy medicinal product (ATMP) regulations, both updated from 2019 to 2024. These mandates require detailed documentation of manufacturing processes, clinical data, and risk management plans. The Chinese National Medical Products Administration (NMPA) has introduced streamlined approval processes for immunotherapeutics, promoting domestic innovation. Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) supports conditional early approvals for innovative therapies, enhancing market access. Collaborative regulatory initiatives across countries aim to harmonize standards and reduce approval redundancies, facilitating global commercialization strategies for dendritic cell vaccines.

- •Government policy frameworks increasingly incentivize research and development through grants, tax benefits, and public-private partnerships. Health technology assessment (HTA) bodies are incorporating patient-reported outcomes and quality-of-life metrics in reimbursement evaluations. Regulatory agencies emphasize transparent communication and stakeholder engagement during product development. International collaborations on regulatory science are fostering the development of standardized assays and biomarkers, supporting consistent clinical evaluation. These policy measures support the sustainable growth and integration of dendritic cell cancer vaccines into mainstream oncology care worldwide.

Market Intelligence

- •15th March 2024, Dendreon Pharmaceuticals LLC announced the commercial launch of its new autologous dendritic cell vaccine targeting advanced melanoma, featuring enhanced antigen loading technology to improve immune activation. This product incorporates innovative adjuvant formulations aimed at boosting T-cell responses, offering an alternative to conventional therapies. The launch is supported by positive Phase III clinical trial data demonstrating improved progression-free survival and tolerability profiles. Dendreon has established a strategic partnership with leading oncology centers across North America to facilitate patient access and real-world data collection, positioning the vaccine as a key player in personalized cancer immunotherapy. This advancement underscores the company’s commitment to innovation and market leadership in dendritic cell vaccine therapeutics. Source: Official company press release

- •22nd August 2023, Biontech SE introduced an RNA-pulsed dendritic cell vaccine platform designed for rapid customization against multiple tumor antigens. The technology leverages proprietary mRNA synthesis and delivery mechanisms to stimulate robust antigen-specific immune responses. Early clinical studies in lung and breast cancer patients have shown promising immunogenicity and safety results. Biontech’s innovation aims to overcome limitations of traditional peptide-based vaccines by enabling scalable manufacturing and off-the-shelf availability. The company plans to initiate pivotal trials across Europe and Asia-Pacific in late 2024, targeting broad market penetration. This development reflects growing industry focus on RNA-based immunotherapies and personalized cancer vaccines. Source: Company website announcement

- •30th November 2024, Immunicum AB announced a strategic collaboration with a major biopharmaceutical company to co-develop combination therapies involving dendritic cell vaccines and immune checkpoint inhibitors. The alliance will leverage Immunicum’s expertise in allogeneic vaccine production and partner’s global commercial infrastructure to accelerate market entry. Joint clinical trials are planned for melanoma and prostate cancer indications, aiming to enhance therapeutic efficacy through synergistic immune modulation. This partnership exemplifies the trend of biopharma collaborations to expand immunotherapy portfolios and address complex oncologic challenges. The initiative is expected to drive innovation and competitive positioning in the global dendritic cell cancer vaccine market. Source: Industry publication

- •10th February 2025, Cellular Biomedicine Group, Inc. completed the expansion of its manufacturing facility dedicated to dendritic cell vaccine production, incorporating automated cell processing systems to increase capacity and reduce costs. This investment supports growing demand in the Asia-Pacific region and aims to enhance supply chain reliability and product consistency. The upgraded facility complies with international GMP standards, facilitating regulatory approvals and enabling faster commercial scale-up. Cellular Biomedicine Group’s expansion signals increased regional market focus and commitment to advancing dendritic cell vaccine accessibility. The company also plans to launch new clinical trials targeting hematologic malignancies in 2025. Source: Company website

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 6.7 Billion |

| CAGR | 13.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 13.6% |

| Scope of Report | Market is segmented by Product Type (Autologous DC Vaccine, Allogeneic DC Vaccine, Peptide-Pulsed DC Vaccine, RNA-Pulsed DC Vaccine, Fusion DC Vaccine), Application (Melanoma, Prostate Cancer, Lung Cancer, Breast Cancer, Other Cancers), End-Use Industry (Hospitals, Cancer Research Institutes, Clinical Laboratories, Biopharmaceutical Companies), Distribution Channel (Direct Sales, Specialty Clinics, Online Pharmacies) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Dendreon Pharmaceuticals LLC (United States), Argos Therapeutics, Inc. (United States), Immunicum AB (Sweden), Cellular Biomedicine Group, Inc. (United States), Biontech SE (Germany), Neon Therapeutics, Inc. (United States), Cellectis SA (France), Kite Pharma, Inc. (United States), Immatics Biotechnologies GmbH (Germany), Agenus Inc. (United States), Medigene AG (Germany), Immunocore Limited (United Kingdom), Adaptimmune Therapeutics plc (United Kingdom), MaxCyte, Inc. (United States), OncoSec Medical Incorporated (United States), Novartis AG (Switzerland), Genentech, Inc. (United States), Merck & Co., Inc. (United States), Gritstone Oncology, Inc. (United States), Neon Therapeutics, Inc. (United States), ImmunoCellular Therapeutics, Ltd. (United States), OncoImmunity AS (Norway), BioNTech SE (Germany), Arcellx, Inc. (United States), Hoffmann-La Roche AG (Switzerland) |

Global Dendritic Cell Cancer Vaccine Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.