North America Radiation Shielding Windows Market - Outlook 2025-2034

North America Radiation Shielding Windows Market is segmented by Type (Lead Glass, Acrylic Radiation Shielding Windows, Laminated Glass Shielding, Polycarbonate Shielding Windows, Borosilicate Glass Radiation Shielding), Application (Medical Imaging, Nuclear Power Plants, Research Laboratories, Industrial Radiography, Aerospace), End-Use Industry (Healthcare, Energy & Power, Industrial Manufacturing, Defense & Aerospace), Distribution Channel (Direct Sales, Distributors, System Integrators), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

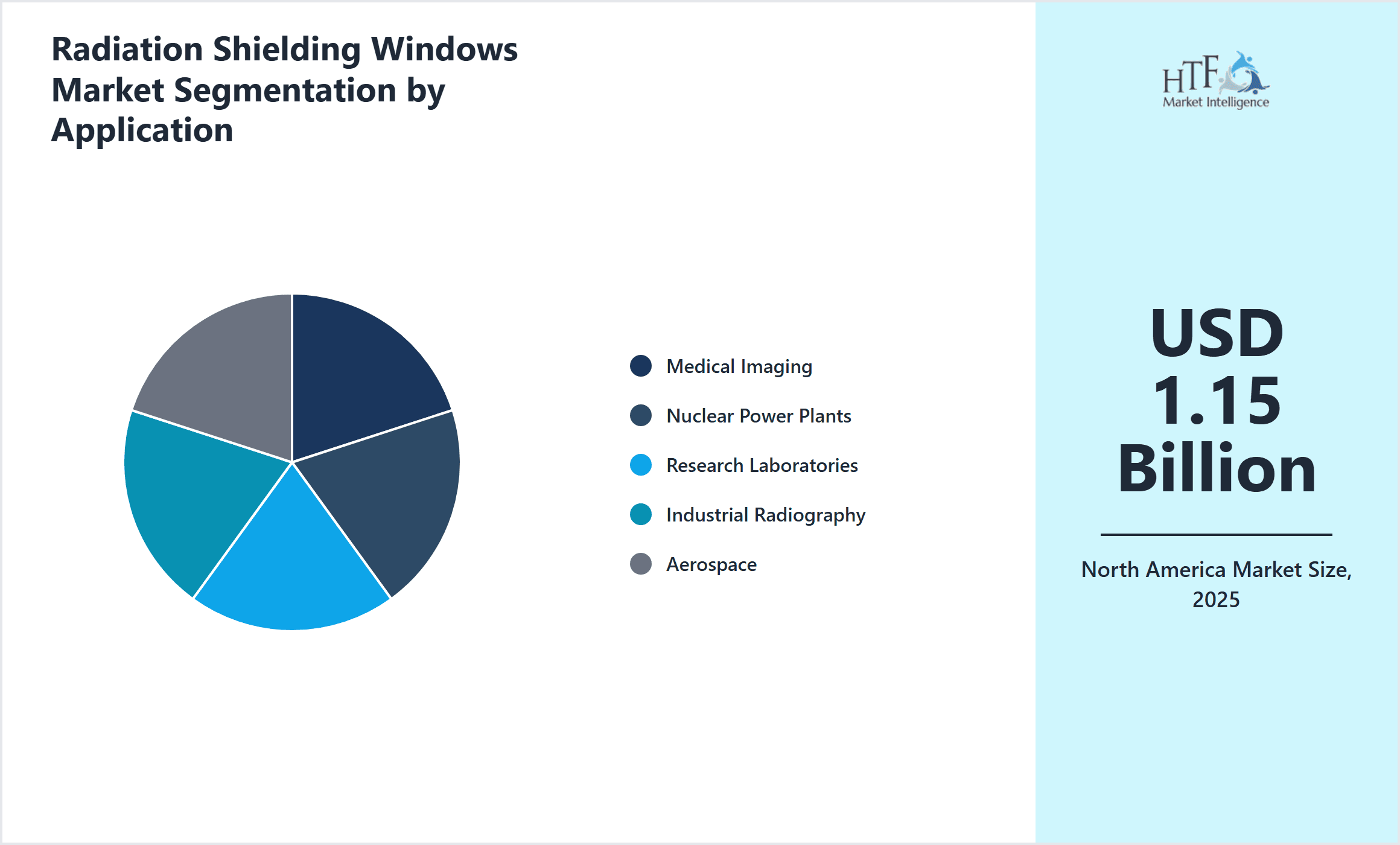

- •The North America Radiation Shielding Windows Market is a specialized segment focused on protective glazing solutions designed to shield personnel and sensitive environments from ionizing radiation exposure. The market caters to critical sectors including healthcare, nuclear energy, research, and aerospace, where radiation safety is paramount. Products in this market range from lead glass to polycarbonate variants, each engineered to balance transparency and shielding efficacy. The scope extends across installations for diagnostic imaging rooms, nuclear reactors, industrial radiography sites, and aerospace testing facilities. With growing regulatory emphasis on radiation protection and increasing investments in healthcare infrastructure, the market is poised for robust growth. Key characteristics include adherence to stringent safety standards, innovation in material science to improve clarity and durability, and customization to suit various radiation intensities and application scenarios. Primary use cases emphasize safeguarding operators and equipment while maintaining operational visibility, driving technological evolution and market expansion in North America.

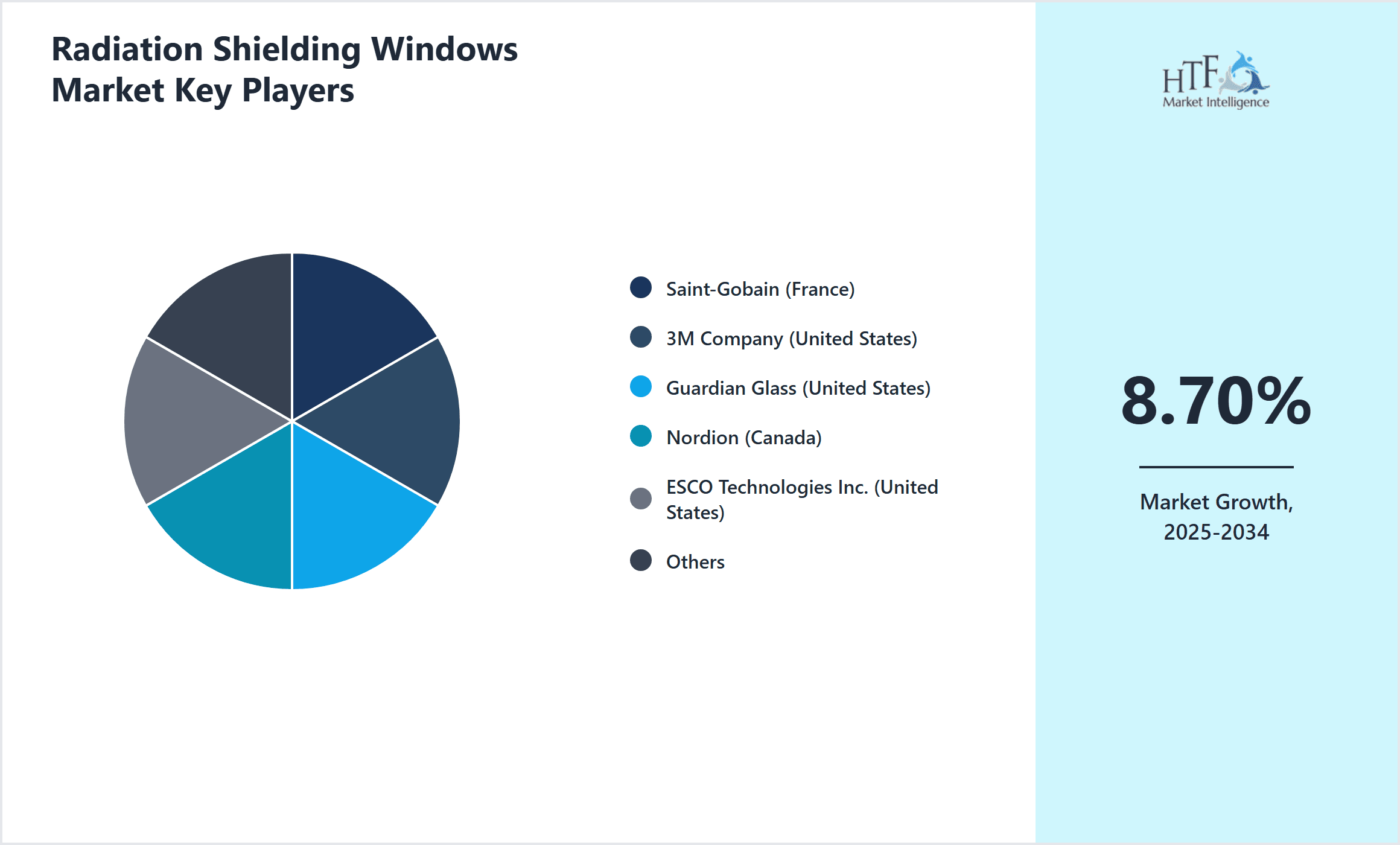

- •The market is projected to grow from USD 1.15 Billion in 2025 to USD 2.45 Billion by 2034, reflecting a compound annual growth rate (CAGR) of approximately 8.7%. Lead glass remains the dominant product type, accounting for the largest market share due to its proven effectiveness and widespread acceptance. Medical imaging applications lead demand, driven by increased diagnostic procedures and infrastructural upgrades. The United States dominates the regional market, supported by advanced healthcare facilities and nuclear power infrastructure, while Canada is identified as the fastest growing country within North America owing to expanding research and industrial activities. Market growth is fueled by advancements in radiation shielding materials, rising awareness of radiation hazards, and stricter compliance with health and safety regulations. Year-over-year growth rates align closely with the CAGR, indicating steady expansion across all major market segments.

- •The North America Radiation Shielding Windows Market offers significant strategic value to stakeholders including manufacturers, healthcare providers, nuclear operators, and regulatory bodies. The market’s growth supports enhanced occupational safety and environmental protection, aligning with public health mandates and radiation control protocols. Technological innovations in shielding materials and window designs provide competitive advantages and address emerging application needs. Investment in research and development drives product differentiation, while adherence to evolving regulations ensures market access and sustains industry credibility. The expanding demand for transparent shielding solutions further integrates with digital imaging and radiation monitoring trends, offering comprehensive safety ecosystems. Overall, the market’s trajectory underscores its critical role in safeguarding human health and operational integrity amid rising applications of radiation technology in North America.

Competitive Landscape

Competition within the North America Radiation Shielding Windows Market is characterized by a mix of established multinational corporations and specialized regional manufacturers focusing on innovation, quality, and regulatory compliance. Leading players leverage advanced material science to develop windows with superior radiation attenuation and optical clarity, differentiating through proprietary glass formulations and hybrid composites. Strategic partnerships with healthcare providers and nuclear facilities enhance market penetration and customization capabilities. Companies adopt competitive pricing strategies and diversified product portfolios to address varied application requirements across medical, industrial, and aerospace sectors. Innovation in lightweight and lead-free shielding materials is a focal point, responding to environmental concerns and operational efficiency demands. Market rivalry intensifies with the entrance of new players emphasizing cost-effective solutions and digital integration for radiation monitoring. Distribution channels including direct sales, system integrators, and authorized dealers are optimized for extensive geographic reach. Future competitive dynamics will likely revolve around technological breakthroughs, sustainability initiatives, and regional expansion strategies, shaping market leadership and growth trajectories in North America.

Leading Companies in Radiation Shielding Windows Market

- •Saint-Gobain (France)

- •3M Company (United States)

- •Guardian Glass (United States)

- •Nordion (Canada)

- •ESCO Technologies Inc. (United States)

- •Radiation Protection Products Inc. (United States)

- •Nukem Technologies (Germany)

- •Nihon Glass Industry Co. Ltd. (Japan)

- •American Glass Products (United States)

- •Marmon/Keystone (United States)

- •Ray-Bar Engineering (United States)

- •Schott AG (Germany)

- •Material Sciences Corporation (United States)

- •Laird Performance Materials (United Kingdom)

- •Hitachi Chemical (Japan)

- •Toshiba Corporation (Japan)

- •General Electric Company (United States)

- •Ceradyne, Inc. (United States)

- •Plexiglas (Germany)

- •Lumicor (United States)

- •China Jingcheng Group (China)

- •Kuraray Co. Ltd. (Japan)

- •Borosil Limited (India)

- •AGC Inc. (Japan)

- •Shanghai Glass Group (China)

Market Breakdown

- •By Type

- ◦Lead Glass

- ◦Acrylic Radiation Shielding Windows

- ◦Laminated Glass Shielding

- ◦Polycarbonate Shielding Windows

- ◦Borosilicate Glass Radiation Shielding

- •By Application

- ◦Medical Imaging

- ◦Nuclear Power Plants

- ◦Research Laboratories

- ◦Industrial Radiography

- ◦Aerospace

- •By End-Use Industry

- ◦Healthcare

- ◦Energy & Power

- ◦Industrial Manufacturing

- ◦Defense & Aerospace

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦System Integrators

Growth Dynamics

- •Increasing demand for advanced medical imaging procedures in North America is a primary growth driver, as hospitals and diagnostic centers upgrade facilities with high-performance radiation shielding windows to ensure safety and compliance. The surge in diagnostic imaging volumes, particularly in MRI and X-ray, has amplified the need for specialized protective glazing.

- •Technological innovations focusing on lead-free and lightweight radiation shielding materials are accelerating market growth by addressing environmental concerns and enhancing ease of installation. Polycarbonate and acrylic composites have gained traction due to improved durability and transparency, expanding application scope.

- •Government regulations and stringent safety standards in North America mandate the use of certified radiation shielding products, driving adoption across nuclear power plants and research laboratories. Regulatory compliance acts as a catalyst for market penetration and product development.

- •Rising investments in nuclear energy infrastructure and aerospace research facilities in the region are creating new opportunities for radiation shielding window manufacturers to supply specialized solutions tailored to high-radiation environments.

- •Increasing awareness of occupational health and safety among healthcare and industrial workers encourages upgrades and replacements of existing shielding solutions, contributing to sustained market demand.

Market Trends

- •The adoption of eco-friendly, lead-free radiation shielding materials is gaining momentum, aligning with broader sustainability goals and regulatory pressures to reduce toxic substance usage in construction and medical equipment.

- •Integration of smart window technologies with radiation sensors and digital monitoring systems is an emerging trend, enhancing real-time safety management in critical radiation environments.

- •Customized radiation shielding window solutions designed for modular and mobile medical units are increasingly sought after, reflecting the growth of portable diagnostic services in remote and emergency settings.

- •Collaborations between glass manufacturers and healthcare technology firms are fostering innovation in high-transparency, high-shielding composite materials, improving user experience and operational efficiency.

- •Market players are investing in research to develop multi-functional shielding windows that combine radiation protection with thermal insulation and acoustic dampening, catering to holistic building performance requirements.

Market Opportunities

- •Expansion into emerging nuclear power projects and decommissioning facilities in North America offers significant growth prospects for radiation shielding window manufacturers, as these installations require updated protective solutions.

- •Development of lightweight, portable shielding windows can open new market segments in mobile healthcare and defense applications, where ease of transport and rapid deployment are critical.

- •Rising demand for radiation shielding in aerospace testing and satellite manufacturing presents novel application avenues, encouraging innovation in materials suited for extreme environments.

- •Government incentives and funding for healthcare infrastructure modernization provide opportunities to integrate advanced shielding technologies into new and retrofit construction projects.

- •Strategic partnerships with construction firms and medical equipment providers can facilitate bundled offerings, enhancing market reach and customer loyalty.

Market Challenges

- •High production costs associated with advanced radiation shielding materials and the complexity of custom manufacturing processes limit price competitiveness and market penetration in cost-sensitive segments.

- •Stringent regulatory approval processes and certification requirements can delay product launches and increase compliance costs, especially for innovative or novel shielding materials.

- •Limited awareness in smaller medical facilities and industrial units about the importance of updated radiation shielding solutions restricts market expansion beyond major urban centers.

- •Competition from alternative radiation protection technologies, such as wall-mounted shields and portable barriers, poses substitution threats to window-based shielding solutions.

- •Supply chain disruptions and raw material price volatility can impact production schedules and profitability, complicating long-term strategic planning for manufacturers.

Regulatory Framework

- •Between 2020 and 2025, the U.S. Nuclear Regulatory Commission updated radiation protection standards requiring enhanced shielding verification for all nuclear facility windows, mandating stricter testing and certification protocols to ensure occupational safety.

- •The Food and Drug Administration (FDA) revised medical imaging facility guidelines in 2022, specifying minimum shielding requirements for diagnostic rooms, leading to increased demand for certified radiation shielding windows in healthcare settings.

- •Environmental Protection Agency regulations enacted in 2021 emphasize the reduction of lead usage in construction materials, encouraging manufacturers to innovate lead-free radiation shielding alternatives to meet compliance.

- •Canadian Nuclear Safety Commission introduced updated radiation safety protocols in 2023 that require periodic inspection and replacement of shielding materials in research laboratories, promoting market growth in Canada.

- •Occupational Safety and Health Administration regulations tightened in 2024, increasing enforcement of radiation exposure limits in industrial radiography sites, driving adoption of high-performance shielding windows.

Market Intelligence

- •15th January 2025, Saint-Gobain launched a new line of eco-friendly lead-free radiation shielding windows incorporating advanced borosilicate composites. These windows provide enhanced optical clarity and superior radiation attenuation while meeting stringent environmental standards. Targeted at medical and nuclear sectors, the product aims to replace traditional lead glass, addressing both safety and sustainability concerns. Saint-Gobain's strategic objective focuses on expanding its market share in North America by leveraging regulatory trends favoring lead-free materials and responding to growing demand from healthcare infrastructure modernization projects. The launch includes comprehensive certification ensuring compliance with NRC and FDA requirements, positioning the company as a technology leader. Source: Official Saint-Gobain Press Release

- •23rd March 2025, 3M Company introduced a novel polycarbonate radiation shielding window designed for aerospace and defense applications. The product features lightweight construction and superior impact resistance, enabling deployment in harsh operational environments. It integrates advanced anti-reflective coatings to optimize visibility and incorporates embedded radiation sensors for real-time exposure monitoring. 3M aims to capitalize on increasing aerospace research activities in North America, aligning with government investments and technological innovation trends. This launch enhances 3M’s portfolio by addressing emerging requirements for multifunctional shielding solutions combining safety and operational efficiency. Source: 3M Official Announcement

- •10th February 2025, Radiation Protection Products Inc. announced a strategic partnership with leading healthcare construction firms to supply custom-designed radiation shielding window solutions for new hospital builds and imaging center upgrades across the United States. This collaboration focuses on integrating high-performance lead glass products with advanced installation services, streamlining project delivery timelines and ensuring regulatory compliance. The initiative is expected to boost market penetration by addressing complex architectural requirements and enhancing end-user satisfaction. Radiation Protection Products Inc. leverages this partnership to strengthen its distribution network and establish long-term contracts within the expanding North American healthcare infrastructure sector. Source: Radiation Protection Products Corporate Communications

- •7th April 2025, Guardian Glass expanded its North American manufacturing capacity for laminated radiation shielding glass to meet rising demand from nuclear power and industrial sectors. The expansion includes state-of-the-art production lines incorporating automated quality control systems and environmentally sustainable processes. Guardian’s investment supports faster delivery times and product customization capabilities, reinforcing its competitive position. The company anticipates capturing significant market share growth by addressing supply chain challenges and fulfilling large-scale infrastructure projects requiring certified shielding solutions. This strategic move aligns with regional energy development plans and regulatory mandates for enhanced radiation protection. Source: Guardian Glass Annual Report 2025

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.15 Billion |

| Forecast Year Market Size | USD 2.45 Billion |

| CAGR | 8.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.4% |

| Scope of Report | Market is segmented by Type (Lead Glass, Acrylic Radiation Shielding Windows, Laminated Glass Shielding, Polycarbonate Shielding Windows, Borosilicate Glass Radiation Shielding), Application (Medical Imaging, Nuclear Power Plants, Research Laboratories, Industrial Radiography, Aerospace), End-Use Industry (Healthcare, Energy & Power, Industrial Manufacturing, Defense & Aerospace), Distribution Channel (Direct Sales, Distributors, System Integrators) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Saint-Gobain (France), 3M Company (United States), Guardian Glass (United States), Nordion (Canada), ESCO Technologies Inc. (United States), Radiation Protection Products Inc. (United States), Nukem Technologies (Germany), Nihon Glass Industry Co. Ltd. (Japan), American Glass Products (United States), Marmon/Keystone (United States), Ray-Bar Engineering (United States), Schott AG (Germany), Material Sciences Corporation (United States), Laird Performance Materials (United Kingdom), Hitachi Chemical (Japan), Toshiba Corporation (Japan), General Electric Company (United States), Ceradyne, Inc. (United States), Plexiglas (Germany), Lumicor (United States), China Jingcheng Group (China), Kuraray Co. Ltd. (Japan), Borosil Limited (India), AGC Inc. (Japan), Shanghai Glass Group (China) |

North America Radiation Shielding Windows Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.