Calcium Channel Blocker Market - Europe Size & Outlook 2020-2034

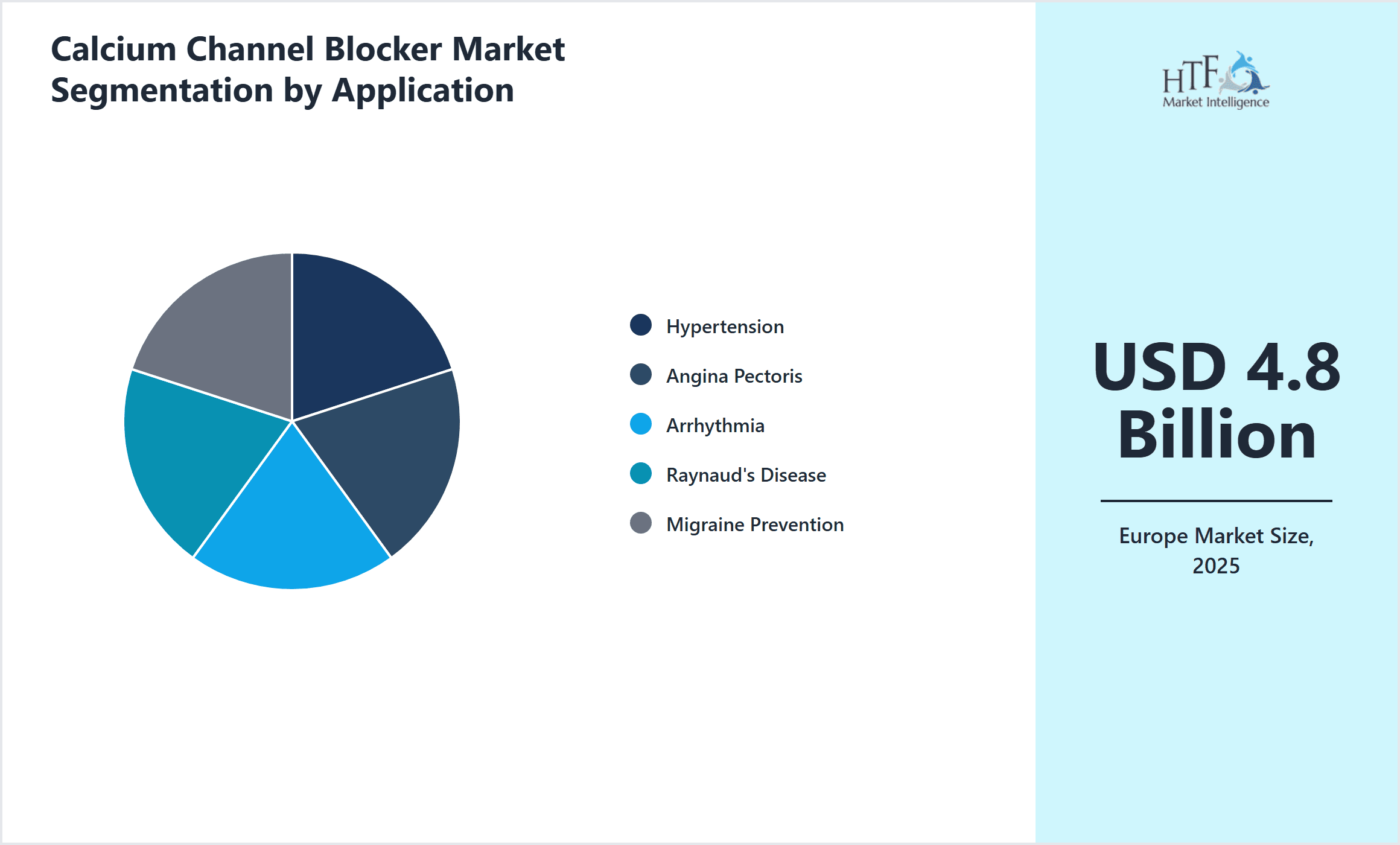

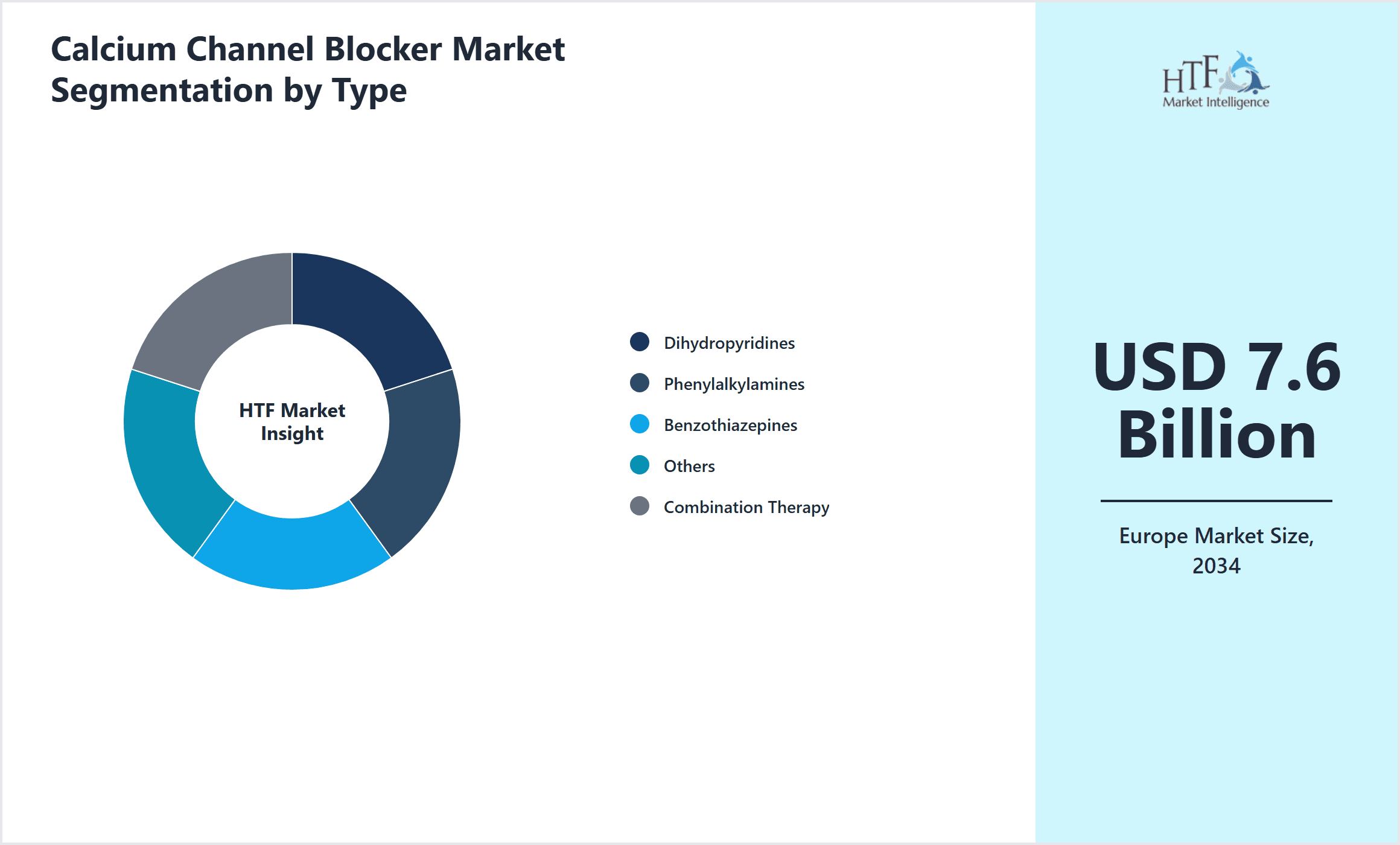

Europe Calcium Channel Blocker Market is segmented by Product Type (Dihydropyridines, Phenylalkylamines, Benzothiazepines, Others, Combination Therapy), Application (Hypertension, Angina Pectoris, Arrhythmia, Raynaud's Disease, Migraine Prevention), End-Use Industry (Hospitals, Clinics, Outpatient Care Centers, Retail Pharmacies), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Calcium Channel Blocker market primarily comprises pharmaceutical agents designed to regulate calcium ion flow through cardiac and vascular smooth muscle cells, offering therapeutic benefits in cardiovascular diseases including hypertension, angina, and arrhythmias. This market covers a diverse range of drug types such as dihydropyridines, phenylalkylamines, benzothiazepines, and combination therapies, each with distinct clinical profiles and indications. Applications extend to managing hypertension, alleviating angina pectoris, stabilizing cardiac rhythm disturbances, treating Raynaud's phenomenon, and preventing migraines. The value chain integrates raw material sourcing, drug formulation, regulatory compliance, distribution through wholesalers and pharmacies, and administration by healthcare professionals. Market growth is driven by the high prevalence of cardiovascular disorders in the aging European population, advancements in drug formulations improving patient compliance, and increasing adoption in outpatient settings. Regulatory frameworks across European countries impact market dynamics, ensuring drug safety and efficacy. The competitive landscape features both multinational pharmaceutical companies and regional generic drug manufacturers, fostering innovation and pricing competition. Strategic importance lies in the market's role in reducing cardiovascular morbidity and mortality, making it critical for healthcare systems and investors focused on pharmaceutical and healthcare sectors.

- •Key highlights include a base market size of USD 4.8 billion in 2025, with projections estimating growth to USD 7.6 billion by 2034, reflecting a CAGR of 5.6%. Germany leads the market in terms of revenue, attributable to its advanced healthcare infrastructure and high patient awareness. Poland is identified as the fastest growing country, driven by improving healthcare access and rising cardiovascular disease prevalence. Dihydropyridines maintain dominance as the leading product type due to their established efficacy and widespread clinical use, while combination therapy is the fastest growing segment, reflecting evolving treatment paradigms emphasizing multi-drug regimens for enhanced outcomes.

- •The Europe Calcium Channel Blocker market offers significant value propositions to healthcare providers, including improved management of complex cardiovascular conditions, reduced hospitalizations, and enhanced patient quality of life. For pharmaceutical companies and investors, the market presents robust growth opportunities driven by demographic trends, innovation in drug delivery systems, and expanding indications. Policymakers also benefit from improved population health outcomes and cost-effective treatment alternatives. Overall, the market’s strategic importance is underscored by its contribution to reducing the cardiovascular disease burden, a leading cause of morbidity and mortality in Europe.

Competitive Landscape

The Europe Calcium Channel Blocker market features a competitive environment characterized by both multinational pharmaceutical companies and emerging regional manufacturers. Market dynamics are influenced by patent expirations, generic drug penetration, and the continuous innovation of combination therapies designed to enhance therapeutic efficacy and patient adherence. Companies employ diverse competitive strategies including extensive R&D investment, strategic partnerships, and mergers and acquisitions to consolidate market presence and expand their product portfolios. Market positioning is often strengthened through differentiated drug formulations and targeted marketing efforts to healthcare professionals. Pricing strategies balance affordability with innovation incentives, while distribution channels include direct hospital sales, pharmacy networks, and online platforms. Technology adoption such as advanced drug delivery systems and digital patient monitoring is gaining traction, providing competitive advantages. Barriers to entry include stringent regulatory compliance and high development costs, which protect established players but also encourage continuous innovation. Regional competition varies with Western European countries exhibiting mature markets and Eastern European countries showing rapid growth, indicating evolving opportunities. Future competitive trends suggest increased focus on personalized medicine approaches and integration of digital health technologies to optimize cardiovascular disease management.

Key Participants in Calcium Channel Blocker Market

- •Pfizer Inc. (United States)

- •Novartis AG (Switzerland)

- •Bayer AG (Germany)

- •Sanofi S.A. (France)

- •AstraZeneca PLC (United Kingdom)

- •Teva Pharmaceutical Industries Ltd. (Israel)

- •Mylan N.V. (United States)

- •Fresenius SE & Co. KGaA (Germany)

- •Servier Laboratories (France)

- •Sandoz International GmbH (Switzerland)

- •Ipsen S.A. (France)

- •STADA Arzneimittel AG (Germany)

- •Recordati S.p.A. (Italy)

- •Lupin Limited (India)

- •Sun Pharmaceutical Industries Ltd. (India)

- •Zentiva Group (Czech Republic)

- •Chiesi Farmaceutici S.p.A. (Italy)

- •H. Lundbeck A/S (Denmark)

- •Meda AB (Sweden)

- •Gedeon Richter Plc (Hungary)

- •Orion Corporation (Finland)

- •Almirall S.A. (Spain)

- •Siegfried Holding AG (Switzerland)

- •Biocodex (France)

- •Recordati Rare Diseases (Italy)

Market Breakdown

- •By Product Type

- ◦Dihydropyridines

- ◦Phenylalkylamines

- ◦Benzothiazepines

- ◦Others

- ◦Combination Therapy

- •By Application

- ◦Hypertension

- ◦Angina Pectoris

- ◦Arrhythmia

- ◦Raynaud's Disease

- ◦Migraine Prevention

- •By End-Use Industry

- ◦Hospitals

- ◦Clinics

- ◦Outpatient Care Centers

- ◦Retail Pharmacies

- •By Distribution Channel

- ◦Hospital Pharmacies

- ◦Retail Pharmacies

- ◦Online Pharmacies

Growth Dynamics

- •The increasing prevalence of cardiovascular diseases, especially hypertension and angina, across the aging European population is a primary growth driver for the Calcium Channel Blocker market. Government healthcare initiatives promoting early diagnosis and treatment have further accelerated market expansion.

- •Advancements in pharmaceutical technology leading to the development of combination therapies have improved patient adherence and treatment outcomes, thereby driving market growth significantly in recent years.

- •Rising awareness among healthcare professionals and patients regarding the benefits of Calcium Channel Blockers for managing complex cardiovascular conditions has increased prescription rates across Europe.

- •Expanding outpatient care services and growing accessibility to retail and online pharmacies have enhanced the availability and convenience of Calcium Channel Blocker therapies, contributing to market growth.

- •Supportive regulatory policies and inclusion of Calcium Channel Blockers in national essential medicines lists have enabled wider adoption and reimbursement, reinforcing market expansion.

Market Trends

- •There is a significant trend toward the development and adoption of combination therapies that integrate Calcium Channel Blockers with other antihypertensive agents to enhance therapeutic efficacy and reduce pill burden.

- •Pharmaceutical companies are increasingly investing in sustained-release formulations of Calcium Channel Blockers to improve patient compliance and minimize side effects.

- •Digital health solutions, including telemedicine and remote patient monitoring, are being integrated with Calcium Channel Blocker treatment regimens to optimize outcomes and adherence.

- •Market players are focusing on expanding their presence in emerging Eastern European countries, where rising cardiovascular disease prevalence is creating new demand.

Market Opportunities

- •Emerging markets within Eastern Europe offer significant growth opportunities due to increasing healthcare infrastructure investments and rising prevalence of cardiovascular conditions.

- •Innovation in drug delivery systems, such as transdermal patches and novel oral formulations, presents opportunities to enhance patient experience and expand market share.

- •Expanding indications of Calcium Channel Blockers in conditions like migraine prevention and Raynaud's disease can open new application segments and revenue streams.

- •Strategic partnerships and licensing agreements between multinational and regional pharmaceutical companies can facilitate market penetration and accelerate product launches.

Market Challenges

- •Patent expirations have led to increased generic competition, exerting pricing pressure and squeezing profit margins for branded Calcium Channel Blocker products.

- •Stringent regulatory requirements across different European countries prolong the drug approval process, delaying market entry and increasing development costs.

- •Variability in healthcare reimbursement policies and pricing controls across Europe can limit market access and affect sales volumes in certain countries.

- •Patient adherence issues due to side effects and complex medication regimens remain a challenge, impacting treatment outcomes and market growth potential.

Regulatory Framework

- •The European Medicines Agency (EMA) implemented revised guidelines between 2020 and 2025 focusing on enhanced safety monitoring and post-marketing surveillance of Calcium Channel Blockers, ensuring higher patient safety standards and better risk management.

- •The EU Clinical Trials Regulation (Regulation (EU) No 536/2014) became fully applicable in 2022, streamlining clinical trial approvals and promoting transparency for new drug candidates including Calcium Channel Blockers.

- •Various countries within Europe have adopted national policies mandating inclusion of essential cardiovascular drugs, including Calcium Channel Blockers, in reimbursement lists, improving patient access while controlling healthcare costs.

- •Regulatory requirements for bioequivalence studies were harmonized across Europe between 2020 and 2025, facilitating generic drug approvals and market entry for Calcium Channel Blocker generics.

- •The EU’s pharmacovigilance legislation has been strengthened with stricter adverse event reporting obligations for pharmaceutical companies, impacting post-approval monitoring and compliance strategies for Calcium Channel Blockers.

Market Intelligence

- •15th January 2025, Novartis AG announced the launch of a novel sustained-release combination therapy integrating dihydropyridine Calcium Channel Blockers with ACE inhibitors, targeting hypertension patients with improved efficacy and adherence. The new formulation, developed through advanced pharmaceutical technologies, aims to reduce cardiovascular events and hospitalizations. Novartis plans a phased rollout across major European countries with expected regulatory approvals completed in late 2024. This strategic launch is poised to address unmet patient needs while strengthening the company's cardiovascular portfolio. Source: Novartis Official Press Release

- •10th March 2025, Bayer AG introduced an innovative transdermal patch delivering phenylalkylamine Calcium Channel Blockers, designed for patients with angina pectoris requiring continuous dosing but experiencing gastrointestinal side effects from oral medications. The patch utilizes novel permeation enhancers ensuring consistent plasma concentrations over 24 hours. Bayer’s market positioning focuses on elderly patient segments and those with adherence challenges, targeting European markets with high cardiovascular disease prevalence. Clinical trials demonstrated improved tolerability and patient satisfaction, supporting regulatory submissions across the EU. Source: Bayer Annual Report 2025

- •5th May 2025, Pfizer Inc. announced a strategic partnership with a leading European generic pharmaceutical company to co-develop and commercialize combination Calcium Channel Blocker therapies aiming to capture growing generic markets in Eastern Europe. The collaboration focuses on licensing agreements, shared R&D resources, and joint marketing efforts to expand regional presence and optimize cost efficiencies. This initiative is expected to accelerate access to affordable cardiovascular therapies while enhancing Pfizer’s portfolio diversity. Regulatory filings for the first joint product are underway with anticipated launches in late 2025. Source: Pfizer Investor Relations

- •20th June 2025, AstraZeneca PLC completed the acquisition of a mid-sized European specialty pharma firm focused on innovative drug delivery systems for cardiovascular therapies. The deal enhances AstraZeneca’s capabilities in sustained-release and combination formulations of Calcium Channel Blockers. Integration plans include leveraging advanced manufacturing technologies and expanding market access through existing AstraZeneca channels. This acquisition aligns with AstraZeneca’s strategy to strengthen its cardiovascular franchise and address unmet medical needs across Europe. Source: AstraZeneca Corporate Announcement

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Poland is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.8 Billion |

| Forecast Year Market Size | USD 7.6 Billion |

| CAGR | 5.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 5.4% |

| Scope of Report | Market is segmented by Product Type (Dihydropyridines, Phenylalkylamines, Benzothiazepines, Others, Combination Therapy), Application (Hypertension, Angina Pectoris, Arrhythmia, Raynaud's Disease, Migraine Prevention), End-Use Industry (Hospitals, Clinics, Outpatient Care Centers, Retail Pharmacies), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Emerging markets within Eastern Europe offer significant growth opportunities due to increasing healthcare infrastructure investments and rising prevalence of cardiovascular conditions., Innovation in drug delivery systems, such as transdermal patches and novel oral formulations, presents opportunities to enhance patient experience and expand market share., Expanding indications of Calcium Channel Blockers in conditions like migraine prevention and Raynaud's disease can open new application segments and revenue streams., Strategic partnerships and licensing agreements between multinational and regional pharmaceutical companies can facilitate market penetration and accelerate product launches. |

Calcium Channel Blocker Market - Europe Size & Outlook 2020-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.