Europe Cold-formed Steel Market - Europe Industry Size & Growth Analysis 2025-2034

Europe Cold-formed Steel Market is segmented by Product Type (Galvanized Steel, Stainless Steel, Aluminum-Coated Steel, Zinc-Aluminum Alloy Steel, Pre-painted Steel), Application (Building Construction, Automotive Components, HVAC Systems, Electrical Appliances, Furniture), End-Use Industry (Residential Construction, Commercial Construction, Automotive Industry, Appliance Manufacturing), Distribution Channel (Direct Sales, Distributors and Dealers, Online Platforms), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Cold-formed Steel (CFS) market is a pivotal segment within the regional steel industry, focusing on the manufacture and utilization of steel products formed at ambient temperatures into lightweight yet strong components. This market caters to a broad spectrum of industries including construction, automotive, HVAC, electrical appliances, and furniture, where cold-formed steel offers advantages such as enhanced durability, corrosion resistance, and environmental sustainability. The market's scope includes multiple alloys and coatings like galvanized steel, stainless steel, and pre-painted steel, addressing specific functional requirements across applications. Europe’s stringent regulatory environment and increasing emphasis on green building practices have heightened demand for innovative steel solutions that reduce carbon footprints while maintaining structural integrity. Market participants engage in advanced production technologies, including high-strength steel formulations and surface treatments, to meet growing needs for energy efficiency and design flexibility. The region’s economic recovery post-pandemic and infrastructure development plans further underpin the expansion of the cold-formed steel market, driving significant investment and innovation in product development and supply chain optimization.

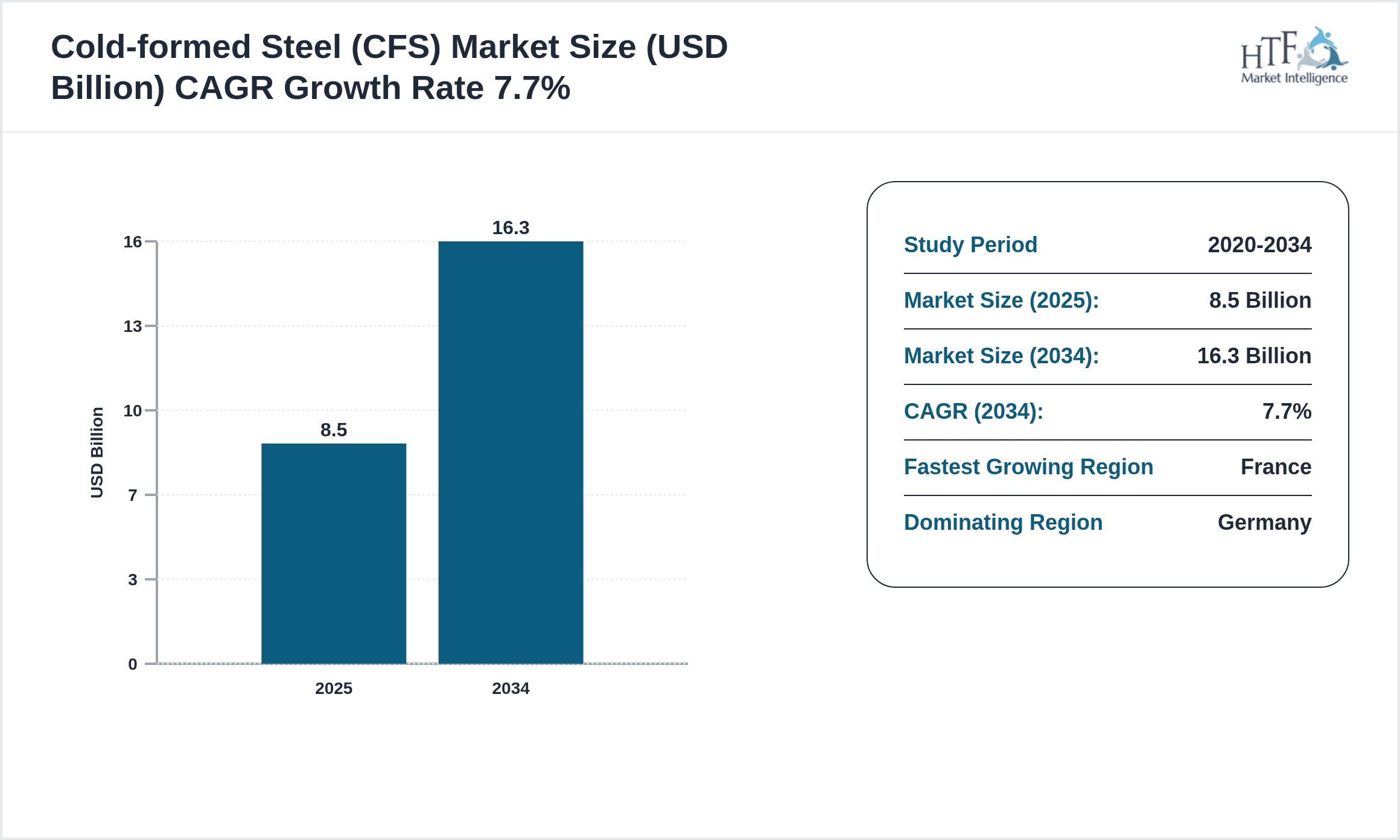

- •Key market highlights include a base market size of USD 8.5 billion in 2025 with a robust forecast to reach USD 16.3 billion by 2034, reflecting a CAGR of approximately 7.7%. The galvanized steel segment dominates the product type category, driven by its widespread applicability and cost efficiency, while pre-painted steel is the fastest-growing type due to increasing demand for aesthetic and protective finishes. Application-wise, building construction leads the market owing to extensive infrastructure projects across Europe. Germany emerges as the dominating country, attributed to its advanced manufacturing base and construction activity, whereas France is identified as the fastest-growing market within the region due to favorable government policies and rising investments in energy-efficient buildings.

- •The Europe CFS market offers substantial value propositions by enabling lightweight, flexible, and sustainable construction materials that contribute to reduced environmental impact and enhanced performance. Stakeholders including manufacturers, fabricators, architects, and regulatory bodies benefit from the market’s drive towards innovation, compliance with environmental standards, and adoption of digital fabrication techniques. These factors collectively facilitate cost savings, improved safety, and longer service life for end products, reinforcing the strategic importance of cold-formed steel as a key material in Europe’s sustainable industrial landscape.

Competitive Landscape

The competitive environment of the Europe Cold-formed Steel market is characterized by a mix of established multinational corporations and specialized regional manufacturers competing on innovation, quality, and service. Market players prioritize investment in advanced production technologies such as automated roll forming, laser cutting, and high-strength steel alloys to enhance product differentiation and meet strict European standards. Strategic collaborations and joint ventures are common to expand geographic reach and product portfolios, while mergers and acquisitions facilitate consolidation and access to new technologies. Pricing strategies often reflect the balance between raw material cost fluctuations and the premium for value-added coatings and finishes. Distribution channels include direct sales, dealer networks, and digital platforms, enabling extensive market penetration. Innovation in lightweight design, environmental compliance, and customization capabilities represent key competitive levers. Regional competition is intense, with Germany, France, and the UK hosting significant manufacturing hubs, while emerging markets in Eastern Europe offer cost advantages and growth opportunities. The outlook suggests sustained rivalry fueled by continuous product development and expanding applications in construction and automotive sectors.

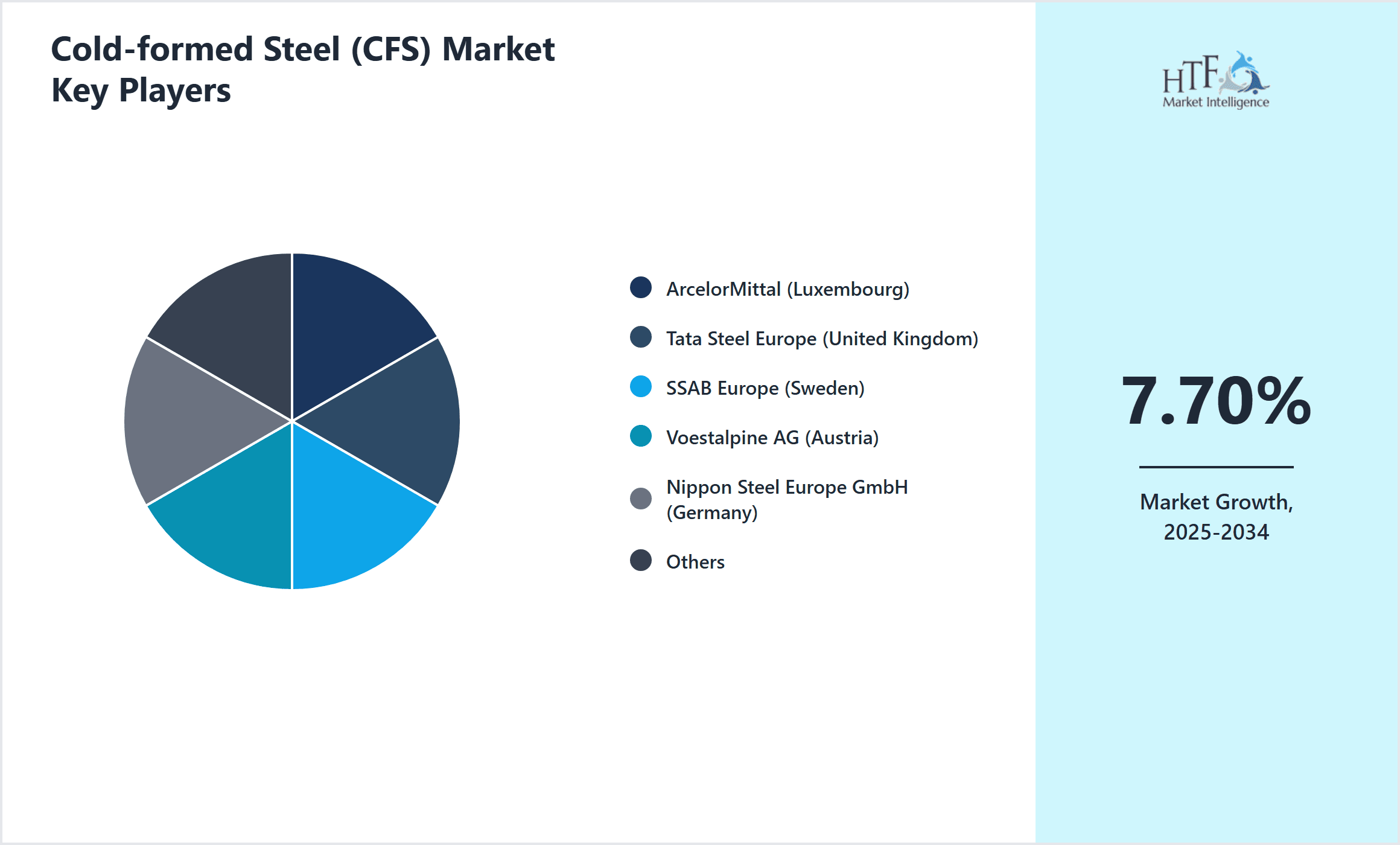

Leading Companies in Cold-formed Steel Market

- •ArcelorMittal (Luxembourg)

- •Tata Steel Europe (United Kingdom)

- •SSAB Europe (Sweden)

- •Voestalpine AG (Austria)

- •Nippon Steel Europe GmbH (Germany)

- •Salzgitter AG (Germany)

- •Thyssenkrupp Steel Europe (Germany)

- •Ruukki Construction (Finland)

- •Hydro Aluminium (Norway)

- •Novelis Europe (Belgium)

- •Danieli Group (Italy)

- •Metinvest Holding (Ukraine)

- •Outokumpu (Finland)

- •British Steel Limited (United Kingdom)

- •Severstal Europe (Russia)

- •Salvagnini Group (Italy)

- •Aperam (Luxembourg)

- •Celsa Group (Spain)

- •Gränges AB (Sweden)

- •Kloeckner Metals Europe (Germany)

- •JSW Steel Europe (Poland)

- •Sidenor Steel Industry (Greece)

- •Outotec (Finland)

- •Aperam Stainless Europe (Luxembourg)

- •Rautaruukki Oyj (Finland)

Market Breakdown

- •By Product Type

- ◦Galvanized Steel

- ◦Stainless Steel

- ◦Aluminum-Coated Steel

- ◦Zinc-Aluminum Alloy Steel

- ◦Pre-painted Steel

- •By Application

- ◦Building Construction

- ◦Automotive Components

- ◦HVAC Systems

- ◦Electrical Appliances

- ◦Furniture

- •By End-Use Industry

- ◦Residential Construction

- ◦Commercial Construction

- ◦Automotive Industry

- ◦Appliance Manufacturing

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors and Dealers

- ◦Online Platforms

Growth Dynamics

- •The growing demand for sustainable and lightweight building materials is a primary driver of the Europe CFS market. Increasing urbanization and infrastructure modernization require efficient structural solutions that cold-formed steel readily provides, enabling faster construction and reduced environmental impact.

- •Advancements in steel processing technologies, including high-strength steel grades and eco-friendly coatings, enhance product performance and widen application scope. These innovations support manufacturers in meeting evolving regulatory requirements and customer expectations.

- •Government incentives promoting green construction and energy-efficient buildings drive adoption of cold-formed steel products, particularly galvanized and pre-painted types. European Union directives on carbon reduction encourage manufacturers to innovate and increase market penetration.

- •The automotive sector's shift towards lightweight materials to improve fuel efficiency and reduce emissions significantly boosts the demand for cold-formed steel components. This trend aligns with Europe’s stringent emission norms and vehicle safety standards.

- •Expansion of distribution networks and digitization in supply chain management facilitate better market reach and customer engagement. Online platforms enhance accessibility and transparency, supporting sales growth and service improvement across Europe.

- •Rising investments in renovation and retrofitting of aging infrastructure in Europe further stimulate the market, as cold-formed steel provides economical and durable solutions suitable for refurbishment projects.

- •The integration of Industry 4.0 technologies including automation and robotics in manufacturing processes improves production efficiency and quality control, reinforcing competitive advantages for European CFS producers.

Market Trends

- •An increasing focus on environmental sustainability has led to the adoption of recycled content in cold-formed steel production, reducing carbon footprints while maintaining product quality and performance across Europe.

- •Smart manufacturing practices including digital twins and IoT integration allow real-time monitoring and predictive maintenance in steel fabrication plants, enhancing operational efficiency and reducing downtime.

- •The trend toward modular and prefabricated building construction favors cold-formed steel due to its precision, ease of assembly, and adaptability to customized architectural designs, accelerating project timelines.

- •Sustainability certification programs such as LEED and BREEAM increasingly influence material selection, driving demand for cold-formed steel products that comply with green building standards.

- •Collaborative initiatives between steel producers and construction firms promote innovation in lightweight structural components, focusing on enhanced strength-to-weight ratios and corrosion resistance.

- •Customer preferences are shifting towards aesthetically versatile steel products, leading to growth in pre-painted and coated steel segments that offer design flexibility alongside durability.

- •Future market directions include the exploration of hybrid materials combining steel with composites to achieve superior performance metrics in automotive and construction applications.

Market Opportunities

- •The rising demand for energy-efficient and sustainable construction materials presents significant growth opportunities, especially for manufacturers focusing on eco-friendly coatings and recycled steel content.

- •Untapped markets in Eastern Europe offer potential for expansion, driven by increasing industrialization and infrastructure investments, providing scope for new distribution partnerships and localized production.

- •Technological innovation in pre-painted and coated steel products opens avenues for differentiated offerings catering to architectural and automotive aesthetics, enhancing market penetration.

- •Geographical expansion through strategic alliances and joint ventures can help companies access emerging markets within Europe, leveraging regional expertise and reducing operational costs.

- •Development of customized cold-formed steel solutions for specialized applications such as renewable energy infrastructure and smart buildings presents lucrative investment prospects.

- •Increasing adoption of digital platforms for sales and supply chain management enables broader market reach and improved customer engagement, offering new business models and revenue streams.

- •Government incentives for green construction and circular economy initiatives stimulate innovation and adoption of sustainable steel products, creating competitive advantages for proactive market participants.

Market Challenges

- •Volatility in raw material prices, particularly steel scrap and zinc, poses profitability challenges for cold-formed steel manufacturers, impacting cost structures and pricing strategies.

- •Stringent environmental and safety regulations require continuous investment in compliance and certification processes, increasing operational complexity and costs within the European market.

- •Competition from alternative lightweight materials such as aluminum and composites in automotive and construction sectors pressures market share and necessitates ongoing product innovation.

- •Supply chain disruptions and logistical challenges, exacerbated by geopolitical factors and energy price fluctuations, affect timely delivery and inventory management.

- •Skilled labor shortages in steel fabrication and construction industries hinder capacity expansion and quality control, limiting market growth potential in certain regions.

- •High capital expenditure requirements for adopting advanced manufacturing technologies can deter small and medium enterprises from scaling production capabilities.

- •Market fragmentation and regional disparities in demand complicate strategic planning and necessitate tailored approaches for diverse European sub-markets.

Regulatory Framework

- •The EU Construction Products Regulation (CPR) updated between 2020 and 2025 mandates harmonized standards for steel products used in construction, emphasizing safety, performance, and environmental impact. Compliance is mandatory for market access across member states, driving manufacturers to enhance product certification and testing protocols.

- •The REACH regulation, reinforced during 2021-2025, restricts the use of hazardous substances in steel coatings and galvanizing processes, compelling producers to adopt eco-friendly materials and sustainable practices to meet stringent chemical safety standards.

- •Energy Efficiency Directive updates introduced in 2022 require steel manufacturing plants to improve energy consumption and reduce greenhouse gas emissions, catalyzing investments in cleaner technologies and process optimizations.

- •The European Green Deal policy framework, with milestones set through 2025, promotes circular economy principles in steel production, incentivizing recycling and reuse of steel scrap and minimizing environmental footprint.

- •Country-specific mandates, such as Germany’s Climate Action Plan 2030, impose stricter emission reduction targets on industrial sectors including steel manufacturing, encouraging adoption of low-carbon technologies and sustainable steel grades within the cold-formed steel industry.

Market Intelligence

- •15th January 2025, ArcelorMittal announced the launch of a new high-strength galvanized cold-formed steel product designed specifically for modular construction applications. This product features enhanced corrosion resistance and improved formability, targeting rapid urbanization projects across Europe. The initiative aims to support sustainable building practices by reducing material weight and extending service life, aligning with EU environmental regulations. The launch is expected to strengthen ArcelorMittal’s market position in the building construction segment and foster collaborations with leading construction companies.

- •3rd March 2025, Tata Steel Europe introduced its innovative pre-painted steel range featuring advanced UV and scratch-resistant coatings. Developed to meet the growing demand for aesthetically versatile and durable steel components in automotive and appliance industries, this product enhances lifecycle performance while lowering maintenance costs. Tata Steel's strategic objective includes expanding its footprint in the automotive lightweight materials market by integrating this product into electric vehicle component manufacturing, supporting the region’s shift towards sustainable mobility solutions.

- •22nd May 2025, Voestalpine AG announced a strategic partnership with leading European HVAC manufacturers to co-develop customized zinc-aluminum alloy cold-formed steel products. This collaboration focuses on enhancing thermal efficiency and corrosion resistance in HVAC ducting systems. The joint initiative includes shared R&D investments and pilot production programs aimed at accelerating time-to-market and meeting rising demand for energy-efficient building solutions.

- •10th September 2025, SSAB Europe completed the acquisition of a regional cold-formed steel processor in the Nordic region, expanding its manufacturing capacity and customer base. The acquisition supports SSAB’s growth strategy by enhancing regional distribution networks and enabling faster delivery of tailored steel products. This move consolidates SSAB’s position as a leading supplier in Northern Europe while enabling cross-selling of high-strength steel solutions in construction and automotive sectors.

- •Source: Official company press releases, Industry publications

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.5 Billion |

| Forecast Year Market Size | USD 16.3 Billion |

| CAGR | 7.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.4% |

| Scope of Report | Market is segmented by Product Type (Galvanized Steel, Stainless Steel, Aluminum-Coated Steel, Zinc-Aluminum Alloy Steel, Pre-painted Steel), Application (Building Construction, Automotive Components, HVAC Systems, Electrical Appliances, Furniture), End-Use Industry (Residential Construction, Commercial Construction, Automotive Industry, Appliance Manufacturing), Distribution Channel (Direct Sales, Distributors and Dealers, Online Platforms) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | ArcelorMittal (Luxembourg), Tata Steel Europe (United Kingdom), SSAB Europe (Sweden), Voestalpine AG (Austria), Nippon Steel Europe GmbH (Germany), Salzgitter AG (Germany), Thyssenkrupp Steel Europe (Germany), Ruukki Construction (Finland), Hydro Aluminium (Norway), Novelis Europe (Belgium), Danieli Group (Italy), Metinvest Holding (Ukraine), Outokumpu (Finland), British Steel Limited (United Kingdom), Severstal Europe (Russia), Salvagnini Group (Italy), Aperam (Luxembourg), Celsa Group (Spain), Gränges AB (Sweden), Kloeckner Metals Europe (Germany), JSW Steel Europe (Poland), Sidenor Steel Industry (Greece), Outotec (Finland), Aperam Stainless Europe (Luxembourg), Rautaruukki Oyj (Finland) |

Europe Cold-formed Steel Market - Europe Industry Size & Growth Analysis 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.