Global Direct-to-Consumer Genetic Testing Market Size, Growth & Revenue 2025-2034

Global Direct-to-Consumer Genetic Testing Market is segmented by Genetic Test Type (Whole Genome Sequencing, Genotyping, Exome Sequencing, Targeted DNA Testing, Epigenetic Testing), Application Area (Health Risk Assessment, Ancestry & Genealogy, Nutrigenomics, Pharmacogenomics, Fitness & Wellness), Service Delivery Model (Online Direct Sales, Retail Partnerships, Mobile App-Based Services, Subscription-Based Models), Consumer Demographic (Individual Consumers, Healthcare Providers, Research Institutions, Wellness & Fitness Industry), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

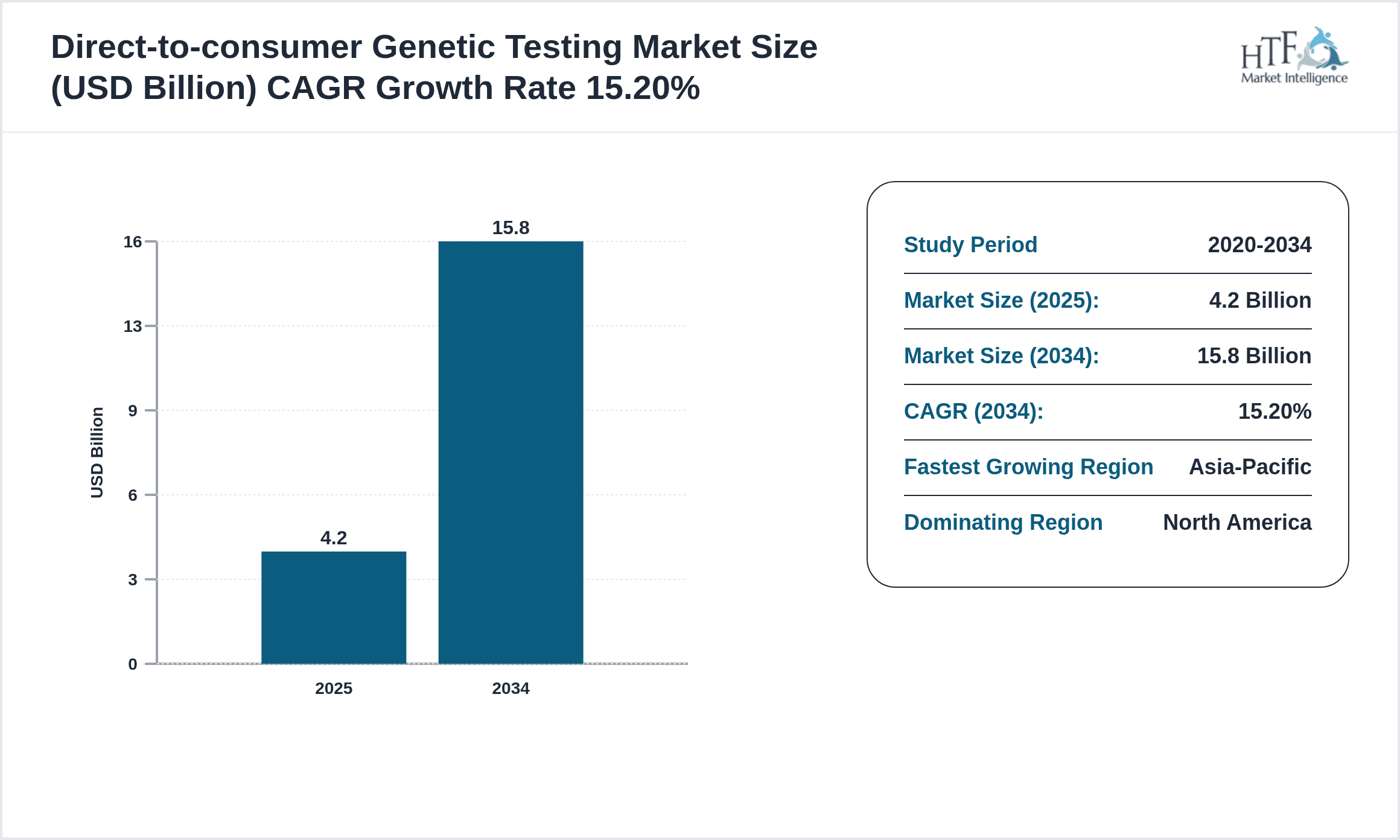

The global direct-to-consumer genetic testing market offers consumers access to their genetic data without intermediary healthcare providers, facilitating insights into ancestry, health risks, drug response, nutrition, and fitness. It comprises a broad spectrum of testing types such as whole genome sequencing, genotyping, exome sequencing, targeted DNA testing, and epigenetic testing. Advanced genomic technologies have empowered individuals to take proactive roles in personal health management, enabling early detection of genetic predispositions and personalized lifestyle choices. The market is marked by rapid technological innovation, increasing consumer health awareness, and expanding digital health ecosystems, which collectively drive adoption worldwide. Leading applications include health risk assessments for chronic diseases, ancestry and genealogy exploration, pharmacogenomics for tailored drug therapies, nutrigenomics for diet optimization, and fitness and wellness tracking. Regulatory oversight and data privacy remain critical factors influencing market trajectory. Geographically, North America dominates due to high healthcare expenditure and technological infrastructure, while Asia-Pacific is the fastest-growing region owing to rising awareness and improving healthcare access. The market’s growth is supported by expanding product portfolios, strategic partnerships, and increasing consumer interest in genetic literacy. Challenges such as ethical concerns, data security, and regulatory complexities persist but are being addressed through collaborative frameworks and innovation. This report provides an in-depth analysis of market size, competitive landscape, regional dynamics, growth drivers, challenges, and future opportunities spanning the period from 2020 to 2034.

Competitive Landscape

The global direct-to-consumer genetic testing market is characterized by intense competition among established biotech companies, emerging startups, and digital health innovators. Market players pursue differentiation through technological innovation, expanded test offerings, and integration with digital health platforms. Competitive strategies include partnerships with healthcare providers, investment in research and development, and acquisitions to broaden product pipelines. Pricing strategies vary from affordable genotyping kits to premium whole genome sequencing services, catering to diverse consumer segments. Distribution channels encompass e-commerce platforms, retail partnerships, and direct online sales, enhancing accessibility. Data privacy, compliance with regulations, and consumer trust are pivotal to competitive positioning. Companies increasingly leverage artificial intelligence and machine learning to enhance variant interpretation and personalized insights. Regional competition is influenced by varying regulatory environments and consumer awareness levels. Strategic alliances and mergers are common to consolidate market share and expand geographic reach. Future competition will likely center on improving test accuracy, data security, and providing holistic consumer experiences through integrated health management solutions.

Leading Companies in Direct-to-Consumer Genetic Testing Market

- •23andMe, Inc. (United States)

- •Ancestry.com LLC (United States)

- •MyHeritage Ltd. (Israel)

- •Invitae Corporation (United States)

- •Gene by Gene, Ltd. (United States)

- •Nebula Genomics, Inc. (United States)

- •Color Genomics, Inc. (United States)

- •Living DNA Ltd. (United Kingdom)

- •Veritas Genetics, Inc. (United States)

- •Helix OpCo, LLC (United States)

- •DNAfit Limited (United Kingdom)

- •Orig3n, Inc. (United States)

- •Circle DNA (Hong Kong)

- •Futura Genetics (Slovakia)

- •TellmeGen (Spain)

- •GenePlanet (Slovenia)

- •Pathway Genomics Corporation (United States)

- •Gene by Gene, Ltd. (United States)

- •Dante Labs (Italy)

- •Genos, Inc. (United States)

- •Invitae Corporation (United States)

- •GeneDx (United States)

- •Mapmygenome India Pvt. Ltd. (India)

- •GeneFi, Inc. (United States)

- •EasyDNA Ltd. (United Kingdom)

Market Breakdown

- •By Genetic Test Type

- ◦Whole Genome Sequencing

- ◦Genotyping

- ◦Exome Sequencing

- ◦Targeted DNA Testing

- ◦Epigenetic Testing

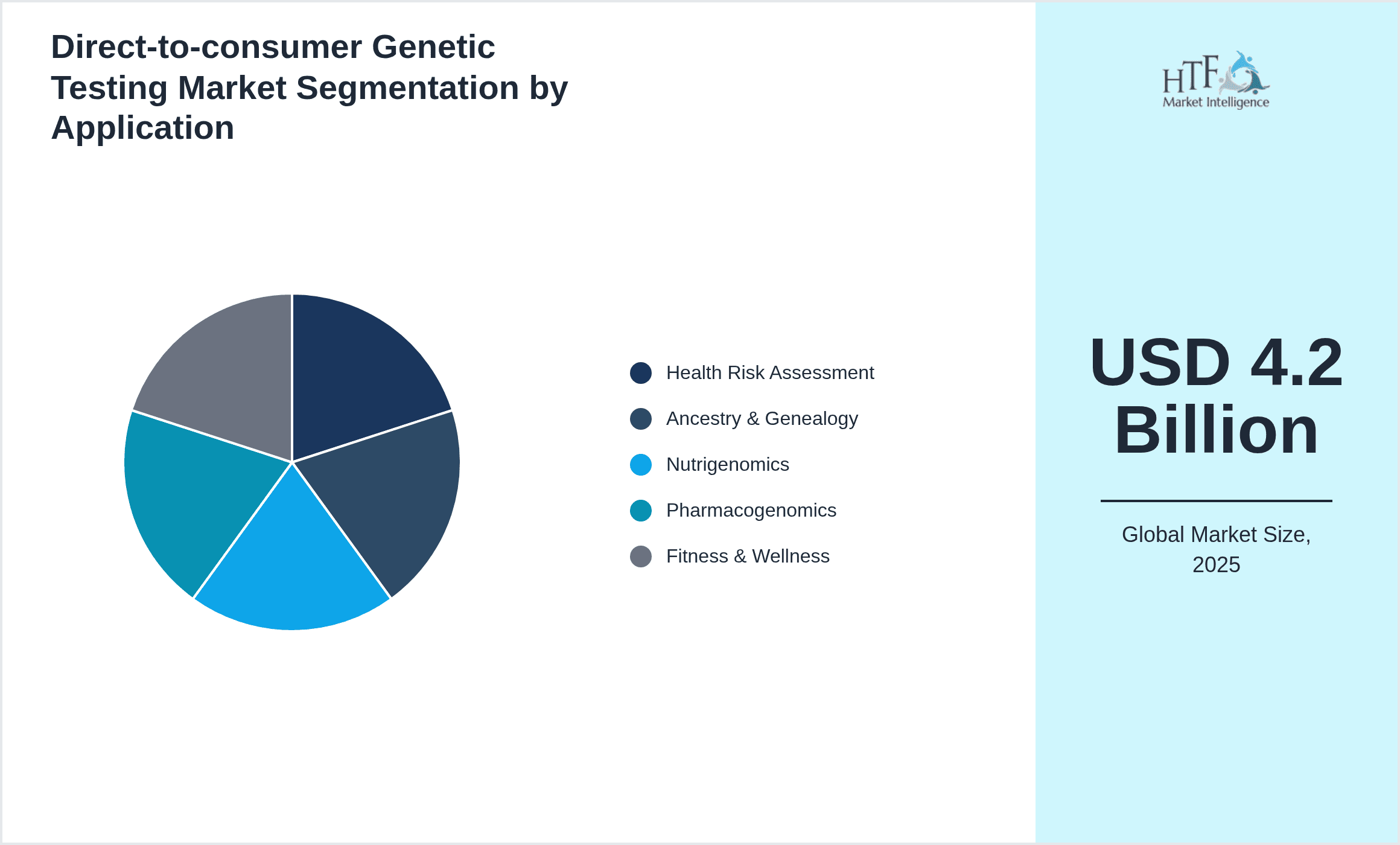

- •By Application Area

- ◦Health Risk Assessment

- ◦Ancestry & Genealogy

- ◦Nutrigenomics

- ◦Pharmacogenomics

- ◦Fitness & Wellness

- •By Service Delivery Model

- ◦Online Direct Sales

- ◦Retail Partnerships

- ◦Mobile App-Based Services

- ◦Subscription-Based Models

- •By Consumer Demographic

- ◦Individual Consumers

- ◦Healthcare Providers

- ◦Research Institutions

- ◦Wellness & Fitness Industry

Growth Dynamics

The global direct-to-consumer genetic testing market is propelled by rising consumer interest in personalized health and wellness, driven by increasing awareness of genetic predispositions to diseases. Advancements in sequencing technologies have drastically reduced costs, making genetic testing more affordable and accessible to the broader public. The proliferation of digital health platforms and mobile applications facilitates easy ordering, sample collection, and result delivery, enhancing consumer engagement. Additionally, growing partnerships between genetic testing companies and healthcare providers enable integrated care models, fostering market expansion. Government initiatives promoting precision medicine and preventive healthcare further stimulate demand, alongside rising investments in genomics research and data analytics.

Market Trends

A significant trend in the direct-to-consumer genetic testing market is the integration of artificial intelligence and machine learning to improve the accuracy and personalization of test interpretations. Companies are expanding services beyond ancestry to include actionable health insights, pharmacogenomics, and lifestyle recommendations. Subscription-based service models and app-driven user experiences are gaining traction, providing continuous engagement and additional value through data updates. Increasing collaborations with pharmaceutical companies and healthcare providers are creating hybrid models that blend consumer-driven testing with clinical validation. Furthermore, heightened focus on data privacy and ethical use of genetic information is shaping regulatory and consumer trust frameworks globally.

Market Opportunities

The direct-to-consumer genetic testing market presents vast opportunities with growing demand from emerging regions such as Asia-Pacific and Latin America, where increasing healthcare awareness and digital penetration are opening new consumer bases. Expanding applications into pharmacogenomics and nutrigenomics offer potential for personalized medicine and diet planning markets. Innovations in epigenetic testing provide opportunities to attract health-conscious consumers interested in dynamic gene expression profiles. Collaborations with wellness and fitness industries can create bundled offerings that combine genetic insights with lifestyle coaching. Additionally, increasing regulatory clarity and standardization efforts globally can build consumer confidence and facilitate market expansion.

Market Challenges

The direct-to-consumer genetic testing market faces challenges including regulatory uncertainties across different countries, which complicate product approvals and marketing claims. Data privacy and security concerns remain paramount, with consumers wary of potential misuse of sensitive genetic information. Ethical issues surrounding genetic counseling, test interpretation, and psychological impacts impose responsibilities on companies and regulators. Additionally, variability in test accuracy and clinical validity across providers can hinder consumer trust. Market fragmentation and intense competition exert pricing pressure, affecting profitability. Furthermore, limited awareness in certain regions and cultural sensitivities also pose adoption barriers.

Regulatory Framework

Between 2020 and 2025, regulatory frameworks governing direct-to-consumer genetic testing have evolved globally to address concerns over accuracy, consumer protection, and data privacy. In North America, agencies such as the U.S. Food and Drug Administration (FDA) have implemented guidance requiring premarket authorization for health-related genetic tests to ensure clinical validity. In Europe, the In Vitro Diagnostic Regulation (IVDR) enacted in 2022 mandates stricter conformity assessments, impacting test manufacturers and distributors. Data protection laws like the General Data Protection Regulation (GDPR) impose stringent requirements on genetic data handling and cross-border transfers. Several countries have introduced genetic counseling mandates to mitigate risks of misinterpretation. These regulations have increased compliance costs but enhanced consumer confidence and market credibility. Emerging economies are in the process of developing tailored regulatory frameworks to balance innovation with safety. Overall, regulatory evolution is fostering responsible growth and harmonization in the global market.

Market Intelligence

- •12th February 2025, 23andMe, Inc. launched an advanced whole genome sequencing service offering expanded health risk reports and personalized wellness recommendations. This service leverages artificial intelligence algorithms to enhance variant interpretation accuracy and provide consumers with actionable insights. The new offering targets health-conscious consumers seeking comprehensive genetic information beyond ancestry, aiming to increase engagement and revenue. The company also introduced a subscription model for continuous data updates and family health tracking. This strategic launch positions 23andMe as a market innovator, responding to growing demand for integrated genetic health services. Source: 23andMe Official Press Release

- •5th May 2025, Invitae Corporation announced a strategic partnership with a leading pharmaceutical company to integrate pharmacogenomic testing into drug prescription workflows. This collaboration aims to promote personalized medicine by enabling clinicians to tailor treatments based on patients' genetic profiles, reducing adverse drug reactions and improving outcomes. Invitae will provide genetic testing kits directly to consumers and healthcare providers, with data analytics support for clinical decision-making. The initiative is expected to accelerate market adoption of pharmacogenomics and expand Invitae’s footprint in both consumer and clinical segments. Source: Invitae Corporation Press Release

- •18th August 2025, Ancestry.com LLC introduced a new mobile app feature that combines genealogy with health insights by integrating user genetic data with historical records and lifestyle analytics. This innovation enhances user experience by offering personalized health risk assessments linked to ancestry origins and environmental factors. The app also incorporates social sharing and community engagement tools to foster user interaction and loyalty. This product update reflects the trend towards holistic genetic services blending heritage and health, aiming to boost subscriber growth and retention. Source: Ancestry.com Official Announcement

- •30th October 2025, MyHeritage Ltd. completed the acquisition of a European epigenetic testing startup to expand its product portfolio into dynamic gene expression analysis. This acquisition brings cutting-edge epigenetic technologies enabling consumers to understand the effects of lifestyle and environment on gene expression over time. The integration is expected to create new revenue streams and enhance MyHeritage’s competitive positioning in personalized health and wellness markets. The move aligns with increasing consumer interest in epigenetics and the growing demand for real-time health monitoring. Source: MyHeritage Ltd. Corporate Communication

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.2 Billion |

| Forecast Year Market Size | USD 15.8 Billion |

| CAGR | 15.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 14.3% |

| Scope of Report | Market is segmented by Genetic Test Type (Whole Genome Sequencing, Genotyping, Exome Sequencing, Targeted DNA Testing, Epigenetic Testing), Application Area (Health Risk Assessment, Ancestry & Genealogy, Nutrigenomics, Pharmacogenomics, Fitness & Wellness), Service Delivery Model (Online Direct Sales, Retail Partnerships, Mobile App-Based Services, Subscription-Based Models), Consumer Demographic (Individual Consumers, Healthcare Providers, Research Institutions, Wellness & Fitness Industry) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | 23andMe, Inc. (United States), Ancestry.com LLC (United States), MyHeritage Ltd. (Israel), Invitae Corporation (United States), Gene by Gene, Ltd. (United States), Nebula Genomics, Inc. (United States), Color Genomics, Inc. (United States), Living DNA Ltd. (United Kingdom), Veritas Genetics, Inc. (United States), Helix OpCo, LLC (United States), DNAfit Limited (United Kingdom), Orig3n, Inc. (United States), Circle DNA (Hong Kong), Futura Genetics (Slovakia), TellmeGen (Spain), GenePlanet (Slovenia), Pathway Genomics Corporation (United States), Gene by Gene, Ltd. (United States), Dante Labs (Italy), Genos, Inc. (United States), Invitae Corporation (United States), GeneDx (United States), Mapmygenome India Pvt. Ltd. (India), GeneFi, Inc. (United States), EasyDNA Ltd. (United Kingdom) |

Global Direct-to-Consumer Genetic Testing Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.