Asia-Pacific Utility Vehicles Market Size, Growth & Revenue 2025-2034

Asia-Pacific Utility Vehicles Market is segmented by Product Type (Electric Utility Vehicles (Electric UTV), Gasoline Utility Vehicles (Gasoline UTV), Diesel Utility Vehicles (Diesel UTV), Hybrid Utility Vehicles (Hybrid UTV), Others (including LPG and specialized utility vehicles)), Application (Agriculture, Construction, Mining, Forestry, Recreation), End-Use Industry (Agriculture and Farming, Construction and Infrastructure, Mining and Quarrying, Forestry and Logging), Distribution Channel (Dealerships, Online Sales Platforms, Direct Sales), and Geography (Japan, China, Southeast Asia, India, Australia, South Korea, Others)

Pricing

Report Overview

Executive Summary

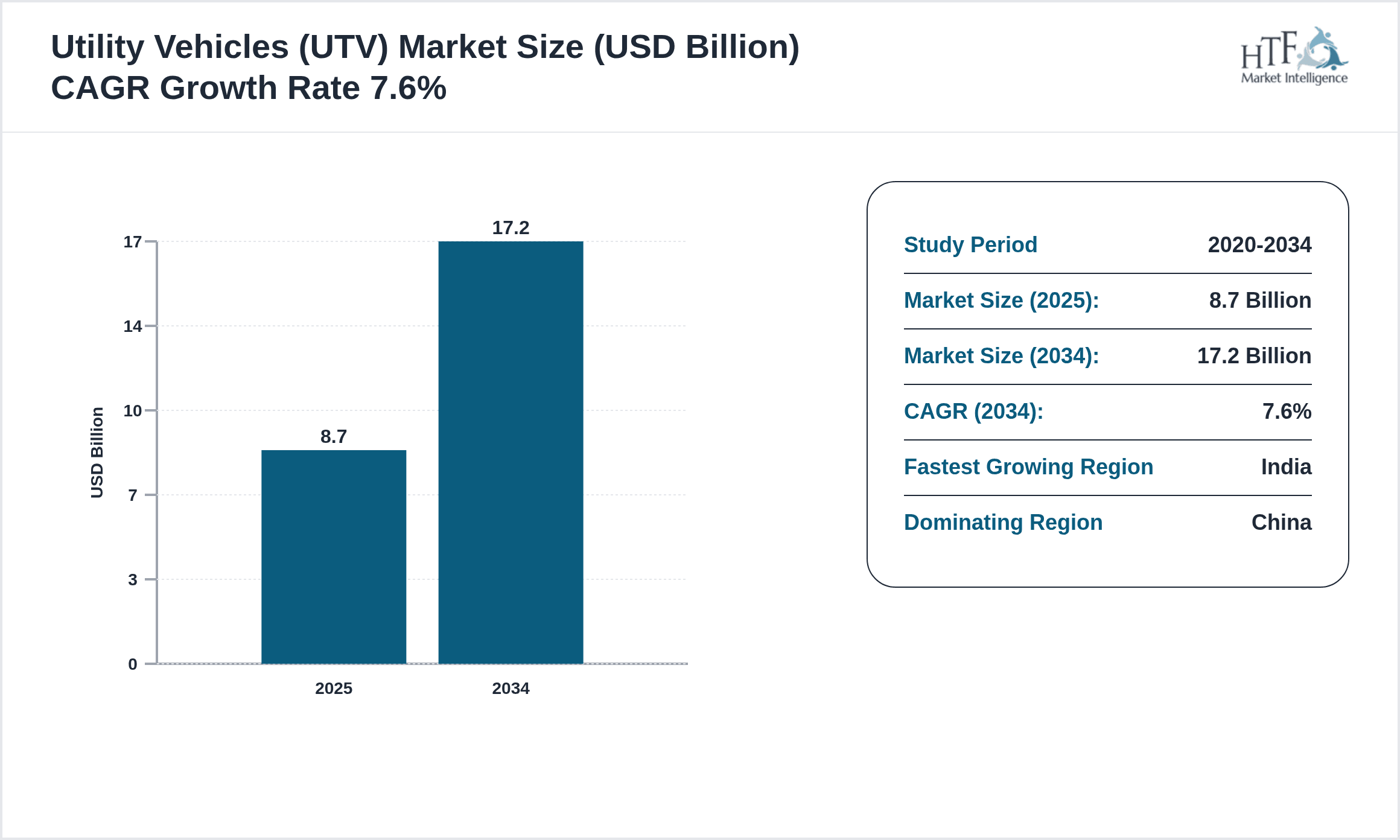

- •The Asia-Pacific Utility Vehicles (UTV) market is a rapidly evolving segment characterized by the production and deployment of multi-purpose off-road vehicles used extensively across agriculture, construction, mining, forestry, and recreational sectors. These vehicles include gasoline, diesel, electric, hybrid, and other specialized types tailored to meet diverse operational needs. The market encompasses a wide value chain involving original equipment manufacturers, component suppliers, distributors, and end-users who rely on these vehicles for enhanced productivity and operational efficiency. Key applications focus on tasks ranging from material transport and field operations to passenger movement in challenging terrains, emphasizing the vehicles' durability and adaptability. Ongoing technological advancements such as electrification, automation, and telematics integration are reshaping the market landscape, fostering sustainable and cost-effective solutions. The Asia-Pacific region is a significant growth hub driven by expanding infrastructure projects, mechanization in agriculture, and rising demand for eco-friendly transport alternatives. Prominent countries like China, India, Japan, South Korea, Australia, and Southeast Asian nations contribute substantially to market growth, supported by government initiatives and increasing industrialization. The market is expected to witness robust CAGR of approximately 7.6% from 2025 to 2034, fueled by innovation, regulatory support, and expanding end-use industries, making it a strategic focus area for manufacturers, investors, and policymakers.

- •Key market highlights include a base market size of USD 8.7 Billion in 2025, expanding to USD 17.2 Billion by 2034, with a CAGR of 7.6% and a year-on-year growth rate of 7.3%. China dominates the market by volume and revenue, while India represents the fastest-growing country due to rapid mechanization and infrastructure development. Gasoline UTVs currently lead product demand, but electric UTVs are the fastest-growing segment, driven by sustainability trends and government incentives. The Asia-Pacific region's diversified industrial base and growing recreational vehicle enthusiasm underpin market expansion.

- •The utility vehicles market in Asia-Pacific offers substantial value propositions by enhancing operational efficiency and safety across industrial and agricultural sectors. The vehicles enable cost reductions through mechanization and fuel-efficient technologies while supporting environmental goals through electrification. Stakeholders including manufacturers, distributors, and end-users benefit from innovations such as IoT-enabled fleet management and durable vehicle designs suited for diverse terrains. Strategic importance is underscored by the region's urbanization, infrastructure growth, and evolving regulatory frameworks promoting cleaner vehicles, making the market an attractive opportunity for sustained investment and technological collaboration.

Competitive Landscape

The Asia-Pacific Utility Vehicles market features a highly competitive environment marked by the presence of both multinational corporations and established regional players, fostering dynamic market interactions. Competitive strategies focus on product innovation, expanding electric and hybrid vehicle portfolios, and enhancing after-sales services to strengthen customer loyalty. Market leaders invest significantly in R&D to develop advanced safety features, telematics integration, and environmentally friendly powertrains, responding to stringent regional regulations and growing consumer awareness. Strategic partnerships and collaborations with local distributors enable wider market penetration, especially in emerging economies within the region. Pricing strategies balance affordability with quality, catering to diverse customer segments from large industrial users to recreational consumers. Mergers and acquisitions, while less frequent recently, remain a strategic tool for technology acquisition and geographic expansion. Distribution channels blend traditional dealerships with online platforms, improving accessibility. Regional competition is influenced by government incentives promoting electric vehicles in countries like China, South Korea, and India, encouraging players to align offerings with sustainability trends. Looking ahead, competitive advantage will increasingly hinge on digitalization, customization, and the ability to navigate complex regulatory landscapes, ensuring adaptability and resilience in the evolving Asia-Pacific market.

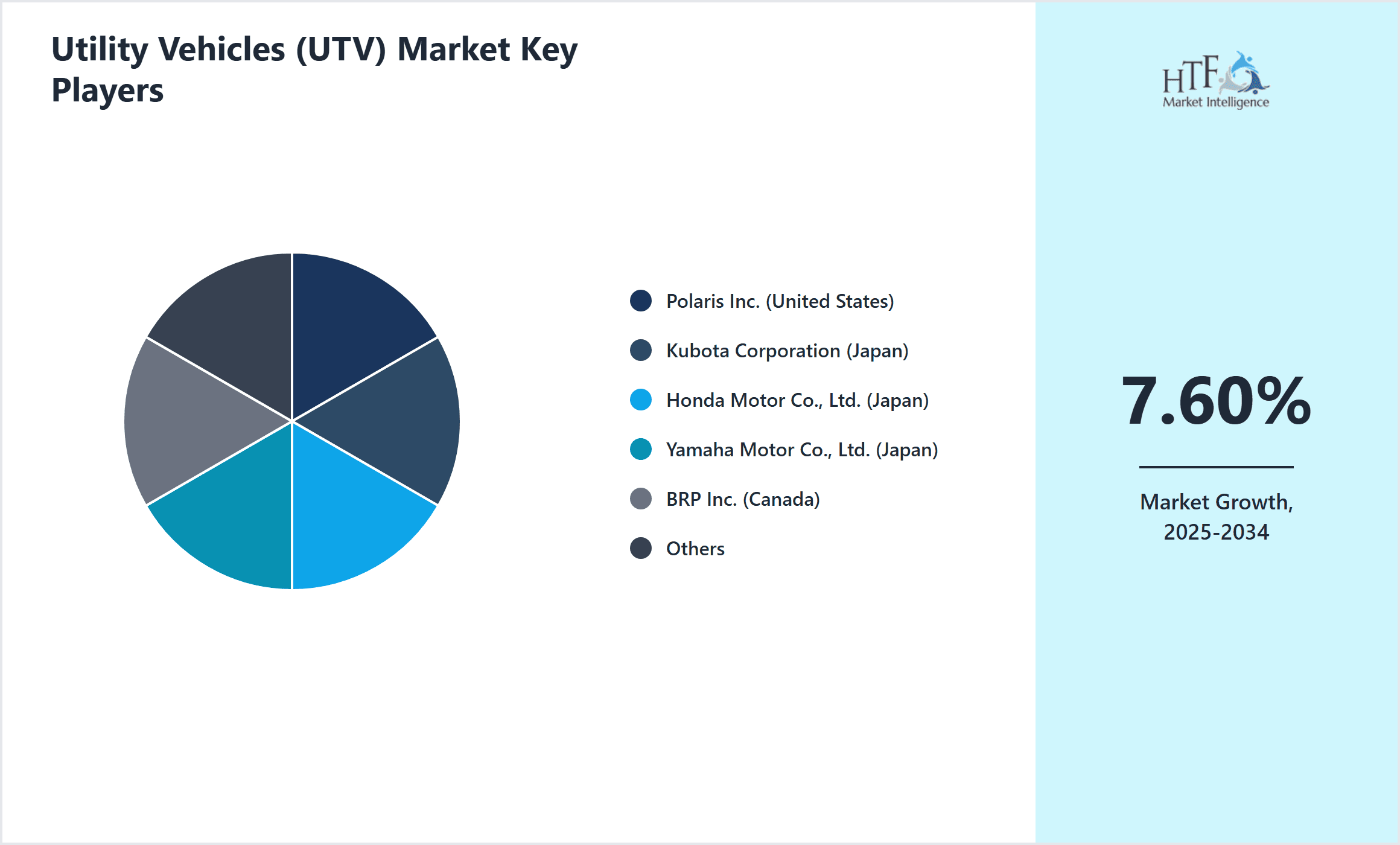

Prominent Players in Utility Vehicles Market

- •Polaris Inc. (United States)

- •Kubota Corporation (Japan)

- •Honda Motor Co., Ltd. (Japan)

- •Yamaha Motor Co., Ltd. (Japan)

- •BRP Inc. (Canada)

- •John Deere (United States)

- •Arctic Cat Inc. (United States)

- •Suzuki Motor Corporation (Japan)

- •CFMOTO (China)

- •Mahindra & Mahindra Ltd. (India)

- •Bombardier Recreational Products (Canada)

- •Textron Inc. (United States)

- •Kawasaki Heavy Industries Ltd. (Japan)

- •CFMOTO Powersports (China)

- •Linhai Motor Co., Ltd. (China)

- •Hisun Motors Co., Ltd. (China)

- •Can-Am (Canada)

- •Odes Motorcycles (China)

- •TGB Corporation (Taiwan)

- •Textron Specialized Vehicles (United States)

- •Honda R&D Co., Ltd. (Japan)

- •Kymco (Taiwan)

- •Polaris Asia Pacific Pty Ltd. (Australia)

- •Kubota Australia Pty Ltd. (Australia)

- •Suzuki Motor Corporation India Pvt. Ltd. (India)

Market Breakdown

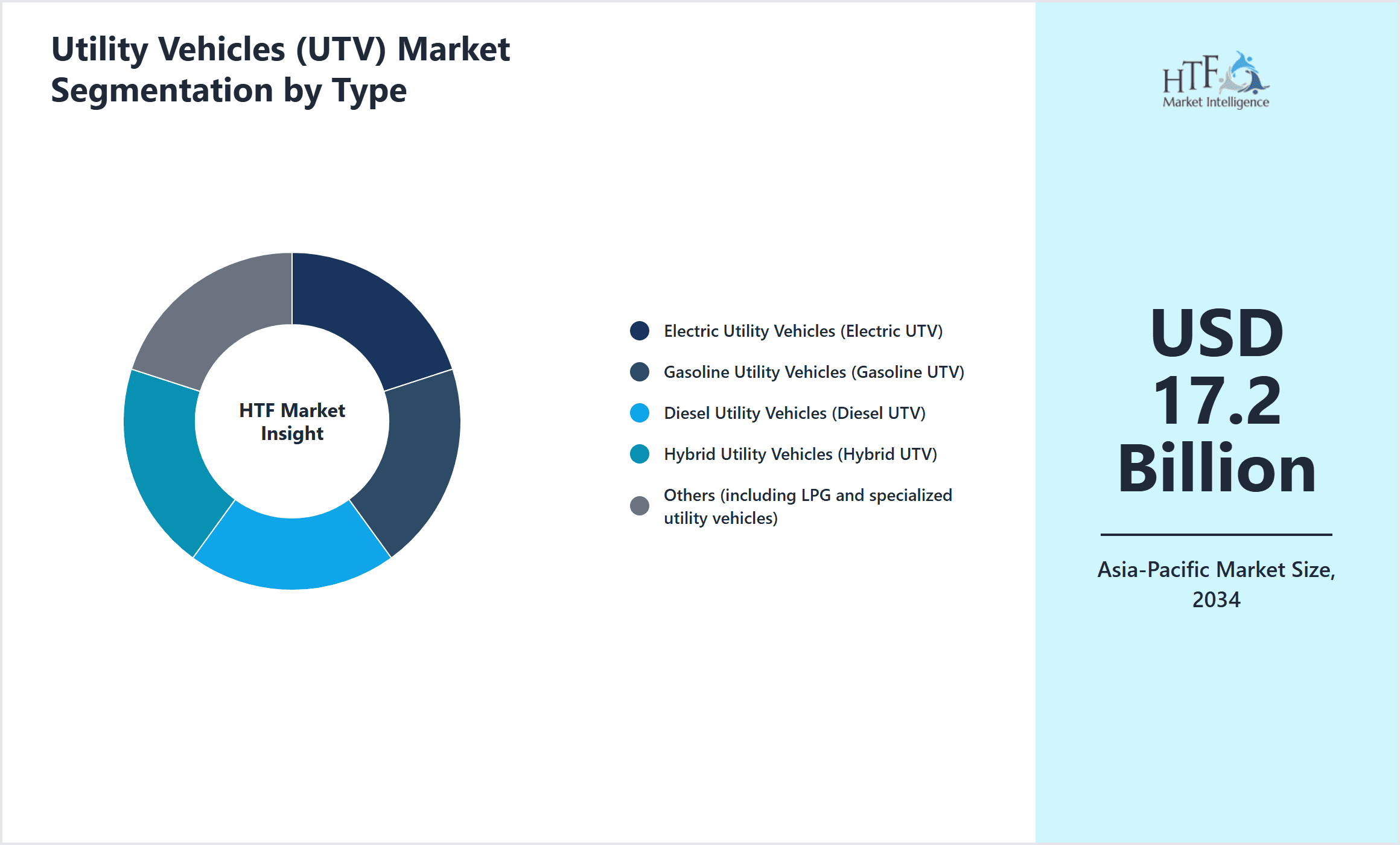

- •By Product Type

- ◦Electric Utility Vehicles (Electric UTV)

- ◦Gasoline Utility Vehicles (Gasoline UTV)

- ◦Diesel Utility Vehicles (Diesel UTV)

- ◦Hybrid Utility Vehicles (Hybrid UTV)

- ◦Others (including LPG and specialized utility vehicles)

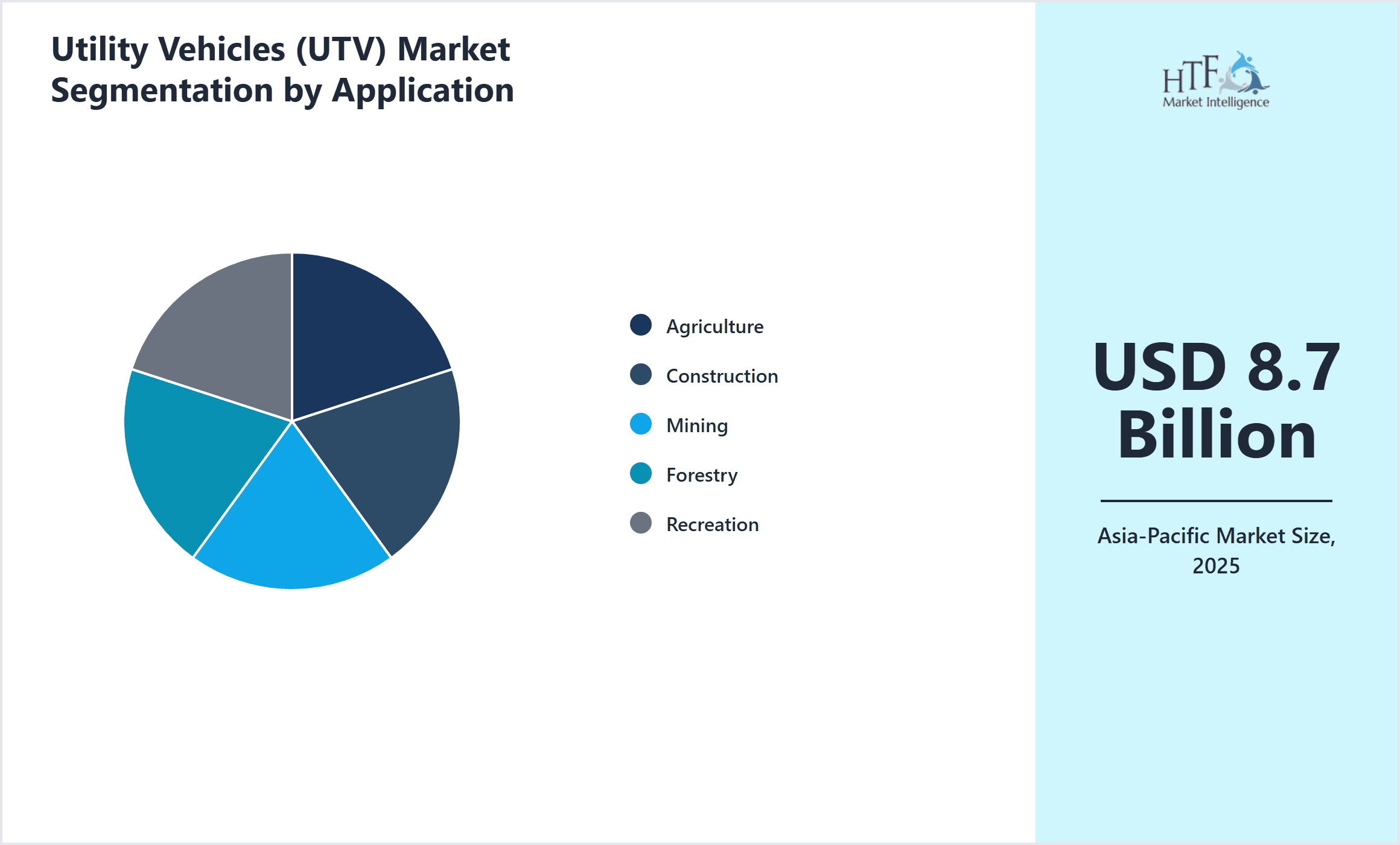

- •By Application

- ◦Agriculture

- ◦Construction

- ◦Mining

- ◦Forestry

- ◦Recreation

- •By End-Use Industry

- ◦Agriculture and Farming

- ◦Construction and Infrastructure

- ◦Mining and Quarrying

- ◦Forestry and Logging

- •By Distribution Channel

- ◦Dealerships

- ◦Online Sales Platforms

- ◦Direct Sales

Growth Dynamics

- •The Asia-Pacific Utility Vehicles market is driven by rapid mechanization in agriculture, especially in countries like India and China, where the shift from manual labor to mechanized solutions is accelerating demand. Government subsidies and incentives for electric vehicle adoption further stimulate market growth by reducing operational costs and enhancing environmental compliance. Infrastructure expansion, particularly in construction and mining sectors, necessitates reliable transport solutions, boosting UTV deployment. Innovation in electric and hybrid vehicle technologies enables manufacturers to meet stringent emission regulations, attracting environmentally conscious customers and expanding the market. Additionally, increasing recreational use in countries such as Australia and Japan contributes to diversified demand, reflecting growing consumer interest in multipurpose off-road vehicles. The confluence of these factors ensures robust growth and expanding market penetration across the Asia-Pacific region.

- •Rising environmental awareness and government mandates in key Asia-Pacific countries are encouraging the development and sales of electric and hybrid utility vehicles. These regulatory frameworks include emission standards and incentives for clean energy vehicles, which are shaping manufacturer strategies and product portfolios. This transition supports sustainable development goals and aligns with global trends toward reducing carbon footprints in transportation. As a result, electric utility vehicles represent the fastest-growing segment, capturing increasing market share and fostering innovation in battery technologies and charging infrastructure.

- •Technological advancements such as telematics, GPS integration, and autonomous driving features are enhancing the functionality and safety of utility vehicles. These innovations improve fleet management, operational efficiency, and reduce downtime, making UTVs more attractive to commercial users. The adoption of Industry 4.0 concepts within manufacturing and operational processes further accelerates market development, enabling data-driven decision-making and predictive maintenance.

- •Expanding infrastructure projects and urbanization across Asia-Pacific countries are increasing demand for robust utility vehicles capable of handling diverse terrains and heavy workloads. This trend is especially significant in developing economies where construction activity is a major economic driver. The need for flexible, durable, and efficient vehicles that can support multiple applications is encouraging manufacturers to diversify offerings and customize solutions for regional requirements.

- •Consumer preference shifts towards multipurpose and recreational utility vehicles are fueling market growth, particularly in more developed Asia-Pacific countries. The increasing popularity of outdoor activities and adventure sports is generating additional demand, prompting manufacturers to innovate with features catering to comfort, performance, and safety.

Market Trends

- •Electrification is a dominant trend in the Asia-Pacific utility vehicles market, as manufacturers prioritize low-emission powertrains to comply with tightening environmental regulations and meet consumer demand for sustainable solutions. This shift is supported by advances in battery technology and growing charging infrastructure.

- •Integration of advanced telematics and IoT technologies enables real-time monitoring, predictive maintenance, and enhanced fleet management, improving operational efficiency and reducing costs for commercial users in agriculture and construction sectors.

- •Customization and modular vehicle design are gaining traction, allowing end-users to tailor utility vehicles for specific tasks, thereby increasing versatility and maximizing return on investment. Manufacturers are offering customizable attachments and enhanced ergonomics to meet diverse application needs.

- •Growing consumer interest in recreational utility vehicles, especially in countries like Australia and Japan, is driving manufacturers to develop models with improved comfort, style, and safety features, expanding the market beyond traditional industrial applications.

- •Collaborative partnerships between OEMs and technology providers are accelerating innovation pipelines and enabling faster deployment of next-generation utility vehicles with smart capabilities and greener powertrains.

- •Market segmentation based on application and vehicle type is becoming more pronounced, with targeted marketing and product development strategies aimed at capturing niche segments and enhancing customer engagement.

- •Sustainability and circular economy principles are influencing vehicle design and manufacturing processes, with increased focus on recyclable materials and energy-efficient production techniques.

Market Opportunities

- •There is significant growth potential in electric utility vehicles driven by government subsidies, increasing environmental awareness, and expanding charging infrastructure across Asia-Pacific countries, offering manufacturers opportunities to innovate and differentiate products.

- •Emerging economies within the region, such as Southeast Asian countries, present untapped markets with rising agricultural mechanization and infrastructure development, creating new demand for versatile utility vehicles.

- •Technological integration opportunities exist in telematics, autonomous driving, and IoT, enabling enhanced fleet management and operational efficiency, which can be leveraged to attract commercial customers looking for cost-effective solutions.

- •Customization and modular product strategies tailored to regional requirements can help manufacturers capture diverse customer segments and increase market share by addressing specific operational challenges.

- •Collaborations and strategic partnerships with local distributors and technology providers can facilitate market entry and expansion, improving service networks and customer support.

- •Expansion into recreational utility vehicle segments in developed Asia-Pacific markets offers growth opportunities driven by lifestyle changes and increased leisure activities.

- •Sustainability-driven product innovations and adoption of circular economy principles in manufacturing can enhance brand reputation and compliance with evolving regulatory frameworks.

Market Challenges

- •High initial investment costs for electric and hybrid utility vehicles limit adoption among small-scale farmers and commercial users in price-sensitive Asia-Pacific markets, constraining market penetration despite long-term operational savings.

- •Lack of widespread charging infrastructure in many developing countries within the region hampers the growth of electric UTVs, creating logistical and operational challenges for end-users.

- •Regulatory heterogeneity across Asia-Pacific countries creates complexities for manufacturers in meeting diverse compliance requirements, increasing costs and delaying product launches.

- •Supply chain disruptions and raw material price volatility, especially for battery components, impact production costs and delivery timelines, affecting market stability and profitability.

- •Intense competition from established global players and regional manufacturers exerts pricing pressures, limiting margin expansions and requiring continuous innovation.

- •Limited consumer awareness and after-sales service networks in rural and remote areas restrict market growth and customer retention.

- •Technological challenges related to battery life, vehicle durability under harsh conditions, and integration of advanced features pose development and adoption hurdles.

Regulatory Framework

- •Between 2020 and 2025, several Asia-Pacific countries, including China and India, introduced stringent emission standards for off-road vehicles, mandating reductions in CO2 and particulate emissions to curb environmental pollution, thereby accelerating the shift towards electric and hybrid utility vehicles.

- •The implementation of safety regulations focusing on vehicle stability, operator protection, and emission controls has required manufacturers to upgrade vehicle designs and incorporate advanced safety features, enhancing market safety standards.

- •Government incentives such as tax rebates, subsidies, and reduced registration fees for electric utility vehicles have been enacted in countries like Japan, South Korea, and Australia, fostering market growth and encouraging consumer adoption.

- •Regional trade agreements and harmonization efforts within Asia-Pacific have facilitated the standardization of vehicle components and regulatory compliance processes, reducing barriers to cross-border trade and market entry.

- •Environmental policies promoting sustainable transport and renewable energy integration have led to mandatory adoption of cleaner technologies in utility vehicles, influencing product development and investment decisions.

Market Intelligence

- •15th March 2025, Kubota Corporation launched its new line of electric utility vehicles in Japan, targeting agricultural and construction sectors with enhanced battery life and advanced telematics integration. The new product range aims to reduce emissions and operational costs, aligning with government sustainability initiatives and customer demands for eco-friendly equipment. Kubota's strategic focus on electrification is expected to strengthen its market position across Asia-Pacific. Source: Kubota Official Press Release

- •28th April 2025, Mahindra & Mahindra Ltd. announced the expansion of its electric UTV portfolio in India, introducing models equipped with improved battery management systems and durability enhancements for rugged terrain use. This move supports the company's commitment to sustainable mobility and caters to increasing demand from commercial and recreational users. The launch is projected to capture significant market share in the rapidly growing electric utility vehicle segment. Source: Mahindra & Mahindra Corporate Communications

- •10th June 2025, Yamaha Motor Co., Ltd. unveiled an autonomous utility vehicle prototype equipped with AI-driven navigation and obstacle detection technologies at the Tokyo Motor Show. The innovation represents a leap forward in automation for utility vehicles, aiming to improve safety and efficiency in agriculture and industrial applications. Yamaha's initiative highlights the growing emphasis on smart vehicle technologies in the Asia-Pacific market. Source: Yamaha Motor Newsroom

- •22nd January 2025, CFMOTO (China) completed a strategic partnership with a leading battery manufacturer to develop high-performance electric utility vehicles tailored for the Asia-Pacific market. This collaboration focuses on enhancing battery capacity and reducing charging times, addressing key barriers to electric UTV adoption. The partnership is expected to accelerate product development and expand market reach. Source: CFMOTO Corporate Announcement

Regional Outlook

The China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, India is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Japan

- China

- Southeast Asia

- India

- Australia

- South Korea

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.7 Billion |

| Forecast Year Market Size | USD 17.2 Billion |

| CAGR | 7.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.3% |

| Scope of Report | Market is segmented by Product Type (Electric Utility Vehicles (Electric UTV), Gasoline Utility Vehicles (Gasoline UTV), Diesel Utility Vehicles (Diesel UTV), Hybrid Utility Vehicles (Hybrid UTV), Others (including LPG and specialized utility vehicles)), Application (Agriculture, Construction, Mining, Forestry, Recreation), End-Use Industry (Agriculture and Farming, Construction and Infrastructure, Mining and Quarrying, Forestry and Logging), Distribution Channel (Dealerships, Online Sales Platforms, Direct Sales) |

| Regions Covered | Japan, China, Southeast Asia, India, Australia, South Korea, Others |

| Key Companies | Polaris Inc. (United States), Kubota Corporation (Japan), Honda Motor Co., Ltd. (Japan), Yamaha Motor Co., Ltd. (Japan), BRP Inc. (Canada), John Deere (United States), Arctic Cat Inc. (United States), Suzuki Motor Corporation (Japan), CFMOTO (China), Mahindra & Mahindra Ltd. (India), Bombardier Recreational Products (Canada), Textron Inc. (United States), Kawasaki Heavy Industries Ltd. (Japan), CFMOTO Powersports (China), Linhai Motor Co., Ltd. (China), Hisun Motors Co., Ltd. (China), Can-Am (Canada), Odes Motorcycles (China), TGB Corporation (Taiwan), Textron Specialized Vehicles (United States), Honda R&D Co., Ltd. (Japan), Kymco (Taiwan), Polaris Asia Pacific Pty Ltd. (Australia), Kubota Australia Pty Ltd. (Australia), Suzuki Motor Corporation India Pvt. Ltd. (India) |

Asia-Pacific Utility Vehicles Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.