Global Public Sector Software Market Size, Growth & Revenue 2024-2034

Global Public Sector Software Market is segmented by Product Type (Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Document Management Systems, Analytics & Reporting Solutions, Cloud Solutions), Application (Government Administration, Public Safety & Security, Healthcare Services, Education & Training, Infrastructure Management), End-User Industry (Federal Government, State and Local Government, Healthcare Institutions, Educational Institutions), Distribution Channel (Direct Sales, Channel Partners/Resellers, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Public Sector Software market is dedicated to providing tailored software solutions that empower government and public institutions to enhance operational efficiency, service delivery, and citizen engagement. This market includes a diverse range of software types such as Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Document Management, Analytics & Reporting, and Cloud Solutions, each addressing unique governmental functions. Applications span from government administration and public safety to healthcare services, education, and infrastructure management, reflecting the broad scope of public sector responsibilities. With increasing digital transformation initiatives worldwide, public sectors are adopting these technologies to improve transparency, compliance, and responsiveness. The market encompasses both on-premise and cloud-based deployments, catering to varying organizational needs and regulatory environments. Growing emphasis on smart cities, data-driven governance, and cybersecurity further expands the market's relevance, positioning it as a cornerstone for modern public administration and societal advancement.

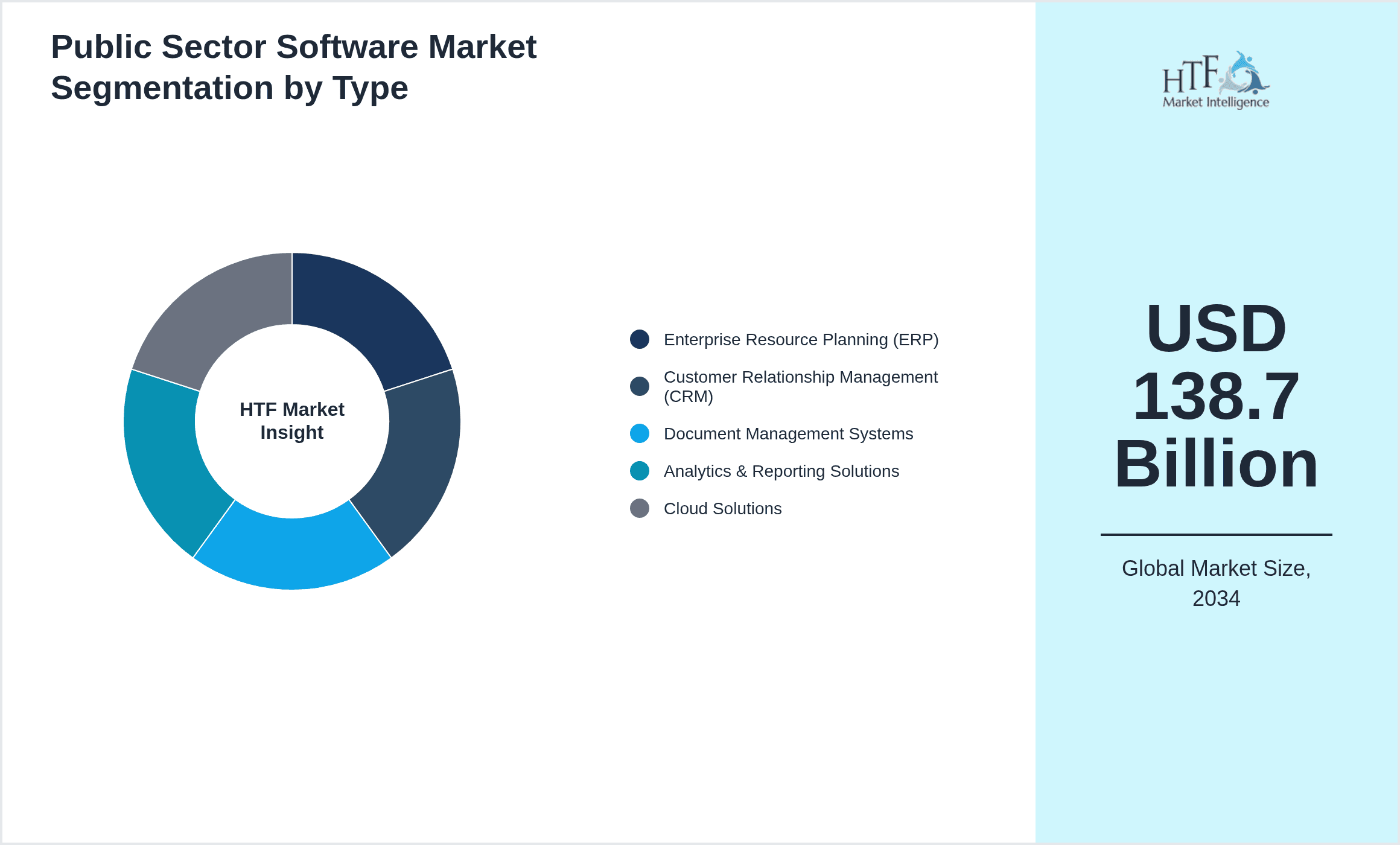

- •Key market highlights include a robust CAGR of 10.4% projected from 2024 to 2034, with the market size expected to grow from USD 52.5 Billion in 2024 to USD 138.7 Billion by 2034. North America currently dominates the market due to advanced infrastructure and high government IT spending, while Asia-Pacific is the fastest-growing region driven by rapid digitalization and increasing government investments. Enterprise Resource Planning remains the leading product type, supported by widespread adoption in resource management and operational integration, whereas Cloud Solutions are witnessing the fastest growth given their scalability and cost efficiency. Applications such as Government Administration and Public Safety & Security hold significant shares, reflecting prioritization of core governance and citizen welfare services.

- •The market offers significant value propositions by enabling governments to streamline complex operations, enhance data-driven decision-making, and improve public service delivery. Strategic importance extends across various industries including healthcare, education, infrastructure, and public safety, making it pivotal for societal development. Stakeholders such as software vendors, system integrators, and government agencies benefit from collaborative innovation, regulatory compliance, and evolving technological capabilities. The increasing focus on cloud migration, AI integration, and cybersecurity underscores the market's critical role in shaping resilient and responsive public sector ecosystems globally.

Competitive Landscape

The competitive landscape of the Global Public Sector Software market is characterized by intense rivalry among established technology providers and emerging innovators. Market players compete through continuous product innovation, strategic partnerships, and comprehensive service offerings tailored to public sector needs. Emphasis on cloud adoption, AI, and data analytics drives differentiation, with companies investing heavily in R&D to enhance scalability, security, and user experience. Multi-tiered strategies involving acquisitions and alliances are prevalent to expand geographical reach and technology portfolios. Pricing strategies vary from subscription-based models to customized enterprise solutions, aligning with diverse government budgets and procurement policies. Regional competition is influenced by local compliance requirements and government initiatives, demanding adaptive solutions and robust support infrastructures. The evolving market dynamics necessitate agility and customer-centric approaches for sustained leadership.

Leading Companies in Public Sector Software Market

- •Microsoft Corporation (United States)

- •Oracle Corporation (United States)

- •SAP SE (Germany)

- •IBM Corporation (United States)

- •Salesforce, Inc. (United States)

- •Tyler Technologies, Inc. (United States)

- •ServiceNow, Inc. (United States)

- •Cerner Corporation (United States)

- •Civica Ltd. (United Kingdom)

- •SAS Institute Inc. (United States)

- •OpenText Corporation (Canada)

- •Infor Inc. (United States)

- •Epic Systems Corporation (United States)

- •Accenture plc (Ireland)

- •NEC Corporation (Japan)

- •CGI Inc. (Canada)

- •Atos SE (France)

- •DXC Technology Company (United States)

- •Sopra Steria Group (France)

- •BAE Systems plc (United Kingdom)

- •Micro Focus International plc (United Kingdom)

- •Fujitsu Limited (Japan)

- •CGI Group Inc. (Canada)

- •KPMG International (Netherlands)

- •Deloitte Touche Tohmatsu Limited (United States)

Market Breakdown

- •By Product Type

- ◦Enterprise Resource Planning (ERP)

- ◦Customer Relationship Management (CRM)

- ◦Document Management Systems

- ◦Analytics & Reporting Solutions

- ◦Cloud Solutions

- •By Application

- ◦Government Administration

- ◦Public Safety & Security

- ◦Healthcare Services

- ◦Education & Training

- ◦Infrastructure Management

- •By End-User Industry

- ◦Federal Government

- ◦State and Local Government

- ◦Healthcare Institutions

- ◦Educational Institutions

- •By Distribution Channel

- ◦Direct Sales

- ◦Channel Partners/Resellers

- ◦Online Platforms

Growth Dynamics

- •Increasing digitization and e-governance initiatives worldwide are propelling the demand for public sector software solutions by enabling efficient service delivery and enhanced citizen engagement. Governments are prioritizing modernization of legacy systems to improve transparency and operational agility, supporting strong market growth.

- •The rising adoption of cloud-based solutions offers scalability, cost savings, and improved accessibility, driving faster deployment across diverse government agencies. Cloud migration supports remote work and disaster recovery, creating a favorable environment for innovative software offerings.

- •Growing regulatory pressures on data security and privacy compel governments to invest in robust software with advanced analytics and compliance features. This trend fosters development of specialized solutions designed to meet stringent legal and operational standards in public administration.

- •Emerging technologies such as artificial intelligence, machine learning, and robotic process automation are integrated into public sector software to enhance decision-making, automate routine tasks, and improve service quality, boosting overall market expansion.

- •Increasing government investments in smart city projects and infrastructure digitization create new avenues for software applications focused on urban planning, resource management, and citizen safety, further accelerating market demand globally.

Market Trends

- •There is a marked shift towards hybrid cloud models combining on-premise and cloud deployments to balance security concerns with flexibility, which is influencing procurement strategies among public sector entities.

- •Blockchain technology is gaining traction in the public sector for secure record-keeping and transparency, particularly in land registries and procurement processes, reflecting innovation trends in software capabilities.

- •Collaborative platforms and citizen engagement portals are increasingly integrated into government software ecosystems, enabling real-time communication and participatory governance.

- •Sustainability and green IT initiatives are shaping software development, with vendors focusing on energy-efficient data centers and eco-friendly coding practices to align with public sector goals.

- •The rise of mobile-first solutions addresses the need for accessible government services, especially in developing regions, enhancing inclusivity and expanding software adoption.

Market Opportunities

- •Expanding cloud infrastructure in emerging economies presents significant growth potential for cloud-based public sector software providers targeting untapped government segments.

- •Integration of AI-driven analytics offers opportunities to develop predictive governance tools that improve policy outcomes and resource allocation efficiency.

- •The increasing need for cybersecurity solutions tailored to public sector environments opens avenues for specialized software development and service offerings.

- •Partnerships with telecom and technology companies facilitate expansion into smart city initiatives, enabling software providers to deliver comprehensive digital infrastructure solutions.

- •Growing demand for interoperable systems across government departments encourages the creation of modular, scalable software platforms with broad integration capabilities.

Market Challenges

- •Legacy system complexities and resistance to change within government organizations hinder rapid adoption of new software solutions, affecting implementation timelines and ROI realization.

- •Budget constraints and lengthy procurement cycles in public sector entities limit the flexibility and speed of software deployment, impacting market penetration rates.

- •Data privacy concerns and regulatory compliance requirements pose significant challenges for software vendors in designing universally acceptable solutions across diverse jurisdictions.

- •The shortage of skilled IT personnel in many government agencies slows down software customization, maintenance, and effective utilization, restraining market growth.

- •Interoperability issues among heterogeneous government IT systems complicate integration efforts, leading to increased costs and operational inefficiencies.

Regulatory Framework

- •Between 2019 and 2024, numerous governments worldwide have enacted data protection regulations emphasizing citizen privacy, mandating strict compliance protocols for public sector software providers to ensure secure data handling and transparency.

- •The implementation of open data policies encourages governments to adopt software solutions capable of facilitating data sharing and interoperability while maintaining confidentiality and integrity standards.

- •Cybersecurity mandates introduced in multiple regions require public sector organizations to comply with enhanced security frameworks, prompting software vendors to incorporate advanced threat detection and response features.

- •Digital accessibility laws have been strengthened, ensuring that public sector software platforms meet usability standards for individuals with disabilities, influencing design and development practices.

- •Government procurement reforms focus on transparency and fairness, impacting vendor selection criteria and encouraging adoption of certified, compliant software solutions.

Market Intelligence

- •12th January 2025, Microsoft Corporation launched an advanced cloud-based public sector platform integrating AI-driven analytics and enhanced security features designed to support smart city initiatives and improve government service efficiency. The platform targets federal and local governments aiming to modernize infrastructure while ensuring data privacy and regulatory compliance. Strategic integrations with existing ERP and CRM solutions enable seamless migration and user adoption. This launch positions Microsoft to strengthen its leadership in the public sector software market by addressing evolving digital transformation demands. Source: Microsoft Official Press Release

- •5th March 2025, Oracle Corporation introduced a next-generation government ERP solution featuring blockchain-enabled transaction transparency and real-time reporting capabilities. The product is tailored to streamline public financial management and procurement processes, enhancing accountability and operational efficiency. Oracle's innovation supports compliance with emerging regulatory frameworks and aligns with increasing demands for digital governance tools. This launch is expected to accelerate Oracle’s market expansion in Asia-Pacific and Latin America regions. Source: Oracle Corporate Announcement

- •20th May 2025, SAP SE announced a strategic partnership with a leading cloud infrastructure provider to co-develop scalable public sector software solutions emphasizing sustainability and resilience. The collaboration focuses on delivering modular platforms adaptable to diverse government needs, integrating AI and IoT technologies to optimize resource management and citizen engagement. This initiative underscores SAP’s commitment to innovation and environmental responsibility within the public sector software domain. Source: SAP News Release

- •15th August 2025, Salesforce, Inc. completed the acquisition of a specialized public safety software firm to enhance its portfolio with advanced emergency response and citizen communication tools. The acquisition supports Salesforce's strategy to offer comprehensive digital transformation solutions to government agencies, combining CRM excellence with sector-specific innovations. This move is anticipated to boost Salesforce’s competitive positioning and accelerate growth in North America and Europe. Source: Salesforce Corporate Communication

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 52.5 Billion |

| Forecast Year Market Size | USD 138.7 Billion |

| CAGR | 10.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.4% |

| Scope of Report | Market is segmented by Product Type (Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Document Management Systems, Analytics & Reporting Solutions, Cloud Solutions), Application (Government Administration, Public Safety & Security, Healthcare Services, Education & Training, Infrastructure Management), End-User Industry (Federal Government, State and Local Government, Healthcare Institutions, Educational Institutions), Distribution Channel (Direct Sales, Channel Partners/Resellers, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Microsoft Corporation (United States), Oracle Corporation (United States), SAP SE (Germany), IBM Corporation (United States), Salesforce, Inc. (United States), Tyler Technologies, Inc. (United States), ServiceNow, Inc. (United States), Cerner Corporation (United States), Civica Ltd. (United Kingdom), SAS Institute Inc. (United States), OpenText Corporation (Canada), Infor Inc. (United States), Epic Systems Corporation (United States), Accenture plc (Ireland), NEC Corporation (Japan), CGI Inc. (Canada), Atos SE (France), DXC Technology Company (United States), Sopra Steria Group (France), BAE Systems plc (United Kingdom), Micro Focus International plc (United Kingdom), Fujitsu Limited (Japan), CGI Group Inc. (Canada), KPMG International (Netherlands), Deloitte Touche Tohmatsu Limited (United States) |

Global Public Sector Software Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.