Global Centerless Grinding Machine Market - Outlook 2024-2034

Global Centerless Grinding Machine Market is segmented by Centerless Grinding Machine Type (Through-Feed Centerless Grinding Machines, In-Feed Centerless Grinding Machines, End-Feed Centerless Grinding Machines, Specialized Centerless Grinding Machines, Automated Centerless Grinding Machines), Industrial Application (Automotive Components, Aerospace Components, Medical Device Components, General Engineering Parts, Other Industrial Applications), End-User Industry (Automotive Manufacturing, Aerospace Manufacturing, Medical Equipment Manufacturing, Heavy Machinery, Precision Engineering), Automation Technology (Manual Operation, Semi-Automatic, Fully Automatic CNC Controlled), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Centerless Grinding Machine market is defined by its focus on precision grinding solutions that operate without the need for centers to hold the workpiece, facilitating high-volume, accurate finishing of cylindrical components. This market includes diverse machine types such as through-feed, in-feed, and end-feed grinders, each catering to varied industrial applications like automotive, aerospace, and medical devices. These machines play a critical role in enhancing manufacturing productivity by offering continuous operation and superior surface finishes with minimal operator involvement. The scope extends beyond manufacturing to encompass CNC automation, Industry 4.0 integration, after-sales services, and spare parts. The industry is influenced by technological innovations, rising demand for precision components, and the need for cost-effective, high-throughput machining processes. Market participants are investing in R&D to improve machine capabilities, energy efficiency, and smart factory compatibility, positioning centerless grinding machines as essential equipment in modern manufacturing ecosystems worldwide.

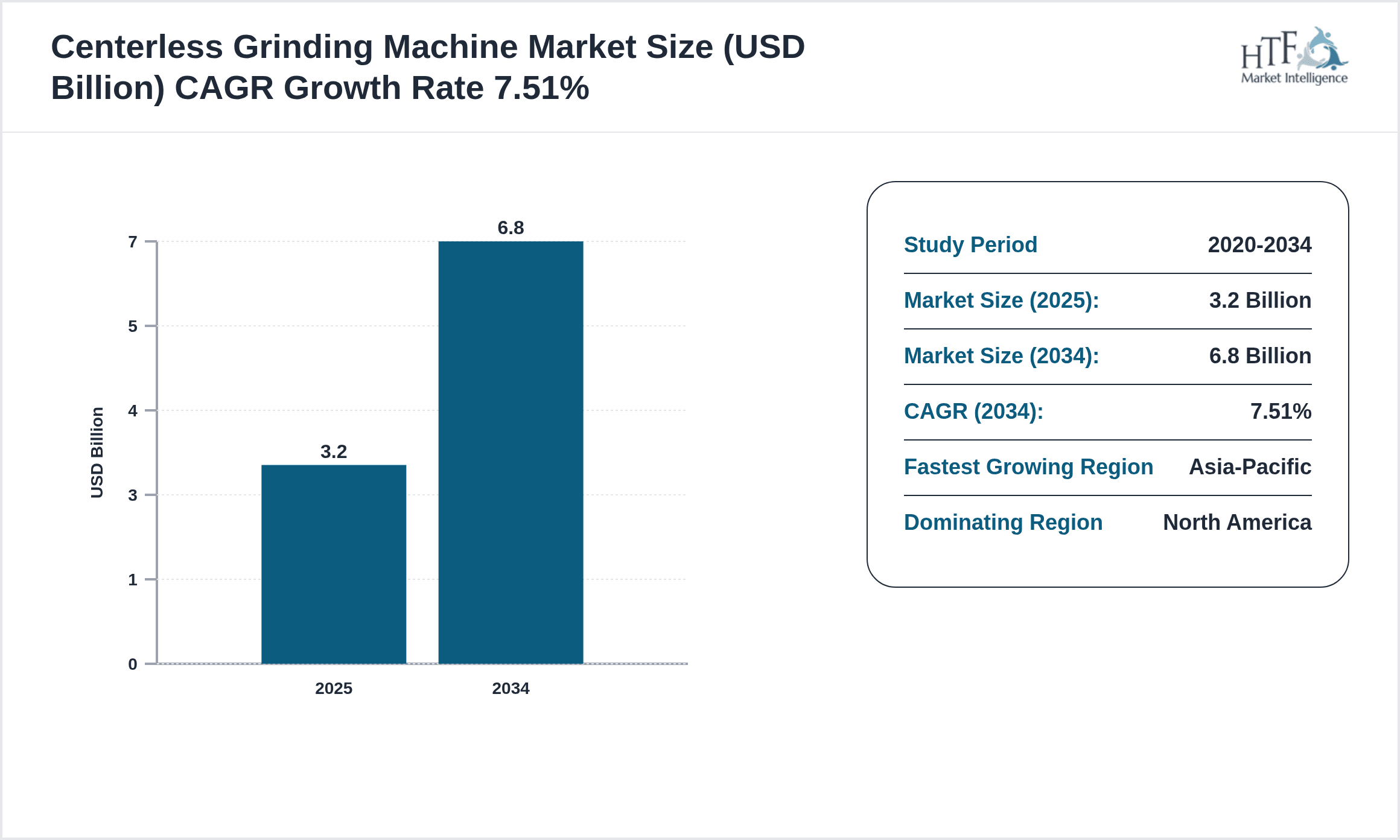

- •Key highlights include a robust CAGR of approximately 7.5% forecasted from 2024 to 2034, with market size expected to more than double from USD 3.2 billion in 2024 to USD 6.8 billion by 2034. Through-feed centerless grinders dominate the product type segment due to their efficiency in mass production, while the in-feed segment shows the fastest growth driven by increasing demand for complex precision components. Asia-Pacific emerges as the fastest-growing region, fueled by rapid industrialization and manufacturing expansion, whereas North America continues to lead in market share due to advanced manufacturing infrastructure. The automotive sector remains the largest application area, followed by aerospace and medical devices, reflecting the critical role of centerless grinding in producing high-precision parts.

- •This market offers strategic value to manufacturers, suppliers, and end-users by enabling enhanced operational efficiency, cost reduction, and product quality improvements. Centerless grinding machines support the production of critical components that meet stringent dimensional and surface finish requirements, contributing to product reliability and performance. The integration of CNC and automation technologies further strengthens the value proposition by reducing labor costs and increasing throughput. Industry stakeholders benefit from technological advancements, evolving regulatory frameworks, and growing demand across diverse sectors, positioning the centerless grinding machine market as a key enabler of modern precision manufacturing and advanced industrial processes globally.

Competitive Landscape

The global centerless grinding machine market is characterized by intense competition among established machine tool manufacturers and emerging technology providers. Market leaders focus on innovation, precision engineering, and the integration of digital technologies such as CNC controls and Industry 4.0 capabilities to differentiate their offerings. Strategic partnerships and collaborations enable companies to expand their product portfolios and geographic reach. The competitive landscape is also shaped by investments in R&D to develop energy-efficient and environmentally friendly grinding solutions, addressing evolving customer requirements. Pricing strategies vary from premium positioning for high-end machines to cost-effective models targeting emerging economies. Distribution channels include direct sales, authorized dealers, and aftermarket support services, crucial for customer retention and brand loyalty. The presence of regional players in Asia-Pacific and Europe intensifies competition, driving continuous product enhancements and customer-centric innovations. Overall, rivalry is expected to escalate with increasing demand for customized, smart grinding solutions across multiple industries worldwide.

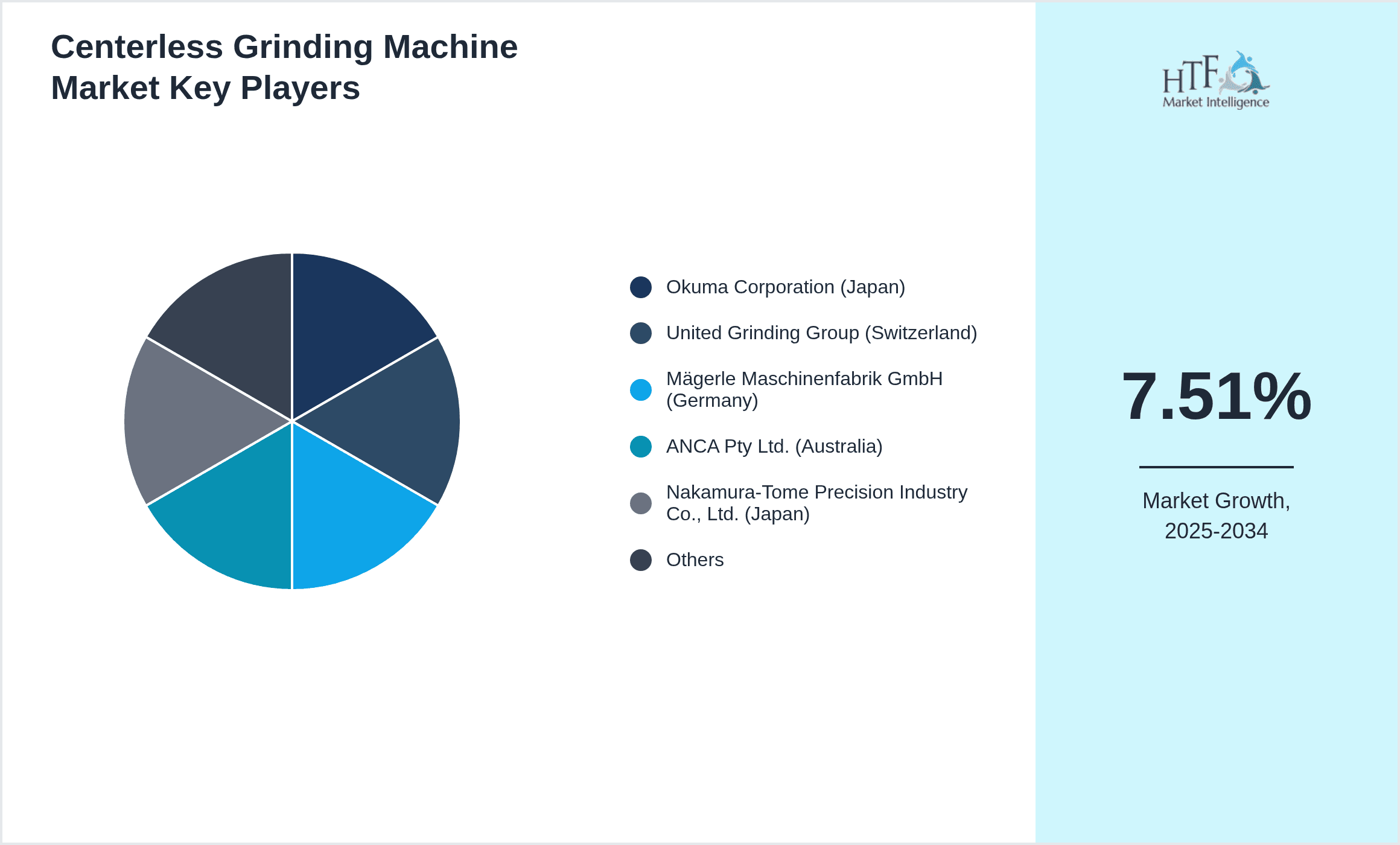

Leading Companies in Centerless Grinding Machine Market

- •Okuma Corporation (Japan)

- •United Grinding Group (Switzerland)

- •Mägerle Maschinenfabrik GmbH (Germany)

- •ANCA Pty Ltd. (Australia)

- •Nakamura-Tome Precision Industry Co., Ltd. (Japan)

- •Studer (Switzerland)

- •Chevalier Machinery Inc. (Taiwan)

- •Toyoda Machinery USA (Japan)

- •Jainnher Machine Co., Ltd. (Taiwan)

- •Danobat Group (Spain)

- •Schaudt Mikrosa GmbH (Germany)

- •Harig Machinery Company (USA)

- •Schaudt Mikrosa GmbH (Germany)

- •Chevalier Machinery Inc. (Taiwan)

- •Koyo Machinery USA, Inc. (Japan)

- •Kellenberger (Switzerland)

- •Bourn & Koch, Inc. (USA)

- •WaldrichSiegen GmbH (Germany)

- •Haas Automation, Inc. (USA)

- •Schütte GmbH & Co. KG (Germany)

- •Mitsubishi Heavy Industries Machine Tool Co., Ltd. (Japan)

- •Chevalier Machinery Inc. (Taiwan)

- •Heald Machine Co. (USA)

- •Nakamura-Tome Precision Industry Co., Ltd. (Japan)

- •Toyoda Machinery USA (Japan)

Market Breakdown

- •By Centerless Grinding Machine Type

- ◦Through-Feed Centerless Grinding Machines

- ◦In-Feed Centerless Grinding Machines

- ◦End-Feed Centerless Grinding Machines

- ◦Specialized Centerless Grinding Machines

- ◦Automated Centerless Grinding Machines

- •By Industrial Application

- ◦Automotive Components

- ◦Aerospace Components

- ◦Medical Device Components

- ◦General Engineering Parts

- ◦Other Industrial Applications

- •By End-User Industry

- ◦Automotive Manufacturing

- ◦Aerospace Manufacturing

- ◦Medical Equipment Manufacturing

- ◦Heavy Machinery

- ◦Precision Engineering

- •By Automation Technology

- ◦Manual Operation

- ◦Semi-Automatic

- ◦Fully Automatic CNC Controlled

Growth Dynamics

The global centerless grinding machine market growth is primarily driven by the expanding automotive and aerospace sectors, which demand high-precision components with tight tolerances. Increasing industrial automation and adoption of CNC technologies enhance production efficiency and machine accuracy, fueling market expansion. Emerging economies investing in advanced manufacturing infrastructure further stimulate demand. Additionally, the shift towards lightweight, high-performance materials requires sophisticated grinding solutions capable of handling complex geometries. Environmental regulations promoting energy-efficient machinery and waste reduction encourage innovation in machine design. The integration of Industry 4.0 and IoT technologies enables predictive maintenance and process optimization, increasing operational uptime and reducing costs. Together, these factors contribute to sustainable market growth, meeting evolving industrial requirements globally.

Market Trends

Recent years have witnessed a significant trend towards the adoption of fully automated and CNC-controlled centerless grinding machines, enhancing precision and reducing labor dependency. The integration of smart sensors and IoT-enabled monitoring systems allows real-time data collection and process adjustments, driving operational excellence. There is also a growing preference for eco-friendly and energy-saving machines aligned with global sustainability goals. Manufacturers are increasingly focusing on modular machine designs that enable flexibility and customization according to specific application needs. The rising use of advanced materials like composites and titanium in aerospace and medical sectors necessitates specialized grinding technologies, promoting innovation. Collaborative robotics and AI integration are emerging to further optimize grinding processes and improve safety standards in manufacturing environments worldwide.

Market Opportunities

The increasing demand for precision components in electric vehicles and renewable energy sectors presents significant growth opportunities for centerless grinding machine manufacturers. Expansion into emerging markets with growing industrial bases offers untapped potential. Developing machines with enhanced automation and predictive maintenance capabilities can attract customers seeking operational efficiency. There is also an opportunity to innovate in grinding solutions for new materials and complex geometries, addressing specialized industry needs. Collaborations with technology providers to integrate AI and machine learning for process optimization can create competitive advantages. Furthermore, aftermarket services including upgrades, training, and remote diagnostics represent additional revenue streams, enhancing customer engagement and market penetration.

Market Challenges

The centerless grinding machine market faces challenges including high initial capital investment and significant maintenance costs, which can deter small and medium enterprises. The complexity of machine operation requires skilled labor, and shortage of trained operators can impact adoption rates. Additionally, stringent environmental regulations necessitate costly compliance measures and machine adaptations. Intense competition from low-cost regional manufacturers can pressure pricing and profitability for established players. Supply chain disruptions affecting availability of precision components and raw materials also pose risks. Furthermore, rapid technological advancements demand continuous R&D investment, which may be challenging for smaller companies. Navigating these challenges requires strategic planning, investment in workforce training, and leveraging technological innovations to maintain competitive positioning.

Regulatory Framework

Between 2020 and 2024, regulatory bodies worldwide have implemented stricter environmental and safety standards impacting manufacturing equipment including centerless grinding machines. Regulations emphasize energy efficiency, emission controls, and waste management, requiring manufacturers to develop machines that minimize environmental footprints. Compliance with ISO and CE standards for machine safety and quality has become mandatory in major markets such as North America and Europe. Additionally, workplace ergonomics and operator safety norms have driven the adoption of automated and remote-controlled grinding systems. Governments have introduced incentives and subsidies for adopting green manufacturing technologies, encouraging investment in energy-saving equipment. These evolving regulations shape product development and market entry strategies, ensuring machines meet global compliance demands while supporting sustainable industrial growth.

Market Intelligence

- •15th March 2024, United Grinding Group launched a new fully automated centerless grinding machine featuring advanced CNC controls and IoT connectivity aimed at aerospace manufacturers seeking higher precision and reduced cycle times. The machine integrates predictive maintenance capabilities, enhancing uptime and operational efficiency. This launch strengthens the company’s portfolio in high-precision grinding solutions and supports Industry 4.0 adoption in aerospace component production. The product has received positive market feedback for its innovative design and energy efficiency. Source: Official United Grinding Group press release.

- •10th November 2023, Okuma Corporation introduced the Okuma Centerless 5000, a highly flexible in-feed grinding machine equipped with AI-based process optimization software. Designed for medical device and automotive industries, the machine offers enhanced accuracy and surface finish quality while reducing operator input. Okuma’s strategic initiative aims to capture growing demand in sectors requiring complex geometries and tight tolerances. The new product launch is expected to drive significant market share gains. Source: Okuma Corporation official announcement.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.2 Billion |

| Forecast Year Market Size | USD 6.8 Billion |

| CAGR | 7.51% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.25% |

| Scope of Report | Market is segmented by Centerless Grinding Machine Type (Through-Feed Centerless Grinding Machines, In-Feed Centerless Grinding Machines, End-Feed Centerless Grinding Machines, Specialized Centerless Grinding Machines, Automated Centerless Grinding Machines), Industrial Application (Automotive Components, Aerospace Components, Medical Device Components, General Engineering Parts, Other Industrial Applications), End-User Industry (Automotive Manufacturing, Aerospace Manufacturing, Medical Equipment Manufacturing, Heavy Machinery, Precision Engineering), Automation Technology (Manual Operation, Semi-Automatic, Fully Automatic CNC Controlled) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Okuma Corporation (Japan), United Grinding Group (Switzerland), Mägerle Maschinenfabrik GmbH (Germany), ANCA Pty Ltd. (Australia), Nakamura-Tome Precision Industry Co., Ltd. (Japan), Studer (Switzerland), Chevalier Machinery Inc. (Taiwan), Toyoda Machinery USA (Japan), Jainnher Machine Co., Ltd. (Taiwan), Danobat Group (Spain), Schaudt Mikrosa GmbH (Germany), Harig Machinery Company (USA), Schaudt Mikrosa GmbH (Germany), Chevalier Machinery Inc. (Taiwan), Koyo Machinery USA, Inc. (Japan), Kellenberger (Switzerland), Bourn & Koch, Inc. (USA), WaldrichSiegen GmbH (Germany), Haas Automation, Inc. (USA), Schütte GmbH & Co. KG (Germany), Mitsubishi Heavy Industries Machine Tool Co., Ltd. (Japan), Chevalier Machinery Inc. (Taiwan), Heald Machine Co. (USA), Nakamura-Tome Precision Industry Co., Ltd. (Japan), Toyoda Machinery USA (Japan) |

Global Centerless Grinding Machine Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.