Global Nuclear Density Gauge Market Size, Growth & Revenue 2025-2034

Global Nuclear Density Gauge Market is segmented by Nuclear Density Gauge Product Type (Portable Nuclear Density Gauges, Fixed Nuclear Density Gauges, Non-Nuclear Density Gauges, Hybrid Density Gauges, Advanced Sensor-Based Gauges), Application Segment (Construction Testing, Soil Compaction, Asphalt Compaction, Concrete Density Measurement, Industrial Quality Assurance), Service Type (Calibration Services, Maintenance & Repair, Training & Certification, Technical Support), Deployment Model (Cloud-Enabled Devices, On-Premise Solutions, Hybrid Deployment), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Nuclear Density Gauge market is defined by a wide array of precision instruments designed to measure the density and moisture content of construction materials such as soil, asphalt, and concrete. These devices are essential for ensuring the integrity and quality of infrastructure projects by providing accurate, real-time data critical for compaction and material performance verification. The market covers portable nuclear density gauges widely used onsite for construction and road maintenance, fixed gauges for ongoing monitoring, and emerging non-nuclear and hybrid technologies aimed at improving safety and reducing regulatory constraints. End users span construction companies, civil engineering firms, governmental agencies, and industrial quality assurance entities that rely on these measurements to comply with stringent regulations and enhance operational efficiency. The value chain involves raw material sourcing, advanced manufacturing processes, calibration and testing services, and distribution networks that serve a global clientele. The market is driven by increased infrastructure development globally, regulatory emphasis on construction quality, technological innovations improving device safety and accuracy, and growing demand in emerging regions. Applications include soil compaction testing, asphalt density verification, concrete density measurement, and industrial quality assurance, each critical to maintaining structural integrity and environmental standards. As global urbanization accelerates, the demand for reliable nuclear density gauges is projected to grow steadily over the forecast period, supported by advancements in hybrid sensor integration and digital data management.

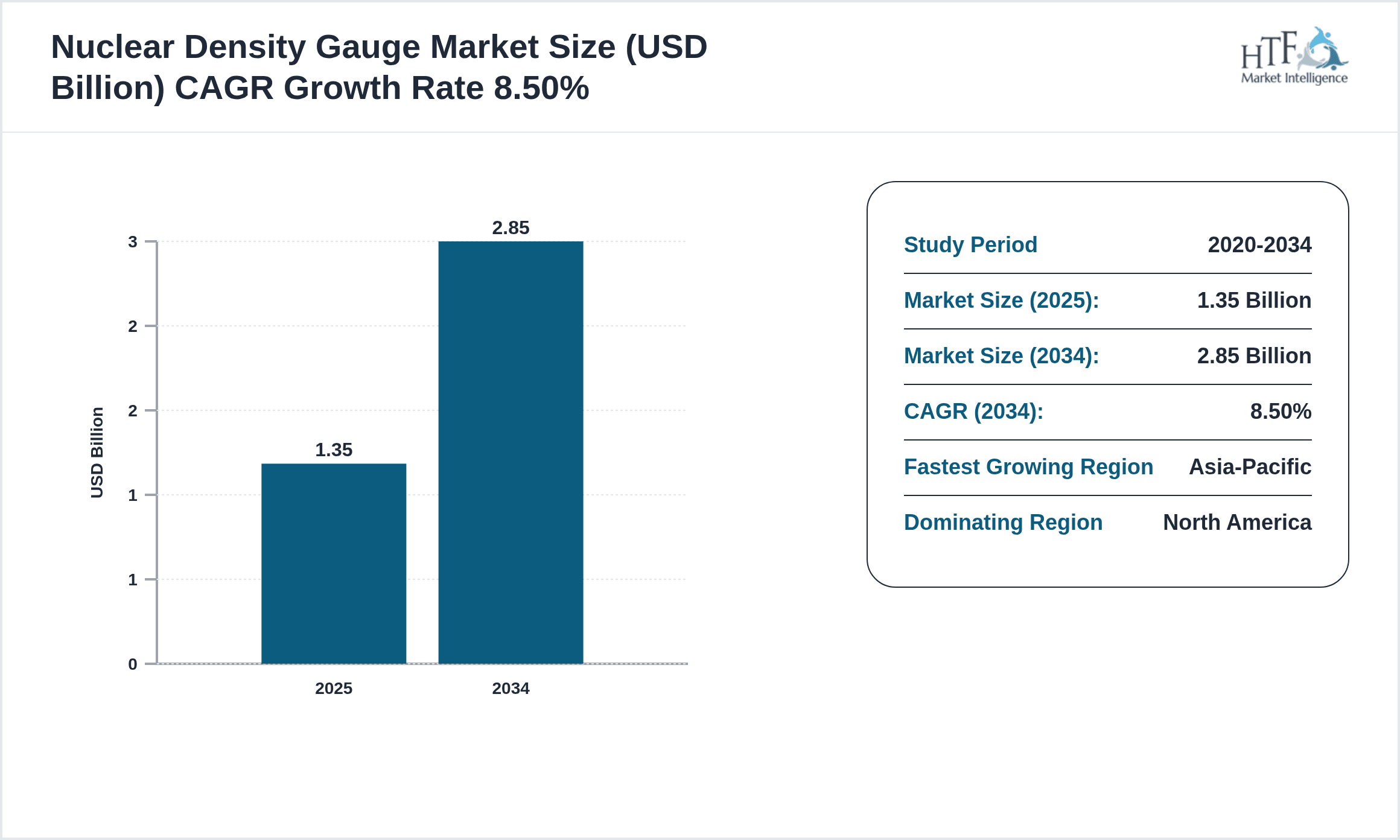

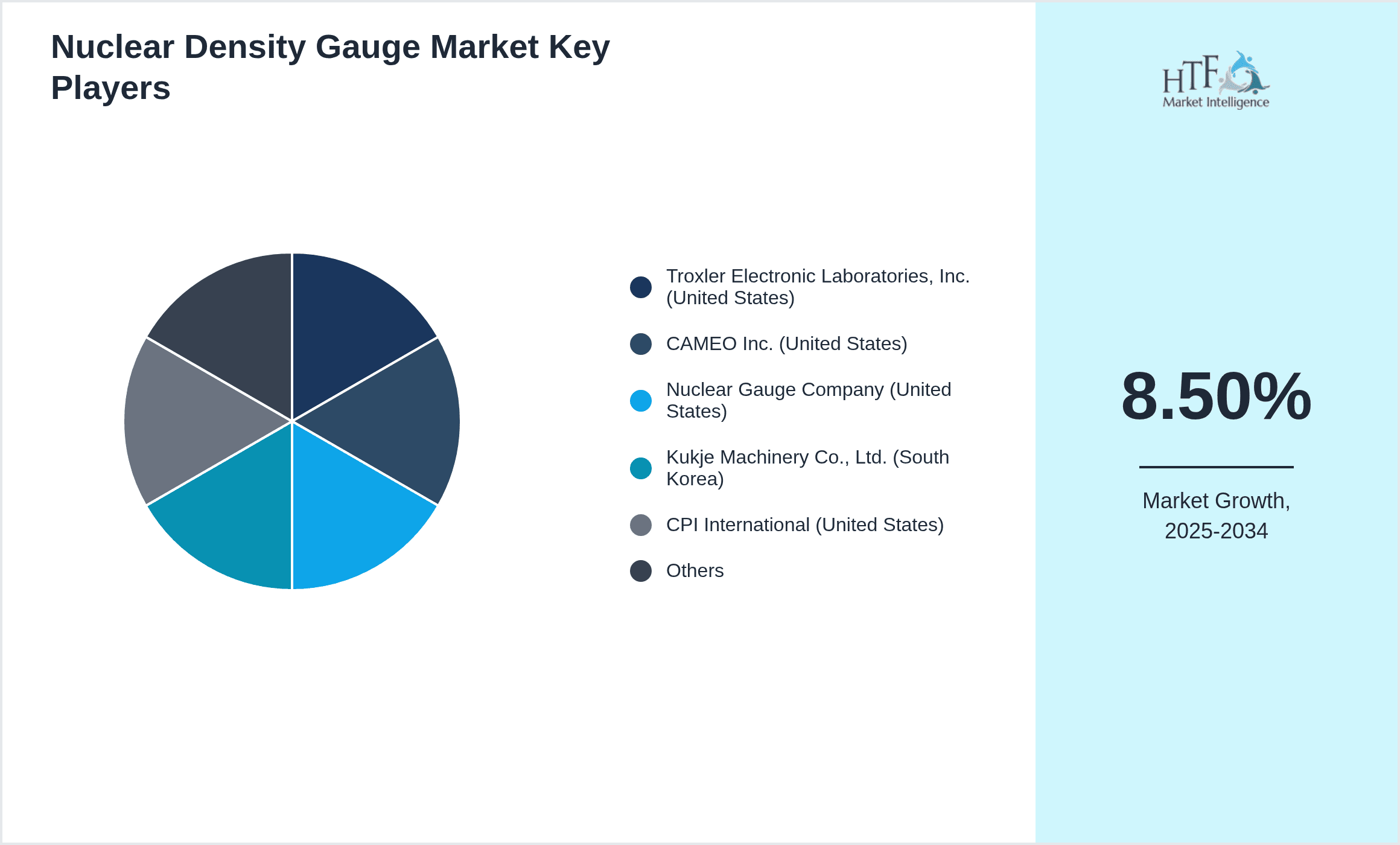

- •Key market highlights include a base market size of USD 1.35 Billion in 2025 expanding to USD 2.85 Billion by 2034, reflecting a robust CAGR of 8.5%. North America currently dominates the market, driven by extensive infrastructure projects and stringent regulatory frameworks. Asia-Pacific is the fastest growing region due to rapid urbanization, infrastructure modernization, and increased adoption of advanced gauge technologies. Portable nuclear density gauges lead the product segment owing to their ease of use and versatility, while hybrid density gauges are the fastest growing type, offering enhanced safety and operational efficiency. Market growth is supported by technological innovation, regulatory compliance requirements, and rising awareness of the benefits of precise density measurement in construction quality assurance.

- •The nuclear density gauge market holds significant strategic importance across multiple industries including construction, civil engineering, and industrial manufacturing. Accurate density measurement ensures structural safety, compliance with legal standards, and cost-effective project execution. Stakeholders including manufacturers, distributors, regulatory bodies, and end users benefit from advancements in gauge technology that reduce radiation risks and improve data reliability. The market's expansion is critical for supporting global infrastructure development, environmental sustainability, and innovation in material testing methodologies. As the market evolves, opportunities for integration with digital monitoring systems and remote data analytics are expected to redefine operational paradigms, offering enhanced value propositions to customers and investors alike.

Competitive Landscape

The competitive environment in the global Nuclear Density Gauge market is characterized by a mix of established multinational corporations and emerging specialized technology providers. Market dynamics revolve around innovation in gauge safety and accuracy, with companies investing heavily in R&D to develop non-nuclear and hybrid sensor technologies that address regulatory and environmental concerns. Competitive strategies include product differentiation through advanced features such as wireless data transmission, real-time analytics, and ergonomic design. Strategic partnerships and collaborations between technology firms and construction service providers enhance market reach and customer engagement. Mergers and acquisitions play a pivotal role in market consolidation, enabling companies to expand geographic presence and product portfolios. Pricing strategies are influenced by the cost of raw materials, technological complexity, and customer demand for precision instruments. Distribution channels are diversified across direct sales, authorized dealers, and digital platforms, facilitating global accessibility. The market entry barriers include high capital investment, stringent regulatory approvals, and the need for specialized technical expertise. Regional competition is intensified in Asia-Pacific, where rapid infrastructure development fuels demand and innovation. Future trends point towards increased adoption of digital integration, automation, and environmentally friendly gauge technologies, shaping the competitive landscape towards sustainability and operational efficiency.

Leading Companies in Nuclear Density Gauge Market

- •Troxler Electronic Laboratories, Inc. (United States)

- •CAMEO Inc. (United States)

- •Nuclear Gauge Company (United States)

- •Kukje Machinery Co., Ltd. (South Korea)

- •CPI International (United States)

- •Geotek Ltd. (United Kingdom)

- •INNOVATEST Europe B.V. (Netherlands)

- •Thermo Fisher Scientific Inc. (United States)

- •Mirion Technologies, Inc. (United States)

- •MKS Instruments, Inc. (United States)

- •Niton Analyzers (United States)

- •Ludlum Measurements, Inc. (United States)

- •Radiation Solutions, Inc. (Canada)

- •FARO Technologies, Inc. (United States)

- •Berthold Technologies GmbH & Co. KG (Germany)

- •Shimadzu Corporation (Japan)

- •Thermo Fisher Scientific (United States)

- •Bureau Veritas S.A. (France)

- •Hexagon AB (Sweden)

- •Aperio Diagnostics (United States)

- •Fluke Corporation (United States)

- •Agilent Technologies, Inc. (United States)

- •Carl Zeiss AG (Germany)

- •Hitachi High-Tech Corporation (Japan)

- •PerkinElmer, Inc. (United States)

Market Breakdown

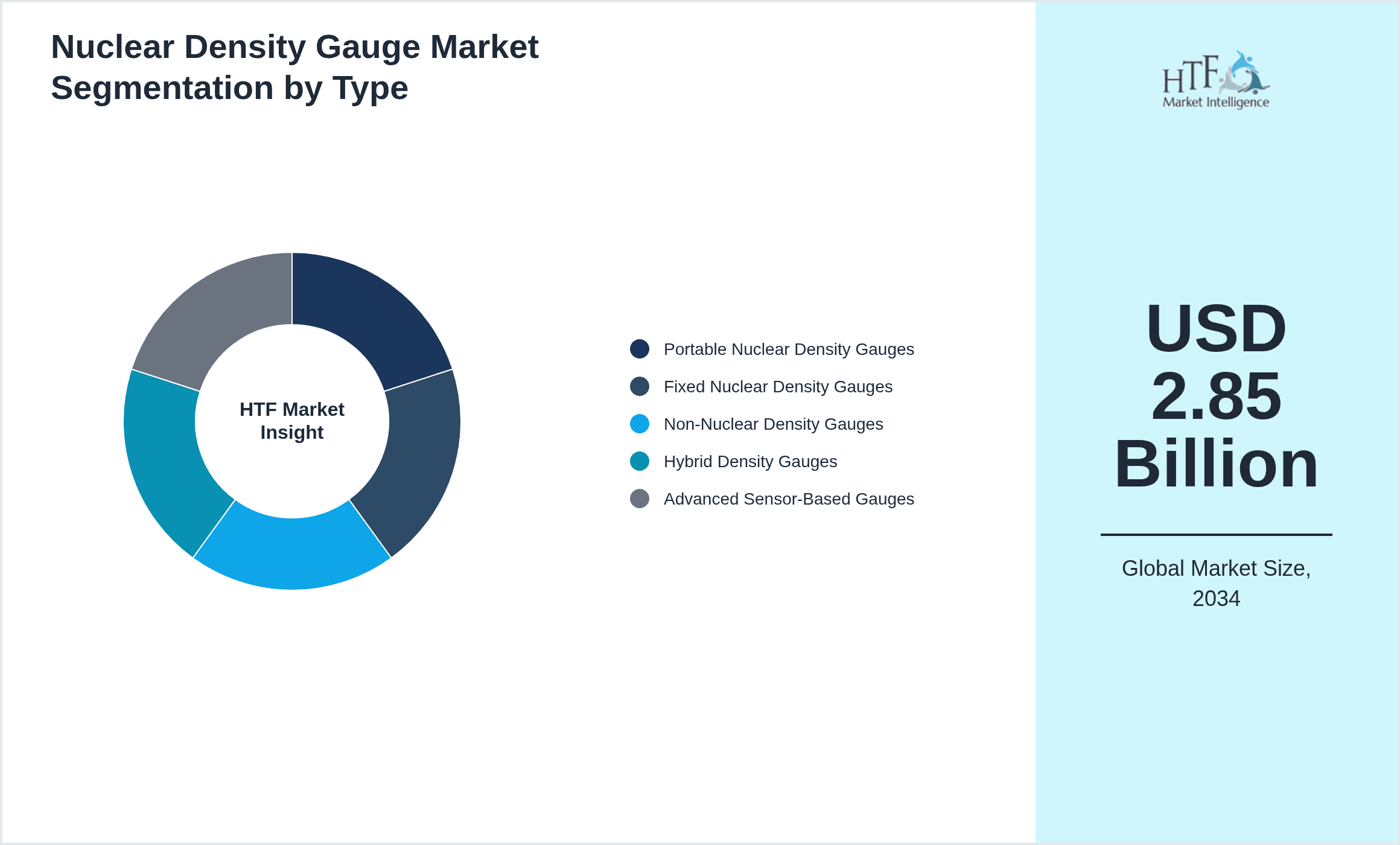

- •By Nuclear Density Gauge Product Type

- ◦Portable Nuclear Density Gauges

- ◦Fixed Nuclear Density Gauges

- ◦Non-Nuclear Density Gauges

- ◦Hybrid Density Gauges

- ◦Advanced Sensor-Based Gauges

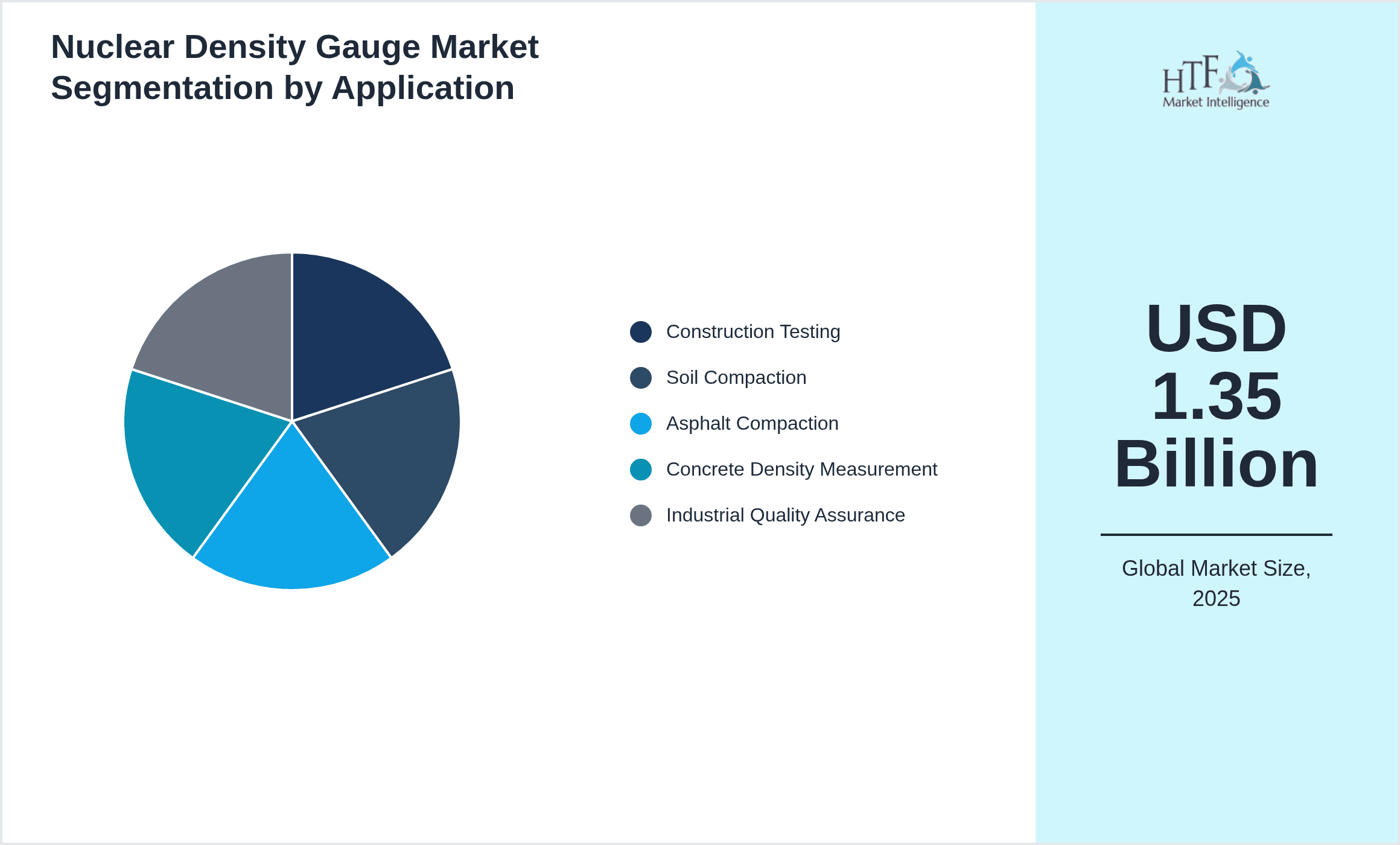

- •By Application Segment

- ◦Construction Testing

- ◦Soil Compaction

- ◦Asphalt Compaction

- ◦Concrete Density Measurement

- ◦Industrial Quality Assurance

- •By Service Type

- ◦Calibration Services

- ◦Maintenance & Repair

- ◦Training & Certification

- ◦Technical Support

- •By Deployment Model

- ◦Cloud-Enabled Devices

- ◦On-Premise Solutions

- ◦Hybrid Deployment

Growth Dynamics

- •Increasing global infrastructure investments are driving demand for nuclear density gauges as governments prioritize quality control in road and building construction projects. This trend is particularly strong in emerging economies where rapid urbanization necessitates reliable compaction measurement to ensure structural safety.

- •Technological advancements in hybrid and non-nuclear density gauges are reducing radiation concerns and regulatory barriers, enabling wider adoption across diverse construction and industrial sectors. Enhanced device portability and real-time data analytics are improving operational efficiency on job sites.

- •Stringent government regulations and standards concerning construction material quality and environmental safety are compelling contractors and engineers to utilize certified nuclear density gauges, thus bolstering market growth globally. Compliance ensures project approvals and reduces liability risks.

- •Growing emphasis on sustainability and environmental monitoring in construction projects is encouraging the use of advanced density measurement technologies that minimize ecological impact, supporting green building certifications and eco-friendly infrastructure development.

- •The integration of cloud computing and IoT with nuclear density gauges enables remote monitoring and data management, enhancing decision-making processes and reducing manual errors. This digital transformation is attracting investments and fostering new market opportunities.

- •Expansion of construction activities in Asia-Pacific, driven by governmental infrastructure initiatives, is significantly contributing to the rapid growth of the nuclear density gauge market in the region, creating a lucrative environment for new entrants and existing players.

- •Increased awareness of the importance of quality assurance in industrial manufacturing processes is driving the adoption of nuclear density gauges beyond traditional construction applications, diversifying market demand and application scopes.

Market Trends

- •The market is witnessing a shift towards hybrid nuclear density gauges combining traditional radiation technology with advanced sensor systems to provide safer, more accurate measurements, reducing the dependency on radioactive materials.

- •Digitalization and cloud connectivity are becoming standard features, allowing real-time data access, remote diagnostics, and integration with project management software, enhancing operational transparency and efficiency.

- •Sustainability-focused construction is driving demand for eco-friendly density measurement solutions, with non-nuclear gauges gaining traction as regulatory frameworks tighten around radiation safety and environmental impact.

- •The rise of smart infrastructure and IoT-enabled construction sites is fostering innovation in nuclear density gauge designs, incorporating wireless communication and automated reporting to streamline quality control workflows.

- •Collaborations between gauge manufacturers and technology firms are increasing, aiming to develop next-generation devices with enhanced safety, usability, and analytics capabilities, accelerating market evolution.

- •Emerging markets in Latin America and the Middle East are adopting nuclear density gauge technology at an accelerated pace, driven by infrastructure modernization programs and international construction standards adoption.

- •The competitive landscape is increasingly focused on product differentiation through ergonomic design, extended battery life, and user-friendly interfaces to meet the demands of field operators and reduce training requirements.

Market Opportunities

- •Developing hybrid nuclear density gauges that minimize radioactive material use presents a significant growth opportunity by addressing health and regulatory concerns, expanding market acceptance globally.

- •Expanding penetration in emerging economies through tailored product offerings and localized service networks can unlock substantial market potential, especially in fast-growing Asia-Pacific and Latin American regions.

- •Integration of AI and machine learning algorithms with nuclear density data can enhance predictive maintenance and quality forecasting, offering new service-based revenue models for manufacturers and service providers.

- •Growing demand for digital construction solutions opens avenues for cloud-enabled nuclear density gauges that facilitate remote monitoring, data analytics, and seamless integration with Building Information Modeling (BIM) systems.

- •Strategic partnerships with construction and infrastructure firms to provide end-to-end quality assurance solutions can create differentiated offerings and increase customer loyalty.

- •Innovative rental and leasing models for nuclear density gauges can reduce upfront costs for small and medium enterprises, broadening the customer base and encouraging adoption.

- •Development of region-specific calibration and certification services aligned with local regulatory frameworks can improve market penetration and compliance adherence.

Market Challenges

- •Stringent regulations and safety concerns related to the use of radioactive materials in nuclear density gauges pose significant barriers to market growth and product acceptance in certain regions.

- •High costs associated with advanced nuclear density gauge technologies and maintenance can limit adoption, especially among small and medium-sized construction firms in developing markets.

- •Technical complexities in device calibration and the need for skilled operators create challenges in widespread deployment and consistent data accuracy across diverse field conditions.

- •Competition from alternative non-nuclear density measurement technologies that offer safer and simpler operation may reduce demand for traditional nuclear gauges over time.

- •Supply chain disruptions impacting availability of specialized components and materials can delay production and increase costs, affecting market dynamics.

- •Lack of awareness and training in emerging markets about the benefits and proper use of nuclear density gauges hampers market penetration and effective utilization.

- •Regulatory compliance costs and lengthy certification processes can limit innovation speed and delay product launches in multiple jurisdictions.

Regulatory Framework

- •The International Atomic Energy Agency (IAEA) established comprehensive safety standards between 2020 and 2025 to regulate the handling, transport, and use of nuclear density gauges, ensuring radiation protection and environmental safety. These guidelines require manufacturers and users to implement strict controls and certifications.

- •In North America, the Nuclear Regulatory Commission (NRC) enforced enhanced licensing requirements from 2020 to 2025, mandating rigorous device testing, operator training, and periodic audits, which have significantly improved safety and compliance in the nuclear density gauge market.

- •The European Union’s Euratom Directive revisions implemented during the 2021-2025 period introduced stricter limits on radioactive source activity in nuclear gauges, promoting the development and adoption of non-nuclear alternatives and hybrid technologies.

- •Regulatory frameworks in Asia-Pacific countries like Japan and South Korea have progressively aligned with international standards, establishing mandatory certification and calibration protocols for nuclear density gauges to ensure accuracy and safety in construction and industrial applications.

- •Government initiatives providing incentives for the adoption of low-radiation and non-nuclear measurement devices have emerged between 2023 and 2025, accelerating innovation and market shifts towards safer technology solutions globally.

Market Intelligence

- •15th January 2025, Troxler Electronic Laboratories, Inc. announced the launch of its latest hybrid nuclear density gauge model featuring integrated sensor technology that reduces radioactive material usage by 40% while enhancing measurement accuracy. The device includes wireless connectivity and cloud integration, targeting construction firms seeking safer, real-time data solutions. This innovation is expected to set new safety benchmarks in the industry and expand adoption in regions with stringent radiation regulations. Troxler aims to leverage this launch to strengthen its market leadership and address growing environmental concerns. Source: Troxler Official Press Release

- •2nd March 2025, Mirion Technologies, Inc. introduced an AI-powered nuclear density gauge platform capable of predictive maintenance and automated quality reporting. The system integrates machine learning algorithms analyzing density data trends to forecast equipment servicing needs and potential failure points, reducing downtime and operational costs. This strategic innovation enhances the value proposition to construction and industrial customers by improving reliability and efficiency. Mirion’s initiative reflects the broader market trend of digital transformation and advanced analytics adoption. Source: Mirion Technologies Corporate Announcement

- •10th June 2025, Geotek Ltd. completed a strategic partnership with a leading global construction conglomerate to develop customized nuclear density testing solutions for large infrastructure projects in Asia-Pacific. The collaboration focuses on integrating cloud-based data management with on-site testing to optimize construction quality control workflows. This alliance is positioned to accelerate Geotek’s market penetration in high-growth regions and enhance service delivery capabilities. The partnership underscores the increasing importance of collaborative innovation in the nuclear density gauge market. Source: Geotek Ltd. Press Release

- •28th September 2025, Thermo Fisher Scientific Inc. finalized the acquisition of a niche sensor technology firm specializing in non-nuclear density measurement solutions. This acquisition aims to expand Thermo Fisher’s product portfolio with safer and environmentally friendly alternatives, aligning with evolving market demands and regulatory trends. The move is expected to consolidate Thermo Fisher’s competitive position and accelerate the transition towards hybrid technologies. Market analysts anticipate that this strategic acquisition will influence pricing and innovation dynamics in the upcoming years. Source: Thermo Fisher Scientific Investor Relations

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.35 Billion |

| Forecast Year Market Size | USD 2.85 Billion |

| CAGR | 8.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.2% |

| Scope of Report | Market is segmented by Nuclear Density Gauge Product Type (Portable Nuclear Density Gauges, Fixed Nuclear Density Gauges, Non-Nuclear Density Gauges, Hybrid Density Gauges, Advanced Sensor-Based Gauges), Application Segment (Construction Testing, Soil Compaction, Asphalt Compaction, Concrete Density Measurement, Industrial Quality Assurance), Service Type (Calibration Services, Maintenance & Repair, Training & Certification, Technical Support), Deployment Model (Cloud-Enabled Devices, On-Premise Solutions, Hybrid Deployment) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Troxler Electronic Laboratories, Inc. (United States), CAMEO Inc. (United States), Nuclear Gauge Company (United States), Kukje Machinery Co., Ltd. (South Korea), CPI International (United States), Geotek Ltd. (United Kingdom), INNOVATEST Europe B.V. (Netherlands), Thermo Fisher Scientific Inc. (United States), Mirion Technologies, Inc. (United States), MKS Instruments, Inc. (United States), Niton Analyzers (United States), Ludlum Measurements, Inc. (United States), Radiation Solutions, Inc. (Canada), FARO Technologies, Inc. (United States), Berthold Technologies GmbH & Co. KG (Germany), Shimadzu Corporation (Japan), Thermo Fisher Scientific (United States), Bureau Veritas S.A. (France), Hexagon AB (Sweden), Aperio Diagnostics (United States), Fluke Corporation (United States), Agilent Technologies, Inc. (United States), Carl Zeiss AG (Germany), Hitachi High-Tech Corporation (Japan), PerkinElmer, Inc. (United States) |

Global Nuclear Density Gauge Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.