Global Plough Market Size, Growth & Revenue 2024-2034

Global Plough Market is segmented by Type (Moldboard Ploughs, Disc Ploughs, Chisel Ploughs, Rotary Ploughs, Subsoilers), Application (Agricultural Fields, Horticulture, Landscaping, Soil Preparation, Land Reclamation), End User (Commercial Farms, Smallholder Farms, Government Agricultural Departments, Landscaping Companies), Distribution Channel (Direct Sales, Dealerships, Online Retail, Agricultural Equipment Exhibitions), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Plough Market is a critical segment within the agricultural machinery industry, focusing on soil tillage equipment essential for crop production and land management. It covers a diverse portfolio of plough types, including moldboard, disc, chisel, rotary, and subsoiler ploughs, each tailored for specific soil conditions and farming requirements. The market scope extends to applications such as large-scale farming, horticulture, landscaping, soil preparation, and land reclamation, addressing the global demand for mechanized agriculture. Increasing adoption of advanced materials and technological integration enhances plough efficiency and durability, supporting sustainable farming practices worldwide. The market's growth is propelled by rising food demand, mechanization trends, and the need for improved soil health, making it a vital component of the global agricultural supply chain.

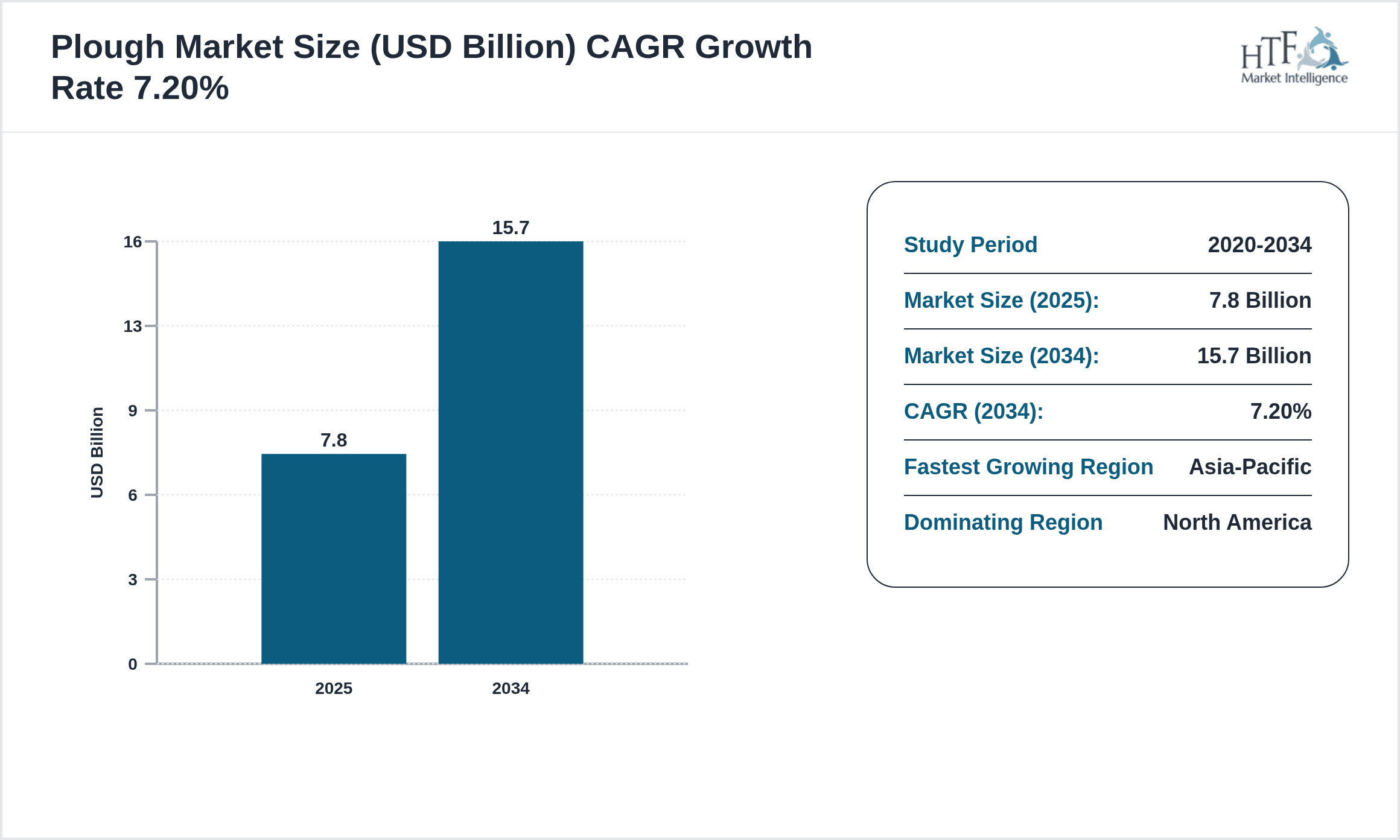

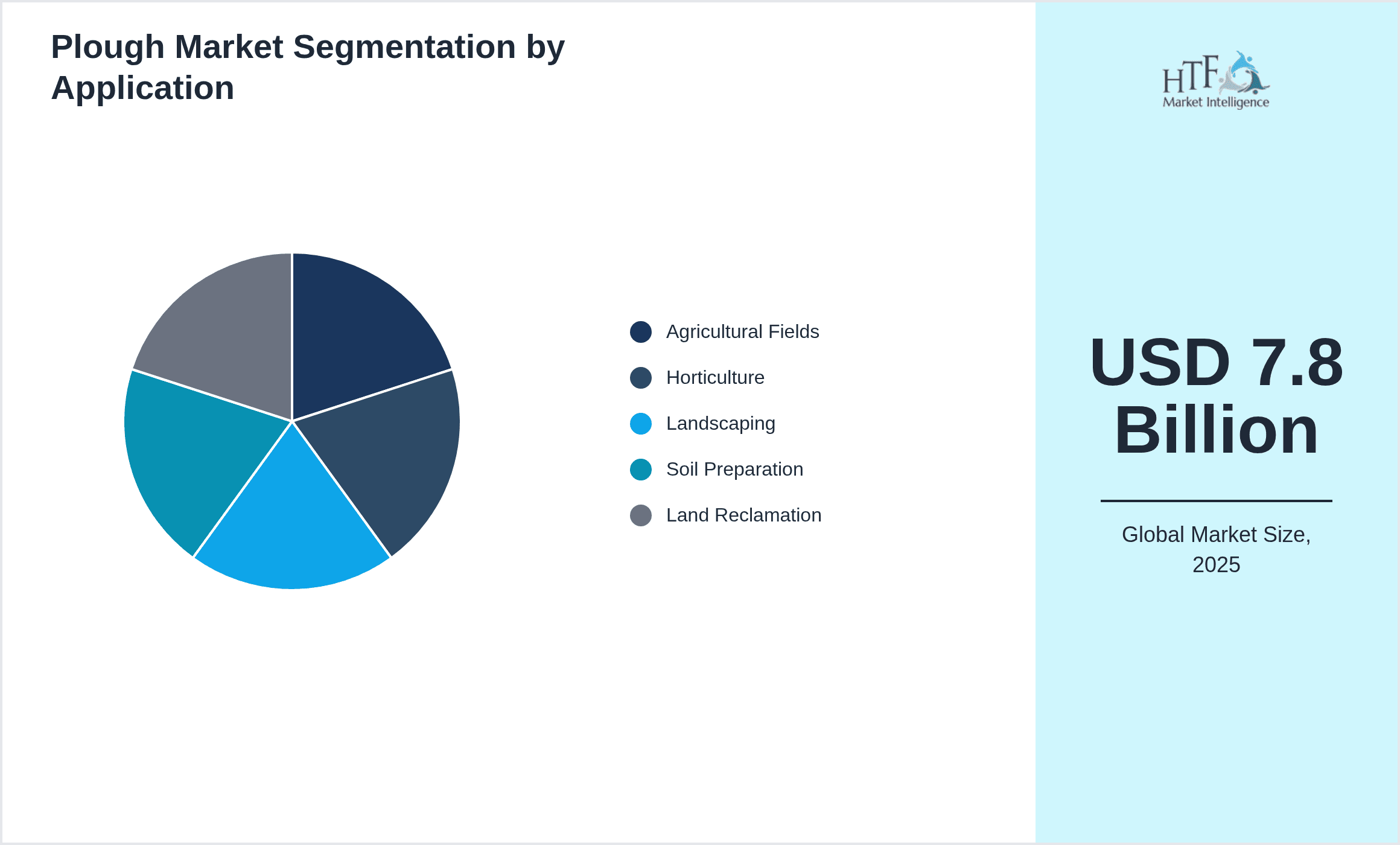

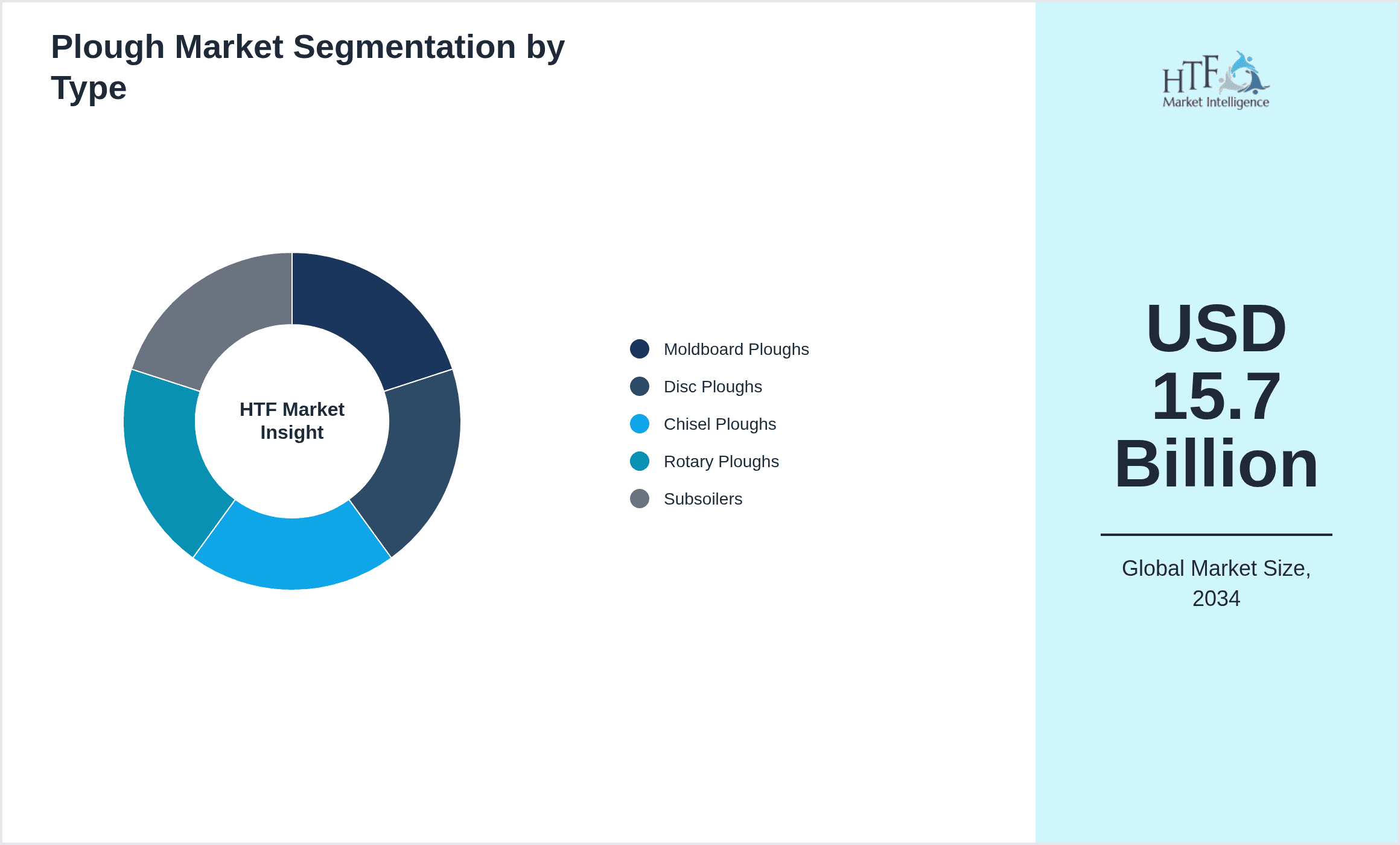

- •Key market highlights include a projected CAGR of 7.2% between 2024 and 2034, with market size expected to double from USD 7.8 Billion in 2024 to USD 15.7 Billion by 2034. North America currently dominates the market with the largest share, while Asia-Pacific is the fastest-growing region due to expanding agricultural mechanization and government support. Moldboard ploughs remain the leading product type, favored for their efficient soil turnover, although rotary ploughs show the highest growth rate due to advances in technology and adaptability to various soil types. Agricultural fields represent the primary application segment, closely followed by horticulture and landscaping sectors, reflecting the broad utility of ploughs across farming scales and types.

- •The Global Plough Market holds strategic importance as it directly impacts agricultural productivity, soil conservation, and resource management. It presents significant value propositions for equipment manufacturers, farmers, and agribusiness stakeholders by enabling efficient land preparation and sustainable farming practices. Technological advancements such as precision ploughing, automation, and durable material usage offer competitive advantages and operational cost savings. Furthermore, increasing emphasis on environmental stewardship and soil health is driving innovation and adoption of eco-friendly plough designs. As agricultural mechanization accelerates worldwide, the plough market is positioned for robust growth, underlining its critical role in feeding the growing global population and advancing modern agriculture.

Competitive Landscape

The competitive environment in the global Plough Market is characterized by a mix of well-established multinational manufacturers and specialized regional players. Market leaders focus on continuous innovation, incorporating advanced materials, automation, and digital technologies to differentiate their offerings and improve operational efficiency. Strategic partnerships and collaborations with agricultural research institutions and technology providers are common to foster product development and market expansion. Competition is intense, with companies leveraging pricing strategies, comprehensive after-sales services, and global distribution networks to strengthen market positioning. Innovation-driven differentiation, coupled with efforts to meet regional agricultural needs and sustainability criteria, creates significant market entry barriers. Future competitive trends suggest an increasing emphasis on smart ploughing solutions, integration with precision agriculture platforms, and expansion into emerging markets such as Asia-Pacific and Latin America.

Prominent Players in Plough Market

- •John Deere (United States)

- •AGCO Corporation (United States)

- •CNH Industrial N.V. (United Kingdom/Netherlands)

- •Kubota Corporation (Japan)

- •CLAAS KGaA mbH (Germany)

- •Mahindra & Mahindra Ltd. (India)

- •Väderstad AB (Sweden)

- •Kverneland Group (Norway)

- •SAME Deutz-Fahr (Italy)

- •Amazone Werke GmbH & Co. KG (Germany)

- •Argo Tractors S.p.A. (Italy)

- •Yanmar Co., Ltd. (Japan)

- •Sonalika Tractors (India)

- •Fendt (Germany)

- •New Holland Agriculture (Italy/United States)

- •Lemken GmbH & Co. KG (Germany)

- •AG Leader Technology (United States)

- •Maschio Gaspardo (Italy)

- •Kuhn Group (France)

- •Grégoire-Besson (France)

- •Horsch Maschinen GmbH (Germany)

- •Great Plains Manufacturing (United States)

- •Tatu Marchesan (Brazil)

- •Zetor Tractors (Czech Republic)

- •Shandong Lingong Construction Machinery Co., Ltd. (China)

Market Breakdown

- •By Type

- ◦Moldboard Ploughs

- ◦Disc Ploughs

- ◦Chisel Ploughs

- ◦Rotary Ploughs

- ◦Subsoilers

- •By Application

- ◦Agricultural Fields

- ◦Horticulture

- ◦Landscaping

- ◦Soil Preparation

- ◦Land Reclamation

- •By End User

- ◦Commercial Farms

- ◦Smallholder Farms

- ◦Government Agricultural Departments

- ◦Landscaping Companies

- •By Distribution Channel

- ◦Direct Sales

- ◦Dealerships

- ◦Online Retail

- ◦Agricultural Equipment Exhibitions

Growth Dynamics

- •Increasing global demand for food due to population growth is driving mechanization in agriculture, thereby boosting the adoption of ploughs for efficient soil preparation. Enhanced productivity and reduced labor costs make ploughs indispensable in both developed and emerging markets.

- •Technological advancements, such as the integration of precision farming tools and automation with plough equipment, are improving operational efficiency and soil health management, attracting investment and adoption.

- •Government initiatives and subsidies promoting sustainable agriculture and mechanization in regions like Asia-Pacific and Latin America are accelerating market growth and expanding the customer base for plough manufacturers.

- •Rising awareness of soil conservation and environmental sustainability is encouraging the development and use of advanced plough designs that minimize soil erosion and maintain fertility.

- •Growing demand for versatile plough types that can adapt to diverse soil conditions and farming practices is prompting manufacturers to innovate, thereby expanding market opportunities globally.

Market Trends

- •There is a notable trend towards the adoption of rotary ploughs equipped with GPS and IoT-enabled sensors, allowing real-time soil condition monitoring and precise tillage, improving crop yields and reducing input costs.

- •Sustainability-focused trends are driving demand for ploughs made from eco-friendly and durable materials, reducing environmental impact while ensuring long-lasting performance.

- •Manufacturers are increasingly offering customizable plough solutions tailored to specific crop types and soil conditions, enhancing user experience and operational efficiency.

- •The rise of e-commerce and digital platforms is reshaping distribution channels, enabling easier access to plough equipment in remote and underserved markets globally.

- •Collaborations between agricultural machinery companies and technology firms are fostering innovation in smart ploughing systems integrated with autonomous tractors and AI analytics.

Market Opportunities

- •Emerging economies in Asia-Pacific and Latin America offer significant growth potential due to increasing mechanization and government support for modern farming practices.

- •Development of multifunctional ploughs that combine tillage with fertilization or seeding presents new product avenues addressing farmer efficiency demands.

- •Investment in digital and precision agriculture technologies integrated with plough equipment can create competitive advantages and open new revenue streams.

- •Expanding aftermarket services and maintenance support in developing regions can enhance customer loyalty and market penetration.

- •Collaborations with agricultural research institutions to innovate soil-friendly plough designs can meet sustainability mandates and attract eco-conscious buyers.

Market Challenges

- •High initial investment costs for advanced plough equipment limit adoption among smallholder farmers, especially in developing regions with limited access to credit.

- •Lack of skilled operators and maintenance personnel can affect the optimal use and longevity of technologically sophisticated ploughs.

- •Variability in soil types and climatic conditions worldwide poses challenges to designing universally effective ploughs, requiring market-specific customization.

- •Intense competition and price sensitivity among buyers lead to narrow profit margins and pressure on manufacturers to continuously innovate cost-effectively.

- •Regulatory hurdles related to emissions, safety standards, and import-export restrictions in various regions complicate market entry and expansion strategies.

Regulatory Framework

- •Between 2019 and 2024, several regions introduced stricter environmental regulations mandating reduced emissions and noise levels from agricultural machinery, compelling plough manufacturers to innovate cleaner and quieter equipment.

- •Safety standards have been enhanced globally, requiring ploughs to include fail-safe mechanisms and operator protection features, influencing design and manufacturing protocols.

- •Trade policies and tariffs implemented during this period have impacted the global supply chain of plough components, affecting pricing and availability in certain markets.

- •Country-specific mandates in regions like Europe and North America emphasize energy efficiency and sustainability certifications for agricultural equipment to qualify for subsidies and incentives.

- •Government programs supporting mechanization in developing countries often include compliance requirements for equipment quality and environmental impact, shaping market demand and product standards.

Market Intelligence

- •15th January 2025, John Deere announced the launch of its new precision rotary plough featuring integrated GPS technology and real-time soil mapping capabilities. This innovative product targets large-scale commercial farms seeking to optimize tillage efficiency and reduce fuel consumption. The plough incorporates durable, lightweight materials to enhance performance and ease of operation while meeting stringent environmental standards. John Deere’s strategic objective is to capture growing demand in Asia-Pacific and Latin America, where mechanization trends are rapidly advancing. The launch positions John Deere as a leader in smart agricultural equipment, reinforcing its commitment to sustainable farming solutions. Source: Official John Deere Press Release

- •3rd March 2025, Kubota Corporation introduced an advanced moldboard plough model equipped with IoT-enabled sensors for monitoring soil moisture and compaction levels during operation. This product innovation aims to support sustainable soil management and increase productivity for mid-sized farms globally. Kubota’s development reflects a growing market trend towards integrating digital technologies with traditional farming implements to enhance decision-making and reduce resource use. The new plough model is expected to strengthen Kubota’s market presence in Europe and North America, where precision agriculture adoption is high. Source: Kubota Corporate Website

- •22nd April 2025, CNH Industrial N.V. announced a strategic partnership with an AI technology firm to develop autonomous ploughing systems. The collaboration focuses on creating self-driving ploughs that leverage machine learning to adapt tillage depth and speed to varying field conditions, enhancing efficiency and reducing operator fatigue. This initiative aligns with CNH’s long-term vision of integrating automation across its agricultural machinery portfolio. The partnership is expected to accelerate innovation cycles and expand CNH’s competitive edge in the global plough market. Source: Industry Publication

- •10th May 2025, Väderstad AB completed the acquisition of a regional plough manufacturer specializing in eco-friendly tillage solutions. This strategic move aims to broaden Väderstad’s product range and strengthen its foothold in emerging markets such as Latin America and Southeast Asia. The acquisition facilitates access to localized technologies and enhances Väderstad’s capacity to meet growing demand for sustainable farming equipment worldwide. This consolidation reflects ongoing market trends of mergers and acquisitions to drive growth and innovation. Source: Väderstad Official Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 7.8 Billion |

| Forecast Year Market Size | USD 15.7 Billion |

| CAGR | 7.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Type (Moldboard Ploughs, Disc Ploughs, Chisel Ploughs, Rotary Ploughs, Subsoilers), Application (Agricultural Fields, Horticulture, Landscaping, Soil Preparation, Land Reclamation), End User (Commercial Farms, Smallholder Farms, Government Agricultural Departments, Landscaping Companies), Distribution Channel (Direct Sales, Dealerships, Online Retail, Agricultural Equipment Exhibitions) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | John Deere (United States), AGCO Corporation (United States), CNH Industrial N.V. (United Kingdom/Netherlands), Kubota Corporation (Japan), CLAAS KGaA mbH (Germany), Mahindra & Mahindra Ltd. (India), Väderstad AB (Sweden), Kverneland Group (Norway), SAME Deutz-Fahr (Italy), Amazone Werke GmbH & Co. KG (Germany), Argo Tractors S.p.A. (Italy), Yanmar Co., Ltd. (Japan), Sonalika Tractors (India), Fendt (Germany), New Holland Agriculture (Italy/United States), Lemken GmbH & Co. KG (Germany), AG Leader Technology (United States), Maschio Gaspardo (Italy), Kuhn Group (France), Grégoire-Besson (France), Horsch Maschinen GmbH (Germany), Great Plains Manufacturing (United States), Tatu Marchesan (Brazil), Zetor Tractors (Czech Republic), Shandong Lingong Construction Machinery Co., Ltd. (China) |

Global Plough Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.