Global Heavy Duty Coating Market Size, Growth & Revenue 2025-2034

Global Heavy Duty Coating Market is segmented by Type (Epoxy Coatings, Polyurethane Coatings, Acrylic Coatings, Alkyd Coatings, Fluoropolymer Coatings), Application (Industrial Equipment, Automotive, Construction, Marine, Oil & Gas), Service Type (Surface Preparation, Coating Application, Inspection & Testing, Maintenance & Repair), Deployment Model (Spray Coating, Brush Coating, Roller Coating), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global heavy duty coating market is defined by its provision of robust protective coatings engineered to withstand harsh environmental and operational conditions across multiple industrial segments. These coatings include epoxy, polyurethane, acrylic, alkyd, and fluoropolymer types, each tailored to specific performance needs such as chemical resistance, abrasion protection, and corrosion prevention. Heavy duty coatings find extensive applications in industrial equipment, automotive manufacturing, construction machinery, marine vessels, and oil & gas infrastructure, where they enhance asset longevity and reduce maintenance demands. The market is driven by increasing industrialization, stringent environmental regulations mandating durable and eco-friendly coatings, and technological innovations focusing on high-performance materials and sustainable formulations. Regional dynamics highlight strong demand in North America and Asia-Pacific, with emerging economies accelerating infrastructure and industrial growth. The market also faces challenges from volatile raw material prices and regulatory complexities but offers significant opportunities through advancements in nano-coatings and green chemistry. Overall, the heavy duty coating market is poised for substantial growth driven by expanding end-use industries and evolving technological capabilities, making it a critical segment for investors and industry stakeholders globally.

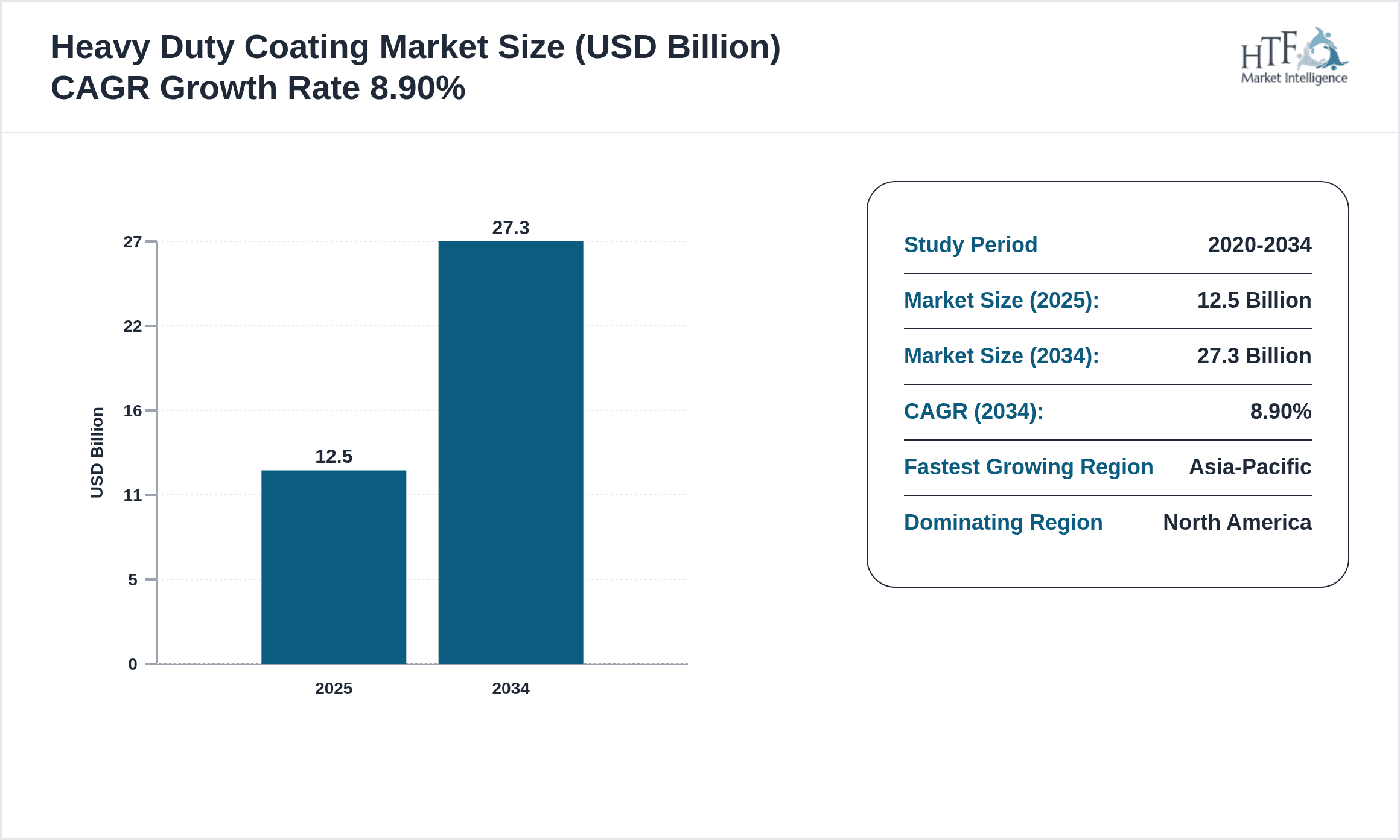

- •Key highlights indicate a base market size of USD 12.5 Billion in 2025, with projections reaching USD 27.3 Billion by 2034, reflecting a CAGR of approximately 8.9%. The Asia-Pacific region is identified as the fastest growing, propelled by rapid industrial expansion and infrastructure development. Epoxy coatings dominate the market share due to their superior adhesion and chemical resistance, while fluoropolymer coatings exhibit the highest growth trajectory driven by demand for high durability in extreme conditions. Year-on-year growth rates maintain near 8.7%, underscoring steady market expansion. The competitive landscape is marked by innovation in eco-friendly formulations and strategic partnerships aimed at broadening market reach.

- •The value proposition of heavy duty coatings lies in their ability to significantly prolong asset life, minimize downtime through reduced maintenance cycles, and comply with evolving environmental standards. This positions the market as strategically important across industries such as manufacturing, automotive, marine, and energy sectors. Investors and stakeholders benefit from understanding the market dynamics driven by regulatory frameworks, material science advancements, and regional growth disparities, enabling informed decision-making and strategic planning for sustainable growth.

Competitive Landscape

The competitive environment of the global heavy duty coating market is characterized by a diverse set of players employing multifaceted strategies to maintain and expand their market presence. Companies focus on product innovation, particularly in sustainable and high-performance coatings, to meet stringent environmental regulations and customer demands. Strategic partnerships, joint ventures, and mergers and acquisitions are common tactics to enhance technological capabilities and geographic reach. Pricing strategies balance premium product offerings with competitive cost structures to address varying market segments. Distribution channels are evolving with increased emphasis on direct sales and digital platforms for customer engagement. Regional competition is robust, with North America and Europe showcasing mature markets emphasizing quality and compliance, while Asia-Pacific is marked by rapid growth and cost-competitive strategies. Companies invest heavily in R&D to develop next-generation coatings featuring enhanced durability, corrosion resistance, and eco-friendliness. Market entry barriers such as high capital investment and regulatory compliance inhibit new entrants but encourage innovation among established players. Future trends indicate intensified competition driven by technological advancements, sustainability initiatives, and expanding end-use applications, requiring continuous strategic adaptation for competitive advantage.

Prominent Players in Heavy Duty Coating Market

- •PPG Industries (United States)

- •Sherwin-Williams Company (United States)

- •Akzo Nobel N.V. (Netherlands)

- •RPM International Inc. (United States)

- •Axalta Coating Systems Ltd. (United States)

- •Jotun Group (Norway)

- •Hempel A/S (Denmark)

- •Nippon Paint Holdings Co., Ltd. (Japan)

- •BASF SE (Germany)

- •The Valspar Corporation (United States)

- •Valspar (United States)

- •Asian Paints Limited (India)

- •RPM Performance Coatings (United States)

- •Clariant AG (Switzerland)

- •The Sherwin-Williams Company (United States)

- •PPG Architectural Coatings (United States)

- •Axalta Coating Systems (United States)

- •Rust-Oleum Corporation (United States)

- •Kansai Paint Co., Ltd. (Japan)

- •Nippon Paint Co., Ltd. (Japan)

- •Sherwin-Williams Company (United States)

- •RPM International Inc. (United States)

- •Akzo Nobel Coatings (Netherlands)

- •Jotun Coatings (Norway)

- •Hempel Coatings (Denmark)

Market Breakdown

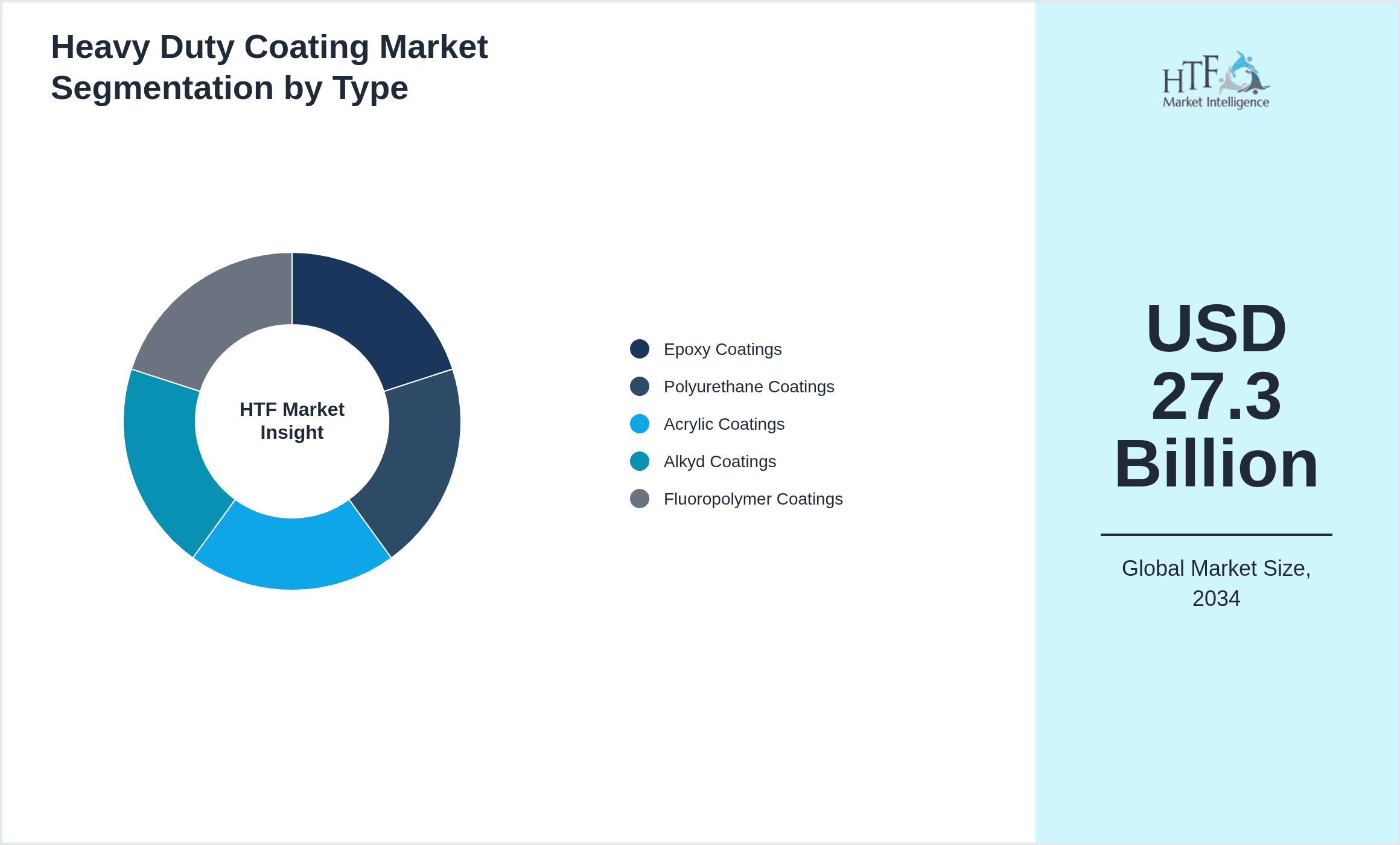

- •By Type

- ◦Epoxy Coatings

- ◦Polyurethane Coatings

- ◦Acrylic Coatings

- ◦Alkyd Coatings

- ◦Fluoropolymer Coatings

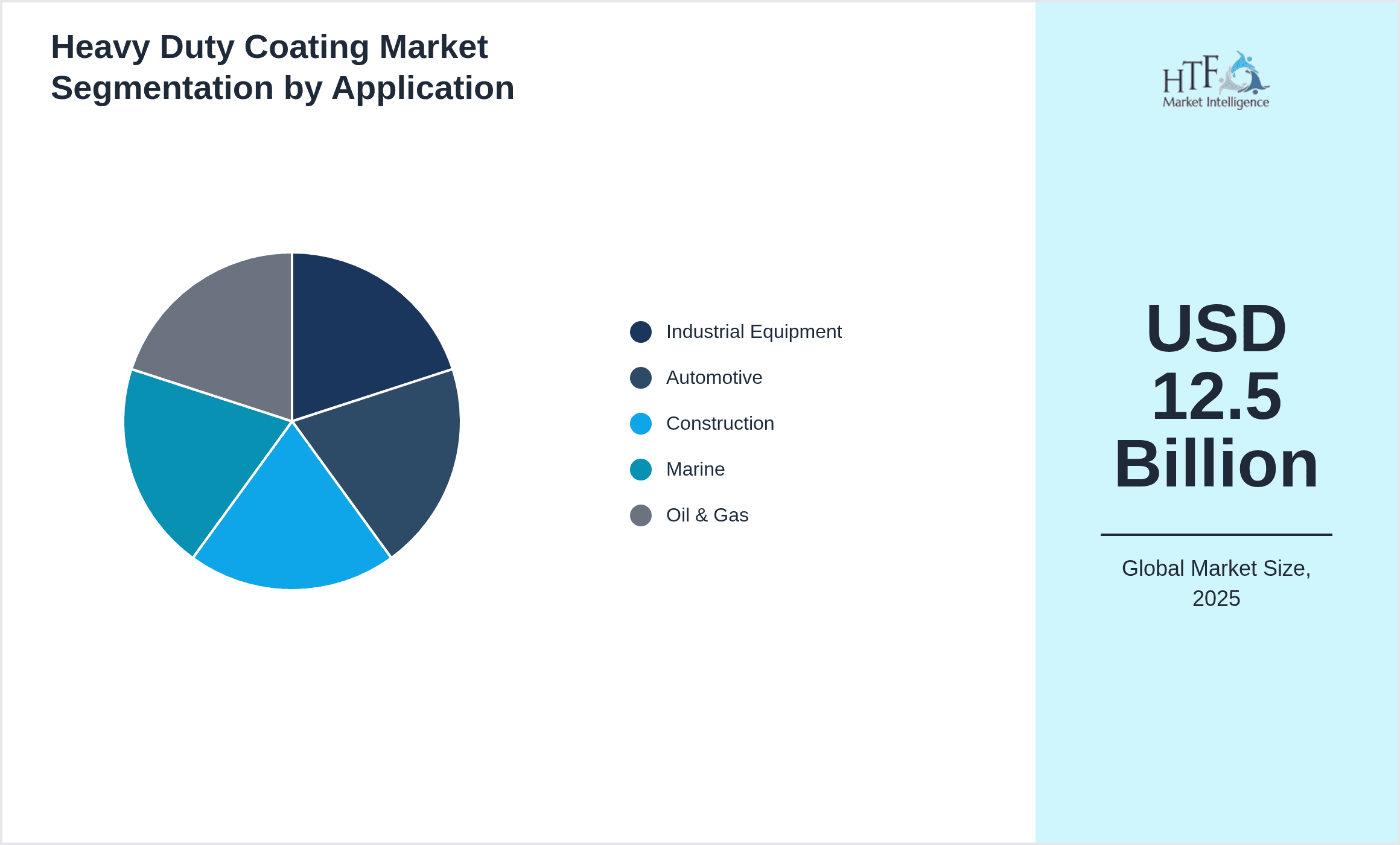

- •By Application

- ◦Industrial Equipment

- ◦Automotive

- ◦Construction

- ◦Marine

- ◦Oil & Gas

- •By Service Type

- ◦Surface Preparation

- ◦Coating Application

- ◦Inspection & Testing

- ◦Maintenance & Repair

- •By Deployment Model

- ◦Spray Coating

- ◦Brush Coating

- ◦Roller Coating

Growth Dynamics

The global heavy duty coating market is propelled by increasing industrialization and infrastructure development, especially in emerging economies. Growing demand for durable and corrosion-resistant coatings in the automotive, marine, and oil & gas sectors fuels market expansion. Technological advancements in eco-friendly and high-performance coatings enhance product appeal and regulatory compliance, driving adoption. Additionally, rising expenditures on maintenance and asset protection by industries to reduce downtime and costs further stimulate growth. The market benefits from increasing awareness about sustainability and the integration of smart coating technologies, positioning it for sustained long-term growth worldwide.

Market Trends

A significant trend is the shift toward environmentally friendly heavy duty coatings with low volatile organic compounds (VOC) content, driven by stringent global environmental regulations. There is rising adoption of fluoropolymer and nano-coatings that provide superior durability and chemical resistance. Digitization in coating application processes, such as automated spray systems, enhances efficiency and quality control. Strategic collaborations between chemical manufacturers and end-users foster innovation in customized coating solutions. Additionally, the incorporation of antimicrobial and self-healing properties in coatings is gaining traction in industrial applications, reflecting evolving market demands.

Market Opportunities

The heavy duty coating market offers substantial opportunities in developing regions due to infrastructure modernization and industrial expansion. Innovation in sustainable coatings using bio-based materials and nanotechnology represents a lucrative avenue for product differentiation. Expanding applications in renewable energy infrastructure, such as wind turbines and solar panels, provide new growth segments. Furthermore, increasing investments in marine coatings to combat biofouling and corrosion open additional markets. Collaborations and partnerships for technology transfer and regional market penetration further enable growth potential, especially in Asia-Pacific and Latin America.

Market Challenges

The market faces challenges including raw material price volatility which impacts production costs and profitability. Regulatory complexities across regions create compliance hurdles for manufacturers, especially concerning VOC emissions and hazardous substances. Technical difficulties related to coating application in extreme environments require specialized expertise and equipment. Intense competition and price sensitivity in emerging markets pressure margins. Additionally, supply chain disruptions and scarcity of skilled labor in coating application and maintenance pose operational challenges for industry players globally.

Regulatory Framework

Between 2020 and 2025, global regulatory bodies have enacted stringent norms targeting emissions of volatile organic compounds (VOCs) and hazardous air pollutants (HAPs) from coating products. Regulations such as the U.S. EPA's National Emission Standards for Hazardous Air Pollutants and the European Union’s REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) framework mandate compliance for manufacturers and users of heavy duty coatings. These regulations enforce limits on toxic substances, requiring reformulations to reduce environmental impact while maintaining performance. Regional directives in Asia-Pacific countries increasingly align with global standards, promoting sustainable coatings. Compliance with occupational health and safety standards for application processes is also emphasized globally. The regulatory landscape shapes market innovation by encouraging development of low-VOC, eco-friendly coatings and influences supply chain and product lifecycle management strategies.

Market Intelligence

- •12th February 2025, PPG Industries announced the launch of a new line of ultra-durable epoxy coatings designed for extreme industrial applications, featuring enhanced chemical resistance and faster curing times. The product targets the automotive and oil & gas sectors, aiming to reduce maintenance cycles and improve operational efficiency. This innovation incorporates advanced resin technology to meet evolving environmental regulations while delivering superior performance. PPG's strategic objective includes expanding market share in Asia-Pacific through partnerships with regional distributors. The launch is expected to reinforce PPG's leadership in the heavy duty coating segment and stimulate further industry advancements. Source: PPG Industries official press release.

- •30th March 2025, Akzo Nobel N.V. introduced a sustainable polyurethane coating system employing bio-based raw materials, marking a significant step towards eco-friendly solutions within the heavy duty coatings market. The product offers high abrasion and corrosion resistance with a reduced carbon footprint, complying with stringent global VOC regulations. Target markets include marine and construction industries, where environmental impact reduction is critical. This innovation aligns with Akzo Nobel's global sustainability goals and positions the company competitively in green coatings. The product rollout is supported by extensive field testing and customer collaborations to ensure performance reliability. Source: Akzo Nobel corporate announcement.

- •15th May 2025, Sherwin-Williams Company completed the acquisition of a regional coatings manufacturer specializing in fluoropolymer coatings, enhancing its product portfolio for heavy duty industrial applications. The acquisition aims to bolster Sherwin-Williams’ presence in the Asia-Pacific market and accelerate innovation in high-performance coatings. Strategic integration plans focus on leveraging combined R&D capabilities and expanding distribution networks. This move strengthens Sherwin-Williams’ competitive positioning and enables access to emerging growth segments, particularly in infrastructure and energy sectors. The deal reflects ongoing consolidation trends within the coatings industry to drive scale and technological leadership. Source: Sherwin-Williams official press release.

- •Market Intelligence: Recent developments and industry insights are being monitored. For the latest updates, consult official company announcements and industry publications.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 27.3 Billion |

| CAGR | 8.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.7% |

| Scope of Report | Market is segmented by Type (Epoxy Coatings, Polyurethane Coatings, Acrylic Coatings, Alkyd Coatings, Fluoropolymer Coatings), Application (Industrial Equipment, Automotive, Construction, Marine, Oil & Gas), Service Type (Surface Preparation, Coating Application, Inspection & Testing, Maintenance & Repair), Deployment Model (Spray Coating, Brush Coating, Roller Coating) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | PPG Industries (United States), Sherwin-Williams Company (United States), Akzo Nobel N.V. (Netherlands), RPM International Inc. (United States), Axalta Coating Systems Ltd. (United States), Jotun Group (Norway), Hempel A/S (Denmark), Nippon Paint Holdings Co., Ltd. (Japan), BASF SE (Germany), The Valspar Corporation (United States), Valspar (United States), Asian Paints Limited (India), RPM Performance Coatings (United States), Clariant AG (Switzerland), The Sherwin-Williams Company (United States), PPG Architectural Coatings (United States), Axalta Coating Systems (United States), Rust-Oleum Corporation (United States), Kansai Paint Co., Ltd. (Japan), Nippon Paint Co., Ltd. (Japan), Sherwin-Williams Company (United States), RPM International Inc. (United States), Akzo Nobel Coatings (Netherlands), Jotun Coatings (Norway), Hempel Coatings (Denmark) |

Global Heavy Duty Coating Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.