Global Aircraft Carpet Market Size, Growth & Revenue 2024-2034

Global Aircraft Carpet Market is segmented by Carpet Type (Nylon Aircraft Carpets, Polyester Aircraft Carpets, Wool Aircraft Carpets, Acrylic Aircraft Carpets, Olefin Aircraft Carpets), Aircraft Application (Commercial Aircraft, Military Aircraft, Private Jets, Helicopters, Cargo Aircraft), Installation Type (Original Equipment Manufacturer (OEM) Installation, Aftermarket Installation), Distribution Channel (Direct Sales, Distributors/Dealers, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Aircraft Carpet Market refers to the specialized segment focusing on the production and supply of carpets designed explicitly for aircraft interiors. These carpets serve multiple purposes, including enhancing passenger comfort, improving cabin aesthetics, reducing noise, and meeting strict safety and fire resistance standards mandated by aviation authorities. The market covers a wide range of aircraft types such as commercial airliners, military aircraft, private jets, helicopters, and cargo planes, with materials tailored to meet their specific operational demands. The industry includes various carpet types like nylon, polyester, wool, acrylic, and olefin, each selected based on durability, weight, and performance characteristics. The scope extends to innovations in eco-friendly materials and advanced manufacturing processes which are reshaping market growth. Increasing global air travel, aircraft refurbishment cycles, and stringent regulatory frameworks are primary drivers shaping this market's expansion worldwide.

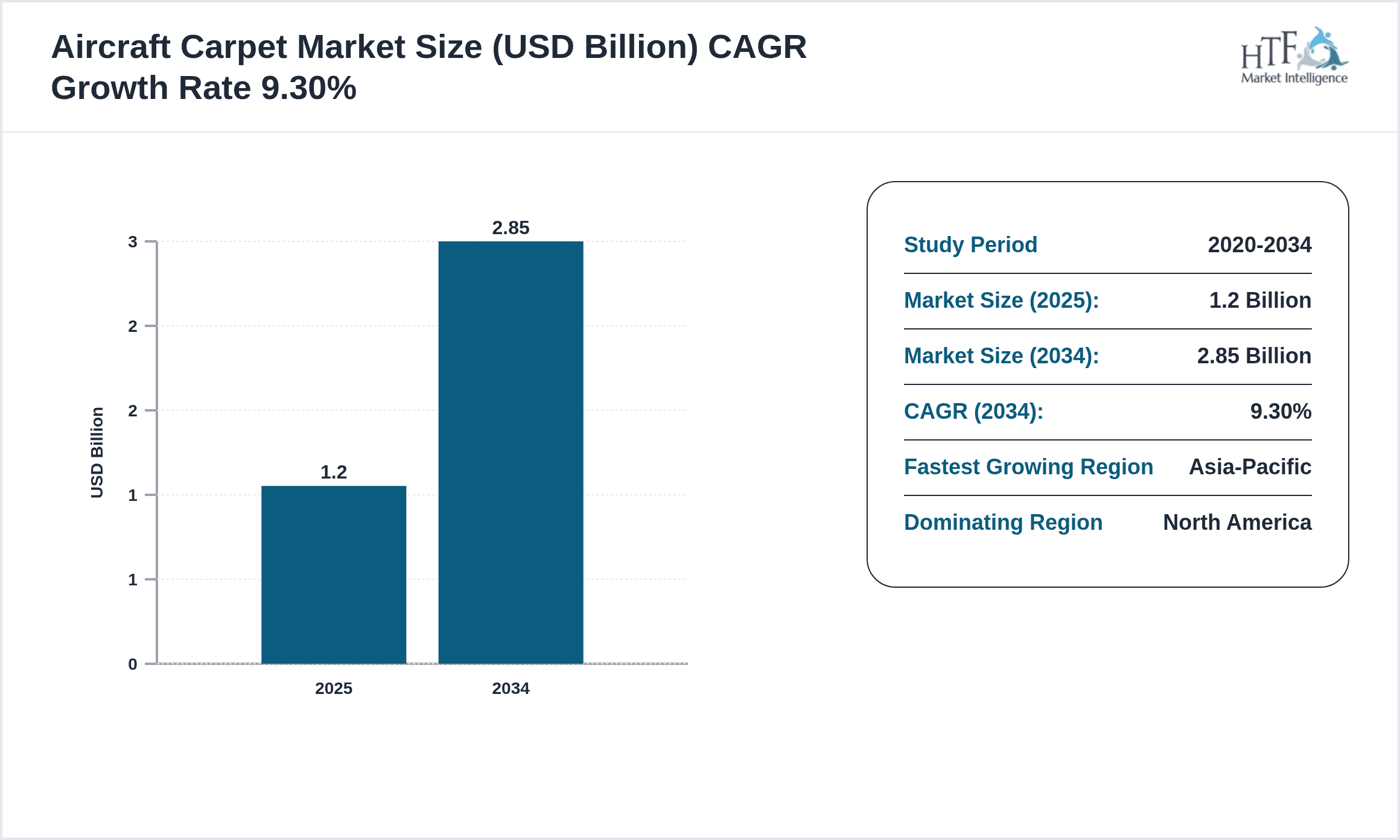

- •Key market highlights include a base market size estimated at USD 1.2 Billion in 2024, projected to reach USD 2.85 Billion by 2034, reflecting a robust CAGR of approximately 9.3%. The market is dominated by the Nylon carpet segment due to its superior durability and fire-resistant properties. Applications in commercial aircraft hold the largest share, driven by the high volume of passenger flights globally. Geographically, North America leads the market in terms of revenue and adoption, while the Asia-Pacific region is identified as the fastest-growing market due to rising aircraft manufacturing and increasing airline fleets. The market demonstrates significant opportunities in sustainable material adoption and aftermarket refurbishment services, contributing to long-term revenue streams.

- •The aircraft carpet market offers strategic value to aircraft manufacturers, airline operators, and interior suppliers by enhancing cabin environment quality and operational safety. For OEMs and aftermarket service providers, high-performance carpets represent a critical product category that impacts overall aircraft lifecycle cost and passenger experience. Moreover, the market's alignment with sustainability trends and lightweight material innovation supports broader aviation industry goals of reducing environmental footprint and improving fuel efficiency. Stakeholders benefit from diverse application segments spanning commercial to military aviation, ensuring resilience against sector-specific economic cycles. Innovations in carpet design and manufacturing processes continue to drive differentiation and competitive advantage in this specialized market.

Competitive Landscape

The Global Aircraft Carpet Market exhibits a moderately concentrated competitive environment characterized by a blend of established multinational textile manufacturers and specialized aviation interior suppliers. Market participants compete primarily through product innovation focusing on durability, fire resistance, lightweight materials, and eco-friendly solutions. Strategic partnerships with aircraft OEMs and aftermarket refurbishment companies enhance market positioning. Companies leverage advanced manufacturing technologies such as tufting and weaving with high-performance fibers to meet stringent aviation standards. Pricing strategies are influenced by raw material costs and compliance requirements, with premium segments commanding higher margins. Barriers to entry include certification complexities and the need for adherence to rigorous aviation safety regulations. Regional competition is pronounced, with North American and European players leading in technological advancements, while Asia-Pacific firms capitalize on cost efficiencies and growing regional aircraft production. Future trends indicate increased consolidation through mergers, acquisitions, and joint ventures aimed at expanding global footprint and technology portfolios.

Leading Companies in Aircraft Carpet Market

- •Milliken & Company (United States)

- •Interface, Inc. (United States)

- •Jiangsu Sainty Carpets Co., Ltd. (China)

- •Shaw Industries Group, Inc. (United States)

- •Mannington Mills, Inc. (United States)

- •Mohawk Industries, Inc. (United States)

- •Tarkett Group (France)

- •Beaulieu International Group (Belgium)

- •Bentley Fabrics (United Kingdom)

- •JAB Anstoetz Group (Germany)

- •Tandus Centiva (United States)

- •Avery Dennison Corporation (United States)

- •Kvadrat AS (Denmark)

- •Milliken Carpets (United States)

- •Balta Group (Belgium)

- •Ege Carpets (Denmark)

- •Desso BV (Netherlands)

- •Sahib Carpet and Flooring (India)

- •Autex Industries Limited (New Zealand)

- •Wilton Carpets (United Kingdom)

- •Fabrica de Carpets (Turkey)

- •Oriental Weavers (Egypt)

- •Lloyd’s of London Carpets (United Kingdom)

- •Shaw Contract Group (United States)

- •Milliken Aerospace (United States)

Market Breakdown

- •By Carpet Type

- ◦Nylon Aircraft Carpets

- ◦Polyester Aircraft Carpets

- ◦Wool Aircraft Carpets

- ◦Acrylic Aircraft Carpets

- ◦Olefin Aircraft Carpets

- •By Aircraft Application

- ◦Commercial Aircraft

- ◦Military Aircraft

- ◦Private Jets

- ◦Helicopters

- ◦Cargo Aircraft

- •By Installation Type

- ◦Original Equipment Manufacturer (OEM) Installation

- ◦Aftermarket Installation

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors/Dealers

- ◦Online Platforms

Growth Dynamics

- •The growing demand for aircraft refurbishment and interior upgrades in commercial airlines is fueling the aircraft carpet market expansion globally. As airlines focus on passenger comfort and cabin aesthetics, investments in high-quality carpet materials have increased significantly.

- •Rising aircraft production, especially in the Asia-Pacific region driven by domestic manufacturers, is propelling demand for OEM carpet installations. This growth is supported by increasing air travel and fleet modernization programs.

- •Technological advancements in carpet materials, including lightweight and fire-resistant fibers, are enhancing product appeal among aircraft manufacturers, helping meet stringent safety regulations and reduce aircraft weight for fuel efficiency.

- •Increasing focus on sustainability and the introduction of eco-friendly carpet options made from recycled or bio-based fibers are attracting interest from green-conscious airlines and operators, providing a new growth avenue.

- •Expansion of aftermarket services and refurbishment programs globally is creating opportunities for replacement carpet sales, especially in mature fleets and regions with high aircraft utilization rates.

Market Trends

- •A dominant trend is the integration of antimicrobial and stain-resistant treatments in aircraft carpets to enhance hygiene and durability, particularly accelerated by the COVID-19 pandemic’s hygiene focus.

- •Customization and design personalization driven by airline branding strategies have increased, with carpets now serving as a key element of cabin design differentiation.

- •The adoption of modular carpet tiles instead of traditional broadloom carpets is gaining traction for easier maintenance and replacement, reducing downtime during aircraft servicing.

- •Digital printing technologies are enabling more intricate and vibrant carpet patterns, allowing airlines to differentiate interior aesthetics and improve passenger experience.

- •Collaborations between carpet manufacturers and textile innovators are fostering development of high-performance, lightweight materials that meet evolving aviation safety standards.

Market Opportunities

- •The rising trend of aircraft cabin modernization in emerging markets presents a significant opportunity for suppliers to introduce advanced carpet solutions tailored for regional airlines expanding their fleets.

- •Growing demand for sustainable and recyclable carpet materials offers manufacturers the chance to innovate and capture environmentally conscious market segments in both OEM and aftermarket spaces.

- •Expanding the aftermarket refurbishment services globally, especially in Asia-Pacific and Latin America, can unlock substantial revenue streams as fleets age and require carpet replacements.

- •Technological integration, such as embedding RFID or sensors into carpets for maintenance tracking, provides an innovative avenue for product differentiation and enhanced service offerings.

- •Collaborations with aircraft cabin interior designers and OEMs to develop bespoke carpet products can deepen market penetration and foster long-term supply agreements.

Market Challenges

- •High raw material costs and volatility in fiber prices impact production expenses, limiting profit margins for aircraft carpet manufacturers and creating pricing pressures.

- •Strict aviation safety and fire resistance regulations require extensive testing and certification, increasing time-to-market and compliance costs for new carpet products.

- •Competition from low-cost regional manufacturers offering less durable products poses challenges to premium carpet suppliers in price-sensitive markets.

- •Long aircraft refurbishment cycles and airline budget constraints can delay aftermarket carpet replacements, affecting steady demand streams for suppliers.

- •Supply chain disruptions due to geopolitical tensions or pandemics can impact raw material availability and delivery schedules, hampering market growth.

Regulatory Framework

- •Between 2019 and 2024, key regulations such as FAA Advisory Circulars and EASA Certification Specifications have mandated strict fire resistance, smoke toxicity, and flammability standards for aircraft interior materials, including carpets. Manufacturers must comply with FAR 25.853 and equivalent standards, ensuring that carpets resist ignition and limit toxic gas emissions during fire incidents. These regulations have led to increased R&D in flame-retardant fibers and materials.

- •The implementation of environmental regulations focusing on sustainable materials and waste reduction within the European Union has driven adoption of recyclable and low-VOC aircraft carpet materials. Compliance with REACH and RoHS directives influences material selection and manufacturing processes.

- •Regional mandates in North America require robust certification processes overseen by the FAA for any new carpet product introduced to the aircraft market, including rigorous testing for durability and safety under varied flight conditions.

- •The International Air Transport Association (IATA) promotes industry-wide standards for cabin interiors, encouraging use of environmentally friendly and lightweight carpet materials to reduce aircraft fuel consumption and emissions.

- •Government initiatives in Asia-Pacific countries are incentivizing domestic production of aerospace materials, including carpets, under 'Make in India' and 'Made in China 2025' programs, indirectly impacting market dynamics by encouraging local manufacturing capabilities.

Market Intelligence

- •15th January 2025, Milliken & Company launched a new line of lightweight, antimicrobial aircraft carpets designed for commercial airliners. The new product combines advanced nylon fibers treated with silver-ion technology to inhibit microbial growth, enhancing cabin hygiene and passenger safety. Targeting major airline refurbishments in North America and Europe, the launch aims to cater to increasing health-conscious travel trends while meeting strict FAA and EASA fire safety standards. The carpets also offer weight reduction benefits contributing to fuel efficiency. This innovation aligns with Milliken's strategic focus on sustainable and high-performance aviation interior solutions. Source: Milliken Official Press Release

- •10th March 2025, Interface, Inc. introduced a range of fully recyclable polyester aircraft carpets featuring digital printing capabilities for customizable cabin designs. The product targets private jet and business aircraft segments, allowing bespoke aesthetic options while supporting circular economy principles. Interface's carpets meet all major aviation fire resistance certifications and are designed for quick installation and maintenance. This launch supports growing industry demand for environmentally responsible interior materials without compromising on performance or compliance. The initiative reflects Interface’s commitment to innovation in sustainable aviation textiles. Source: Interface Corporate News

- •22nd February 2025, Mohawk Industries announced a strategic partnership with a leading aircraft interior firm to supply OEM-grade wool and nylon carpets for new commercial aircraft models. The collaboration focuses on integrating durable, fire-resistant carpets with enhanced acoustic properties to improve passenger comfort. Mohawk’s extensive manufacturing capabilities and global distribution network enable rapid scale-up to meet growing aircraft production in Asia-Pacific and North America. This partnership strengthens Mohawk's presence in the aerospace market and aligns with expanding global air travel infrastructure. Source: Mohawk Industries Press Release

- •5th April 2025, Shaw Industries Group expanded its aircraft carpet manufacturing facility in Europe to increase production capacity for military and cargo aircraft segments. The expansion includes investment in automated tufting technologies and environmentally friendly dyeing processes to reduce carbon footprint. This move positions Shaw to meet rising demand from defense contractors and cargo operators upgrading fleets globally. The enhanced facility supports compliance with evolving EU environmental regulations and aims to deliver faster lead times. Source: Shaw Industries Quarterly Report

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 2.85 Billion |

| CAGR | 9.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.3% |

| Scope of Report | Market is segmented by Carpet Type (Nylon Aircraft Carpets, Polyester Aircraft Carpets, Wool Aircraft Carpets, Acrylic Aircraft Carpets, Olefin Aircraft Carpets), Aircraft Application (Commercial Aircraft, Military Aircraft, Private Jets, Helicopters, Cargo Aircraft), Installation Type (Original Equipment Manufacturer (OEM) Installation, Aftermarket Installation), Distribution Channel (Direct Sales, Distributors/Dealers, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Milliken & Company (United States), Interface, Inc. (United States), Jiangsu Sainty Carpets Co., Ltd. (China), Shaw Industries Group, Inc. (United States), Mannington Mills, Inc. (United States), Mohawk Industries, Inc. (United States), Tarkett Group (France), Beaulieu International Group (Belgium), Bentley Fabrics (United Kingdom), JAB Anstoetz Group (Germany), Tandus Centiva (United States), Avery Dennison Corporation (United States), Kvadrat AS (Denmark), Milliken Carpets (United States), Balta Group (Belgium), Ege Carpets (Denmark), Desso BV (Netherlands), Sahib Carpet and Flooring (India), Autex Industries Limited (New Zealand), Wilton Carpets (United Kingdom), Fabrica de Carpets (Turkey), Oriental Weavers (Egypt), Lloyd’s of London Carpets (United Kingdom), Shaw Contract Group (United States), Milliken Aerospace (United States) |

Global Aircraft Carpet Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.