Global Built-in Kitchen Appliance Market - Outlook 2025-2034

Global Built-in Kitchen Appliance Market is segmented by Type (Built-in Ovens, Smart Cooktops, Microwave Ovens, Integrated Dishwashers, Built-in Refrigerators), Application (Cooking, Refrigeration, Dishwashing, Ventilation, Food Preparation), Technology (IoT-enabled Appliances, Energy-efficient Models, Touch Control Panels, Voice-activated Systems), Distribution Channel (Retail Stores, Online Platforms, Specialty Dealers), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global built-in kitchen appliance market is defined by the integration of household appliances within kitchen cabinetry, offering a blend of functionality, space optimization, and aesthetic appeal. This market includes a variety of products such as ovens, cooktops, microwaves, dishwashers, and refrigerators, which are engineered with advanced technologies including smart connectivity, energy efficiency, and innovative design features. Serving residential, commercial, and hospitality applications, the market caters to the growing demand for modular kitchens and smart homes. The scope of the market extends to multiple global regions, each influenced by factors such as urbanization, lifestyle changes, and technological advancements. Key use cases range from cooking and refrigeration to dishwashing and ventilation, reflecting the diverse needs of end-users worldwide. The industry is characterized by rapid innovation, increasing consumer preference for integrated solutions, and significant investments in product development to enhance user convenience and sustainability. The built-in kitchen appliance market is thus positioned as a critical segment within the broader home appliance industry, driven by evolving consumer preferences and technological progress.

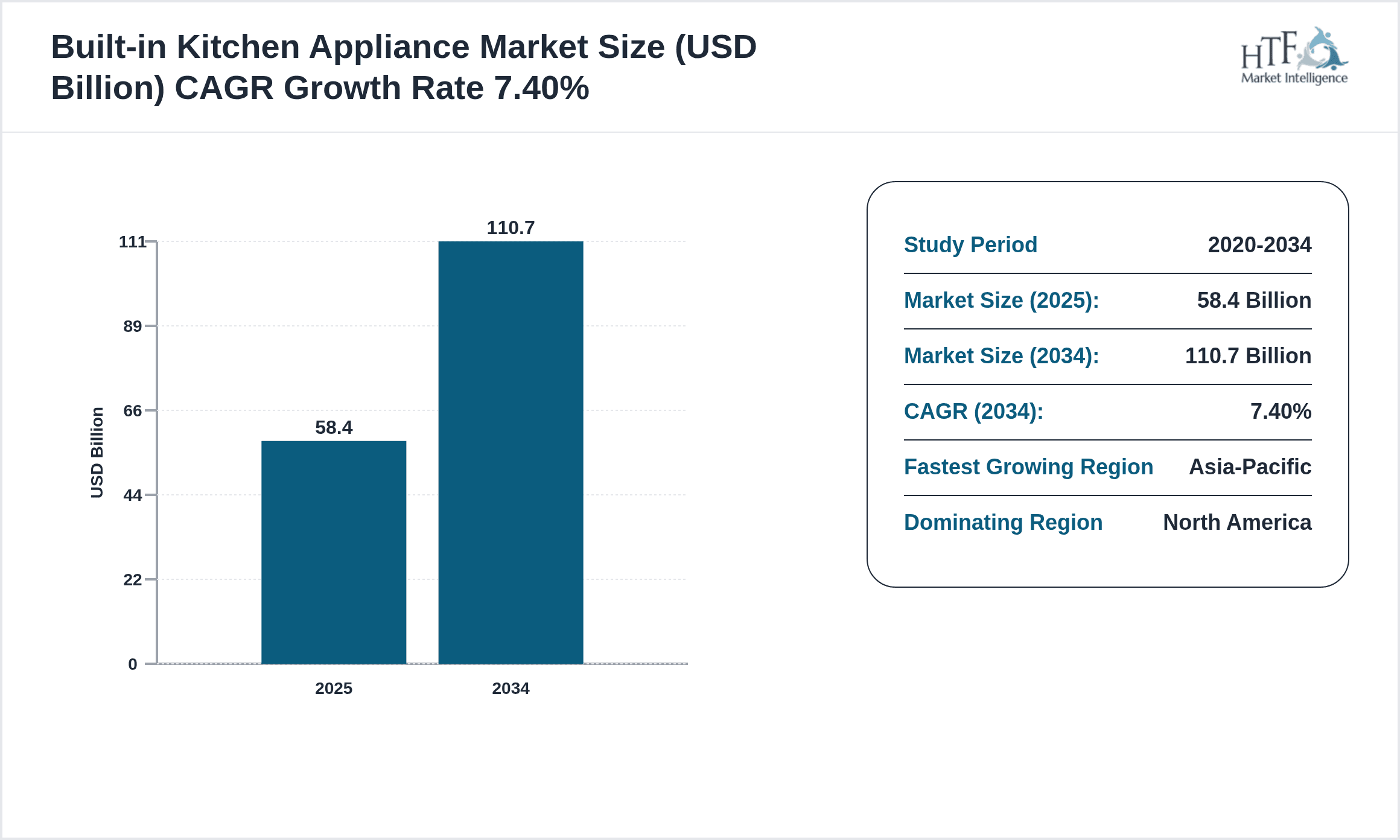

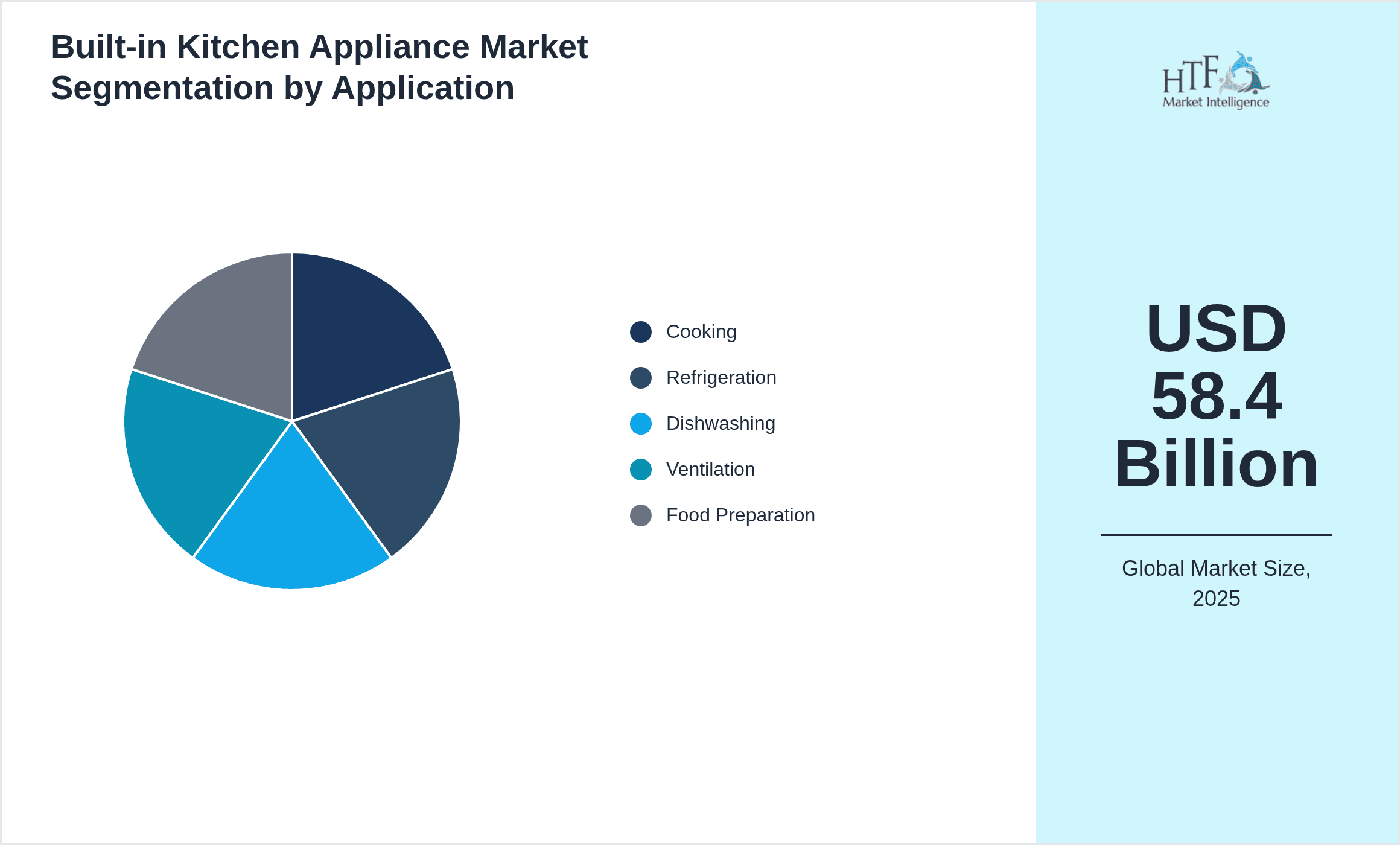

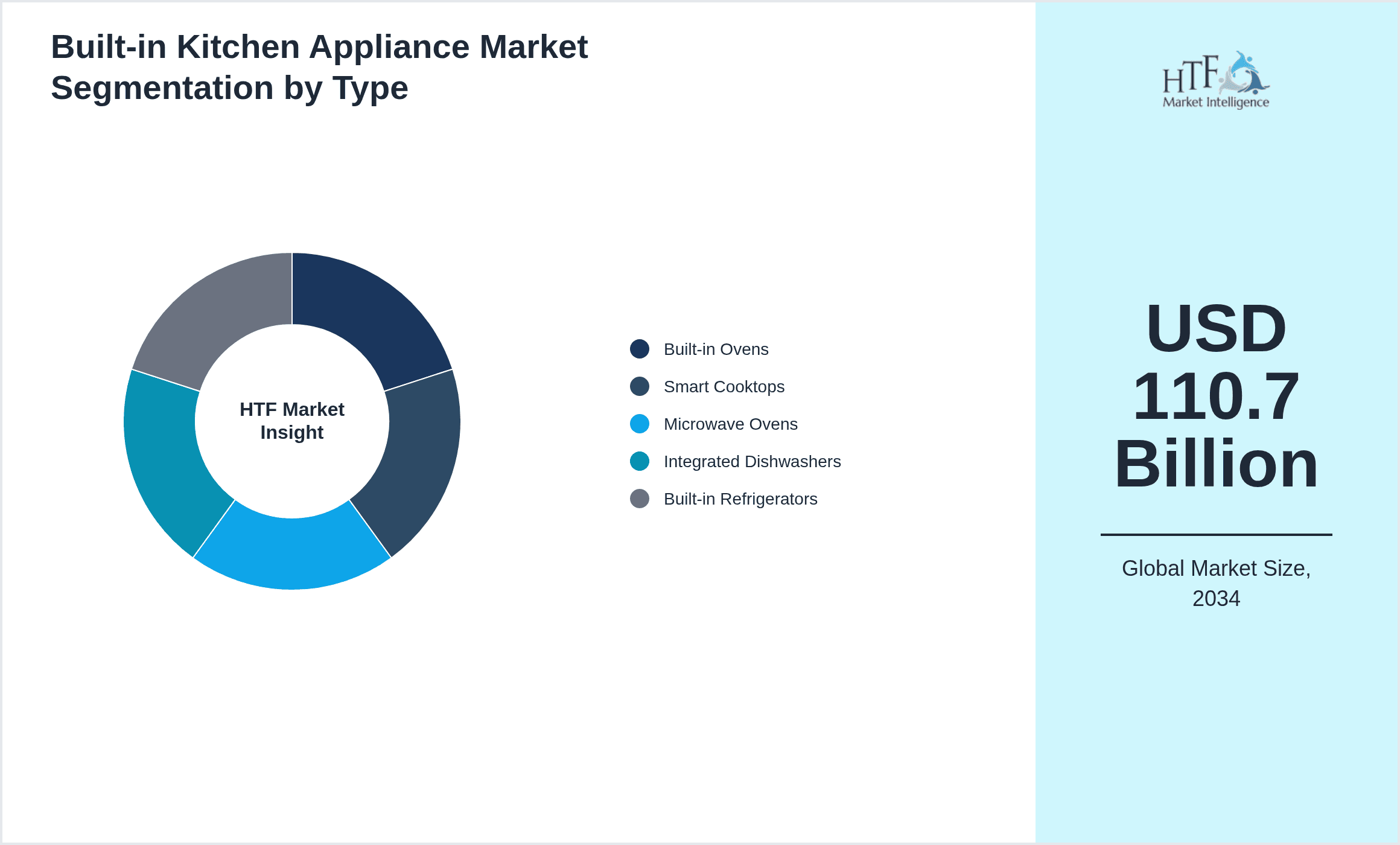

- •The market highlights include a strong growth trajectory with an estimated base market size of USD 58.4 Billion in 2025, projected to reach USD 110.7 Billion by 2034, reflecting a CAGR of 7.4%. North America currently leads in market share due to high adoption of premium appliances and smart technology integration, while Asia-Pacific is the fastest-growing region, driven by rising urbanization and increasing middle-class populations. Ovens hold the dominant product type segment, whereas smart cooktops represent the fastest-growing category, fueled by consumer demand for convenience and advanced features. Application-wise, cooking appliances dominate, followed by refrigeration units, both vital in modern kitchen setups. These trends indicate a robust market environment characterized by innovation, increasing consumer spending, and expanding distribution channels globally.

- •The built-in kitchen appliance market offers significant strategic value to manufacturers, retailers, and technology providers, as it aligns with evolving consumer lifestyles emphasizing smart living and kitchen efficiency. The integration of IoT and smart home technologies enhances product appeal and provides differentiation opportunities. Market stakeholders benefit from expanding urban populations, increasing preferences for modular kitchens, and growing environmental regulations promoting energy-efficient appliances. This market also presents lucrative prospects for new entrants and established players focusing on innovation, quality, and sustainability. The convergence of design aesthetics with functional excellence drives consumer loyalty and repeat purchases, underscoring the importance of continuous product development and strategic marketing in capturing market share across diverse global regions.

Competitive Landscape

The competitive environment in the global built-in kitchen appliance market is marked by intense rivalry among established multinational corporations and emerging regional players. Leading companies focus on innovation-driven strategies, leveraging smart technology integration, energy efficiency, and sleek design to differentiate their offerings. Market positioning relies heavily on brand reputation, product quality, and extensive distribution networks. Strategic collaborations, mergers, and acquisitions are common to consolidate market presence and expand geographical reach. Pricing strategies balance premium positioning with value offerings to cater to diverse consumer segments. The adoption of sustainable manufacturing practices and adherence to evolving regulatory standards further influence competitive dynamics. Companies also invest significantly in R&D to introduce cutting-edge features such as voice control, AI-enabled cooking assistance, and advanced safety mechanisms. Regional competition is shaped by local consumer preferences and economic conditions, with Asia-Pacific witnessing rising local manufacturers challenging global incumbents. Future competitive trends will focus on digital transformation, customization, and enhanced customer engagement to maintain market leadership.

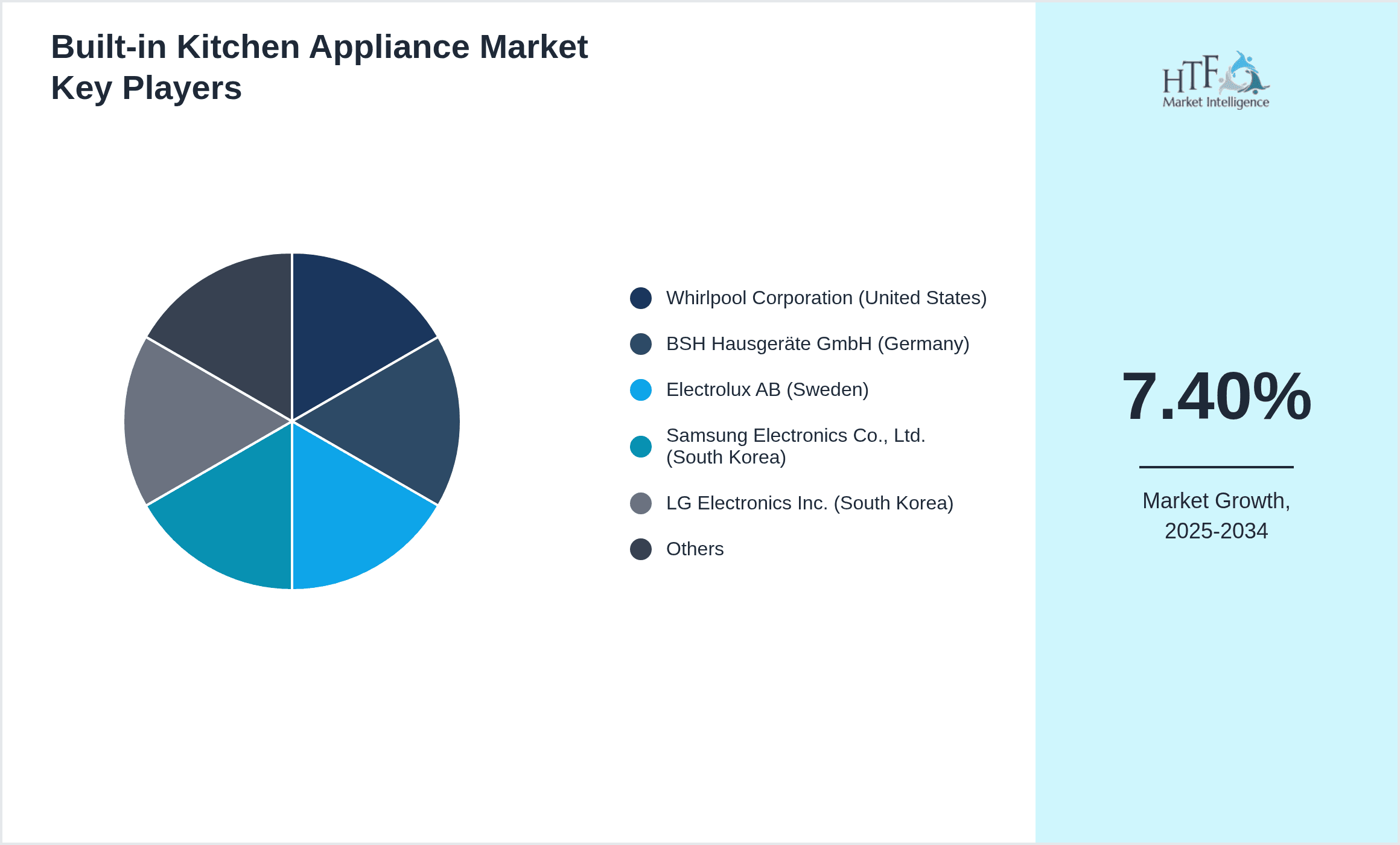

Companies Shaping the Built-in Kitchen Appliance Market

- •Whirlpool Corporation (United States)

- •BSH Hausgeräte GmbH (Germany)

- •Electrolux AB (Sweden)

- •Samsung Electronics Co., Ltd. (South Korea)

- •LG Electronics Inc. (South Korea)

- •Haier Smart Home Co., Ltd. (China)

- •Miele & Cie. KG (Germany)

- •Fisher & Paykel Appliances Holdings Ltd. (New Zealand)

- •Panasonic Corporation (Japan)

- •GE Appliances (United States)

- •Gorenje Group (Slovenia)

- •Arcelik A.S. (Turkey)

- •Fagor Electrodomésticos S. Coop. (Spain)

- •V-ZUG AG (Switzerland)

- •Smeg S.p.A. (Italy)

- •Candy Hoover Group (Italy)

- •Ariston Thermo Group (Italy)

- •Electrolux Professional AB (Sweden)

- •Haier Europe (Netherlands)

- •Bosch Home Appliances (Germany)

- •Fulgor Milano (Italy)

- •Blomberg GmbH (Germany)

- •Thermador (United States)

- •Asko Appliances AB (Sweden)

- •Siemens Home Appliances (Germany)

Market Breakdown

- •By Type

- ◦Built-in Ovens

- ◦Smart Cooktops

- ◦Microwave Ovens

- ◦Integrated Dishwashers

- ◦Built-in Refrigerators

- •By Application

- ◦Cooking

- ◦Refrigeration

- ◦Dishwashing

- ◦Ventilation

- ◦Food Preparation

- •By Technology

- ◦IoT-enabled Appliances

- ◦Energy-efficient Models

- ◦Touch Control Panels

- ◦Voice-activated Systems

- •By Distribution Channel

- ◦Retail Stores

- ◦Online Platforms

- ◦Specialty Dealers

Growth Dynamics

- •The global built-in kitchen appliance market is propelled by increasing urbanization and rising disposable incomes, which drive demand for modern and space-saving kitchen solutions. Consumers are prioritizing smart and energy-efficient appliances that offer convenience and sustainability. Government initiatives promoting energy conservation and green technologies further stimulate market growth. Additionally, growth in the real estate sector, particularly in urban areas, supports the adoption of built-in appliances in new residential and commercial projects. The integration of IoT and AI technologies enhances product functionality, attracting tech-savvy customers and fostering innovation among manufacturers.

- •The proliferation of smart home ecosystems is a key growth factor, with consumers seeking interconnected appliances that provide seamless control and automation. Advancements in voice control, remote monitoring, and adaptive cooking features improve user experience and encourage market expansion. The trend toward modular kitchen designs aligns with increasing demand for built-in appliances, enabling customized and aesthetically pleasing kitchen spaces. Moreover, growing awareness about health and hygiene motivates adoption of appliances with advanced sterilization and air purification functionalities, creating new avenues for product development and market penetration.

- •Rising e-commerce penetration worldwide facilitates greater accessibility and wider distribution of built-in kitchen appliances, enabling manufacturers to reach diverse consumer segments efficiently. The availability of financing options and extended warranties incentivize purchases, especially in emerging markets. Strategic collaborations between appliance manufacturers and home improvement companies further accelerate market growth by bundling products and services. Additionally, the increasing preference for premium and luxury kitchen appliances among affluent consumers drives R&D investments and product differentiation, expanding the market’s value proposition.

- •Regulatory support for energy-efficient appliances and environmental sustainability is fostering innovation in product design and manufacturing processes. Compliance with international energy standards encourages the development of eco-friendly built-in kitchen appliances, attracting environmentally conscious buyers. The incorporation of recycled materials and reduction of hazardous substances in appliance production align with global sustainability goals. These factors contribute to positive brand perception and competitive advantage, enhancing market growth potential across regions.

- •The expanding hospitality and commercial kitchen sectors also contribute to the demand for built-in kitchen appliances, as these facilities seek durable, space-optimized, and technologically advanced equipment. Hotels, restaurants, and institutional kitchens prioritize appliances that improve operational efficiency and meet stringent hygiene standards. This segment provides opportunities for tailored product offerings and customized solutions, further stimulating market development and vendor diversification.

Market Trends

- •Smart kitchen appliances integrated with IoT and AI capabilities are transforming the market by enabling remote control, predictive maintenance, and personalized cooking experiences. This trend is supported by increasing consumer demand for convenience and connectivity, leading to rapid adoption of voice-activated and app-controlled devices. Manufacturers are investing in software and hardware innovation to stay competitive.

- •Sustainability is a defining trend, with energy-efficient appliances gaining prominence due to rising environmental awareness and regulatory mandates. Products featuring low power consumption, recyclable materials, and eco-friendly refrigerants are increasingly favored, influencing purchasing decisions and product development.

- •Minimalist and modular kitchen designs drive demand for built-in appliances that blend seamlessly with cabinetry, offering sleek aesthetics and space optimization. The customization of kitchen layouts to suit individual preferences is encouraging manufacturers to develop versatile and compact appliance models.

- •The rise of multi-functional appliances that combine cooking, steaming, and baking functions caters to consumers seeking space-saving solutions without compromising utility. These hybrid products offer enhanced usability and appeal to smaller households and urban apartments.

- •Collaborations between technology firms and appliance manufacturers foster innovation in user interfaces, incorporating touchscreens, gesture controls, and AI assistants. This convergence of technologies enriches the user experience and sets new standards in kitchen appliance functionality.

- •Emerging markets are witnessing increasing penetration of built-in kitchen appliances due to growing middle-class populations and urban modernization. Market entrants focus on affordable, feature-rich products tailored to local preferences and purchasing power.

- •Enhanced hygiene features, including antimicrobial surfaces and sterilization functions, have gained traction post-pandemic, reflecting consumer priorities on health and cleanliness in kitchen environments.

Market Opportunities

- •Expanding the portfolio of smart and connected appliances presents a lucrative opportunity to capture tech-savvy consumers seeking integrated kitchen ecosystems. Developing user-friendly interfaces and interoperability with other smart home devices can enhance market penetration.

- •Emerging economies offer significant growth potential due to rapid urbanization, increasing disposable incomes, and evolving lifestyles. Targeted marketing and affordable product lines can unlock demand in these regions.

- •Investing in sustainable product development, including energy-efficient and eco-friendly appliances, can differentiate brands and comply with tightening environmental regulations, appealing to environmentally conscious consumers.

- •Collaborations with real estate developers and kitchen designers to bundle built-in appliances with modular kitchens can streamline sales channels and enhance customer acquisition.

- •The hospitality sector’s demand for customized, durable, and high-performance built-in appliances opens avenues for specialized product innovation and B2B partnerships.

- •Leveraging e-commerce growth through improved digital marketing and after-sales service can expand reach and customer engagement globally.

- •Integration of AI-driven cooking assistance and predictive maintenance features offers scope for premium product offerings and subscription-based service models.

Market Challenges

- •High initial costs of built-in kitchen appliances, especially smart and premium models, limit adoption among price-sensitive consumers, particularly in developing regions, posing a barrier to market expansion.

- •Complex installation requirements and the need for compatible kitchen cabinetry deter potential buyers and complicate after-sales service, impacting customer satisfaction and repeat purchases.

- •Rapid technological advancements require continuous R&D investments, increasing operational costs and creating pressure on manufacturers to regularly update product lines to remain competitive.

- •Supply chain disruptions and rising raw material costs affect production timelines and pricing strategies, challenging manufacturers to maintain profitability and market share.

- •Regulatory compliance across diverse global markets necessitates adaptation to varying standards and certifications, complicating product development and market entry strategies.

- •Competition from standalone and portable kitchen appliances offering flexibility and lower costs restricts built-in appliance market growth in certain segments.

- •Consumer reluctance to adopt new technologies due to lack of awareness or perceived complexity may slow penetration of advanced smart kitchen appliances.

Regulatory Framework

- •Between 2020 and 2025, key regulations such as the Energy Star certification and EU’s Ecodesign Directive have mandated minimum energy efficiency standards for built-in kitchen appliances, compelling manufacturers to innovate and reduce power consumption.

- •Safety standards including UL listing in North America and CE marking in Europe have enforced rigorous testing for electrical safety, electromagnetic compatibility, and user protection, ensuring product reliability and consumer confidence.

- •Environmental regulations restricting the use of hazardous substances, such as RoHS and REACH, have impacted material selection and manufacturing processes, promoting greener production practices.

- •Regional mandates on refrigerant usage, such as the phasedown of high-global warming potential (GWP) refrigerants under the Kigali Amendment, have influenced design changes in built-in refrigeration units.

- •Government incentives and rebate programs in regions like North America and Europe encourage the adoption of energy-efficient appliances, supporting market growth through financial benefits to consumers.

Market Intelligence

- •15th January 2025, Samsung Electronics Co., Ltd. unveiled its latest line of AI-powered built-in ovens equipped with smart sensors that adapt cooking modes based on food type, enhancing precision and convenience for consumers. Targeted at premium kitchen segment, these ovens integrate seamlessly with Samsung's SmartThings ecosystem, enabling remote control and recipe recommendations. The launch aims to capitalize on rising demand for intelligent kitchen solutions and strengthen Samsung’s position in the global appliance market. Source: Samsung Official Press Release

- •3rd March 2025, Whirlpool Corporation announced a strategic partnership with a leading smart home platform to integrate voice-activated controls across its range of built-in kitchen appliances. This initiative focuses on enhancing user experience through interoperability and personalized kitchen management, with plans to expand the collaboration into emerging markets by late 2025. The partnership underscores Whirlpool’s commitment to innovation and digital transformation in the appliance sector. Source: Whirlpool Corporate News

- •20th May 2025, Bosch Home Appliances launched a new series of eco-friendly built-in refrigerators featuring advanced cooling technology that reduces energy consumption by 30%. Designed for environmentally conscious consumers, these appliances comply with the latest EU energy regulations and include smart diagnostics for predictive maintenance. The launch reinforces Bosch’s sustainability agenda and responds to growing market demand for green products. Source: Bosch Press Release

- •10th August 2025, LG Electronics introduced an innovative built-in dishwasher model with enhanced noise reduction technology and customizable wash cycles controlled via mobile applications. The product targets urban households seeking quiet and efficient kitchen appliances compatible with smart home systems. This launch reflects LG’s focus on blending technology with user-centric design to capture market share globally. Source: LG Electronics Newsroom

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 58.4 Billion |

| Forecast Year Market Size | USD 110.7 Billion |

| CAGR | 7.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.2% |

| Scope of Report | Market is segmented by Type (Built-in Ovens, Smart Cooktops, Microwave Ovens, Integrated Dishwashers, Built-in Refrigerators), Application (Cooking, Refrigeration, Dishwashing, Ventilation, Food Preparation), Technology (IoT-enabled Appliances, Energy-efficient Models, Touch Control Panels, Voice-activated Systems), Distribution Channel (Retail Stores, Online Platforms, Specialty Dealers) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Whirlpool Corporation (United States), BSH Hausgeräte GmbH (Germany), Electrolux AB (Sweden), Samsung Electronics Co., Ltd. (South Korea), LG Electronics Inc. (South Korea) |

Global Built-in Kitchen Appliance Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.