Europe Security Orchestration Market - Europe Size & Outlook 2025-2034

Europe Security Orchestration Market is segmented by Security Orchestration Solution Type (Cloud-based Security Orchestration Platforms, On-premise Security Orchestration Systems, Hybrid Security Orchestration Solutions, API Integration Platforms, AI-Driven Security Orchestration Technologies), Application of Security Orchestration (Incident Response Management, Threat Intelligence Integration, Compliance Management, Vulnerability Management, Security Automation), Industry Vertical (Financial Services, Healthcare, Government and Public Sector, Manufacturing, Telecommunications), Deployment Model (Cloud Deployment, On-premise Deployment, Hybrid Deployment), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Security Orchestration Market is a dynamic sector focused on delivering advanced cybersecurity solutions that integrate and automate security operations across enterprises and public sector organizations. This market includes platforms and services designed to unify threat detection, response, and compliance management to create efficient, scalable, and adaptive security environments. It covers multiple deployment types such as cloud-based, on-premise, hybrid models, API integrations, and emerging AI-driven orchestration technologies. The primary applications include incident response, threat intelligence, compliance management, vulnerability management, and security automation. This market's scope extends to various industries including finance, healthcare, government, and manufacturing, addressing the rising complexity of cyber threats and regulatory pressures unique to the European region. The increasing digital transformation initiatives, coupled with the need for rapid threat mitigation, are key factors shaping market demand. Enterprises in Europe are emphasizing the adoption of AI-powered orchestration to enhance operational efficiency and reduce response times. This market is expected to experience substantial growth driven by technological innovation, evolving threat landscapes, and regulatory mandates.

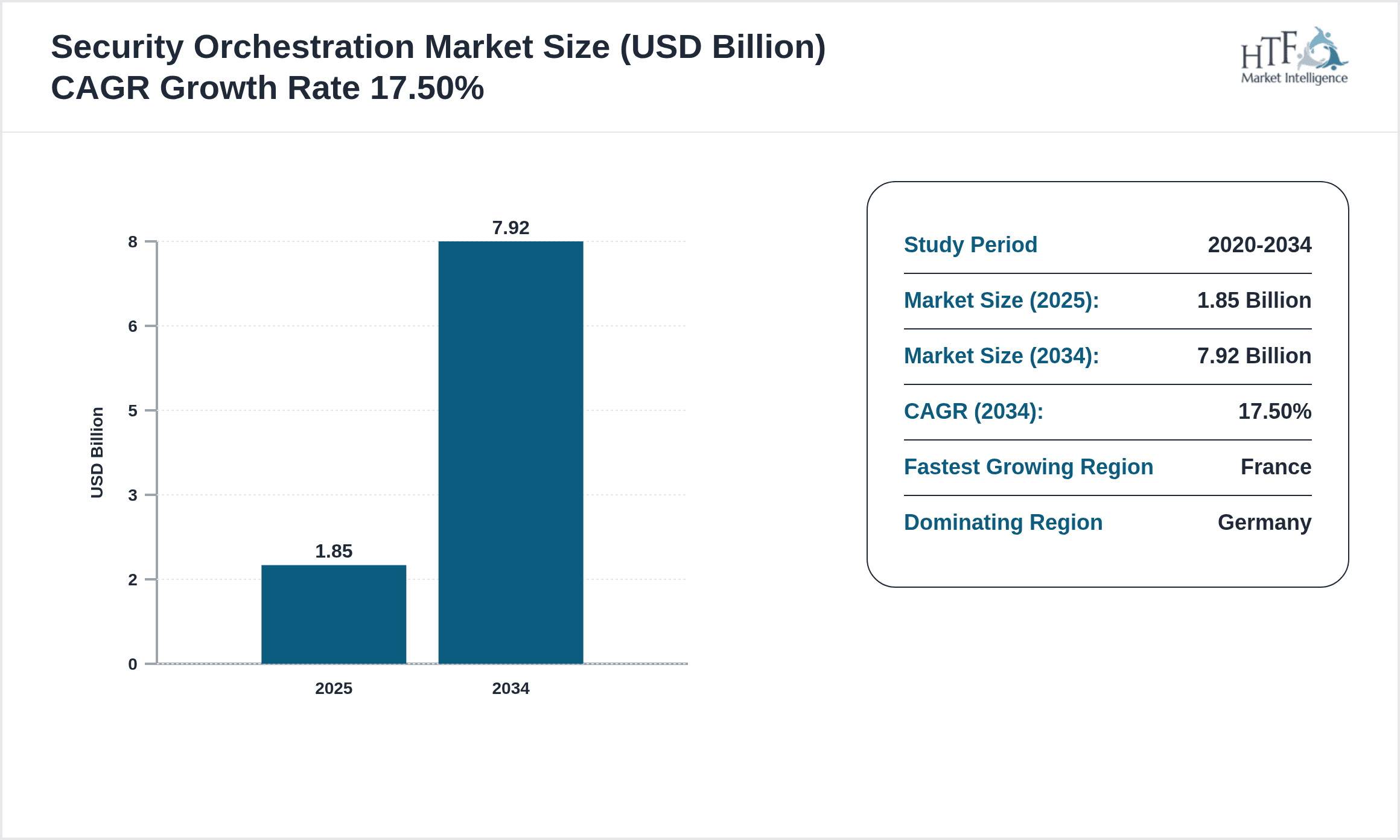

- •Market highlights indicate a robust CAGR of 17.5% between 2025 and 2034, with the market size expanding from USD 1.85 billion in 2025 to USD 7.92 billion by 2034. Cloud-based orchestration solutions dominate, reflecting the widespread adoption of cloud technologies across European enterprises. France emerges as the fastest-growing country, leveraging increased investments in AI-driven security orchestration. Germany leads in market size, attributed to its strong industrial base and stringent cybersecurity regulations. The market growth is supported by rising cybercrime rates, increasing adoption of automation in security operations, and stringent compliance requirements such as GDPR. Key market players focus on innovation, strategic partnerships, and mergers & acquisitions to consolidate their presence in Europe.

- •The security orchestration market offers critical value to enterprises by reducing incident response times, improving threat detection accuracy, and enabling proactive compliance management. Its strategic importance spans across sectors that require robust cybersecurity frameworks to safeguard sensitive data and critical infrastructure. For stakeholders including cybersecurity service providers, IT departments, and regulatory bodies, the market presents opportunities for technological advancements, enhanced security operations efficiency, and alignment with evolving regulatory landscapes. The integration of AI and machine learning further enhances the market’s value proposition by enabling predictive analytics and automated decision-making, thus transforming security management practices in Europe.

Competitive Landscape

The European security orchestration market is characterized by intense competition among global cybersecurity vendors and emerging regional specialists. Market players compete through continuous innovation in automation, AI-driven analytics, and integration capabilities to deliver comprehensive security solutions that meet stringent European regulatory standards. Companies adopt diverse strategies including strategic partnerships, mergers and acquisitions, and robust R&D investments to expand their product portfolios and geographical reach. The rivalry is intensified by the growing demand for cloud-native orchestration platforms and AI-powered threat intelligence integration. Competitive positioning hinges on the ability to provide scalable, interoperable solutions that effectively unify security toolsets and streamline incident response workflows. The market also experiences pressure from new entrants offering specialized niche solutions, prompting incumbents to invest in enhanced features, customer support, and compliance certifications. Price competitiveness, customization options, and advanced analytics capabilities contribute to differentiation. Future competitive trends indicate a shift towards more integrated, AI-enhanced orchestration suites and the expansion of managed security service offerings tailored for the European market.

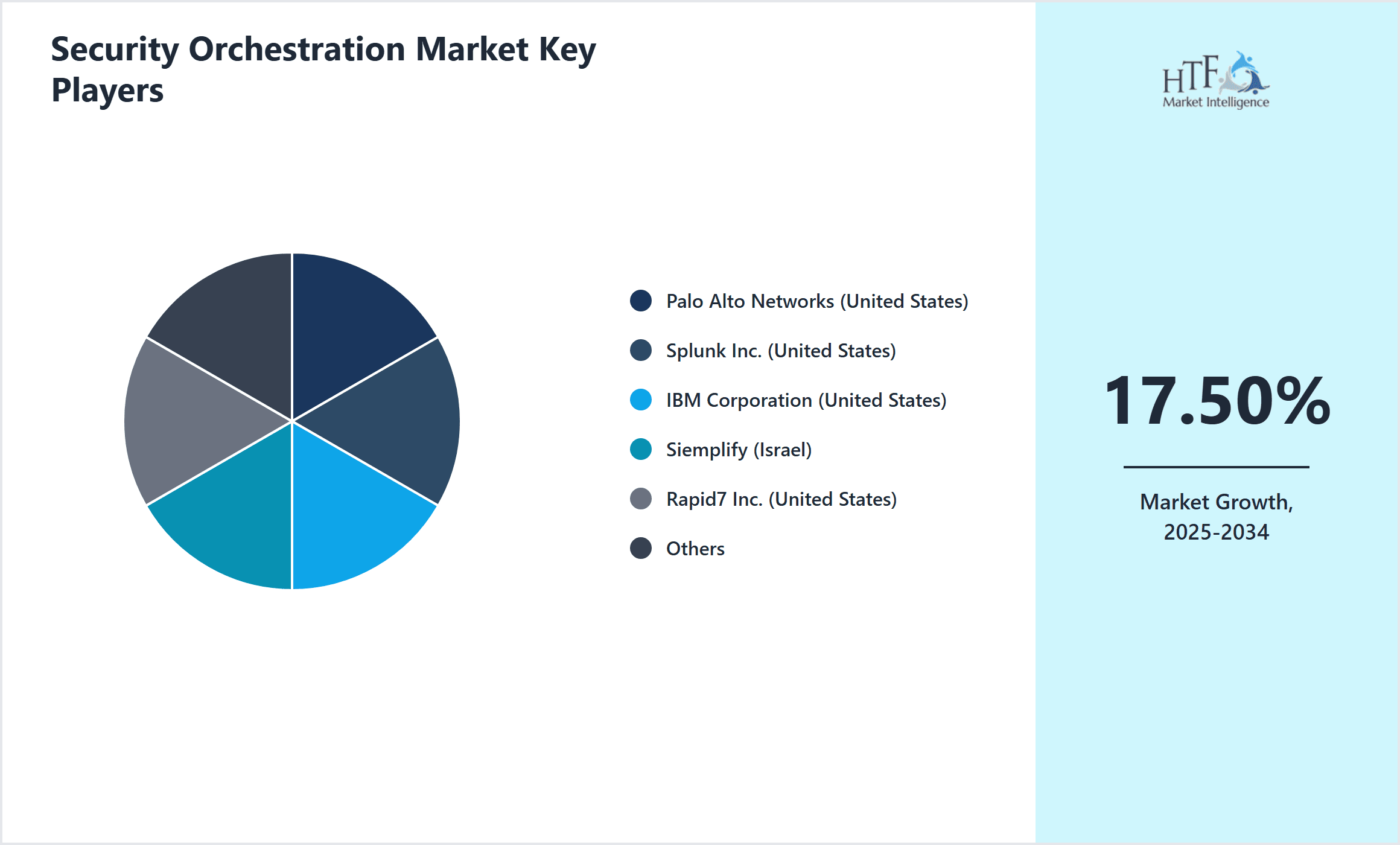

Prominent Players in Europe Security Orchestration Market

- •Palo Alto Networks (United States)

- •Splunk Inc. (United States)

- •IBM Corporation (United States)

- •Siemplify (Israel)

- •Rapid7 Inc. (United States)

- •FireEye Inc. (United States)

- •Swimlane (United States)

- •Cisco Systems, Inc. (United States)

- •McAfee Corp. (United States)

- •Fortinet, Inc. (United States)

- •Micro Focus International (United Kingdom)

- •AT&T Cybersecurity (United States)

- •LogRhythm, Inc. (United States)

- •ServiceNow, Inc. (United States)

- •Cyberbit Ltd. (Israel)

- •Exabeam (United States)

- •DFLabs (United Kingdom)

- •Siemens AG (Germany)

- •Trend Micro Incorporated (Japan)

- •Check Point Software Technologies Ltd. (Israel)

- •Broadcom Inc. (United States)

- •Hewlett Packard Enterprise (United States)

- •Tenable, Inc. (United States)

- •Microsoft Corporation (United States)

- •Darktrace plc (United Kingdom)

Market Breakdown

- •By Security Orchestration Solution Type

- ◦Cloud-based Security Orchestration Platforms

- ◦On-premise Security Orchestration Systems

- ◦Hybrid Security Orchestration Solutions

- ◦API Integration Platforms

- ◦AI-Driven Security Orchestration Technologies

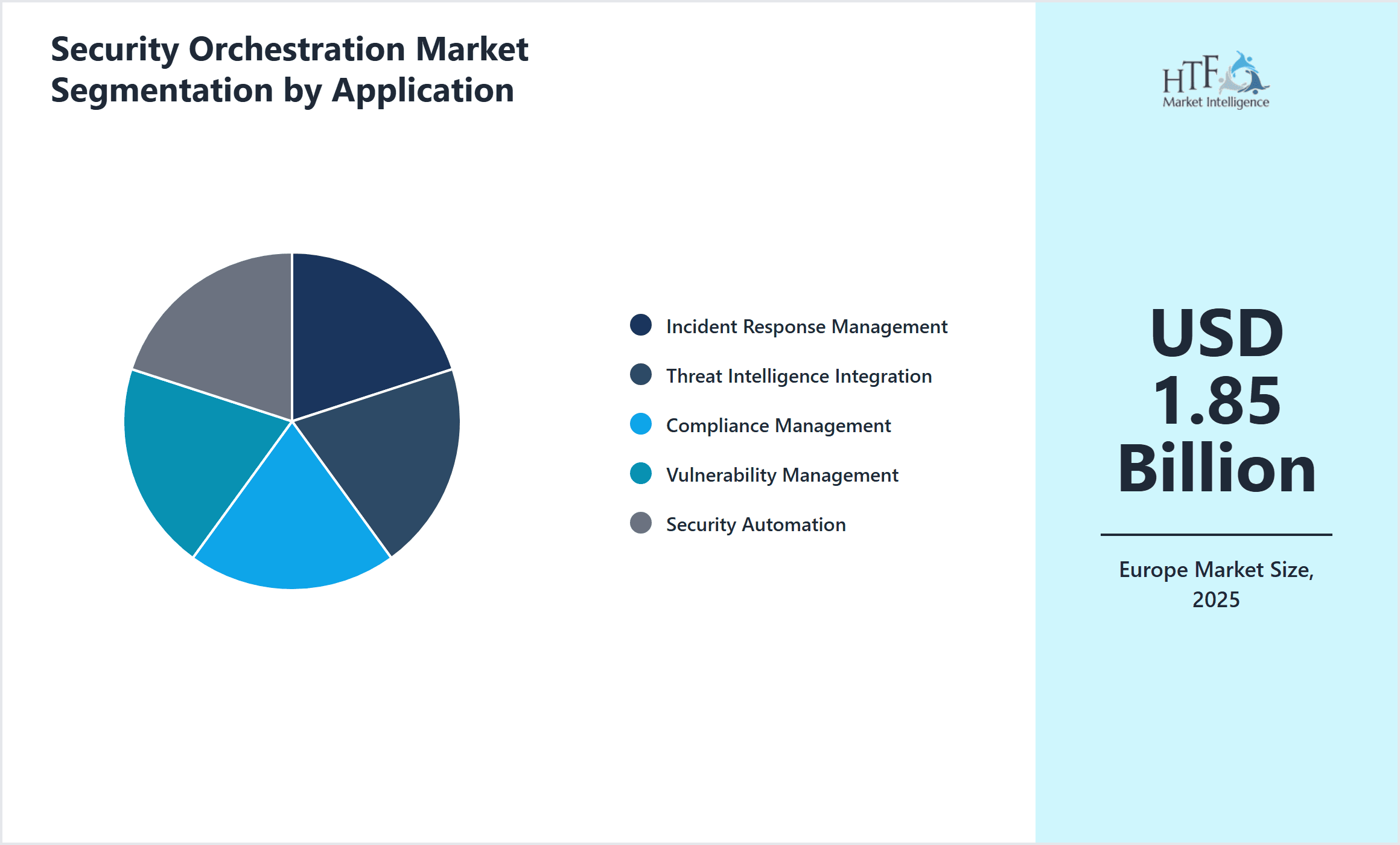

- •By Application of Security Orchestration

- ◦Incident Response Management

- ◦Threat Intelligence Integration

- ◦Compliance Management

- ◦Vulnerability Management

- ◦Security Automation

- •By Industry Vertical

- ◦Financial Services

- ◦Healthcare

- ◦Government and Public Sector

- ◦Manufacturing

- ◦Telecommunications

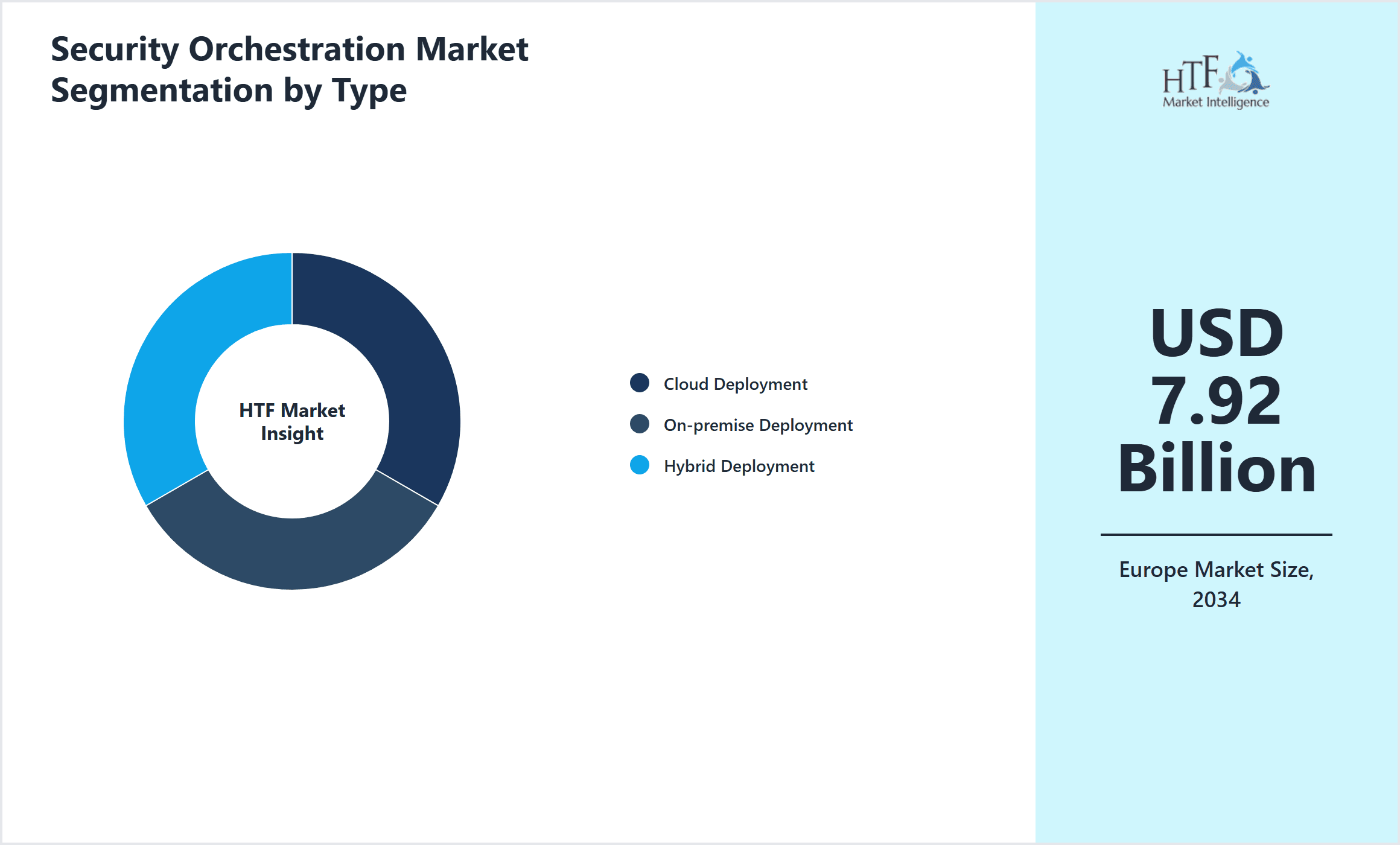

- •By Deployment Model

- ◦Cloud Deployment

- ◦On-premise Deployment

- ◦Hybrid Deployment

Growth Dynamics

- •Europe's Security Orchestration Market is propelled by the increasing sophistication and frequency of cyberattacks targeting critical infrastructure and enterprises. The demand for automated incident response and real-time threat intelligence integration accelerates adoption across industries. Furthermore, stringent regulations such as GDPR and NIS Directive compel organizations to enhance compliance management capabilities via advanced orchestration platforms, fostering market expansion.

- •Technological advancements in artificial intelligence and machine learning significantly drive market growth by enabling predictive threat detection and automated decision-making. These innovations reduce manual intervention and improve operational efficiency, making AI-driven orchestration solutions highly attractive to European enterprises. Additionally, the growing adoption of cloud computing fosters demand for cloud-native orchestration platforms that offer scalability and flexibility.

- •The proliferation of digital transformation initiatives across Europe, including IoT integration and Industry 4.0 adoption, increases the attack surface, necessitating comprehensive security orchestration solutions. Organizations prioritize unified security management to mitigate risks associated with diverse IT environments. This trend underpins investments in hybrid deployment models that combine cloud and on-premise capabilities to meet complex security needs effectively.

- •Increasing collaboration among cybersecurity vendors and service providers enhances the ecosystem’s capability to deliver integrated orchestration solutions. Partnerships facilitate interoperability among heterogeneous security tools, improving threat response times and overall security posture. This collaborative approach supports market growth by enabling end-users to deploy cohesive security frameworks tailored to evolving threat landscapes.

- •Rising awareness about the cost implications of security breaches motivates organizations to invest in orchestration platforms that optimize resource utilization and reduce incident resolution times. Enhanced visibility and automated workflows empower security teams to proactively address vulnerabilities and compliance gaps, contributing to widespread market acceptance and sustained growth momentum in Europe’s cybersecurity sector.

Market Trends

- •A prevailing trend in the Europe Security Orchestration Market is the integration of AI and machine learning to enhance threat detection accuracy and automate complex response sequences. Leading vendors are embedding advanced analytics to provide predictive capabilities and reduce false positives, enabling security teams to focus on high-priority threats effectively.

- •The adoption of cloud-native orchestration solutions is accelerating as organizations shift workloads to cloud environments, seeking scalable and flexible security operations platforms. This shift is supported by the increasing acceptance of hybrid deployment models that balance cloud agility with on-premise control.

- •There is growing emphasis on compliance-oriented orchestration functionalities to address evolving regulatory requirements across European countries. Security orchestration platforms now incorporate automated compliance checks and reporting features to simplify adherence to GDPR, NIS Directive, and sector-specific mandates.

- •Collaborative threat intelligence sharing among enterprises and government agencies is becoming a strategic focus, with orchestration platforms facilitating seamless data exchange and coordinated incident response across organizational boundaries.

- •Vendors are increasingly offering managed security orchestration services, allowing organizations to leverage expert-driven security operations centers (SOCs) without extensive in-house resources, thereby expanding market accessibility.

- •Enhanced API integrations are enabling orchestration platforms to interoperate with a broader array of security products, fostering ecosystem expansion and customization to meet diverse enterprise requirements.

- •Sustainability and energy-efficient security solutions are emerging trends, as data centers and enterprises seek to reduce environmental footprints while maintaining robust cybersecurity postures.

Market Opportunities

- •The rising demand for AI-driven security orchestration solutions presents a significant growth opportunity, as organizations seek to enhance automation and predictive analytics capabilities for proactive threat management. This opens avenues for vendors specializing in AI integrations to capture market share.

- •Expanding cybersecurity needs within the SME segment in Europe offer untapped potential for tailored orchestration platforms that balance cost and functionality, enabling vendors to diversify their customer base and increase penetration.

- •The convergence of security orchestration with emerging technologies such as zero trust architecture and extended detection and response (XDR) creates opportunities for innovative solution development and cross-market expansion.

- •Geographical expansion into underpenetrated European markets like Eastern Europe and the Nordics provides growth potential due to increasing cybersecurity awareness and regulatory enforcement in these regions.

- •Strategic partnerships between orchestration platform providers and cloud service vendors can unlock integrated security offerings, facilitating easier adoption among cloud-first enterprises and accelerating market growth.

- •Investment in user-friendly interfaces and customizable workflows can differentiate products, making security orchestration accessible to non-expert users and broadening market appeal.

- •Government initiatives promoting cybersecurity infrastructure upgrades and funding for digital resilience programs represent promising avenues for market expansion within public sector applications.

Market Challenges

- •The complexity of integrating diverse legacy security tools into unified orchestration platforms poses a significant challenge, requiring substantial customization and technical expertise, which can delay deployments and increase costs.

- •Data privacy concerns and strict European data protection regulations complicate cross-border threat intelligence sharing and automated response actions, limiting the scope of orchestration capabilities.

- •The high initial investment and operational costs associated with deploying advanced security orchestration solutions can be prohibitive for smaller organizations, restricting market penetration in the SME segment.

- •Shortage of skilled cybersecurity professionals in Europe affects the effective management and optimization of orchestration platforms, impacting the realization of their full potential benefits.

- •Rapidly evolving cyber threats require continuous updates to orchestration workflows and threat intelligence feeds, demanding ongoing vendor support and agile platform capabilities, which can strain resources.

- •Interoperability issues among heterogeneous security products from multiple vendors can hinder seamless orchestration, necessitating standardized protocols and extensive integration efforts.

- •Regulatory uncertainties and differences across European countries complicate compliance automation within orchestration platforms, requiring region-specific customization and increasing complexity.

Regulatory Framework

- •Since 2020, the General Data Protection Regulation (GDPR) has mandated stringent data protection and breach notification requirements across Europe, compelling organizations to implement advanced security orchestration for compliance and rapid incident response.

- •The Network and Information Security (NIS) Directive, enforced between 2018 and 2025, establishes cybersecurity standards for essential service operators, influencing the adoption of orchestration platforms to meet regulatory expectations.

- •Recent updates to the EU Cybersecurity Act (2021) introduced certification frameworks for ICT products and services, encouraging vendors to develop compliant security orchestration solutions adhering to these standards.

- •Country-specific mandates such as Germany's IT Security Act 2.0 (effective 2022) require critical infrastructure operators to enhance cybersecurity measures, driving demand for integrated orchestration and automation technologies.

- •The European Union Agency for Cybersecurity (ENISA) guidelines promote best practices for incident management and security automation, shaping market offerings and encouraging harmonized security orchestration adoption across member states.

Market Intelligence

- •15th January 2025, Palo Alto Networks expanded its Cortex XSOAR platform with advanced AI-driven automation capabilities tailored for European enterprises, enabling faster incident response and enhanced threat intelligence integration. The update includes GDPR-compliant data handling features, reflecting regulatory alignment and market demand for privacy-centric security orchestration. This strategic enhancement supports the firm's competitive positioning in Europe, addressing evolving cybersecurity challenges while improving operational efficiency for clients across multiple industries. Source: Official Company Press Release

- •3rd March 2025, Micro Focus International launched a new cloud-native orchestration solution designed to integrate seamlessly with existing European IT infrastructures, focusing on compliance management and vulnerability automation. The product leverages machine learning to prioritize security alerts and automate workflow processes, reducing manual intervention and operational costs. This launch strengthens Micro Focus’s footprint in the European market by addressing critical security orchestration needs in regulated sectors such as finance and healthcare. Source: Industry Publication

- •22nd June 2025, Siemens AG announced a strategic partnership with Darktrace plc to integrate AI-powered threat detection with Siemens’ existing orchestration platforms, enhancing automated response capabilities across critical infrastructure sectors in Europe. This collaboration aims to provide comprehensive cybersecurity solutions that address complex industrial control system vulnerabilities, a growing concern in European markets. The joint initiative is expected to accelerate adoption of advanced orchestration technologies among industrial clients and elevate Siemens’ competitive edge. Source: Official Company Website

- •10th September 2025, IBM Corporation unveiled an enhanced version of its Security SOAR platform, featuring expanded API integrations and real-time compliance automation to meet evolving European regulations. The upgrade includes predictive analytics powered by Watson AI, enabling proactive security operations and improved threat hunting efficiency. This innovation reflects IBM’s commitment to supporting European enterprises in managing sophisticated cyber risks while maintaining regulatory compliance. Source: Industry News Release

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 7.92 Billion |

| CAGR | 17.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 17.5% |

| Scope of Report | Market is segmented by Security Orchestration Solution Type (Cloud-based Security Orchestration Platforms, On-premise Security Orchestration Systems, Hybrid Security Orchestration Solutions, API Integration Platforms, AI-Driven Security Orchestration Technologies), Application of Security Orchestration (Incident Response Management, Threat Intelligence Integration, Compliance Management, Vulnerability Management, Security Automation), Industry Vertical (Financial Services, Healthcare, Government and Public Sector, Manufacturing, Telecommunications), Deployment Model (Cloud Deployment, On-premise Deployment, Hybrid Deployment) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Palo Alto Networks (United States), Splunk Inc. (United States), IBM Corporation (United States), Siemplify (Israel), Rapid7 Inc. (United States), FireEye Inc. (United States), Swimlane (United States), Cisco Systems, Inc. (United States), McAfee Corp. (United States), Fortinet, Inc. (United States), Micro Focus International (United Kingdom), AT&T Cybersecurity (United States), LogRhythm, Inc. (United States), ServiceNow, Inc. (United States), Cyberbit Ltd. (Israel), Exabeam (United States), DFLabs (United Kingdom), Siemens AG (Germany), Trend Micro Incorporated (Japan), Check Point Software Technologies Ltd. (Israel), Broadcom Inc. (United States), Hewlett Packard Enterprise (United States), Tenable, Inc. (United States), Microsoft Corporation (United States), Darktrace plc (United Kingdom) |

Europe Security Orchestration Market - Europe Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.