Global Artificial Intelligence Market - Outlook 2020-2034

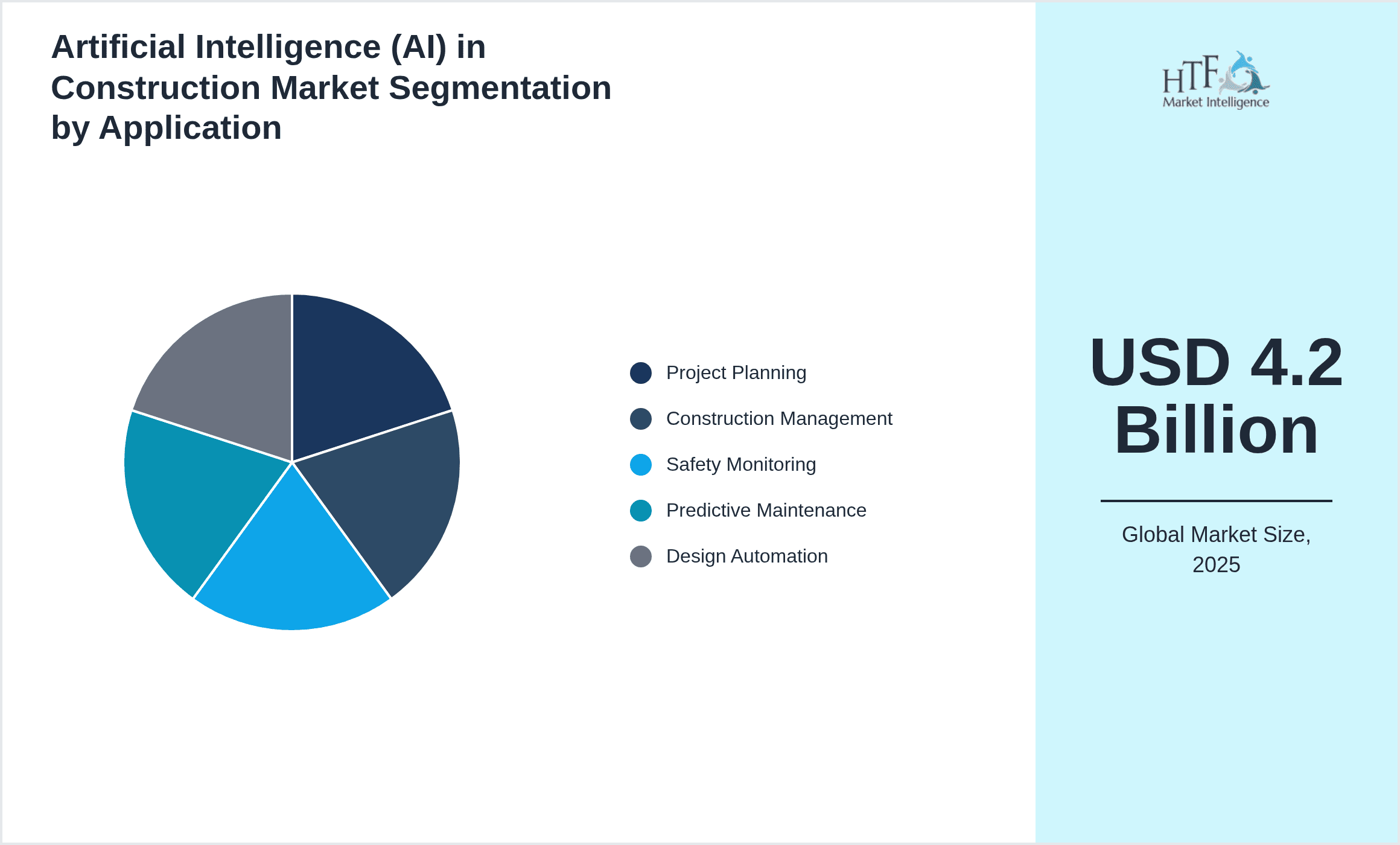

Global Artificial Intelligence (AI) in Construction Market is segmented by Application (Project Planning, Construction Management, Safety Monitoring, Predictive Maintenance, Design Automation), Technology Type (Machine Learning, Computer Vision, Natural Language Processing, Robotics, Expert Systems), Deployment Model (Cloud-based, On-premise, Hybrid), Service Type (Software Solutions, Hardware Devices, AI-enabled Consulting, Maintenance and Support Services), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •Artificial Intelligence (AI) in Construction is transforming the global construction landscape by integrating advanced technologies such as machine learning, computer vision, robotics, natural language processing, and expert systems into diverse construction processes. The market covers AI applications across project planning, design automation, construction management, safety monitoring, and predictive maintenance, enabling enhanced operational efficiency and significant cost savings. End users span construction companies, architectural and engineering firms, infrastructure developers, and facility management organizations, all leveraging AI to mitigate risks, optimize resource utilization, and improve safety compliance. The value chain involves technology providers, system integrators, and service vendors who collaborate closely with end clients to deploy these AI solutions effectively. This market is characterized by rapid innovation, with robotics playing an increasingly pivotal role in automating on-site tasks and AI-powered analytics delivering predictive insights that improve decision-making and project outcomes. Amid rising urbanization and infrastructure demands, AI adoption is accelerating, driven by the need for sustainable, efficient construction practices worldwide, positioning this sector for robust growth through 2034.

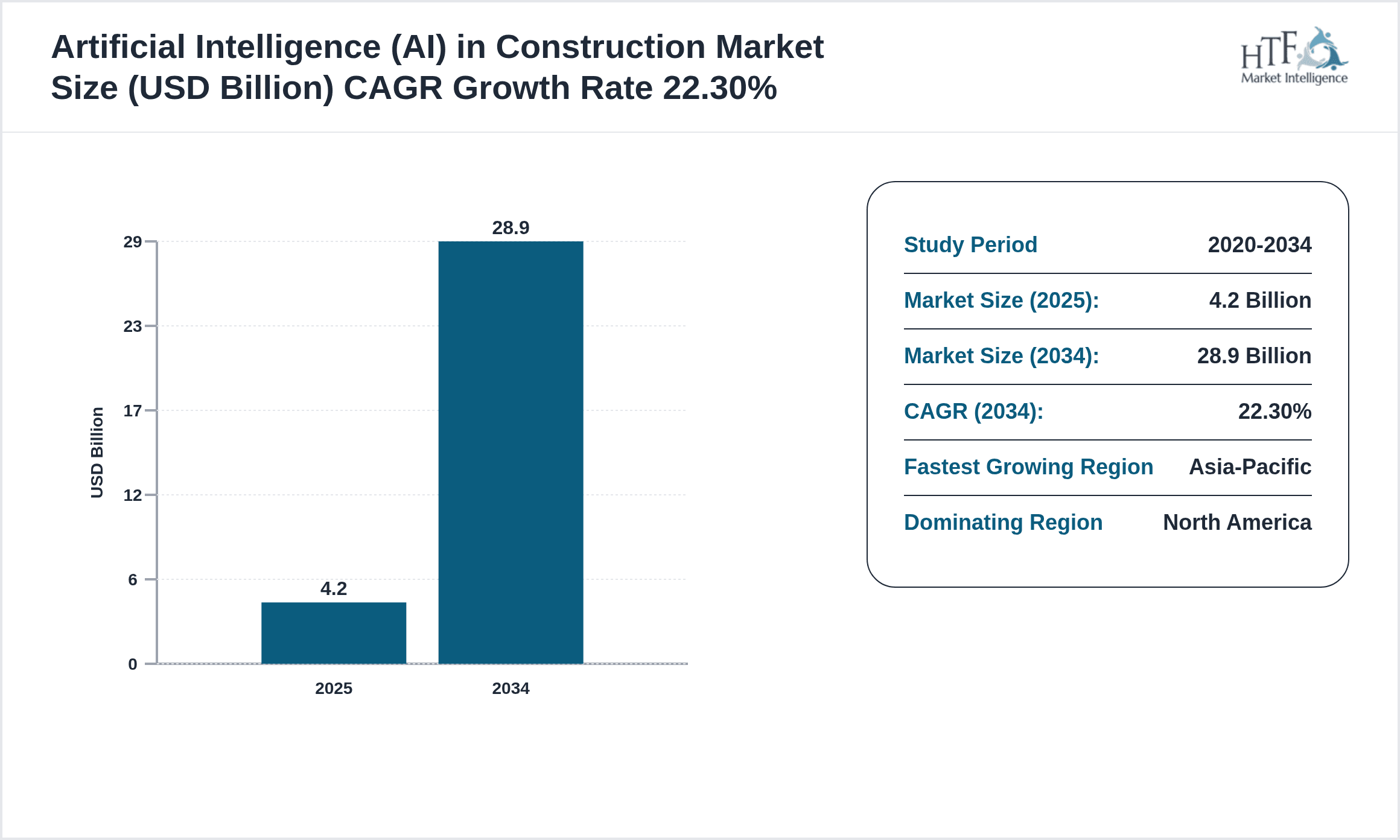

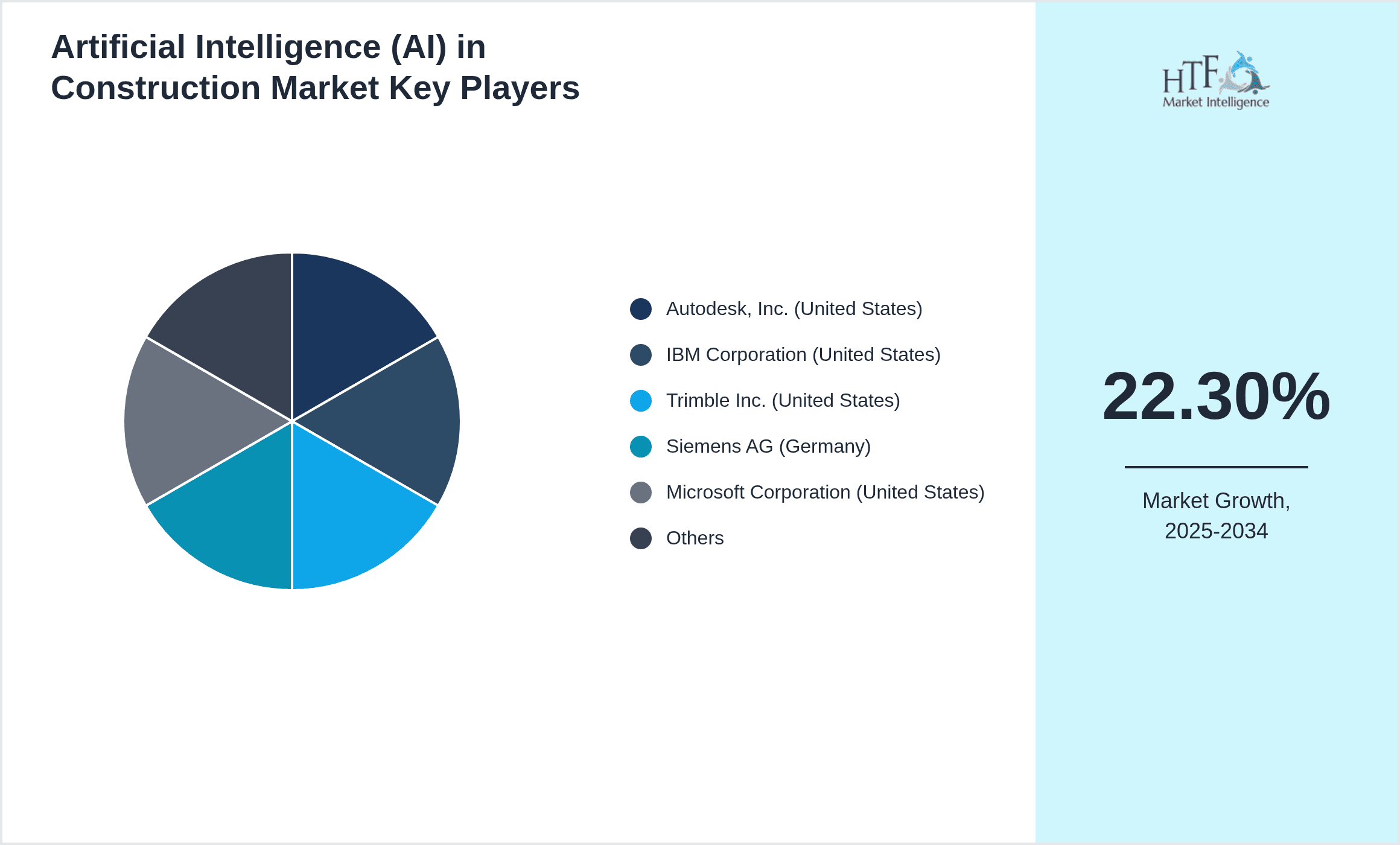

- •The global AI in Construction market was valued at USD 4.2 Billion in 2025 and is projected to reach USD 28.9 Billion by 2034, growing at a CAGR of 22.3%. Key growth drivers include increased digitization efforts, rising safety concerns, and the adoption of automation technologies to reduce labor costs and improve productivity. North America currently dominates the market due to early technology adoption and strong infrastructure investment, while Asia-Pacific is the fastest-growing region fueled by rapid urbanization and government initiatives supporting smart construction technologies. Innovations in robotics and machine learning are propelling new product developments, and regulatory support for AI integration in construction safety and quality assurance further bolsters market expansion.

- •AI in Construction offers significant value propositions to stakeholders by enhancing project accuracy, reducing delays, and minimizing cost overruns. For construction firms, AI-driven solutions enable predictive maintenance and real-time safety monitoring, thereby decreasing accidents and downtime. Technology providers benefit from expanding demand for AI-enabled software and hardware, while end users gain through improved asset management and sustainable construction practices. This strategic importance of AI in Construction spans multiple industries including commercial, residential, and infrastructure development, making it a critical enabler for future-ready construction ecosystems globally.

Competitive Landscape

The global AI in Construction market features a highly competitive landscape characterized by rapid technological advancements and strategic collaborations. Market participants focus on innovation-driven strategies, including the development of proprietary AI algorithms, integration of robotics for automation, and expansion of cloud-based AI platforms to facilitate scalability and real-time data access. Competitive positioning is influenced by product differentiation through enhanced safety features, predictive analytics capabilities, and user-friendly interfaces. Companies engage in mergers and acquisitions to consolidate market presence and acquire new technologies, while partnerships with construction firms and tech startups foster collaborative innovation ecosystems. Pricing strategies vary from subscription-based software models to capital expenditure on hardware and integrated solutions, supporting diverse customer segments. Distribution channels include direct sales, channel partners, and online platforms, ensuring wide market reach. Regional competition reflects varying adoption rates, with North America and Europe displaying mature markets, while Asia-Pacific presents high-growth opportunities driven by infrastructure expansion. Future trends suggest intensified focus on AI ethics, sustainability, and interoperability standards to maintain competitive advantage and address emerging regulatory requirements.

Leading Companies in Artificial Intelligence in Construction Market

- •Autodesk, Inc. (United States)

- •IBM Corporation (United States)

- •Trimble Inc. (United States)

- •Siemens AG (Germany)

- •Microsoft Corporation (United States)

- •Oracle Corporation (United States)

- •Honeywell International Inc. (United States)

- •Boston Dynamics (United States)

- •Bentley Systems, Incorporated (United States)

- •Procore Technologies, Inc. (United States)

- •NVIDIA Corporation (United States)

- •FARO Technologies, Inc. (United States)

- •ABB Ltd (Switzerland)

- •Topcon Corporation (Japan)

- •Hexagon AB (Sweden)

- •Kahua Corporation (United States)

- •Doxel, Inc. (United States)

- •Disperse (United Kingdom)

- •Deltek, Inc. (United States)

- •OpenSpace, Inc. (United States)

- •PlanGrid (United States)

- •ClearEdge3D (United States)

- •Construction Robotics, Inc. (United States)

- •Smartvid.io (United States)

- •Buildots (Israel)

Market Breakdown

- •By Application

- ◦Project Planning

- ◦Construction Management

- ◦Safety Monitoring

- ◦Predictive Maintenance

- ◦Design Automation

- •By Technology Type

- ◦Machine Learning

- ◦Computer Vision

- ◦Natural Language Processing

- ◦Robotics

- ◦Expert Systems

- •By Deployment Model

- ◦Cloud-based

- ◦On-premise

- ◦Hybrid

- •By Service Type

- ◦Software Solutions

- ◦Hardware Devices

- ◦AI-enabled Consulting

- ◦Maintenance and Support Services

Growth Dynamics

- •The increasing adoption of digital transformation initiatives within the construction industry drives significant growth, as companies seek to leverage AI for improved project accuracy and resource optimization. Governments worldwide promote smart infrastructure projects, incentivizing AI integration, which boosts market expansion. For example, machine learning algorithms are used for predictive analytics to forecast project risks, enabling proactive mitigation strategies.

- •Safety concerns on construction sites act as a critical growth driver, with AI-powered computer vision systems and wearable devices being deployed to monitor compliance and prevent accidents, thereby reducing liability and enhancing worker protection.

- •Advancements in robotics technology enable automation of repetitive and hazardous tasks, such as bricklaying and welding, increasing efficiency and reducing labor shortages. Companies like Boston Dynamics have introduced AI-driven robots that operate autonomously in construction environments.

- •Increased availability of big data collected from IoT sensors and drones facilitates AI algorithms to generate actionable insights, optimizing maintenance schedules and reducing downtime through predictive maintenance solutions.

- •Collaborations between AI technology providers and construction firms foster innovation, with investments directed towards developing customizable AI platforms that cater to diverse project scales and complexities, further fueling market growth.

- •The rising trend of sustainable construction practices aligns with AI applications that optimize material usage and energy consumption, contributing to environmental compliance and cost savings.

- •Expansion in emerging economies with growing urban infrastructure needs drives demand for AI-enabled construction technologies to accelerate project delivery and quality assurance.

Market Trends

- •Integration of AI with Building Information Modeling (BIM) is becoming a standard practice, enabling real-time data analytics and enhanced collaboration among stakeholders, improving project outcomes and reducing errors.

- •The emergence of AI-powered drones for site inspection and progress monitoring is revolutionizing data collection, offering high precision and reducing manual labor costs significantly.

- •Increased adoption of natural language processing (NLP) tools facilitates effective communication and documentation management within construction projects, streamlining workflows and improving accuracy.

- •The rise of cloud-based AI platforms allows scalable deployment of AI solutions, enabling small and medium enterprises to access advanced analytics without heavy upfront investments.

- •Collaborative robots (cobots) are gaining traction on construction sites, working alongside human operators to enhance productivity and safety, exemplified by recent deployments in Asia-Pacific regions.

- •Sustainability-driven AI applications are increasingly used to optimize energy consumption and waste management, aligning construction projects with green building certifications.

- •The incorporation of AI in risk management tools offers predictive insights to minimize project delays and budget overruns, influencing contract negotiations and stakeholder decisions.

Market Opportunities

- •Expanding AI adoption in emerging markets presents untapped growth potential, particularly in Asia-Pacific and Latin America, where infrastructure development is rapidly increasing, creating demand for intelligent construction solutions.

- •Development of AI-driven sustainability tools to monitor and manage carbon footprints offers significant opportunity as environmental regulations tighten globally, encouraging green construction practices.

- •Integration of AI with IoT and 5G technologies enables real-time data processing and remote monitoring, opening new avenues for innovation and service delivery models in construction management.

- •Strategic partnerships between AI vendors and construction firms can facilitate customized solutions tailored to specific project needs, enhancing market penetration and client retention.

- •Investment in AI-powered robotics for automation of complex tasks such as concrete pouring and site surveying presents lucrative opportunities to address labor shortages and improve safety.

- •Development of AI-enabled predictive maintenance services can reduce operational costs and extend equipment lifespan, appealing to facility managers and contractors alike.

- •The growing trend towards modular and prefabricated construction methods offers opportunities for AI applications in design optimization and quality control, accelerating project timelines.

Market Challenges

- •High initial investment costs for AI technology implementation act as a barrier, especially for small and medium construction enterprises with limited capital budgets.

- •Lack of skilled workforce proficient in AI and digital tools hampers adoption, necessitating significant training and change management efforts within construction companies.

- •Data privacy and security concerns related to cloud-based AI platforms and IoT devices pose challenges in regulatory compliance and stakeholder trust.

- •Integration complexities arise from heterogeneous construction processes and legacy systems, requiring customized AI solutions and prolonging deployment timelines.

- •Resistance to change and cultural barriers within traditional construction organizations slow the acceptance of AI-driven workflows and automation.

- •Regulatory uncertainties and fragmented standards across regions complicate AI technology approvals and market entry strategies.

- •Concerns about job displacement due to automation create workforce apprehension, affecting adoption rates and necessitating balanced implementation approaches.

Regulatory Framework

- •Between 2020 and 2025, governments across North America and Europe introduced regulations mandating enhanced safety monitoring systems on construction sites, encouraging the deployment of AI-powered computer vision and wearable technologies to comply with occupational health standards.

- •The European Union implemented the Digital Construction Directive in 2023, requiring digital documentation and AI integration in public infrastructure projects, promoting transparency and accountability within the construction supply chain.

- •Regulatory frameworks addressing data privacy and cybersecurity, such as the General Data Protection Regulation (GDPR) in Europe and the California Consumer Privacy Act (CCPA) in the U.S., impact AI solution providers by enforcing strict compliance for cloud-based services handling construction data.

- •In Asia-Pacific, countries like Japan and South Korea enacted guidelines between 2021 and 2024 supporting the use of robotics and AI in construction, including safety certifications and standards for autonomous machinery operation.

- •Government incentives and grants promoting smart city and infrastructure projects have fostered regulatory environments conducive to AI adoption, with policies encouraging innovation through funding and pilot programs across major global regions.

Market Intelligence

- •15th January 2024, Autodesk, Inc. launched an AI-enhanced construction project management platform featuring advanced machine learning algorithms that optimize scheduling and resource allocation. The platform integrates real-time data analytics and predictive insights, targeting large infrastructure developers seeking to reduce project delays and costs. Autodesk's strategic objective is to expand its footprint in the smart construction market by offering scalable solutions that enhance collaboration among stakeholders globally. This launch reflects growing demand for AI-driven tools that can handle complex construction workflows and deliver measurable efficiency gains. Source: Autodesk Official Press Release

- •20th March 2024, IBM Corporation introduced an AI-powered safety monitoring system using computer vision and IoT sensors to detect hazards on construction sites in real-time. The system employs deep learning to analyze video feeds and trigger alerts, aiming to reduce accidents and improve compliance with occupational safety regulations. IBM positions this innovation to address the rising global emphasis on worker safety and regulatory adherence, particularly in North America and Europe. The technology also supports integration with existing construction management software, enhancing ease of adoption. Source: IBM Newsroom

- •10th May 2024, Boston Dynamics announced a strategic partnership with leading construction firms to deploy AI-driven autonomous robots for material handling and site inspection. The collaboration focuses on enhancing productivity and safety by automating hazardous and repetitive tasks, promoting adoption in Asia-Pacific markets experiencing rapid infrastructure growth. The initiative includes pilot programs leveraging advanced robotics and AI for precision and reliability in construction operations. This partnership demonstrates a shift towards integrated AI-robotics solutions addressing labor shortages and operational efficiency. Source: Boston Dynamics Corporate Website

- •5th July 2024, Procore Technologies, Inc. completed the acquisition of a niche AI startup specializing in natural language processing for construction documentation automation. The acquisition aims to enhance Procore’s platform capabilities by enabling automated contract analysis, compliance tracking, and improved communication workflows. This strategic move strengthens Procore’s position in the competitive AI in Construction market and supports its vision of delivering end-to-end digital construction solutions with embedded AI intelligence. The acquisition is expected to accelerate innovation and customer value creation in the coming years. Source: Procore Investor Relations

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.2 Billion |

| Forecast Year Market Size | USD 28.9 Billion |

| CAGR | 22.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 22.4% |

| Scope of Report | Market is segmented by Application (Project Planning, Construction Management, Safety Monitoring, Predictive Maintenance, Design Automation), Technology Type (Machine Learning, Computer Vision, Natural Language Processing, Robotics, Expert Systems), Deployment Model (Cloud-based, On-premise, Hybrid), Service Type (Software Solutions, Hardware Devices, AI-enabled Consulting, Maintenance and Support Services) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Autodesk, Inc. (United States), IBM Corporation (United States), Trimble Inc. (United States), Siemens AG (Germany), Microsoft Corporation (United States), Oracle Corporation (United States), Honeywell International Inc. (United States), Boston Dynamics (United States), Bentley Systems, Incorporated (United States), Procore Technologies, Inc. (United States), NVIDIA Corporation (United States), FARO Technologies, Inc. (United States), ABB Ltd (Switzerland), Topcon Corporation (Japan), Hexagon AB (Sweden), Kahua Corporation (United States), Doxel, Inc. (United States), Disperse (United Kingdom), Deltek, Inc. (United States), OpenSpace, Inc. (United States), PlanGrid (United States), ClearEdge3D (United States), Construction Robotics, Inc. (United States), Smartvid.io (United States), Buildots (Israel) |

Global Artificial Intelligence Market - Outlook 2020-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.