Global Diet Water Market Size, Growth & Revenue 2024-2034

Global Diet Water Market is segmented by Type (Flavored Diet Water, Vitamin-Enhanced Diet Water, Electrolyte-Infused Diet Water, Carbonated Diet Water, Others), Application (Weight Management, Fitness & Sports, Medical Nutrition, Wellness & Lifestyle, Others), Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Specialty Stores), Packaging Material (Plastic Bottles, Glass Bottles, Cartons, Others), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global diet water market is defined by the production and consumption of specialized bottled water products enhanced with flavors, vitamins, electrolytes, and carbonation aimed at promoting health and wellness. These products serve consumers focused on weight management, fitness, medical nutrition, and lifestyle wellness. The market boundary includes diverse product types, a range of applications, and a broad geographical footprint spanning North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Key market characteristics include innovation in formulation, rising consumer health awareness, and integration with lifestyle trends. The primary use cases involve hydration with added dietary benefits, catering to segments such as athletes requiring electrolyte replenishment, individuals seeking low-calorie flavored water alternatives, and patients needing medically tailored hydration solutions. The market's growth is propelled by increasing urbanization, rising disposable incomes, and expanding retail channels including e-commerce platforms globally.

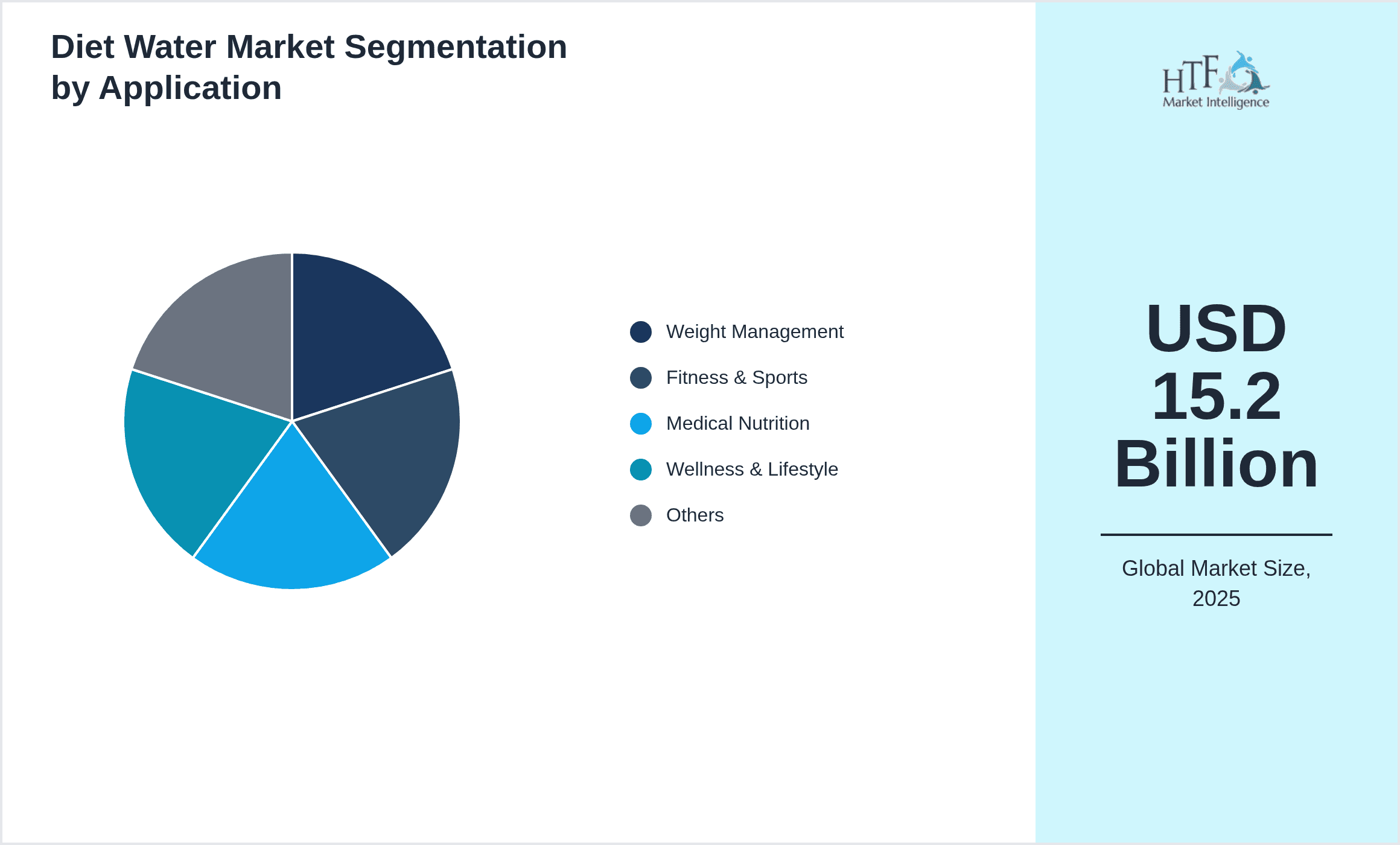

- •Market highlights include a base size of USD 15.2 Billion in 2024 projected to reach USD 48.7 Billion by 2034, driven by a robust CAGR of 12.4%. North America holds the dominant regional market share due to mature health and wellness trends, while Asia-Pacific exhibits the fastest growth fueled by expanding middle-class populations and increasing fitness awareness. Flavored diet water leads the product type segment, with vitamin-enhanced variants gaining rapid traction. Key growth indicators reflect rising demand for functional beverages combined with consumer preference for low-calorie, nutrient-enriched hydration options. The strategic importance of diet water lies in its ability to bridge pure hydration with health benefits, positioning it as a critical category within the global bottled water and functional beverage markets.

- •The value proposition of the diet water market is anchored in offering consumers innovative hydration solutions that align with evolving health and lifestyle priorities. This market plays a vital role for beverage manufacturers, retailers, healthcare providers, and fitness enterprises by enabling product diversification and catering to specific nutritional needs. Its strategic importance is underscored by growing consumer inclination toward wellness and preventive healthcare, making diet water a preferred choice across demographics. Advances in technology allow for enhanced formulations with targeted vitamins and minerals, further expanding market potential. The sector's growth supports broader sustainability initiatives through improved packaging and reduced sugar content compared to traditional soft drinks, aligning with global health and environmental goals.

Competitive Landscape

The global diet water market is characterized by intense competition among multinational beverage corporations, niche players specializing in functional hydration, and emerging startups innovating with natural and fortified ingredients. Market dynamics are influenced by product innovation, brand differentiation, pricing strategies, and extensive distribution networks. Leading companies invest heavily in research and development to create unique formulations that meet diverse consumer preferences and regulatory standards. Strategic partnerships and collaborations with health and wellness brands enhance market positioning. Rivalry also manifests in expanding geographic reach and penetrating emerging markets. Competitive advantages are gained through proprietary technologies, sustainable packaging, and strong marketing campaigns emphasizing health benefits. Market entry barriers include stringent regulatory compliance and high capital requirements for product development and distribution. The competitive environment is expected to intensify with the rising consumer demand for personalized and clean-label diet water products, driving continuous innovation and consolidation in the industry.

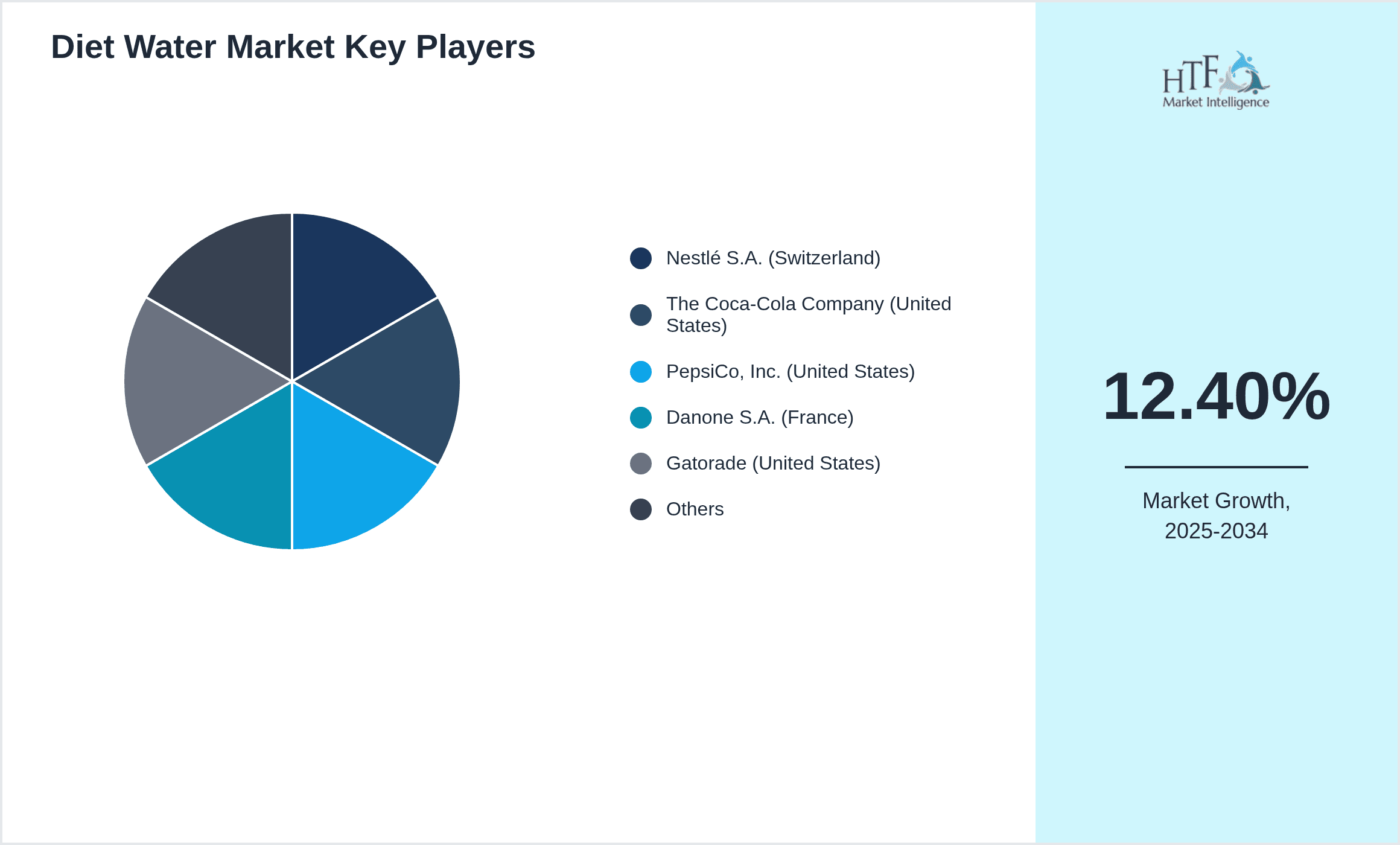

Leading Companies in Diet Water Market

- •Nestlé S.A. (Switzerland)

- •The Coca-Cola Company (United States)

- •PepsiCo, Inc. (United States)

- •Danone S.A. (France)

- •Gatorade (United States)

- •The Kraft Heinz Company (United States)

- •Hain Celestial Group, Inc. (United States)

- •Keurig Dr Pepper Inc. (United States)

- •Monster Beverage Corporation (United States)

- •Britvic plc (United Kingdom)

- •Califia Farms (United States)

- •Suntory Beverage & Food Ltd. (Japan)

- •Peet's Coffee & Tea (United States)

- •LaCroix Sparkling Water (United States)

- •Fiji Water LLC (United States)

- •Vita Coco Company, Inc. (United States)

- •Spindrift Beverage Co. (United States)

- •AQUAhydrate (United States)

- •Peñafiel (Mexico)

- •Bai Brands (United States)

- •Hint, Inc. (United States)

- •Tropicana Products, Inc. (United States)

- •Evian (France)

- •Glacéau (United States)

- •Perrier (France)

Market Breakdown

- •By Type

- ◦Flavored Diet Water

- ◦Vitamin-Enhanced Diet Water

- ◦Electrolyte-Infused Diet Water

- ◦Carbonated Diet Water

- ◦Others

- •By Application

- ◦Weight Management

- ◦Fitness & Sports

- ◦Medical Nutrition

- ◦Wellness & Lifestyle

- ◦Others

- •By Distribution Channel

- ◦Supermarkets & Hypermarkets

- ◦Convenience Stores

- ◦Online Retail

- ◦Specialty Stores

- •By Packaging Material

- ◦Plastic Bottles

- ◦Glass Bottles

- ◦Cartons

- ◦Others

Growth Dynamics

- •The rising consumer preference for healthier beverage options with low or zero calories is a primary growth driver for the diet water market. Increasing awareness about obesity and lifestyle diseases encourages consumers to opt for diet water products that provide hydration without added sugars or calories.

- •Innovations such as vitamin fortification and electrolyte infusion in diet water have expanded its application in fitness and medical nutrition sectors. These product enhancements appeal to athletes and patients requiring specialized hydration solutions, driving market expansion.

- •The convenience of on-the-go packaging and the growth of online retail channels facilitate wider product availability, enhancing consumer access globally. E-commerce platforms enable consumers to explore a broader range of diet water options, supporting rapid market growth.

- •Government initiatives promoting health and wellness along with stringent regulations limiting sugar content in beverages encourage manufacturers to develop diet water alternatives. Such regulatory environments support market growth by fostering innovation and consumer trust.

- •Increasing investments by key players in marketing and distribution networks strengthen brand visibility and consumer adoption. Strategic collaborations with fitness centers and healthcare providers further propel market penetration and acceptance.

Market Trends

- •The rise of clean-label products has led to increased demand for diet water formulations free from artificial additives and preservatives, fostering trust among health-conscious consumers and driving product reformulations.

- •Sustainability initiatives focusing on biodegradable and recyclable packaging materials are influencing product development, with companies investing in eco-friendly bottles to reduce environmental impact.

- •Personalization in diet water products through customizable flavor and nutrient profiles is emerging, catering to individual health goals and boosting consumer engagement.

- •The integration of functional ingredients such as antioxidants, collagen, and probiotics is expanding the functional beverage category, enhancing diet water's appeal beyond basic hydration.

- •Collaborations between beverage companies and fitness technology firms are creating innovative marketing campaigns that link diet water consumption to fitness tracking and wellness apps.

Market Opportunities

- •Emerging markets in Asia-Pacific and Latin America present significant growth potential due to rising health awareness and increasing disposable incomes, offering opportunities for market expansion and new product launches.

- •Development of sugar-free and organic diet water variants can cater to the growing demand for natural and health-focused beverages, tapping into niche consumer segments.

- •Collaborations with healthcare providers to promote diet water as part of medical nutrition therapy can open new application avenues and enhance product credibility.

- •Advancements in packaging technologies such as smart bottles with hydration tracking capabilities provide differentiation opportunities and enhance consumer experience.

- •Expansion of online retail platforms and direct-to-consumer sales models can increase market reach and consumer convenience, fostering brand loyalty.

Market Challenges

- •High production costs associated with vitamin fortification and advanced formulations may limit market entry for smaller players and impact pricing strategies.

- •Consumer skepticism about the health benefits of diet water products due to lack of standardization and regulatory oversight poses a challenge to market growth.

- •Competition from traditional bottled water and other functional beverages may restrict diet water market share unless differentiation is effectively communicated.

- •Stringent regulations across different regions regarding health claims and ingredient labeling require significant compliance efforts from manufacturers.

- •Supply chain disruptions affecting raw material availability and packaging components can hinder production and timely product delivery.

Regulatory Framework

- •Between 2019 and 2024, governments worldwide introduced regulations limiting sugar content in beverages, requiring manufacturers to reformulate diet water products to meet health standards and labeling requirements.

- •New labeling guidelines enforced stricter disclosure of added vitamins and minerals in diet water to ensure consumer transparency and prevent misleading health claims.

- •Environmental regulations promoting sustainable packaging led to mandates for increased use of recyclable and biodegradable materials in bottled beverages.

- •Region-specific mandates in North America and Europe require compliance with food safety standards such as FDA and EFSA regulations covering ingredient safety and manufacturing practices.

- •Incentives and subsidies were introduced in select regions to encourage the production and consumption of low-calorie, functional beverages aligned with public health goals.

Market Intelligence

- •15th January 2025, Nestlé S.A. launched a new range of vitamin-enhanced diet water products featuring a blend of essential nutrients targeted at fitness enthusiasts and health-conscious consumers. The product line, available globally, incorporates natural flavors and zero-calorie formulations to appeal to the growing demand for functional hydration. Nestlé's strategic objective focuses on expanding its market share in the functional beverage sector by leveraging advanced nutrient delivery technologies and sustainable packaging solutions. This launch positions Nestlé competitively in the fast-growing diet water segment, catering to diverse consumer needs while aligning with health and wellness trends. Source: Nestlé Official Press Release

- •10th March 2025, The Coca-Cola Company introduced an innovative electrolyte-infused diet water product designed for athletes and active individuals seeking rapid hydration and recovery. The product features a scientifically balanced electrolyte composition and is marketed through partnerships with major sports events and fitness centers. This launch reflects Coca-Cola's commitment to diversifying its portfolio towards healthier beverage options and capitalizing on the rising trend of functional hydration. The company's focus on digital marketing campaigns and e-commerce distribution channels aims to enhance accessibility and consumer engagement globally. Source: The Coca-Cola Company Newsroom

- •5th June 2024, Danone S.A. announced a strategic partnership with a leading health technology firm to develop smart packaging for diet water products. This collaboration aims to integrate hydration tracking features and personalized nutrition recommendations via connected mobile applications. The initiative supports Danone's innovation roadmap focusing on digital transformation and consumer-centric product development. By combining technology with functional beverages, Danone targets enhanced user experience and strengthened brand loyalty, positioning itself at the forefront of the evolving diet water market. Source: Danone Corporate Communications

- •20th September 2024, PepsiCo, Inc. completed the acquisition of a regional vitamin-enhanced water brand to expand its presence in the functional beverage market across Asia-Pacific. The acquisition enables PepsiCo to leverage localized consumer insights and accelerate portfolio diversification. Integration plans include scaling manufacturing capabilities and expanding distribution networks through PepsiCo's established channels. This move aligns with the company's strategy to capture emerging market demand and drive sustainable growth in the diet water segment. Source: PepsiCo Investor Relations

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 15.2 Billion |

| Forecast Year Market Size | USD 48.7 Billion |

| CAGR | 12.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.6% |

| Scope of Report | Market is segmented by Type (Flavored Diet Water, Vitamin-Enhanced Diet Water, Electrolyte-Infused Diet Water, Carbonated Diet Water, Others), Application (Weight Management, Fitness & Sports, Medical Nutrition, Wellness & Lifestyle, Others), Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Specialty Stores), Packaging Material (Plastic Bottles, Glass Bottles, Cartons, Others) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Nestlé S.A. (Switzerland), The Coca-Cola Company (United States), PepsiCo, Inc. (United States), Danone S.A. (France), Gatorade (United States) |

Global Diet Water Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.