Global Corn Flour Market Size, Growth & Revenue 2024-2034

Global Corn Flour Market is segmented by Type (Native Corn Flour, Modified Corn Flour, Organic Corn Flour, Instant Corn Flour, Other Specialty Corn Flours), Application (Food Industry, Animal Feed, Pharmaceutical, Industrial Uses, Others), Distribution Channel (Supermarkets & Hypermarkets, Online Retail, Specialty Stores, Direct Sales), Processing Technology (Wet Milling, Dry Milling, Nixtamalization, Others), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global corn flour market comprises the production and utilization of powdered corn derived from various corn varieties, serving a wide spectrum of industries including food processing, pharmaceuticals, and animal feed. This market includes multiple types such as native corn flour, modified variants, organic, and instant types, each tailored to meet specific functional and nutritional requirements. The corn flour market's scope covers raw material sourcing, milling technologies, product innovation, and application development across global regions with evolving consumer preferences. The industry benefits from the increasing demand for gluten-free and organic food products, and the growing use of corn flour as a sustainable and cost-effective alternative to wheat flour. Regional dietary habits, regulatory frameworks, and advances in processing technologies shape the competitive landscape. The market's primary use cases involve bakery products, thickening agents in sauces, and industrial applications such as adhesives and biodegradable materials, reflecting a dynamic and expanding industry with significant growth opportunities worldwide.

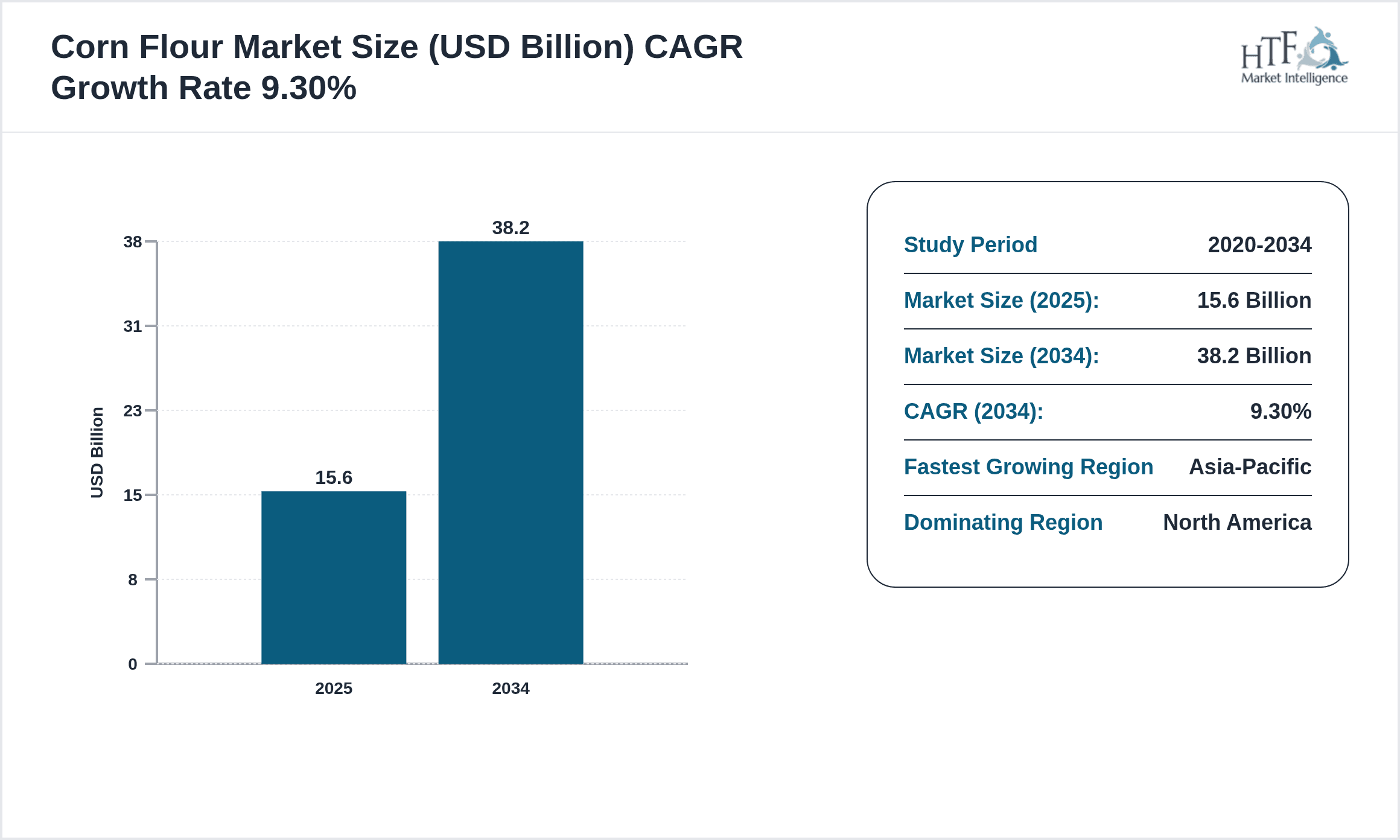

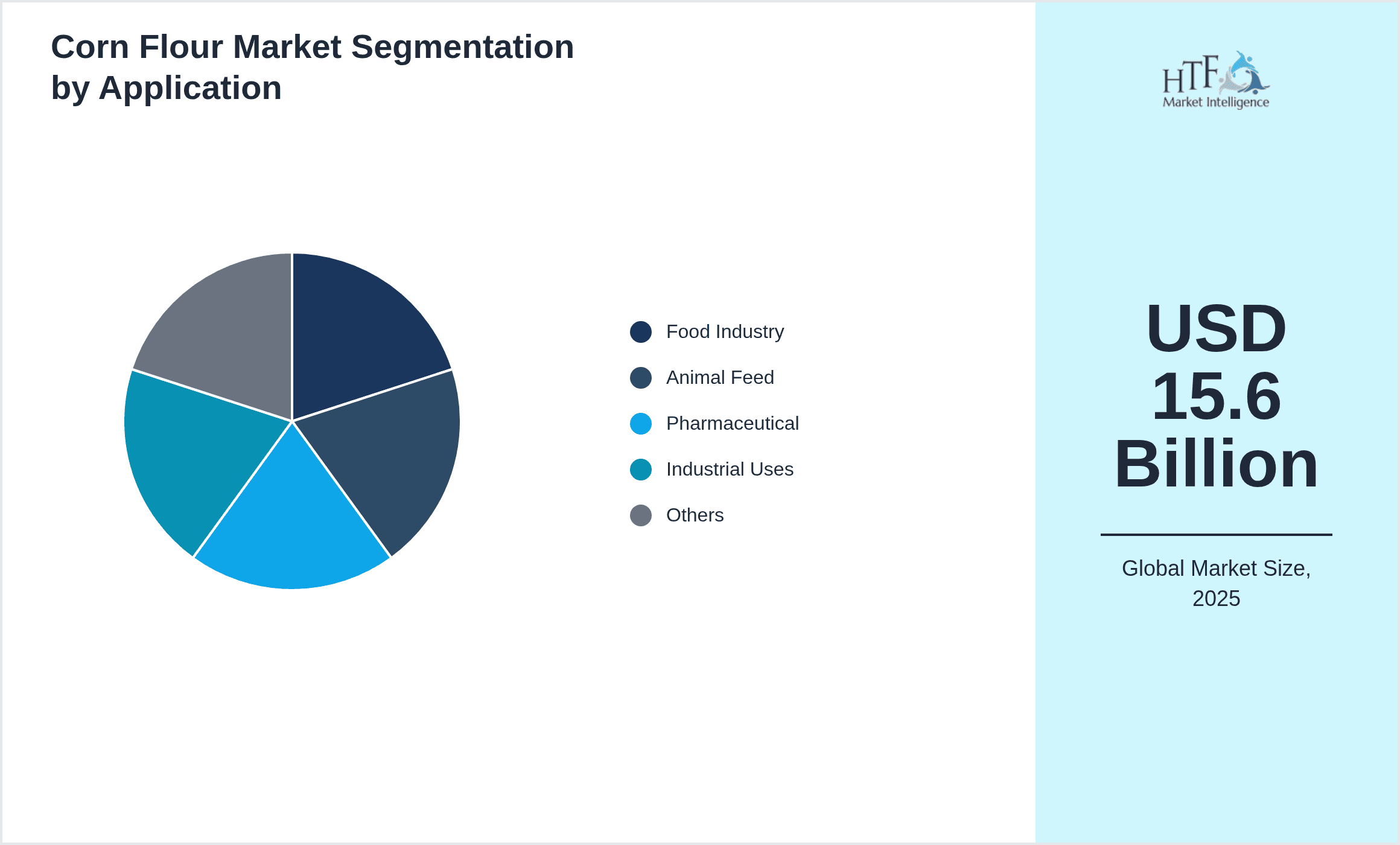

- •Key highlights for the global corn flour market include a projected CAGR of 9.3% from 2024 to 2034, with the market size expected to reach USD 38.2 Billion by 2034 from a base of USD 15.6 Billion in 2024. North America currently dominates the market, holding the largest share due to its well-established food processing industry and high consumption of processed corn products. Asia-Pacific is identified as the fastest-growing region, driven by rising disposable incomes, urbanization, and increasing health-conscious consumer behavior fueling demand for organic and specialty corn flour products. Native corn flour remains the leading product type, while organic corn flour is the fastest growing segment, reflecting shifting consumer preferences towards clean-label and natural ingredients. The food industry application continues to dominate, with expanding uses in bakery, snack foods, and gluten-free products.

- •The global corn flour market offers significant value propositions to stakeholders including manufacturers, distributors, and end-users. For food manufacturers, corn flour provides a versatile, gluten-free base ingredient that aligns with health and dietary trends, enabling product innovation and diversification. Pharmaceutical companies leverage corn flour for its excipient properties in drug formulations. Industrial users benefit from its biodegradability and functional utility in adhesives and packaging. Strategic importance lies in the ability to cater to regional dietary preferences and regulatory compliance, while investing in organic and modified corn flour variants to meet evolving market demands. Overall, the market is positioned for robust growth powered by technological innovation, expanding applications, and increasing global consumption patterns.

Competitive Landscape

The global corn flour market exhibits a highly competitive environment characterized by the presence of multinational corporations, regional producers, and emerging players striving to expand their footprint through product innovation and strategic collaborations. Market leaders focus heavily on research and development to enhance product quality, develop organic and specialty flours, and improve milling efficiencies. Competitive strategies include diversification of product portfolios, geographic expansion, and integration of sustainable sourcing practices. Pricing strategies reflect the balance between raw material costs and consumer willingness to pay for premium products. Companies also invest in branding and marketing to build consumer trust and awareness, particularly in health-conscious segments. Intellectual property protection and regulatory compliance serve as critical barriers to entry. The rivalry is intensified by the growing demand in emerging markets, prompting firms to adopt aggressive expansion and partnership models, while digital transformation in supply chain and distribution channels enhances competitive positioning. Future trends indicate increased consolidation through mergers and acquisitions, fostering innovation and market penetration.

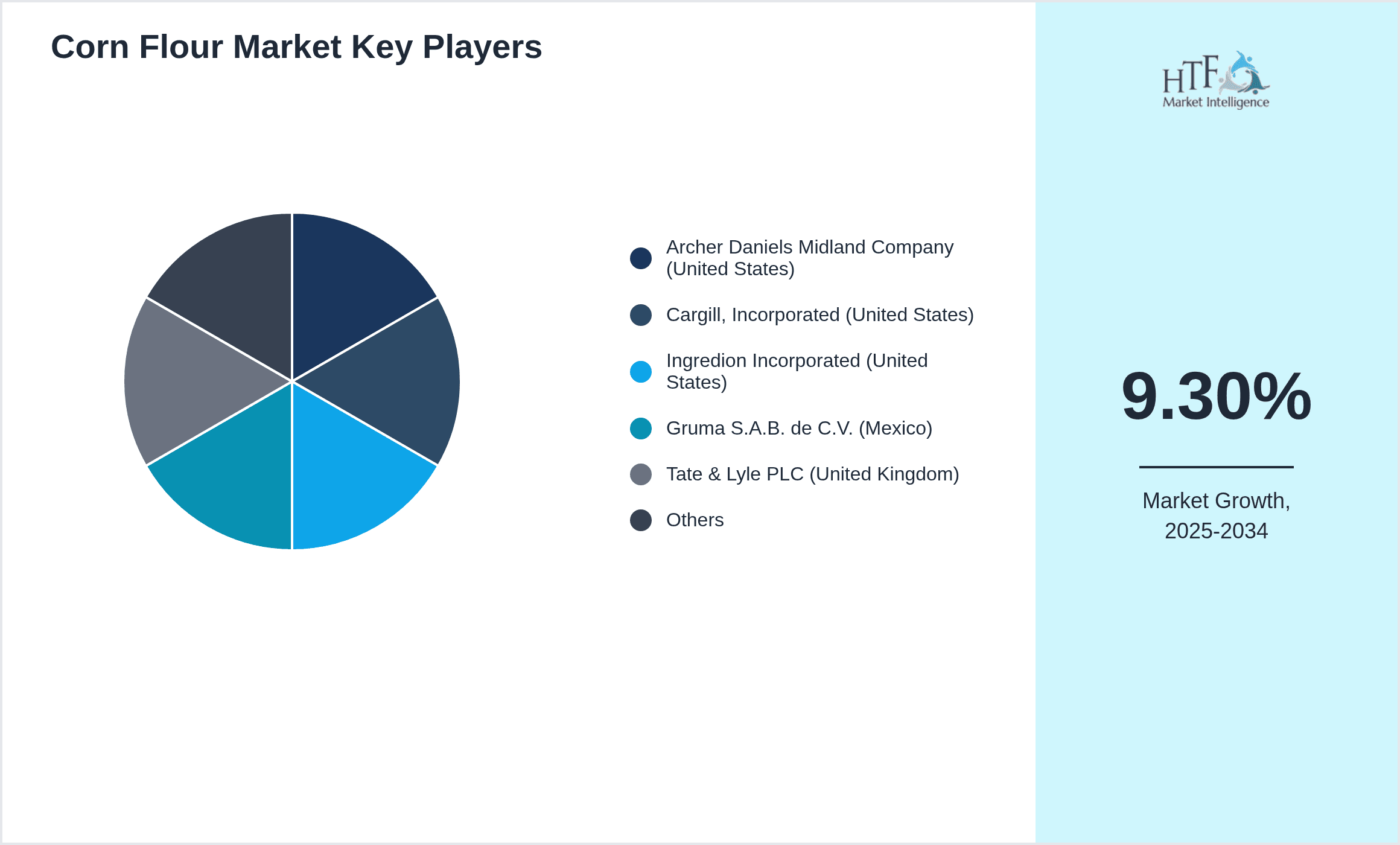

Leading Companies in Corn Flour Market

- •Archer Daniels Midland Company (United States)

- •Cargill, Incorporated (United States)

- •Ingredion Incorporated (United States)

- •Gruma S.A.B. de C.V. (Mexico)

- •Tate & Lyle PLC (United Kingdom)

- •AGRO Merchants Group (Netherlands)

- •Bunge Limited (United States)

- •The Scoular Company (United States)

- •MGP Ingredients, Inc. (United States)

- •Pon Pure Chemicals Group (India)

- •The Hain Celestial Group, Inc. (United States)

- •SunOpta Inc. (Canada)

- •Shandong Luhua Group (China)

- •Puratos Group (Belgium)

- •Kerry Group plc (Ireland)

- •Roquette Frères (France)

- •Weifang Ensign Industry Co., Ltd. (China)

- •Bühler Group (Switzerland)

- •Agridient Inc. (United States)

- •AGT Food and Ingredients Inc. (Canada)

- •Crompton Greaves Consumer Electricals Ltd. (India)

- •Dawn Food Products (United States)

- •Ingredi (France)

- •Sunshine Mills, Inc. (United States)

- •Zhejiang Yixin Food Co., Ltd. (China)

Market Breakdown

- •By Type

- ◦Native Corn Flour

- ◦Modified Corn Flour

- ◦Organic Corn Flour

- ◦Instant Corn Flour

- ◦Other Specialty Corn Flours

- •By Application

- ◦Food Industry

- ◦Animal Feed

- ◦Pharmaceutical

- ◦Industrial Uses

- ◦Others

- •By Distribution Channel

- ◦Supermarkets & Hypermarkets

- ◦Online Retail

- ◦Specialty Stores

- ◦Direct Sales

- •By Processing Technology

- ◦Wet Milling

- ◦Dry Milling

- ◦Nixtamalization

- ◦Others

Growth Dynamics

- •Increasing consumer preference for gluten-free and organic food products is driving demand for organic and native corn flour variants, significantly boosting market growth globally. This shift is fueled by rising awareness about dietary health and food allergies, especially in North America and Europe.

- •Expansion of the food processing industry, particularly in emerging markets within Asia-Pacific and Latin America, is propelling the consumption of corn flour for bakery, snacks, and convenience foods, supported by urbanization and changing lifestyles.

- •Technological advancements in corn flour processing, such as improved milling and modification techniques, enhance product functionality and shelf life, attracting manufacturers seeking innovative ingredients for diverse applications.

- •Rising demand in pharmaceutical and industrial sectors for corn flour as an excipient and biodegradable material, respectively, is creating additional growth avenues, reflecting diversification beyond traditional food uses.

- •Government initiatives promoting sustainable agriculture and organic farming practices globally are encouraging the production and consumption of organic corn flour, creating positive regulatory support for market expansion.

- •Increasing investment in research and development by key players to develop specialty corn flour products tailored for health-conscious consumers and industrial applications is driving innovation and competitive advantage.

- •Growing online retail channels and direct-to-consumer sales models facilitate broader market reach and consumer access to specialty corn flour products, enhancing market penetration worldwide.

Market Trends

- •The rising trend of clean-label and minimally processed food products is encouraging manufacturers to adopt organic and native corn flour, offering natural ingredient claims and better nutritional profiles.

- •Innovation in instant corn flour products that reduce cooking time and improve convenience is gaining traction, especially in urban markets and among younger consumers.

- •Sustainability is becoming a key focus, with companies integrating eco-friendly sourcing and biodegradable packaging solutions to appeal to environmentally conscious consumers.

- •Strategic collaborations between corn flour producers and food manufacturers to co-develop customized ingredients for specific applications such as gluten-free bakery products are becoming more common.

- •Digital transformation in supply chains and e-commerce platforms is enhancing product traceability, consumer engagement, and streamlined distribution in the corn flour market.

- •Regional flavor adaptations and product formulations are increasingly used to cater to diverse cultural tastes and preferences across Asia-Pacific, Latin America, and Europe.

- •Investment in advanced processing technologies, including enzymatic modification and micronization, is driving product differentiation and functional enhancements in corn flour offerings.

Market Opportunities

- •Emerging markets in Asia-Pacific and Latin America present significant growth potential due to rising disposable incomes, urbanization, and increasing demand for processed and convenience foods containing corn flour.

- •Development of organic and specialty corn flour variants tailored towards health-conscious consumers offers lucrative opportunities for product diversification and premium pricing.

- •Expansion into pharmaceutical and industrial applications, leveraging corn flour's functional properties, can unlock new revenue streams beyond traditional food uses.

- •Adoption of e-commerce and digital marketing strategies enables manufacturers to reach niche consumer segments and increase brand visibility globally.

- •Collaborative innovation with food manufacturers to create customized corn flour blends for gluten-free, vegan, and specialized diets can strengthen market position.

- •Investment in sustainable farming and sourcing practices aligns with global environmental goals, enhancing brand reputation and meeting regulatory expectations.

- •Technological advancements in processing and packaging can improve product shelf life, convenience, and appeal, driving higher consumer adoption.

Market Challenges

- •Raw material price volatility due to fluctuating corn crop yields and climate conditions poses a significant risk to cost structures and profitability for corn flour manufacturers globally.

- •Stringent regulatory standards for food safety and labeling in various regions increase compliance costs and complexity, particularly for organic and specialty corn flour products.

- •Competition from alternative flours such as wheat, rice, and tapioca in both food and industrial applications limits market expansion potential in some segments.

- •Supply chain disruptions caused by geopolitical tensions, transportation bottlenecks, and pandemic-related challenges affect timely delivery and inventory management.

- •Limited consumer awareness and education about the benefits of corn flour, especially in emerging markets, constrain demand growth and adoption rates.

- •High capital investment required for advanced processing technologies and organic certification can be a barrier for smaller manufacturers entering the market.

- •Counterfeit and low-quality product circulation in unregulated markets undermines brand trust and poses health risks to consumers.

Regulatory Framework

- •Between 2019 and 2024, global food safety regulations have tightened, including enhanced traceability and labeling requirements for corn flour products to ensure consumer safety and transparency. These regulations mandate compliance with maximum residue limits for pesticides and contaminants, impacting manufacturers’ sourcing and quality control processes.

- •The introduction of organic certification standards by bodies such as USDA Organic and EU Organic in major markets has established rigorous compliance requirements for organic corn flour producers, influencing market entry and product positioning.

- •Environmental regulations focusing on sustainable agriculture practices and reduction of carbon footprints have encouraged corn flour manufacturers to adopt eco-friendly sourcing and production methods, with some markets offering incentives for compliance.

- •Country-specific mandates on allergen labeling and gluten-free certifications have become critical for corn flour products targeting sensitive consumer groups, affecting formulation and packaging standards.

- •Governments have implemented policies promoting local agriculture and food security, influencing corn flour supply chains and encouraging domestic production, thereby affecting global trade dynamics.

Market Intelligence

- •15th January 2025, Archer Daniels Midland Company launched an innovative organic native corn flour product line designed to meet the increasing demand for clean-label and gluten-free ingredients in North America and Europe. This new product features enhanced nutritional profiles and improved processing characteristics, aimed at bakery and snack manufacturers. The launch aligns with growing consumer preferences for health-oriented products and sustainability. The initiative includes comprehensive supply chain transparency and certification to reinforce consumer trust. Strategic marketing campaigns are planned to boost adoption across retail and foodservice sectors. Source: Official Company Website

- •10th March 2025, Cargill, Incorporated introduced a modified corn flour variant with superior thickening and emulsifying properties targeted at pharmaceutical and industrial applications. The product leverages advanced milling technology to optimize functional performance and shelf stability. This launch supports Cargill’s diversification strategy into specialty ingredient markets, enhancing its portfolio with value-added products. The company anticipates increased uptake in emerging markets due to rising industrial demand. Strategic partnerships with pharmaceutical manufacturers are underway to accelerate integration. Source: Industry Publication

- •22nd May 2025, Ingredion Incorporated announced a strategic alliance with a leading food manufacturer to co-develop customized corn flour blends tailored for gluten-free bakery products. This partnership focuses on leveraging Ingredion’s expertise in ingredient functionality and the partner’s extensive distribution network. The collaboration aims to address the expanding gluten-free segment globally, enhancing product quality and consumer acceptance. Joint R&D initiatives include formulation optimization and consumer sensory studies. The alliance is expected to drive significant revenue growth and market share gains. Source: Company Press Release

- •5th August 2025, Gruma S.A.B. de C.V. completed the acquisition of a regional organic corn flour producer in Asia-Pacific, expanding its presence in the fastest-growing market segment. The acquisition strengthens Gruma’s portfolio with organic and specialty corn flour products, aligning with consumer trends and environmental sustainability goals. Post-acquisition integration plans include capacity expansion and technology upgrades to enhance product quality and supply chain efficiency. This move positions Gruma competitively against global and local players, enhancing its footprint in emerging markets. Source: Industry News

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 15.6 Billion |

| Forecast Year Market Size | USD 38.2 Billion |

| CAGR | 9.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.9% |

| Scope of Report | Market is segmented by Type (Native Corn Flour, Modified Corn Flour, Organic Corn Flour, Instant Corn Flour, Other Specialty Corn Flours), Application (Food Industry, Animal Feed, Pharmaceutical, Industrial Uses, Others), Distribution Channel (Supermarkets & Hypermarkets, Online Retail, Specialty Stores, Direct Sales), Processing Technology (Wet Milling, Dry Milling, Nixtamalization, Others) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Archer Daniels Midland Company (United States), Cargill, Incorporated (United States), Ingredion Incorporated (United States), Gruma S.A.B. de C.V. (Mexico), Tate & Lyle PLC (United Kingdom) |

Global Corn Flour Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.