North America Wheat Proteins Market Scope & Changing Dynamics 2025-2034

North America Wheat Proteins (Wheat Gluten) Market is segmented by Product Type (Vital Wheat Gluten, Gluten Powder, Gluten Concentrate, Gluten Hydrolysate, Modified Wheat Gluten), Application (Baking, Meat Alternatives, Animal Feed, Nutraceuticals, Others), Formulation Type (Powdered, Concentrated, Hydrolyzed), Manufacturing Process (Wet Extraction, Dry Milling, Enzymatic Hydrolysis), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

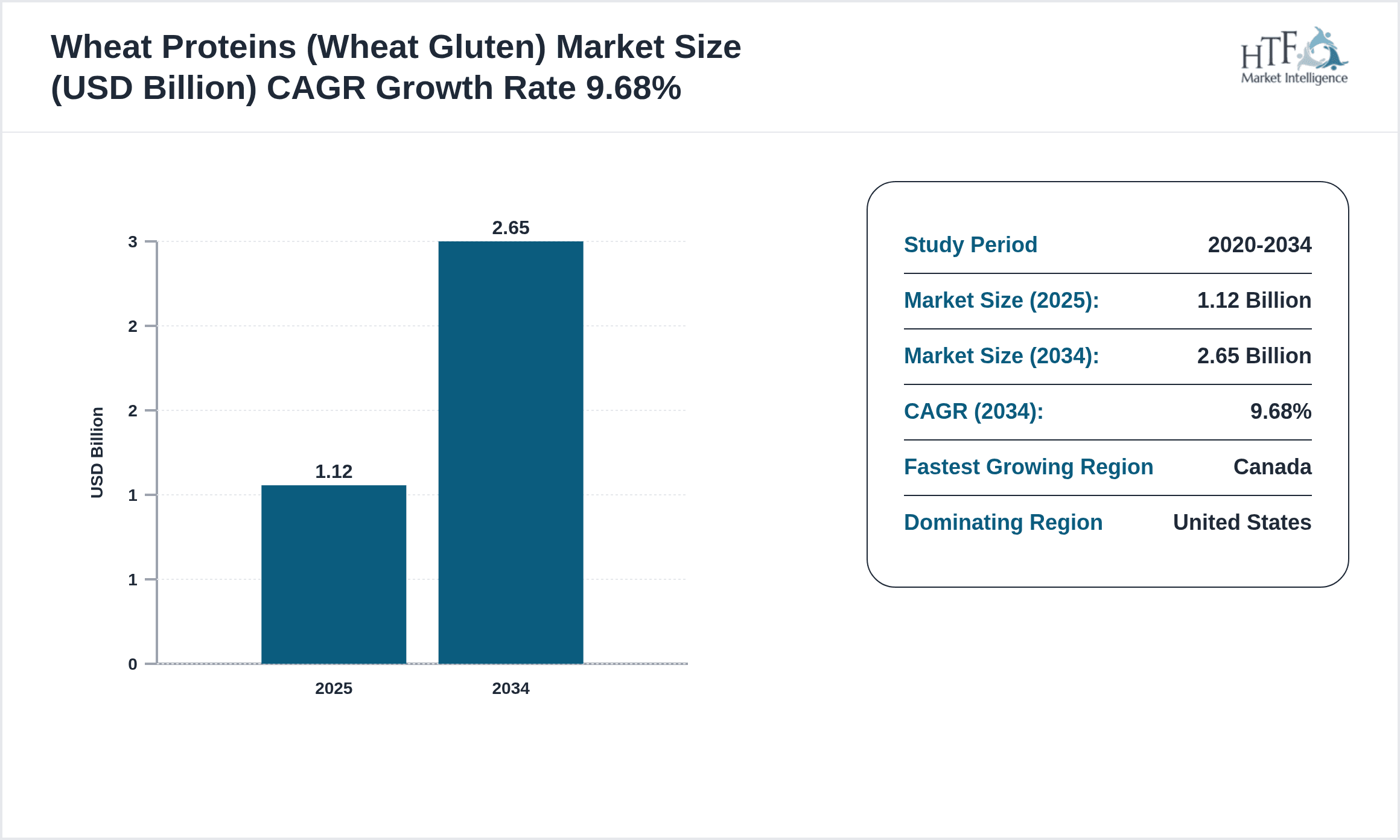

- •The North America Wheat Proteins (Wheat Gluten) market represents a critical segment within the plant-based protein industry, focusing on the extraction and utilization of wheat-derived proteins such as vital wheat gluten, gluten powder, and gluten hydrolysate. This market primarily serves the baking industry where wheat gluten enhances dough elasticity and bread volume, alongside growing applications in meat alternatives, animal feed, and nutraceuticals. The market value chain spans wheat farming, gluten extraction processes, refinement technologies, and end-product formulation, involving key stakeholders from raw material suppliers to food manufacturers. Increasing consumer demand for plant-based proteins driven by health awareness, coupled with technological advancements in gluten modification, supports market expansion. Regulatory compliance and sustainability trends are shaping production and innovation, while North America's established infrastructure and consumption patterns facilitate market penetration. The market is forecasted to experience significant growth driven by shifting dietary preferences, innovative product development, and rising applications across diverse industries.

- •Key highlights include a base market size of USD 1.12 Billion in 2025, expanding to USD 2.65 Billion by 2034, reflecting a robust CAGR of 9.68%. The United States dominates the regional market due to its large food processing industry and high consumer adoption of plant-based diets, whereas Canada is identified as the fastest growing country, driven by rising health-conscious consumers and innovative gluten applications. Vital wheat gluten remains the leading product type, favored for its superior baking properties, while gluten hydrolysate is the fastest growing segment due to its enhanced solubility and nutritional value. These dynamics underscore a vibrant market landscape with ample opportunities for new entrants and technology advancements.

- •The value proposition of the North America Wheat Proteins market lies in its ability to offer functional, nutritional, and sustainable protein solutions aligned with modern food industry demands. It strategically supports bakery manufacturers, plant-based meat producers, animal nutrition formulators, and nutraceutical companies by providing versatile, high-quality gluten products. Stakeholders benefit from ongoing research in protein modification, regulatory adherence ensuring product safety, and growing consumer preference towards natural, plant-sourced ingredients. This market plays an essential role in driving innovation, meeting regulatory mandates, and responding to evolving dietary trends, making it a pivotal sector within the broader food and health industries.

Competitive Landscape

The North America Wheat Proteins (Wheat Gluten) market exhibits a competitive environment characterized by a mix of multinational corporations, regional producers, and specialized ingredient suppliers. Key competitive strategies include product innovation focusing on enhanced functionality and nutritional profiles, strategic partnerships to expand distribution and R&D capabilities, and mergers and acquisitions aimed at consolidating market presence and achieving economies of scale. Companies are investing in sustainable sourcing and cleaner production technologies to meet regulatory and consumer expectations, while pricing strategies are adapted to balance quality and affordability amid raw material cost fluctuations. Market entry barriers include stringent food safety regulations, capital-intensive processing facilities, and the need for strong supply chain networks. Regional competition varies with the United States leading in volume and innovation, while Canada offers growth through niche applications and emerging startups. Future competitive trends indicate increased focus on plant-based protein blends, clean label solutions, and expansion into nutraceutical and functional food segments, positioning the market for dynamic evolution over the forecast period.

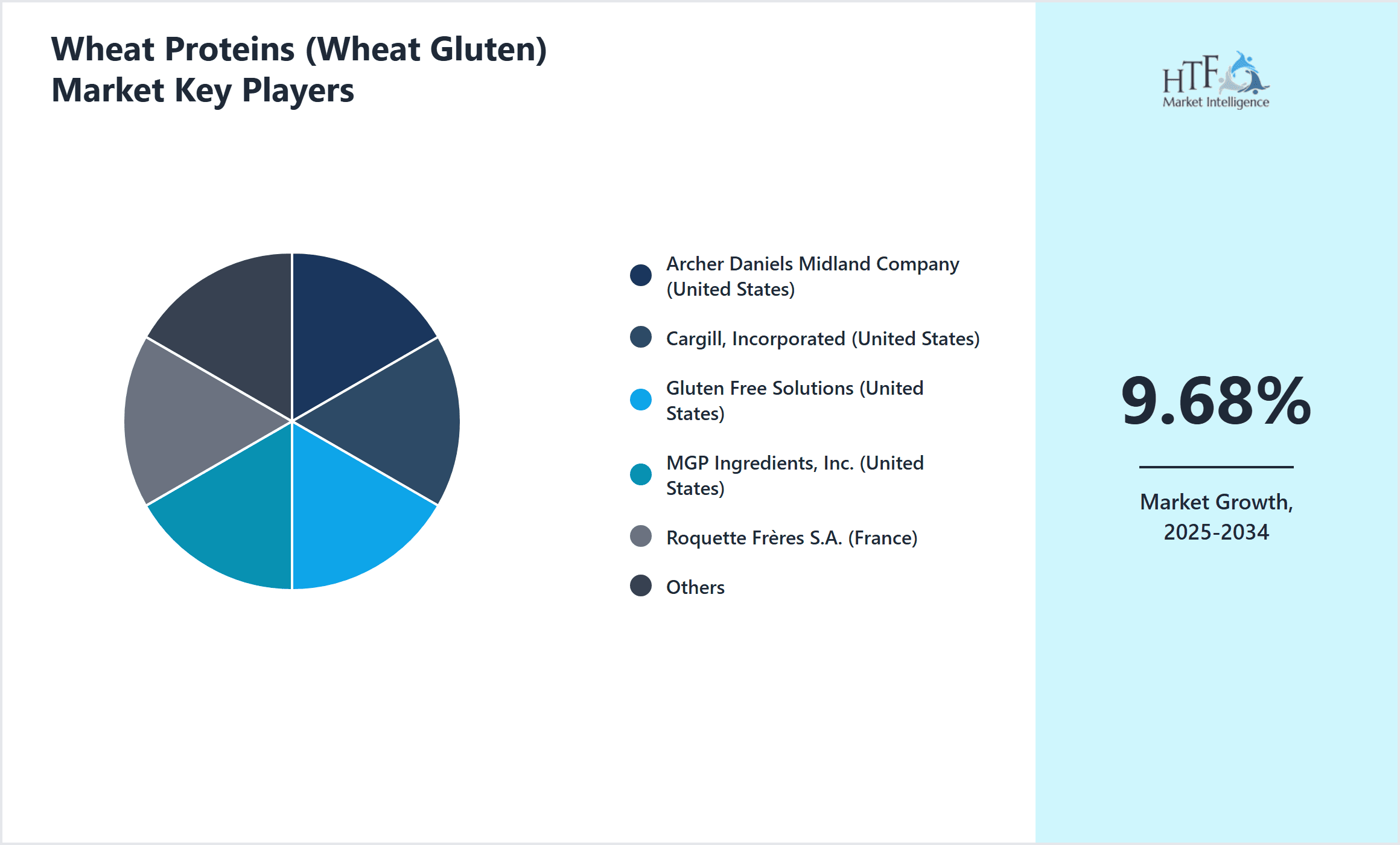

Leading Companies in Wheat Proteins (Wheat Gluten) Market

- •Archer Daniels Midland Company (United States)

- •Cargill, Incorporated (United States)

- •Gluten Free Solutions (United States)

- •MGP Ingredients, Inc. (United States)

- •Roquette Frères S.A. (France)

- •The Scoular Company (United States)

- •AB Mauri (United Kingdom)

- •Ingredion Incorporated (United States)

- •Tate & Lyle PLC (United Kingdom)

- •Axiom Foods, Inc. (United States)

- •Kerry Group plc (Ireland)

- •SunOpta Inc. (Canada)

- •BENEO GmbH (Germany)

- •Puratos Group (Belgium)

- •Pioneer Ingredients, Inc. (United States)

- •Lantmännen Group (Sweden)

- •Ingredion Canada Corporation (Canada)

- •CPI Canada (Canada)

- •Penford Corporation (United States)

- •ADM Milling Co. (United States)

- •Bunge Limited (United States)

- •Viking Malt (Finland)

- •SunOpta Ingredients, Inc. (Canada)

- •VanDrie Group (Netherlands)

- •Glutenberg (Canada)

Market Breakdown

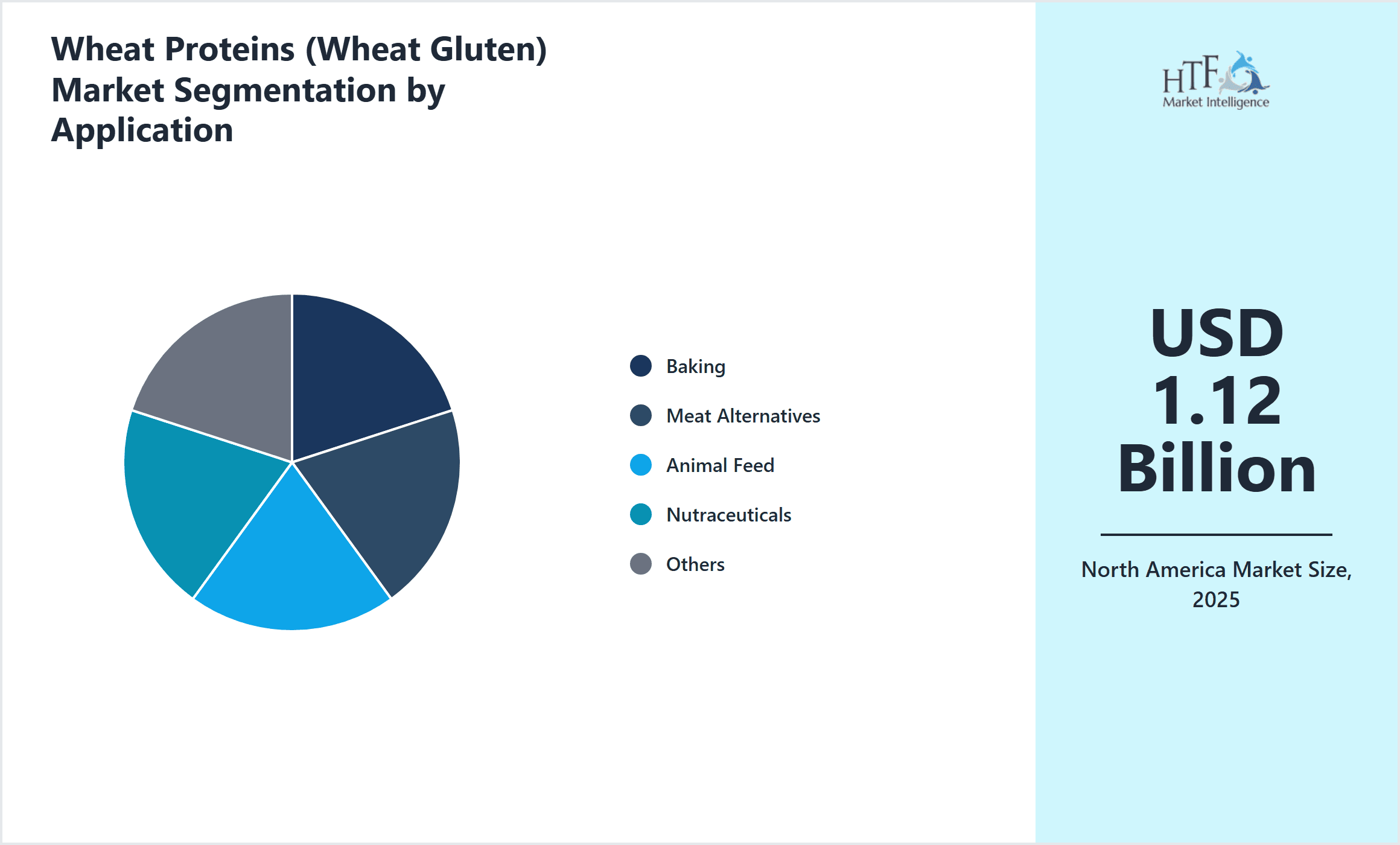

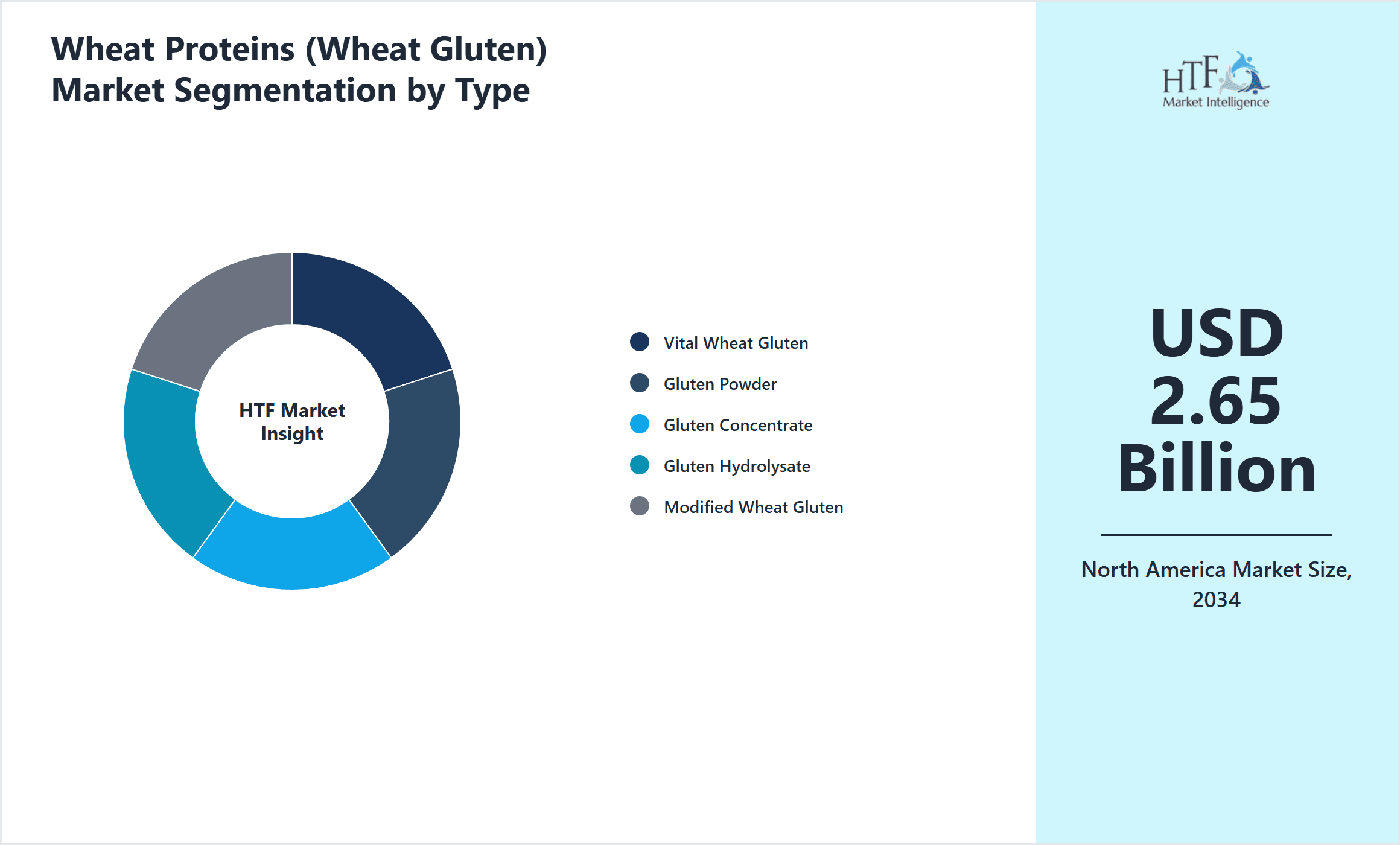

- •By Product Type

- ◦Vital Wheat Gluten

- ◦Gluten Powder

- ◦Gluten Concentrate

- ◦Gluten Hydrolysate

- ◦Modified Wheat Gluten

- •By Application

- ◦Baking

- ◦Meat Alternatives

- ◦Animal Feed

- ◦Nutraceuticals

- ◦Others

- •By Formulation Type

- ◦Powdered

- ◦Concentrated

- ◦Hydrolyzed

- •By Manufacturing Process

- ◦Wet Extraction

- ◦Dry Milling

- ◦Enzymatic Hydrolysis

Growth Dynamics

- •Rising consumer demand for plant-based protein products is a major driver, especially driven by health-conscious and vegan populations in North America. This shift is stimulating growth in wheat protein applications beyond traditional baking into meat alternatives and nutraceuticals, expanding market scope and value.

- •Technological advancements in gluten extraction and modification processes have improved protein functionality and solubility, enabling new product formulations and enhancing application versatility across food and feed industries, thereby supporting market expansion.

- •Increasing regulations promoting clean label and sustainable food ingredients encourage manufacturers to adopt wheat proteins as natural, non-GMO alternatives, boosting market acceptance and encouraging product innovation within regulatory frameworks.

- •Growth in the bakery sector, particularly in artisanal and specialty breads, leverages vital wheat gluten for improved texture and shelf life, reinforcing steady demand and providing stable growth opportunities in North America.

- •Investments in R&D by key companies to develop gluten hydrolysates and modified wheat gluten with enhanced nutritional profiles support penetration into functional foods and dietary supplements, creating new revenue streams and market niches.

- •The expanding pet food and animal feed market incorporating wheat proteins as cost-effective, high-protein ingredients contributes to diversifying demand and strengthening overall market growth dynamics in the region.

- •Strategic collaborations between ingredient suppliers and food manufacturers enable tailored wheat protein solutions, fostering innovation and accelerating market adoption in emerging application segments.

Market Trends

- •The trend towards clean label and natural ingredients is driving manufacturers to replace synthetic additives with wheat proteins, which are perceived as healthier and more sustainable by consumers, thus influencing product development strategies.

- •Increased application of wheat proteins in plant-based meat alternatives is a significant trend, capitalizing on gluten’s texturizing properties to mimic meat textures, which aligns with consumer demand for sustainable protein sources.

- •Emergence of gluten hydrolysates with improved solubility and digestibility is encouraging their use in beverages and nutraceutical formulations, expanding the market beyond traditional solid food applications.

- •Manufacturers are adopting enzymatic hydrolysis techniques to enhance the functional and nutritional attributes of wheat proteins, enabling innovation in high-protein, low-allergen food products.

- •Sustainability initiatives, including sourcing from non-GMO wheat and reducing water consumption in processing, are becoming mainstream trends that appeal to environmentally conscious consumers and regulators alike.

- •Growing e-commerce and direct-to-consumer sales channels are facilitating greater accessibility and awareness of wheat protein ingredients and products among end-users, accelerating market penetration.

- •Collaborations between ingredient manufacturers and food tech startups are fostering rapid innovation cycles, especially in developing novel meat alternative products enriched with wheat protein components.

Market Opportunities

- •Expanding applications of wheat proteins in plant-based meat and dairy alternatives present considerable growth potential, driven by consumer demand for sustainable and nutritious protein sources in North America.

- •Development of gluten hydrolysate and modified wheat gluten with enhanced digestibility and functional properties opens new avenues in nutraceuticals and dietary supplement markets.

- •Increasing demand for clean label, allergen-friendly food products offers opportunities for wheat protein formulations with reduced allergenic potential and natural labeling advantages.

- •Investment in sustainable production technologies and sourcing practices can differentiate products, attract eco-conscious consumers, and comply with tightening regulatory standards, enhancing market competitiveness.

- •Opportunities exist in the animal feed segment by leveraging wheat proteins as cost-effective, high-protein ingredients to improve feed formulations and livestock nutrition efficiency.

- •Collaboration between ingredient suppliers and food manufacturers to co-develop customized wheat protein blends tailored to specific applications can unlock niche markets and drive innovation.

- •Geographic expansion within North America, focusing on emerging markets and health-driven consumer segments, presents untapped growth potential for wheat protein producers.

Market Challenges

- •Gluten sensitivity and celiac disease awareness pose challenges by limiting consumer acceptance of wheat proteins in certain population segments, requiring clear labeling and alternative product development.

- •Fluctuations in wheat crop yields and prices due to climate variability and geopolitical factors impact raw material availability and cost structures, affecting market stability.

- •Complexity in modifying gluten proteins to reduce allergenicity while maintaining functional properties presents technical challenges that require significant R&D investment.

- •Stringent regulatory standards related to food safety, labeling, and claims necessitate continuous compliance efforts and can delay product launches or increase costs.

- •Competition from alternative plant proteins such as soy, pea, and rice protein creates market pressure, requiring differentiation through product innovation and marketing.

- •Consumer misconceptions about gluten and wheat proteins, including associations with negative health effects, may hinder market growth despite scientific evidence supporting their benefits.

- •Supply chain disruptions and logistical challenges can affect timely delivery of wheat protein ingredients, impacting manufacturing schedules and customer satisfaction.

Regulatory Framework

- •Between 2020 and 2025, the Food and Drug Administration (FDA) implemented enhanced labeling requirements for gluten-containing ingredients to protect consumers with gluten-related disorders, impacting product formulations and marketing strategies.

- •The U.S. Department of Agriculture (USDA) established stricter guidelines on non-GMO and organic certifications for wheat-derived protein products, influencing sourcing and production practices in the North American market.

- •The Food Safety Modernization Act (FSMA) enforced updated preventive controls for human and animal food, requiring wheat protein manufacturers to adopt comprehensive risk management and traceability systems.

- •Canada’s Canadian Food Inspection Agency (CFIA) introduced specific allergen labeling regulations for gluten-containing products between 2020 and 2025, aligning with international standards and enhancing consumer safety.

- •Environmental regulations targeting water use efficiency and waste management in food ingredient manufacturing plants have been tightened in both the U.S. and Canada, encouraging sustainable wheat protein production processes.

Market Intelligence

- •15th March 2025, Archer Daniels Midland Company announced the launch of a new line of gluten hydrolysate ingredients designed for enhanced solubility and nutritional benefits targeting the nutraceutical and functional beverage markets in North America. This product is expected to meet rising demand for plant-based protein supplements and support the company’s strategic expansion into health-focused food segments. The initiative includes investment in advanced enzymatic hydrolysis technology to optimize protein profiles and improve digestibility. Market analysts project this product will significantly strengthen ADM’s position in the wheat protein ingredient market. Source: Official company press release.

- •10th June 2025, Cargill, Incorporated introduced a modified wheat gluten product with improved allergen management properties, aimed at bakery and meat alternative manufacturers seeking clean label and hypoallergenic ingredient solutions. This innovation leverages proprietary processing technologies to reduce gluten-related immunogenic peptides while maintaining functional qualities essential for product texture and stability. The launch aligns with growing regulatory demands and consumer preferences for allergen-friendly foods in North America. Cargill’s strategic focus on sustainable sourcing and product diversification is expected to drive long-term market growth. Source: Industry publication report.

- •22nd September 2025, SunOpta Inc. completed the acquisition of a regional wheat protein processing facility in Canada to expand its production capacity and enhance supply chain integration for wheat gluten products. This move supports SunOpta’s objective to meet growing demand in the Canadian and broader North American markets, particularly within plant-based food and nutraceutical segments. The acquisition is expected to enable faster product innovation cycles and improve operational efficiency, reinforcing SunOpta’s competitive position. Market experts view this consolidation as a strategic step toward market leadership in wheat protein ingredients. Source: Company website.

- •30th November 2024, Ingredion Incorporated announced a partnership with a leading North American plant-based meat producer to co-develop wheat gluten formulations tailored for improved texture and nutritional profile. This collaboration aims to accelerate product development and commercialization of next-generation meat alternatives containing wheat proteins. The initiative highlights the growing importance of ingredient customization and collaborative innovation in driving market expansion. Ingredion’s expertise in starch and protein technologies is expected to complement the partner’s product portfolio effectively. Source: Official press release.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.12 Billion |

| Forecast Year Market Size | USD 2.65 Billion |

| CAGR | 9.68% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.23% |

| Scope of Report | Market is segmented by Product Type (Vital Wheat Gluten, Gluten Powder, Gluten Concentrate, Gluten Hydrolysate, Modified Wheat Gluten), Application (Baking, Meat Alternatives, Animal Feed, Nutraceuticals, Others), Formulation Type (Powdered, Concentrated, Hydrolyzed), Manufacturing Process (Wet Extraction, Dry Milling, Enzymatic Hydrolysis) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Archer Daniels Midland Company (United States), Cargill, Incorporated (United States), Gluten Free Solutions (United States), MGP Ingredients, Inc. (United States), Roquette Frères S.A. (France) |

North America Wheat Proteins Market Scope & Changing Dynamics 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.