Asia-Pacific Digital-to-Analog Converter Card Market Scope & Changing Dynamics 2024-2034

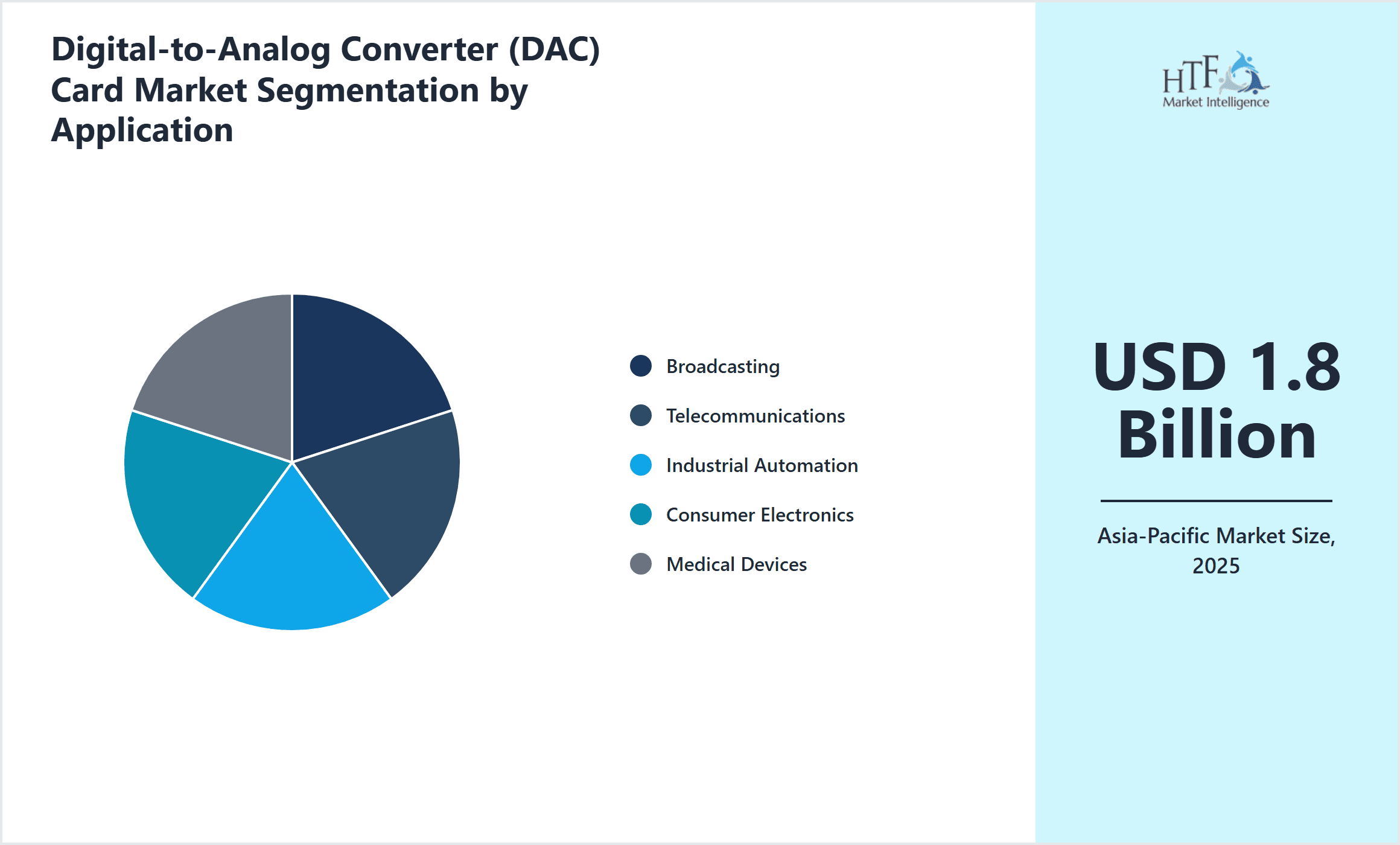

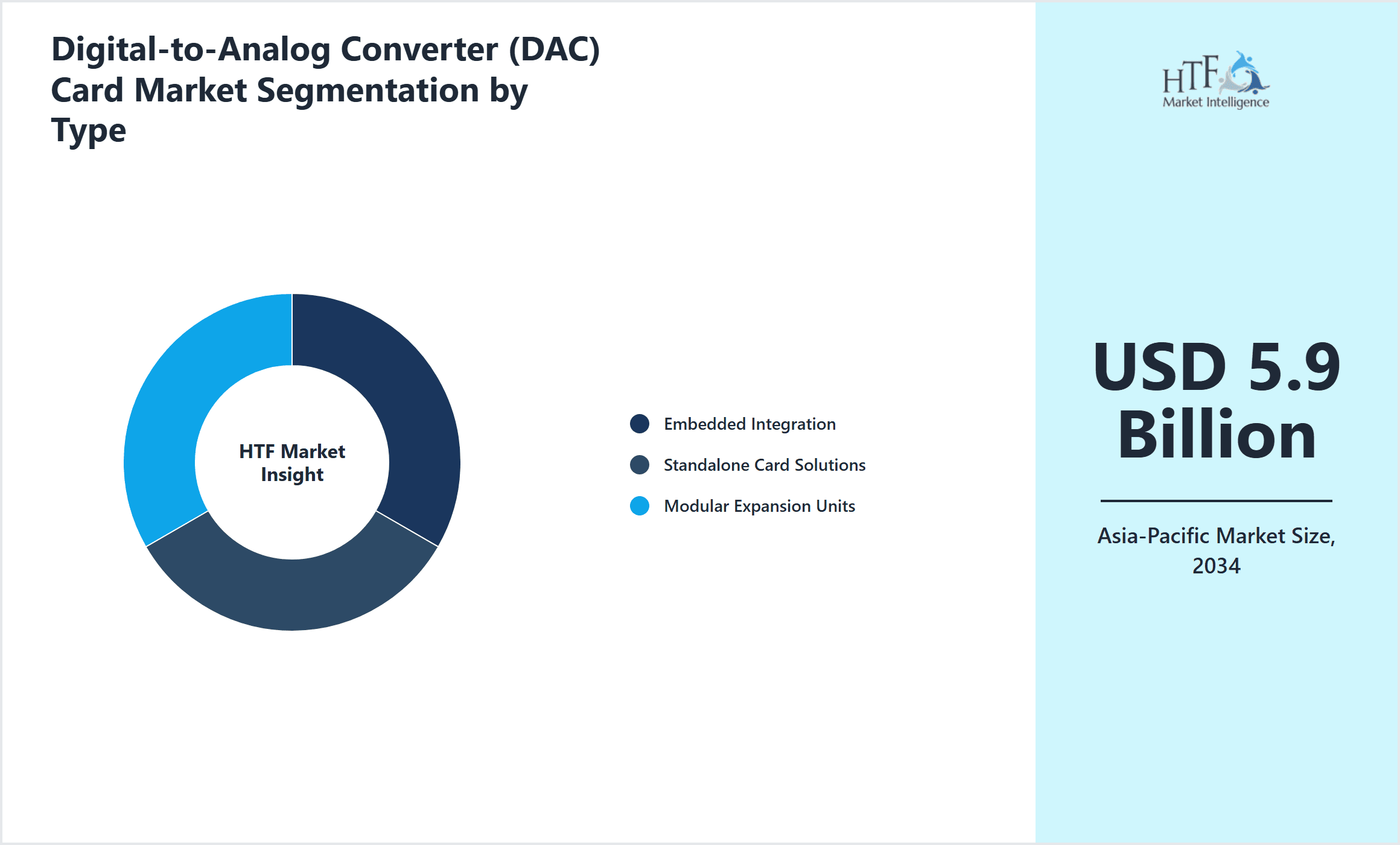

Asia-Pacific Digital-to-Analog Converter Card Market is segmented by Digital-to-Analog Converter Card Type (High-Speed Digital-to-Analog Converter Cards, Low-Power Digital-to-Analog Converter Cards, Multi-Channel Digital-to-Analog Converter Cards, Integrated Digital-to-Analog Converter Solutions, Modular Digital-to-Analog Converter Cards), Application Segment (Broadcasting, Telecommunications, Industrial Automation, Consumer Electronics, Medical Devices), Deployment Model (Embedded Integration, Standalone Card Solutions, Modular Expansion Units), End-User Industry (Broadcast and Media Houses, Telecom Operators, Manufacturing Plants, Consumer Electronics Manufacturers, Healthcare Providers), and Geography (Japan, China, Southeast Asia, India, Australia, South Korea, Others)

Pricing

Report Overview

Executive Summary

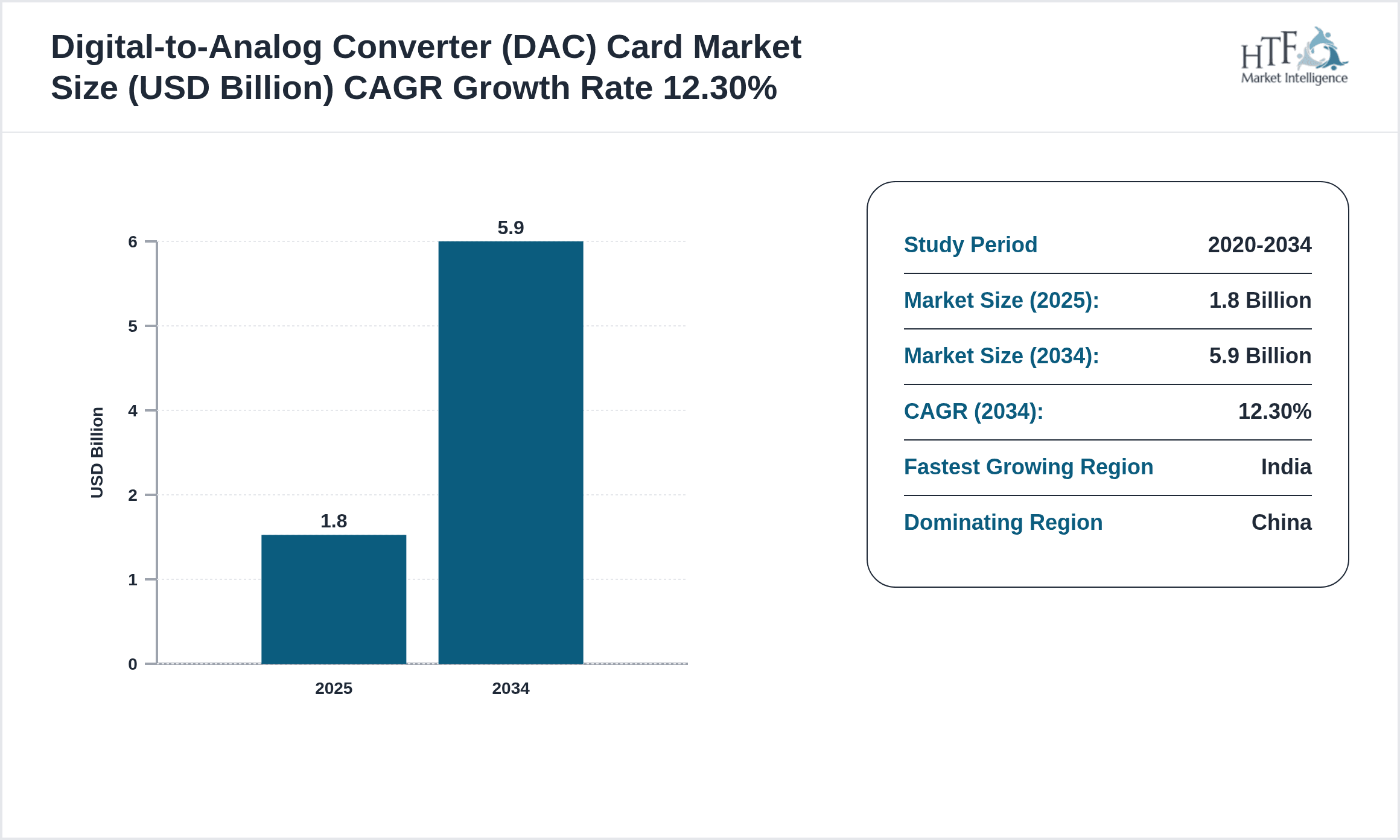

- •The Asia-Pacific Digital-to-Analog Converter (DAC) Card market consists of specialized electronic components that translate digital signals into analog formats necessary for various high-tech applications. This market spans several industries, including broadcasting, telecommunications, industrial automation, consumer electronics, and medical devices, where precise signal conversion is critical for device functionality and performance. Key product types include high-speed DAC cards designed for rapid signal processing, low-power cards for energy-sensitive uses, multi-channel configurations for simultaneous outputs, modular cards offering customization, and integrated solutions embedded in complex electronic systems. The market is driven by increasing demand for improved signal fidelity and efficiency in emerging technologies such as 5G communications and smart industrial equipment. Regional growth is supported by rapid industrialization, technological innovation, and expanding consumer electronics penetration. The Asia-Pacific DAC card market thus represents a vital segment of the broader electronics hardware ecosystem, offering significant value to manufacturers, OEMs, and end users alike.

- •Key highlights include a robust compound annual growth rate (CAGR) of 12.3% projected from 2024 to 2034, with market valuation expected to rise from USD 1.8 billion in 2024 to USD 5.9 billion by 2034. China dominates the regional landscape due to its extensive manufacturing infrastructure and R&D capabilities, while India is emerging as the fastest-growing market driven by expanding telecom and industrial sectors. High-speed DAC cards currently lead product types in market share, with modular DAC cards identified as the fastest-growing segment due to their flexibility in system design. Application-wise, broadcasting holds the largest share, supported by digital media proliferation, whereas medical devices and industrial automation are key growth areas. The market exhibits strong technological innovation, strategic partnerships, and increasing integration of DAC cards into next-generation electronics platforms.

- •The Asia-Pacific DAC card market offers strategic importance across multiple industries by enabling critical digital-to-analog signal conversion that supports enhanced performance, reliability, and precision. For stakeholders such as component manufacturers, system integrators, and technology developers, this market represents significant opportunities for innovation and growth. The expanding adoption of IoT, 5G networks, and smart manufacturing technologies further amplifies the demand for advanced DAC solutions tailored to diverse application requirements. Additionally, government initiatives to boost electronics manufacturing and technology R&D in countries like China, India, and South Korea enhance the market’s attractiveness. Consequently, the Asia-Pacific DAC card market is positioned as a dynamic and vital segment with ongoing evolution driven by technological advancements, competitive dynamics, and increasing end-user demand across broadcast, telecom, industrial, consumer, and medical sectors.

Competitive Landscape

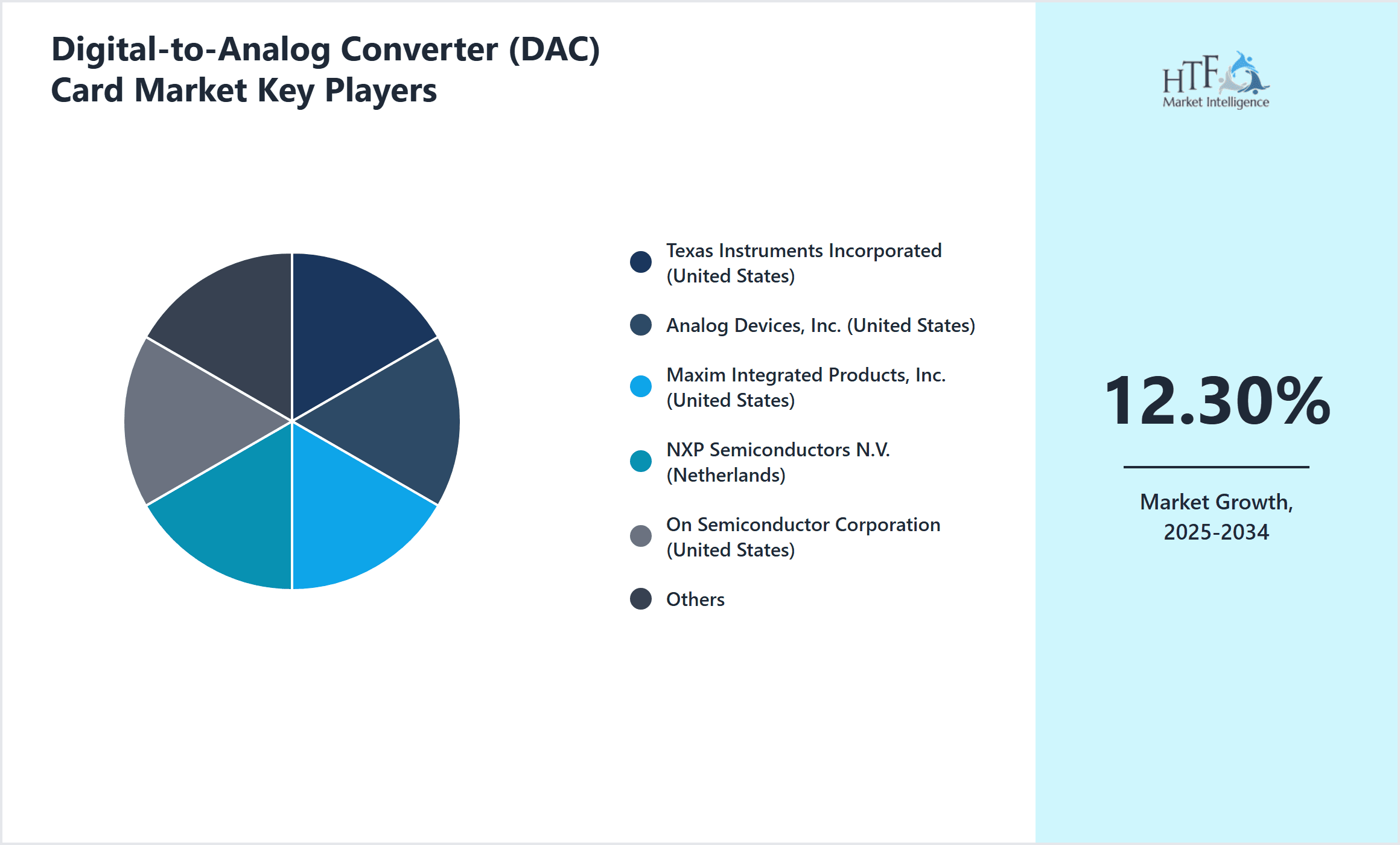

The competitive environment in the Asia-Pacific Digital-to-Analog Converter Card market is marked by intense rivalry among global technology leaders and regional manufacturers. Companies compete through continuous innovation in product speed, power efficiency, and modularity to address diverse application demands. Strategic partnerships and collaborations with system integrators enable enhanced market penetration and customization. Innovation approaches focus on integrating DAC cards with advanced semiconductor technologies such as CMOS and SiGe to improve performance metrics. Market players also leverage geographical advantages by establishing manufacturing hubs in technology clusters across China, South Korea, and India. Pricing strategies balance cost competitiveness with value-added features, while distribution channels include direct sales, OEM partnerships, and specialized electronics distributors. Market entry barriers include high R&D costs and stringent quality requirements, which favor established players but also encourage startups with niche technological expertise. Looking forward, competition is expected to intensify with emerging technologies influencing product evolution and customer preferences.

Prominent Players in Digital-to-Analog Converter Card Market

- •Texas Instruments Incorporated (United States)

- •Analog Devices, Inc. (United States)

- •Maxim Integrated Products, Inc. (United States)

- •NXP Semiconductors N.V. (Netherlands)

- •On Semiconductor Corporation (United States)

- •Renesas Electronics Corporation (Japan)

- •Broadcom Inc. (United States)

- •Rohm Co., Ltd. (Japan)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Infineon Technologies AG (Germany)

- •Cirrus Logic, Inc. (United States)

- •Analogic Corporation (United States)

- •Microchip Technology Inc. (United States)

- •Arrow Electronics, Inc. (United States)

- •Vishay Intertechnology, Inc. (United States)

- •STMicroelectronics N.V. (Switzerland)

- •Toshiba Corporation (Japan)

- •Skyworks Solutions, Inc. (United States)

- •ADI Global Distribution (United States)

- •Marvell Technology Group Ltd. (Bermuda)

- •Semtech Corporation (United States)

- •Cypress Semiconductor Corporation (United States)

- •Analog Devices Asia Pacific Pte Ltd (Singapore)

- •MediaTek Inc. (Taiwan)

- •Texas Instruments Asia Pacific Limited (Singapore)

Market Breakdown

- •By Digital-to-Analog Converter Card Type

- ◦High-Speed Digital-to-Analog Converter Cards

- ◦Low-Power Digital-to-Analog Converter Cards

- ◦Multi-Channel Digital-to-Analog Converter Cards

- ◦Integrated Digital-to-Analog Converter Solutions

- ◦Modular Digital-to-Analog Converter Cards

- •By Application Segment

- ◦Broadcasting

- ◦Telecommunications

- ◦Industrial Automation

- ◦Consumer Electronics

- ◦Medical Devices

- •By Deployment Model

- ◦Embedded Integration

- ◦Standalone Card Solutions

- ◦Modular Expansion Units

- •By End-User Industry

- ◦Broadcast and Media Houses

- ◦Telecom Operators

- ◦Manufacturing Plants

- ◦Consumer Electronics Manufacturers

- ◦Healthcare Providers

Growth Dynamics

- •The Asia-Pacific Digital-to-Analog Converter Card market is propelled by rapid adoption of 5G and next-generation telecommunications technologies requiring high-speed signal conversion. Enhanced broadcasting demand for high-definition audio and video content further accelerates market growth. Additionally, the surge in industrial automation and smart manufacturing initiatives boosts the need for precise DAC solutions. Consumer electronics expansion, including smart devices and wearables, drives demand for low-power and modular DAC cards. Government policies promoting electronics manufacturing and technology R&D in countries like China and India provide a supportive ecosystem. Together, these factors contribute to a sustained double-digit CAGR, creating significant opportunities for manufacturers and technology providers to innovate and capture growing market segments.

- •Trends in the Asia-Pacific DAC card market include increasing integration of DAC functionality within semiconductor chips to reduce size and power consumption. Modular DAC card designs enabling customizable and scalable solutions are gaining traction, particularly in industrial and medical sectors. The rise of IoT and connected devices is driving demand for DAC cards with enhanced precision and multi-channel capabilities. Sustainability considerations encourage development of energy-efficient DAC products, aligning with regional regulatory frameworks. Strategic collaborations between component manufacturers and system integrators foster faster product development cycles and tailored solutions for diverse application needs. These trends collectively push the market towards higher performance, flexibility, and environmental responsibility.

- •Market restraints include the high initial R&D investment required to develop advanced DAC card technologies, which can limit entry for smaller players. Supply chain disruptions, particularly in semiconductor components, can cause production delays and increased costs. Compatibility issues with legacy systems in certain industries may slow adoption of newer DAC card models. Additionally, pricing pressures from low-cost regional manufacturers challenge profit margins for premium product providers. Regulatory compliance complexities across diverse Asia-Pacific countries add to operational challenges. These factors collectively impose constraints on market growth and require strategic navigation by industry participants.

- •Opportunities abound in expanding applications such as medical imaging devices, where precise analog signal conversion is critical. The increasing use of DAC cards in autonomous vehicle systems and smart grid infrastructure offers new growth avenues. Emerging markets within Southeast Asia present untapped demand for cost-effective and scalable DAC solutions. Advances in semiconductor manufacturing, such as the adoption of silicon photonics and advanced packaging, enable more efficient DAC card designs. Partnerships with telecom operators upgrading to 5G and 6G networks provide strategic entry points. Additionally, government incentives supporting digital infrastructure development across Asia-Pacific enhance market prospects for innovative DAC card technologies.

- •Challenges include managing the rapid pace of technological change requiring continual product innovation and upgrades. Intense competition from global and regional players drives the need for differentiation through performance and cost optimization. Navigating diverse regulatory environments across Asia-Pacific countries demands robust compliance strategies. Supply chain vulnerabilities, exacerbated by geopolitical tensions and semiconductor shortages, affect timely production. Furthermore, educating end-users on the benefits and technical nuances of advanced DAC cards remains essential to drive adoption. Addressing these challenges requires strategic investments in R&D, supply chain resilience, and customer engagement.

Market Trends

- •The Asia-Pacific DAC card market is witnessing a shift towards integration of multi-channel capabilities within single cards, enabling simultaneous processing of multiple signal streams. This trend supports complex industrial automation and broadcasting needs, enhancing system efficiency and reducing hardware footprint.

- •Increased adoption of low-power DAC cards aligns with rising demand for energy-efficient consumer electronics and IoT devices, facilitating longer battery life and reduced environmental impact without compromising performance.

- •Modular DAC card architectures are gaining prominence, offering flexibility in configuration and scalability, which appeals to diverse application requirements in medical devices and telecommunications infrastructure.

- •Sustainability and eco-friendly product design are becoming key focus areas, with manufacturers investing in reducing hazardous materials and improving recyclability of DAC card components to meet stringent regional regulations.

- •Collaborations and strategic partnerships between DAC card manufacturers and system integrators enhance customization capabilities and accelerate time-to-market for tailored solutions across vertical industries.

- •Consumer preference for high-definition multimedia content drives demand for high-speed DAC cards capable of supporting ultra-high fidelity audio and video signal conversion.

- •Emerging IoT deployments and smart city initiatives fuel demand for DAC cards with enhanced precision and reliability, supporting sensor networks and connected infrastructure applications.

Market Opportunities

- •Expanding telecom infrastructure upgrades in India and Southeast Asia present significant opportunities for DAC card manufacturers to supply high-speed and modular solutions tailored to 5G and future 6G networks.

- •Growth in medical diagnostics and imaging equipment in Asia-Pacific demands DAC cards with superior precision and reliability, creating avenues for specialized product development and market penetration.

- •The rise of autonomous vehicles and smart transportation systems opens opportunities for DAC cards enabling real-time signal processing in automotive electronics and sensor fusion applications.

- •Increasing adoption of Industry 4.0 and smart manufacturing in China and Japan drives demand for integrated and multi-channel DAC cards, facilitating precise control and monitoring in automated production lines.

- •Emerging economies within Asia-Pacific represent untapped markets for cost-effective DAC card solutions, with potential for growth through localized manufacturing and distribution partnerships.

- •Advancements in semiconductor packaging and materials science enable development of more compact and efficient DAC cards, offering product differentiation and competitive advantage.

- •Government initiatives supporting digital transformation and electronics innovation provide financial incentives and regulatory support to accelerate DAC card market expansion.

Market Challenges

- •The Asia-Pacific DAC card market faces challenges in maintaining rapid innovation cycles required to keep pace with evolving application demands and technology standards, necessitating sustained R&D investment.

- •Supply chain disruptions, particularly in semiconductor materials and components, pose risks to production schedules and cost management, impacting market stability and growth potential.

- •Diverse regulatory frameworks across Asia-Pacific countries create complexities in product certification, safety compliance, and environmental standards, increasing operational hurdles for manufacturers.

- •Pricing pressures from emerging low-cost regional competitors challenge profit margins of established players, compelling focus on cost optimization without compromising quality and innovation.

- •Customer education and awareness regarding advanced DAC card technologies remain limited in certain emerging markets, slowing adoption rates and market penetration.

- •Intense competition necessitates differentiation through continuous product enhancements, strategic partnerships, and superior customer service to maintain market share.

- •Geopolitical tensions and trade restrictions in the Asia-Pacific region may impact cross-border supply chains and technology transfer, affecting market dynamics.

Regulatory Framework

- •Between 2019 and 2024, Asia-Pacific countries have implemented stringent electronic product safety standards requiring DAC card manufacturers to comply with electromagnetic compatibility (EMC) and radio frequency interference (RFI) norms. These regulations ensure minimal disruption to other electronic devices and safeguard user environments.

- •Environmental compliance regulations, including restrictions on hazardous substances (RoHS) and waste electrical and electronic equipment (WEEE) directives, have been adopted across major Asia-Pacific markets such as China, Japan, and South Korea. These mandates require manufacturers to minimize toxic materials and promote recycling programs.

- •Data security and privacy regulations in telecommunications sectors influence DAC card design, especially for cards integrated into network infrastructure, mandating secure data handling and encryption capabilities.

- •Country-specific mandates on electronic component certification, such as the China Compulsory Certification (CCC) and Japan’s PSE mark, have been enforced to ensure product quality and safety, impacting market entry and distribution.

- •Government initiatives promoting domestic electronics manufacturing, including subsidies and tax incentives, encourage local production of DAC cards, fostering market growth while imposing adherence to national standards and reporting requirements.

Market Intelligence

- •15th January 2024, Texas Instruments Incorporated launched a new series of high-speed digital-to-analog converter cards designed for 5G infrastructure applications. These cards feature enhanced signal fidelity and low latency, targeting telecom operators in Asia-Pacific. The product launch aims to support the region’s rapid 5G rollout and next-generation network demands, offering scalable solutions adaptable to various base station configurations. Texas Instruments emphasized the cards’ low power consumption and robust thermal management, critical for dense urban deployments. This innovation strengthens TI’s competitive position in the Asia-Pacific DAC card market by addressing both performance and reliability requirements. Source: Company Press Release

- •22nd September 2023, Renesas Electronics Corporation introduced modular digital-to-analog converter cards tailored for industrial automation systems. The new product line offers flexible channel configurations and seamless integration with existing control architectures. Renesas highlighted the cards’ high precision and durability under harsh environmental conditions, catering to Asia-Pacific’s expanding smart manufacturing sector. This strategic launch supports Renesas’ objective to deepen market penetration in Asia’s industrial electronics space by providing adaptive and scalable DAC solutions. The initiative aligns with rising automation trends and government incentives fostering Industry 4.0 adoption. Source: Industry Publication

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, India is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Japan

- China

- Southeast Asia

- India

- Australia

- South Korea

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 5.9 Billion |

| CAGR | 12.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.4% |

| Scope of Report | Market is segmented by Digital-to-Analog Converter Card Type (High-Speed Digital-to-Analog Converter Cards, Low-Power Digital-to-Analog Converter Cards, Multi-Channel Digital-to-Analog Converter Cards, Integrated Digital-to-Analog Converter Solutions, Modular Digital-to-Analog Converter Cards), Application Segment (Broadcasting, Telecommunications, Industrial Automation, Consumer Electronics, Medical Devices), Deployment Model (Embedded Integration, Standalone Card Solutions, Modular Expansion Units), End-User Industry (Broadcast and Media Houses, Telecom Operators, Manufacturing Plants, Consumer Electronics Manufacturers, Healthcare Providers) |

| Regions Covered | Japan, China, Southeast Asia, India, Australia, South Korea, Others |

| Key Companies | Texas Instruments Incorporated (United States), Analog Devices, Inc. (United States), Maxim Integrated Products, Inc. (United States), NXP Semiconductors N.V. (Netherlands), On Semiconductor Corporation (United States) |

Asia-Pacific Digital-to-Analog Converter Card Market Scope & Changing Dynamics 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.