Global Pest Control Software Market Size, Growth & Revenue 2025-2034

Global Pest Control Software Market is segmented by Type (Cloud-based Pest Control Software, On-premise Pest Control Software, Hybrid Pest Control Software), Application (Residential Pest Control, Commercial Pest Control, Industrial Pest Control, Agricultural Pest Control, Government Pest Control Programs), Deployment Model (Mobile Application, Web-based Platform, Desktop Software), Service Type (Scheduling & Dispatch, Reporting & Analytics, Compliance Management, Customer Relationship Management), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Pest Control Software market integrates advanced digital platforms designed to facilitate efficient pest management across multiple sectors including residential, commercial, industrial, agricultural, and government applications. These software solutions offer comprehensive tools for scheduling, monitoring, reporting, compliance management, and analytics, enabling pest control operators to optimize workflows and improve service quality. The solutions leverage cloud computing, mobile technologies, and hybrid deployment models to provide scalable, real-time access to operational data. Growing concerns over health and environmental safety, along with increasing regulatory requirements, drive adoption of these software platforms worldwide, ensuring timely and effective pest control interventions. The market's scope extends to integration with IoT devices and AI-powered analytics, enhancing predictive pest management capabilities and enabling data-driven decision-making. This facilitates proactive infestation prevention, resource optimization, and improved customer satisfaction across diverse geographic regions and application sectors.

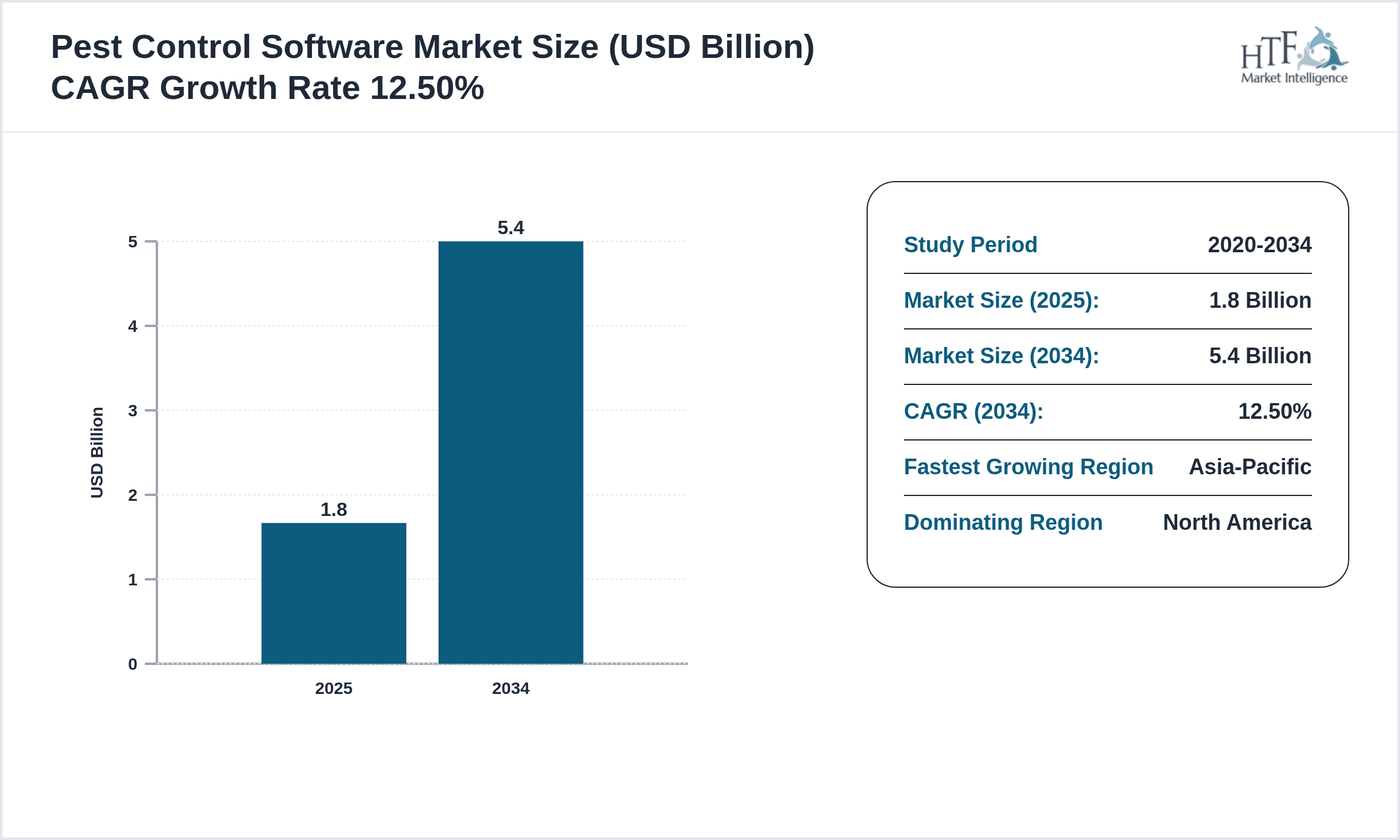

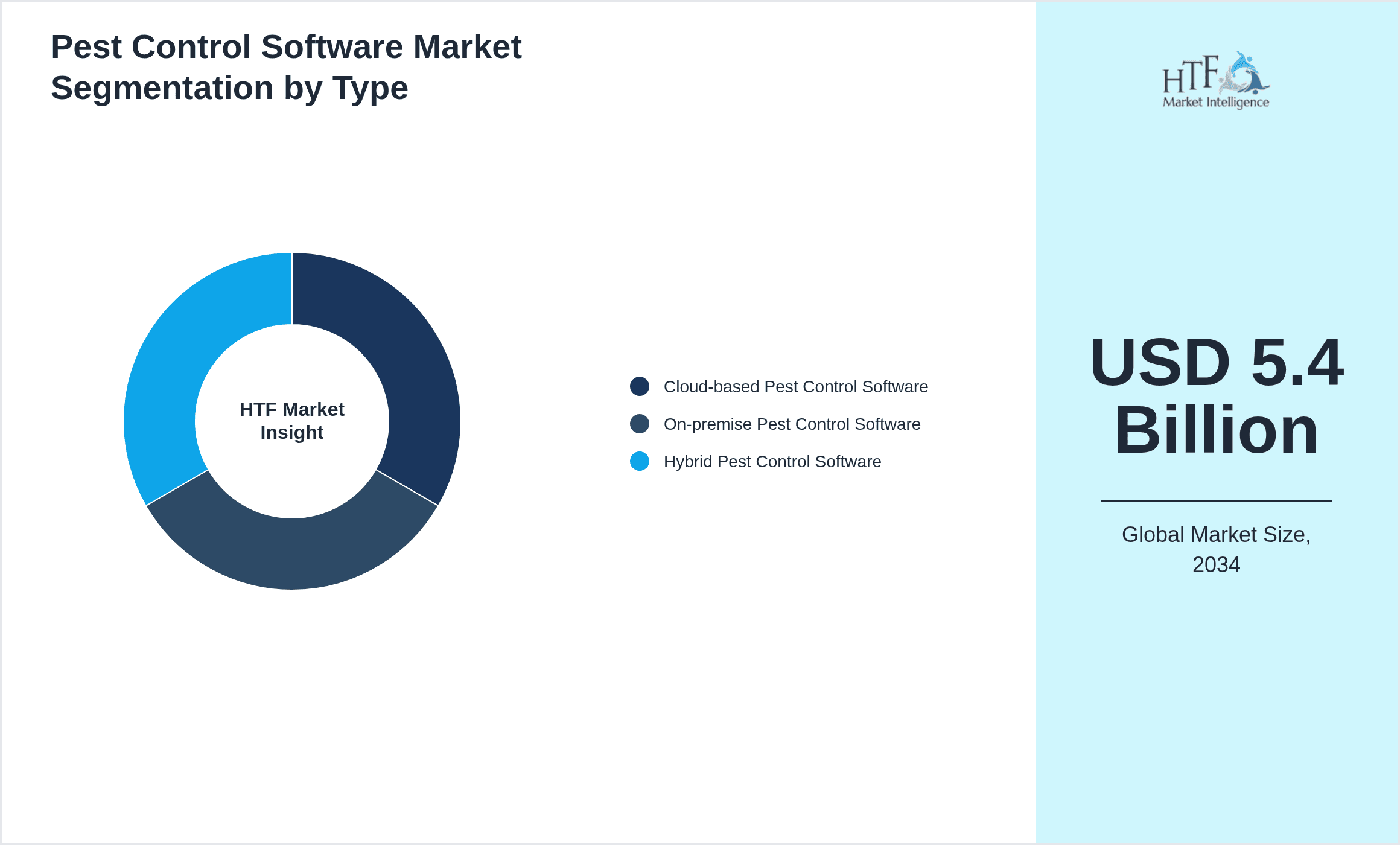

- •Key highlights of the global Pest Control Software market include a robust base market size of USD 1.8 Billion in 2025, growing at a CAGR of 12.5% to reach USD 5.4 Billion by 2034. North America dominates the market with the largest share driven by high technology adoption and stringent regulatory frameworks. Asia-Pacific exhibits the fastest growth fueled by increasing urbanization and rising awareness about pest-related health hazards. Cloud-based solutions lead the product type segment due to their scalability and ease of access, while hybrid models demonstrate the fastest growth rate attributable to their flexibility and security benefits. Residential and commercial applications account for the majority of market consumption, reflecting the broad applicability of pest control software across various end-use sectors globally.

- •Pest Control Software provides strategic value to pest management companies, agricultural businesses, healthcare institutions, and government agencies by enabling efficient operational management, regulatory compliance, and customer engagement. The technology-driven approach reduces manual errors, enhances real-time monitoring, and facilitates predictive analytics, resulting in better resource utilization and cost savings. The market's expansion is further supported by increasing investments in smart city initiatives, IoT integration, and digital transformation across industries. As the global population grows and urbanizes, demand for effective pest control solutions intensifies, positioning Pest Control Software as a critical tool for sustainable pest management and public health protection worldwide.

Competitive Landscape

The competitive landscape of the global Pest Control Software market is characterized by dynamic strategies including technological innovation, strategic partnerships, and global expansion initiatives. Leading companies focus on continuous product enhancements incorporating AI, machine learning, and IoT integration to improve predictive pest management and operational efficiency. Companies actively pursue partnerships with hardware providers and agricultural firms to broaden their solution portfolios and penetrate new markets. Geographic expansion into emerging economies within Asia-Pacific and Latin America leverages local partnerships and customized offerings. Strategic acquisitions enable consolidation of technology and customer base, strengthening market position. Pricing strategies emphasize subscription-based models with scalable features to cater to diverse customer segments. Distribution channels increasingly utilize digital platforms, enhancing accessibility and customer service. The adoption of cloud and hybrid deployment models reflects the industry’s focus on flexibility and data security, sustaining competitive advantages. Future trends indicate a shift towards comprehensive ecosystem development integrating pest control software with broader smart city and agricultural technology platforms.

Key Participants in Pest Control Software Market

- •ServiceTitan (United States)

- •Fieldwork (United States)

- •PestRoutes (United States)

- •WorkWave (United States)

- •Jobber (Canada)

- •PestPac (United States)

- •BMS (United States)

- •Rentokil Initial (United Kingdom)

- •Terminix (United States)

- •Orkin (United States)

- •Rollins Inc. (United States)

- •MTech Systems (United States)

- •Spraymate (Australia)

- •PestWizard (Australia)

- •PestScan (United States)

- •FieldEdge (United States)

- •Zerorez (United States)

- •Flybrix (United States)

- •ProActive Pest Control Software (United States)

- •Ecomedes (United States)

Market Breakdown

- •By Type

- ◦Cloud-based Pest Control Software

- ◦On-premise Pest Control Software

- ◦Hybrid Pest Control Software

- •By Application

- ◦Residential Pest Control

- ◦Commercial Pest Control

- ◦Industrial Pest Control

- ◦Agricultural Pest Control

- ◦Government Pest Control Programs

- •By Deployment Model

- ◦Mobile Application

- ◦Web-based Platform

- ◦Desktop Software

- •By Service Type

- ◦Scheduling & Dispatch

- ◦Reporting & Analytics

- ◦Compliance Management

- ◦Customer Relationship Management

Growth Dynamics

Rapid urbanization and increased awareness of pest-related health risks drive demand for efficient pest control software globally. Real-time monitoring capabilities integrated with IoT devices enable proactive pest management, reducing infestation risks and operational costs. For instance, in 2024, WorkWave expanded its cloud-based platform incorporating AI-driven analytics to enhance predictive pest control accuracy, significantly improving client retention. Regulatory mandates across North America and Europe enforcing compliance with environmental and safety standards boost software adoption to streamline reporting processes. Moreover, the transition from manual to digital pest control operations increases productivity and service quality. Emerging markets in Asia-Pacific exhibit accelerated growth due to rising investments in smart city frameworks and agricultural modernization. The integration of mobile applications facilitates field technician coordination and customer engagement, optimizing resource allocation. Overall, technological advancements, regulatory pressures, and growing urban populations collectively propel market expansion, with companies focusing on innovation and geographic diversification to capitalize on these drivers.

Market Trends

Digital transformation is reshaping the Pest Control Software market with increasing adoption of AI and machine learning to predict pest outbreaks and optimize treatment schedules, minimizing chemical usage. The shift towards cloud-based solutions offers scalability and remote access, supporting pandemic-induced remote work trends. Integration of IoT sensors and drones enables precise environmental monitoring, as demonstrated by PestRoutes’ 2025 launch of a drone-assisted pest surveillance module enhancing data collection accuracy. Sustainability emerges as a key trend with software facilitating eco-friendly pest control methods and compliance with green regulations. Additionally, subscription-based pricing models gain traction, enabling small and medium enterprises to access advanced tools affordably. Strategic collaborations between software providers and agritech companies foster innovation in agricultural pest management. The expansion of mobile platforms improves field operations and customer interactions, further driving software adoption. These trends collectively transform pest control from reactive to predictive and sustainable, creating long-term value for stakeholders.

Market Opportunities

Emerging economies in Asia-Pacific and Latin America present substantial growth opportunities due to increasing urbanization, rising disposable incomes, and expanding commercial infrastructures demanding effective pest control solutions. The agricultural sector’s digitalization offers prospects for integrating pest control software with precision farming technologies, enhancing crop yield and reducing chemical dependency. Recent initiatives in smart city development incorporate pest management within broader environmental monitoring systems, enabling software providers to offer integrated platforms. The growing emphasis on sustainability and regulatory compliance drives demand for advanced analytics and reporting features, opening avenues for innovation. Cloud migration and hybrid deployment models enable flexible adoption across diverse customer segments, including small enterprises. Strategic partnerships with IoT device manufacturers and agritech firms facilitate development of comprehensive pest control ecosystems. Additionally, expanding service offerings to government pest management programs and public health organizations further diversify revenue streams. These opportunities encourage market players to invest in R&D, geographic expansion, and customized solutions to capture untapped potential globally.

Market Challenges

Data security and privacy concerns pose significant challenges as pest control software increasingly relies on cloud and hybrid platforms storing sensitive operational and customer data. Integration complexities with legacy systems hinder seamless adoption, particularly among small and medium enterprises lacking IT infrastructure. High initial implementation costs and subscription fees can restrict market penetration in cost-sensitive regions. Variations in regulatory frameworks across countries complicate compliance management and require continuous software updates, increasing operational burdens on providers. Additionally, resistance to digital transformation within traditional pest control businesses slows adoption rates. The fragmented nature of the pest control industry with numerous small operators challenges uniform software deployment. Recent reports highlight difficulties encountered by companies in Asia-Pacific due to inadequate digital literacy and infrastructure variability. Moreover, competition from generic field service management software limits specialized pest control software growth. Addressing these challenges requires focused investment in user-friendly interfaces, cybersecurity measures, and localized solutions to enhance acceptance and compliance.

Regulatory Framework

The global Pest Control Software market operates under diverse regulatory frameworks emphasizing environmental safety, data privacy, and pest control compliance. Since 2020, the European Union’s General Data Protection Regulation enforces stringent data handling and privacy standards applicable to software providers managing customer and operational data. North American regulations, including the U.S. Environmental Protection Agency’s mandates, require detailed pest control reporting and adherence to chemical usage protocols, compelling software solutions to incorporate compliance management features. Emerging regulations in Asia-Pacific focus on sustainable pest management practices and digital record-keeping to support government monitoring programs. Software developers continuously update platforms to align with these evolving regulations, ensuring operational legality and market acceptance. Industry certifications and standards such as ISO 27001 for information security further influence software design and deployment. These regulatory frameworks collectively enhance market trust, drive innovation, and necessitate ongoing compliance efforts from market participants.

Market Intelligence

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Source: Official company announcements, Industry publications, Regulatory filings

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 5.4 Billion |

| CAGR | 12.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.5% |

| Scope of Report | Market is segmented by Type (Cloud-based Pest Control Software, On-premise Pest Control Software, Hybrid Pest Control Software), Application (Residential Pest Control, Commercial Pest Control, Industrial Pest Control, Agricultural Pest Control, Government Pest Control Programs), Deployment Model (Mobile Application, Web-based Platform, Desktop Software), Service Type (Scheduling & Dispatch, Reporting & Analytics, Compliance Management, Customer Relationship Management) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Emerging economies in Asia-Pacific and Latin America present substantial growth opportunities due to increasing urbanization, rising disposable incomes, and expanding commercial infrastructures demanding effective pest control solutions. The agricultural sector’s digitalization offers prospects for integrating pest control software with precision farming technologies, enhancing crop yield and reducing chemical dependency. Recent initiatives in smart city development incorporate pest management within broader environmental monitoring systems, enabling software providers to offer integrated platforms. The growing emphasis on sustainability and regulatory compliance drives demand for advanced analytics and reporting features, opening avenues for innovation. Cloud migration and hybrid deployment models enable flexible adoption across diverse customer segments, including small enterprises. Strategic partnerships with IoT device manufacturers and agritech firms facilitate development of comprehensive pest control ecosystems. Additionally, expanding service offerings to government pest management programs and public health organizations further diversify revenue streams. These opportunities encourage market players to invest in R&D, geographic expansion, and customized solutions to capture untapped potential globally. |

Global Pest Control Software Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.