Global Premium Gin Market - Outlook 2020-2034

Global Premium Gin Market is segmented by Premium Gin Type (London Dry Gin, Old Tom Gin, Plymouth Gin, Navy Strength Gin, Contemporary Gin), Premium Gin Application (Cocktails, Neat Consumption, Culinary Use, Mixology, Gifts), Distribution Channel (On-Trade (Bars and Restaurants), Off-Trade (Retail and Online), Duty-Free, Direct-to-Consumer), Packaging Format (Glass Bottles, Limited Edition Packaging, Gift Sets), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global premium gin market is defined by the production and consumption of high-quality gin products crafted using superior botanicals and advanced distillation techniques. This market covers a broad spectrum of product types, including London Dry, Old Tom, Plymouth, Navy Strength, and Contemporary gins, each catering to distinct consumer tastes and occasions such as cocktails, neat consumption, culinary use, mixology, and gifting. The value chain extends from sourcing premium raw materials to distillation, blending, packaging, marketing, and distribution across various channels including bars, restaurants, specialty retail, and e-commerce platforms. Increasing consumer inclination towards artisanal and craft spirits, coupled with rising disposable incomes and sophisticated cocktail culture globally, drives demand. Additionally, innovation in flavor profiles and packaging, alongside emerging markets in Asia-Pacific and Latin America, expand the market footprint. The market is poised for robust growth influenced by evolving consumer preferences, premiumization trends, and strategic brand collaborations, making premium gin a critical segment within the global spirits industry.

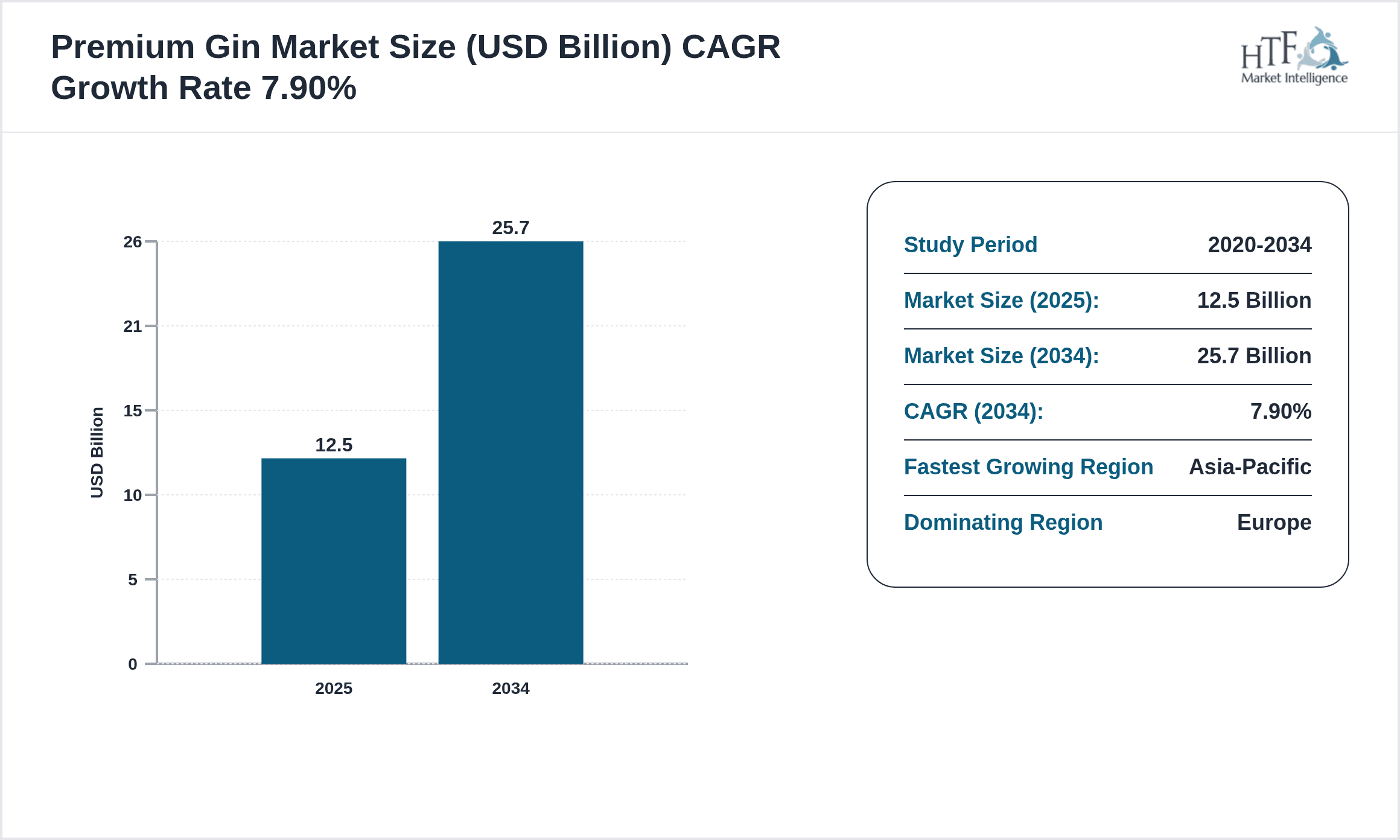

- •Key highlights of the premium gin market include a 7.9% CAGR forecast from 2025 to 2034, with the market size expected to more than double from USD 12.5 billion in 2025 to USD 25.7 billion by 2034. Europe currently dominates the market, driven by strong heritage brands and mature consumer bases, while Asia-Pacific is the fastest growing region, fueled by expanding middle-class populations and increasing cocktail culture adoption. London Dry Gin remains the leading product type due to its classic profile and widespread consumer acceptance, whereas Navy Strength Gin is emerging as the fastest growing segment owing to its higher alcohol content appealing to adventurous consumers. Year-on-year growth rates average 7.6%, reflecting steady demand and innovation momentum across product lines and regions.

- •The premium gin market holds strategic importance for distillers, distributors, hospitality sectors, and investors due to its expanding consumer base and premiumization trend. The segment offers value through brand differentiation, innovative product offerings, and premium pricing strategies. Its growth is also propelled by increasing consumer interest in craft and artisanal spirits, which supports sustained investment in R&D, marketing, and distribution infrastructure. For stakeholders, understanding regional preferences, evolving consumer behaviors, and regulatory frameworks is essential to capitalize on emerging opportunities and navigate market challenges effectively.

Competitive Landscape

The global premium gin market exhibits a highly competitive landscape characterized by a mix of heritage brands and innovative craft distilleries. Market dynamics are shaped by strategic collaborations, product innovation, and aggressive marketing campaigns focusing on brand heritage, quality, and unique flavor profiles. Companies adopt diversified strategies including premiumization, geographic expansion, and sustainability initiatives to differentiate offerings. Innovation in packaging and limited-edition releases further enhance consumer engagement. Pricing strategies vary, with premium and super-premium segments commanding higher margins. Distribution channels encompass on-trade, off-trade, and direct-to-consumer platforms, each offering specific competitive advantages. Barriers to entry include stringent regulatory compliance, high production costs, and brand loyalty. Regional competition varies, with Europe leading in brand heritage and North America and Asia-Pacific driving growth through new product launches and expanding consumer bases. Future trends indicate increased consolidation through mergers and acquisitions, digital marketing penetration, and focus on sustainability to gain competitive advantage.

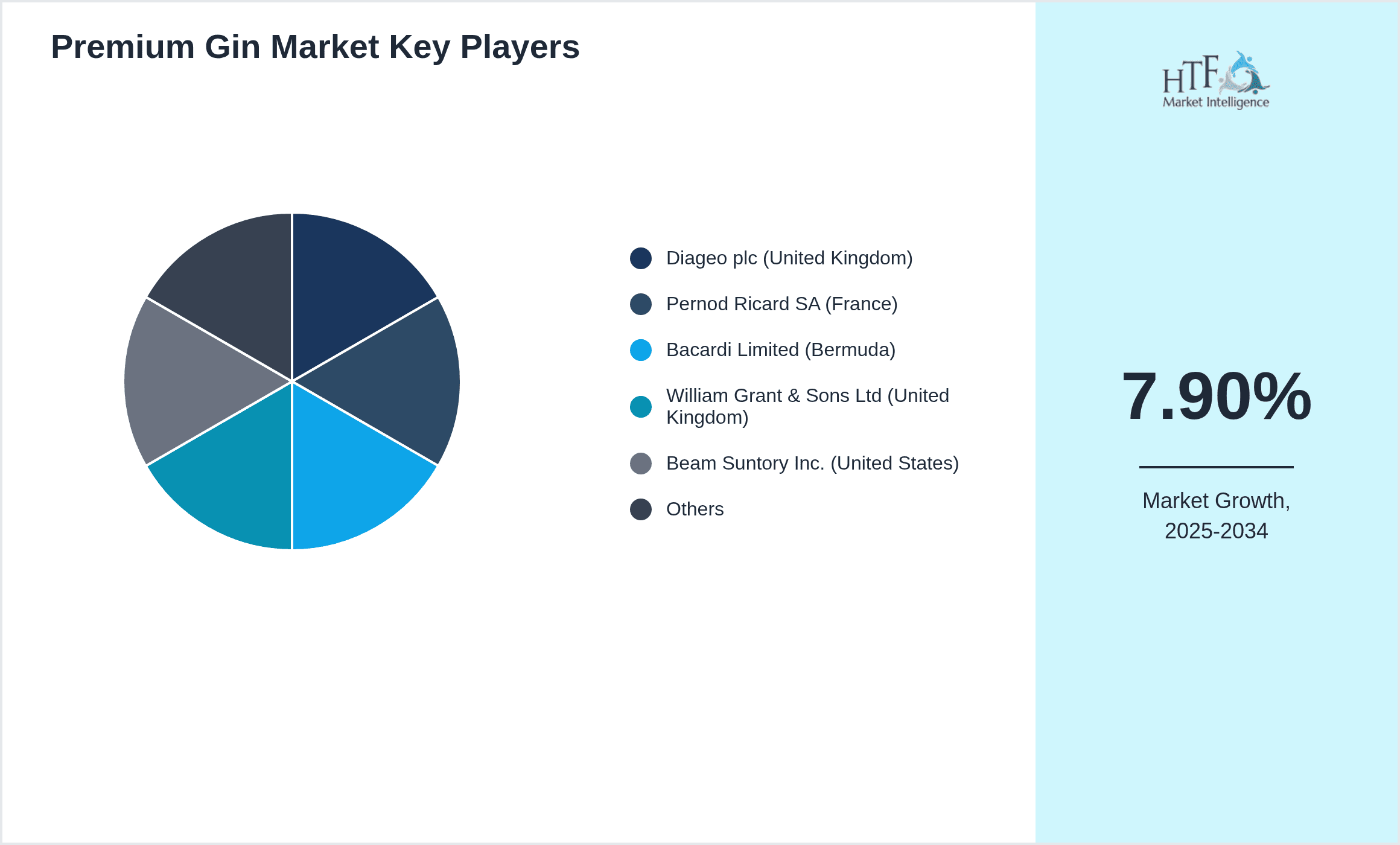

Prominent Players in Premium Gin Market

- •Diageo plc (United Kingdom)

- •Pernod Ricard SA (France)

- •Bacardi Limited (Bermuda)

- •William Grant & Sons Ltd (United Kingdom)

- •Beam Suntory Inc. (United States)

- •Suntory Holdings Limited (Japan)

- •Campari Group (Italy)

- •Brown-Forman Corporation (United States)

- •Hendrick's Gin (Scotland)

- •Gordon's (United Kingdom)

- •Tanqueray (United Kingdom)

- •Bombay Sapphire (United Kingdom)

- •Fever-Tree Ltd (United Kingdom)

- •Sipsmith (United Kingdom)

- •The Botanist (United Kingdom)

- •Monkey 47 (Germany)

- •Malfy Gin (Italy)

- •Roku Gin (Japan)

- •Elephant Gin (Germany)

- •Aviation American Gin (United States)

- •Strathearn Distillery (Scotland)

- •Four Pillars Gin (Australia)

- •Gin Mare (Spain)

- •Tanqueray No. Ten (United Kingdom)

- •Whitley Neill Gin (United Kingdom)

Market Breakdown

- •By Premium Gin Type

- ◦London Dry Gin

- ◦Old Tom Gin

- ◦Plymouth Gin

- ◦Navy Strength Gin

- ◦Contemporary Gin

- •By Premium Gin Application

- ◦Cocktails

- ◦Neat Consumption

- ◦Culinary Use

- ◦Mixology

- ◦Gifts

- •By Distribution Channel

- ◦On-Trade (Bars and Restaurants)

- ◦Off-Trade (Retail and Online)

- ◦Duty-Free

- ◦Direct-to-Consumer

- •By Packaging Format

- ◦Glass Bottles

- ◦Limited Edition Packaging

- ◦Gift Sets

Growth Dynamics

- •The rising consumer preference for premium and craft spirits is driving the global premium gin market growth. Increasing disposable income and urbanization in emerging economies fuel demand for luxury alcoholic beverages, supporting premium gin sales worldwide.

- •Expansion of cocktail culture and mixology trends globally encourages bars and restaurants to feature premium gin-based drinks, thereby boosting market penetration and introducing new consumer segments.

- •Innovation in botanical blends and flavor profiles by distillers is attracting consumers seeking unique sensory experiences, promoting product differentiation and brand loyalty in a competitive marketplace.

- •Growing e-commerce platforms and digital marketing strategies enable premium gin brands to reach broader audiences efficiently, lowering entry barriers and facilitating consumer engagement.

- •Sustainability initiatives and organic product offerings appeal to environmentally conscious consumers, providing growth avenues through responsible sourcing and production methods.

- •Collaborations between distilleries and hospitality sectors enhance brand visibility and consumer experience, driving demand through exclusive events and limited-edition releases.

- •Government regulations facilitating alcohol trade and relaxation of licensing norms in various regions contribute to improved market accessibility and expansion prospects.

Market Trends

- •Premium gin brands are increasingly incorporating exotic botanicals and locally sourced ingredients to create distinct flavor profiles, enhancing consumer appeal and regional differentiation.

- •The rise of low-alcohol and flavored premium gins caters to health-conscious consumers and expands market reach beyond traditional gin drinkers.

- •Sustainability trends motivate brands to adopt eco-friendly packaging and carbon-neutral production processes, responding to growing environmental concerns among consumers.

- •Digital engagement via social media and influencer marketing drives brand awareness and consumer interaction, particularly among younger demographics.

- •Limited edition and artisanal gin releases create exclusivity and drive collector interest, supporting premium pricing strategies and brand prestige.

- •Cross-category collaborations with luxury lifestyle brands and food pairings elevate premium gin positioning in the broader premium consumer market.

- •Increased adoption of online sales channels and direct-to-consumer models enhances convenience and personalized consumer experiences.

Market Opportunities

- •Emerging markets in Asia-Pacific and Latin America present significant growth potential due to rising middle-class populations and evolving drinking cultures favoring premium spirits.

- •Product innovation in flavored and organic premium gins addresses unmet consumer needs, opening new segments and enhancing market penetration.

- •Expansion of e-commerce and online retail channels offers opportunities for premium gin brands to reach untapped customers and innovate in digital marketing.

- •Strategic partnerships with hospitality and luxury lifestyle brands enable co-branding opportunities and experiential marketing to boost consumer engagement.

- •Sustainability certifications and eco-labeling can attract environmentally aware consumers, differentiating brands in a crowded marketplace.

- •Limited edition and collector’s series release strategies can drive exclusivity and higher margins while building brand loyalty.

- •Investment in emerging markets’ distribution infrastructure facilitates better market access and consumer reach, enhancing growth trajectory.

Market Challenges

- •Stringent alcohol regulations and varying tax regimes across global regions complicate market entry and increase compliance costs for premium gin producers.

- •High production and marketing costs associated with premium positioning can limit profitability, especially for smaller craft distilleries competing with established brands.

- •Intense competition from other premium spirits categories such as whiskey and vodka may restrict market share growth for premium gin segments.

- •Supply chain disruptions, including shortages of key botanicals and packaging materials, impact production consistency and cost structures.

- •Consumer skepticism regarding authenticity and quality claims requires brands to invest heavily in transparency and certification processes.

- •Changing consumer preferences and the rise of low-alcohol or non-alcoholic alternatives pose potential threats to traditional premium gin consumption patterns.

- •Limited awareness and penetration in certain emerging markets necessitate significant educational and promotional investments.

Regulatory Framework

- •Between 2020 and 2025, major regulatory frameworks such as the EU Spirits Regulation 2019 set stringent labeling, origin, and ingredient standards impacting premium gin classification and marketing practices.

- •In the United States, the Alcohol and Tobacco Tax and Trade Bureau (TTB) updated guidelines from 2021 to 2024 governing distillation processes and product claims to ensure authenticity and consumer transparency.

- •Several countries implemented stricter advertising and promotion laws for alcoholic beverages between 2020 and 2025, requiring compliance with responsible marketing codes and age restrictions.

- •Environmental regulations focusing on sustainable production and waste management emerged globally, with governments encouraging eco-friendly distillation and packaging practices.

- •Trade policies and tariffs affecting alcohol import-export fluctuated during 2020-2025, influencing premium gin pricing and market access in key regions such as Asia-Pacific and Europe.

Market Intelligence

- •15th January 2025, Diageo plc launched an innovative London Dry Gin variant incorporating rare botanicals sourced from sustainable farms in Europe. This new product line targets environmentally conscious consumers and premium cocktail enthusiasts, featuring a refined flavor profile and eco-friendly packaging. The launch is part of Diageo’s strategic initiative to lead sustainability in the spirits industry and expand its premium portfolio globally. The campaign includes collaborations with top mixologists and a digital marketing push across multiple regions to maximize consumer engagement. Source: Diageo official press release

- •10th March 2025, Pernod Ricard SA introduced a Navy Strength Gin with a unique blend of citrus and spice botanicals aimed at luxury consumers in Asia-Pacific and Europe. This launch leverages advanced distillation techniques to deliver a higher alcohol content without compromising smoothness, catering to adventurous drinkers seeking bold experiences. Pernod Ricard’s move is aligned with growing demand for distinctive premium spirits and positions the company competitively in emerging markets with rising cocktail culture adoption. Extensive promotional events and influencer partnerships support this product rollout. Source: Pernod Ricard corporate news

- •20th May 2025, Beam Suntory Inc. announced a strategic partnership with a leading e-commerce platform to enhance direct-to-consumer sales of its premium gin brands in North America and Europe. This initiative aims to capitalize on the accelerated shift towards online alcohol purchases, driven by consumer convenience and personalized shopping experiences. The partnership includes exclusive online product launches, virtual tasting events, and targeted digital advertising to increase brand visibility and market penetration. This collaboration is expected to significantly contribute to Beam Suntory’s revenue growth and customer base expansion. Source: Beam Suntory press release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Europe currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 25.7 Billion |

| CAGR | 7.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.6% |

| Scope of Report | Market is segmented by Premium Gin Type (London Dry Gin, Old Tom Gin, Plymouth Gin, Navy Strength Gin, Contemporary Gin), Premium Gin Application (Cocktails, Neat Consumption, Culinary Use, Mixology, Gifts), Distribution Channel (On-Trade (Bars and Restaurants), Off-Trade (Retail and Online), Duty-Free, Direct-to-Consumer), Packaging Format (Glass Bottles, Limited Edition Packaging, Gift Sets) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Diageo plc (United Kingdom), Pernod Ricard SA (France), Bacardi Limited (Bermuda), William Grant & Sons Ltd (United Kingdom), Beam Suntory Inc. (United States), Suntory Holdings Limited (Japan), Campari Group (Italy), Brown-Forman Corporation (United States), Hendrick's Gin (Scotland), Gordon's (United Kingdom), Tanqueray (United Kingdom), Bombay Sapphire (United Kingdom), Fever-Tree Ltd (United Kingdom), Sipsmith (United Kingdom), The Botanist (United Kingdom), Monkey 47 (Germany), Malfy Gin (Italy), Roku Gin (Japan), Elephant Gin (Germany), Aviation American Gin (United States), Strathearn Distillery (Scotland), Four Pillars Gin (Australia), Gin Mare (Spain), Tanqueray No. Ten (United Kingdom), Whitley Neill Gin (United Kingdom) |

Global Premium Gin Market - Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.