EMEA Stainless Steel Cookware Market - Outlook 2020-2034

EMEA Stainless Steel Cookware Market is segmented by Product Type (Tri-ply Stainless Steel Cookware, Copper Bottom Stainless Steel Cookware, Clad Stainless Steel Cookware, Electro-polished Stainless Steel Cookware, Mirror-finish Stainless Steel Cookware), Application (Home Cooking, Commercial Kitchens, Catering Services, Outdoor Cooking, Specialty Food Preparation), Surface Treatment (Polished Finish, Brushed Finish, Electro-polished Finish, Mirror Finish), Distribution Channel (Specialty Kitchenware Retailers, E-commerce Platforms, Department Stores, Wholesale Distributors), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Stainless Steel Cookware market defines a sector dedicated to the manufacture and supply of high-quality stainless steel cookware products tailored for diverse culinary applications in homes and professional settings. This market comprises a variety of product types such as tri-ply stainless steel, copper bottom, clad, electro-polished, and mirror-finish cookware, each engineered to meet specific cooking needs and preferences. Applications span home cooking, commercial kitchens, catering services, outdoor cooking, and specialty food preparation, representing a broad end-user base including households, hotels, restaurants, and catering firms. The value chain involves raw material extraction, processing, manufacturing, distribution, and retailing, with emphasis on innovation, durability, and design aesthetics. Market growth is stimulated by rising culinary trends, increasing disposable incomes, and growing awareness of health and sustainability, coupled with advancements in cookware technology that enhance cooking efficiency and user convenience. Key countries such as Germany, France, the United Kingdom, Italy, and Spain anchor market activities within the EMEA region, supported by regulatory frameworks, consumer preferences, and competitive dynamics shaping future opportunities.

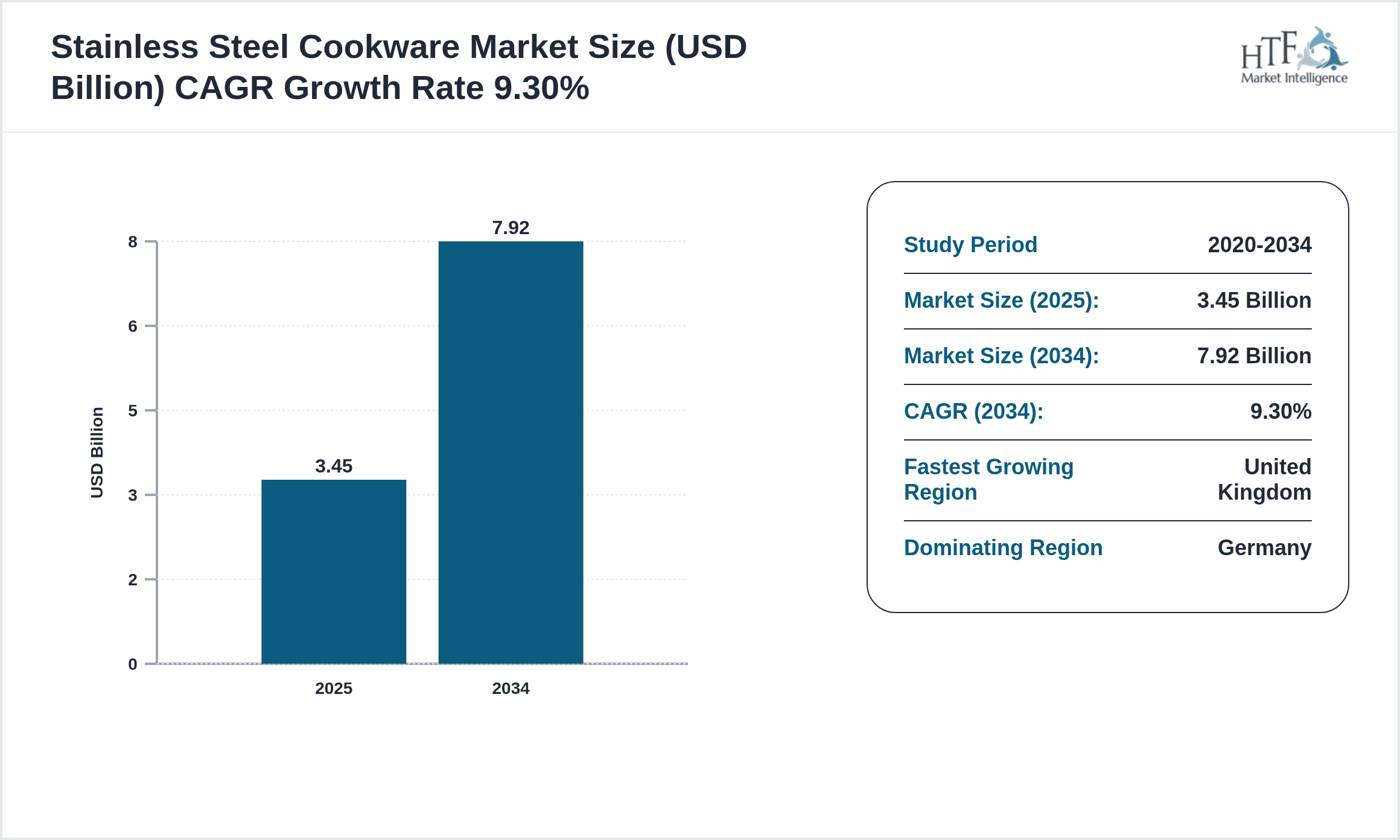

- •Market highlights include a base market size of USD 3.45 billion in 2025, expanding to an anticipated USD 7.92 billion by 2034, reflecting a compound annual growth rate (CAGR) of 9.3%. The market exhibits a year-on-year growth rate of 9.1%, driven by robust demand in both residential and commercial sectors. Tri-ply stainless steel cookware remains the leading product type due to its optimal heat distribution and durability, while electro-polished stainless steel cookware is identified as the fastest growing segment, attributable to its enhanced aesthetic appeal and corrosion resistance. Germany dominates the regional market in terms of revenue generation, whereas the United Kingdom is recognized as the fastest growing market, propelled by increasing demand for premium cookware and evolving culinary trends.

- •The value proposition of the EMEA stainless steel cookware market lies in delivering durable, efficient, and versatile cookware solutions that meet the evolving needs of various end-users. The market's strategic importance is underscored by its role in supporting food service industries, enhancing cooking experiences, and responding to sustainability imperatives through eco-friendly manufacturing practices. Stakeholders including manufacturers, distributors, retailers, and consumers benefit from ongoing innovation, premium product offerings, and expanding distribution networks. This market also offers investors opportunities for growth through technological advancements, brand differentiation, and expansion into emerging markets within the region.

Competitive Landscape

The competitive environment of the EMEA stainless steel cookware market is characterized by the presence of established global and regional players who leverage innovation, brand equity, and extensive distribution networks to maintain and expand their market positions. Market dynamics include aggressive product differentiation strategies focusing on advanced materials, superior heat conduction technologies, and ergonomic designs that cater to diverse consumer preferences. Companies emphasize sustainability by adopting eco-friendly manufacturing processes and recyclable materials, enhancing their appeal to environmentally conscious consumers. Strategic partnerships, mergers, and acquisitions continue to shape the competitive landscape, enabling firms to broaden their product portfolios, enter new markets, and optimize operational efficiencies. Pricing strategies are carefully devised to balance affordability with premium quality, addressing both mass-market and niche customer segments. Distribution channels encompass traditional retail, e-commerce platforms, and specialty kitchenware stores, with digital transformation playing a significant role in market penetration and customer engagement. Regional competition is influenced by varying consumer tastes and regulatory standards across countries in EMEA, prompting firms to customize offerings and comply with stringent quality and safety norms. Future competitive trends indicate increased investment in smart cookware technologies, enhanced customization options, and expansion into emerging markets within the region to sustain growth and profitability.

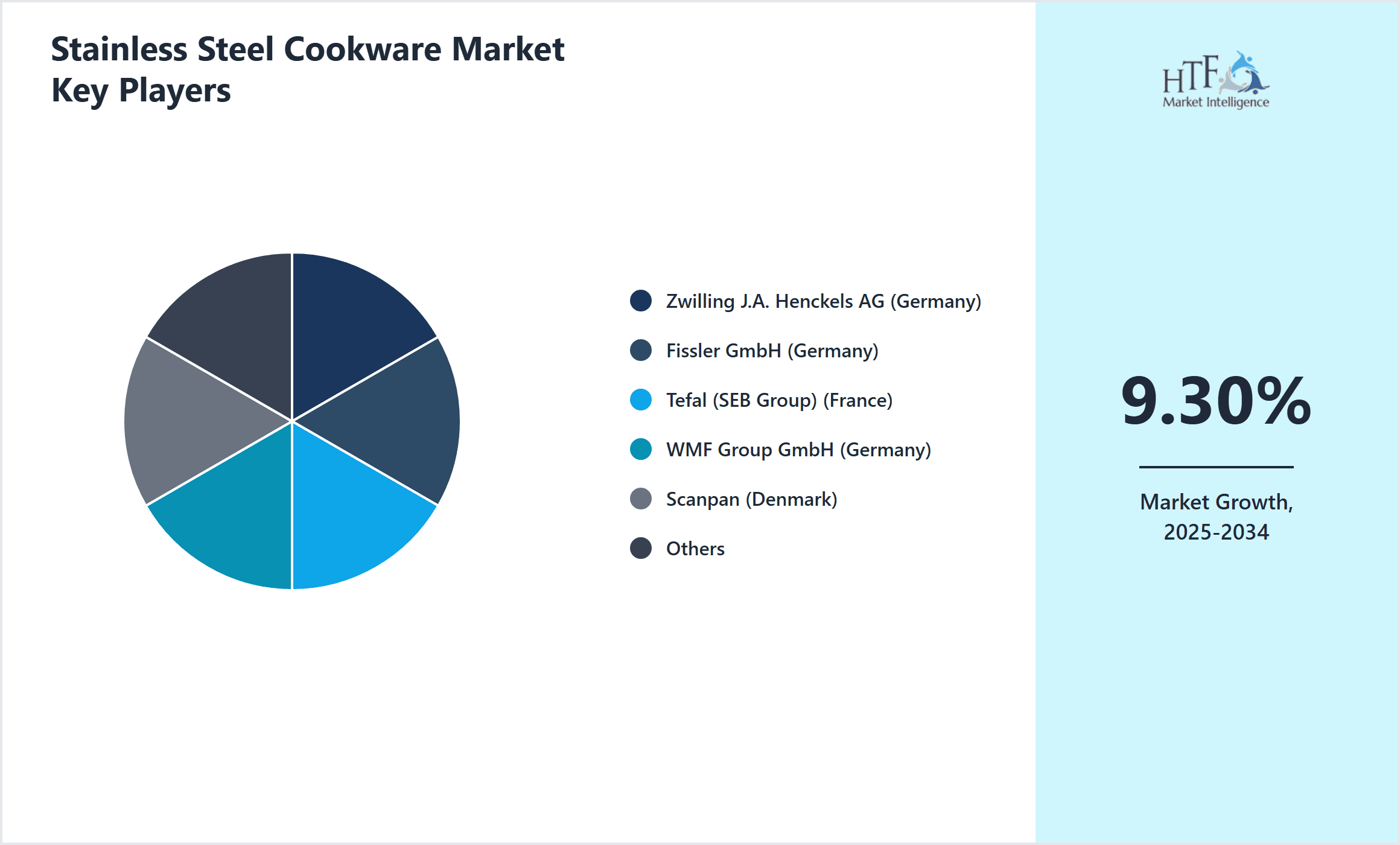

Leading Companies in Stainless Steel Cookware Market

- •Zwilling J.A. Henckels AG (Germany)

- •Fissler GmbH (Germany)

- •Tefal (SEB Group) (France)

- •WMF Group GmbH (Germany)

- •Scanpan (Denmark)

- •BekaertDeslee (Belgium)

- •Berndes (Germany)

- •Le Creuset (France)

- •Demeyere (Belgium)

- •All-Clad Metalcrafters LLC (United States)

- •Calphalon (Newell Brands) (United States)

- •Scanwood (United Kingdom)

- •Russell Hobbs (Spectrum Brands) (United Kingdom)

- •GreenPan (Belgium)

- •Silit (Germany)

- •Cristel (France)

- •Lodge Manufacturing Company (United States)

- •Anolon (Gibson Brands) (United States)

- •Lagostina (Italy)

- •Ballarini (Italy)

- •KitchenAid (Whirlpool Corporation) (United States)

- •Mauviel (France)

- •Cuisinart (Conair Corporation) (United States)

- •De Buyer (France)

- •Zwilling Gourmet (Germany)

Market Breakdown

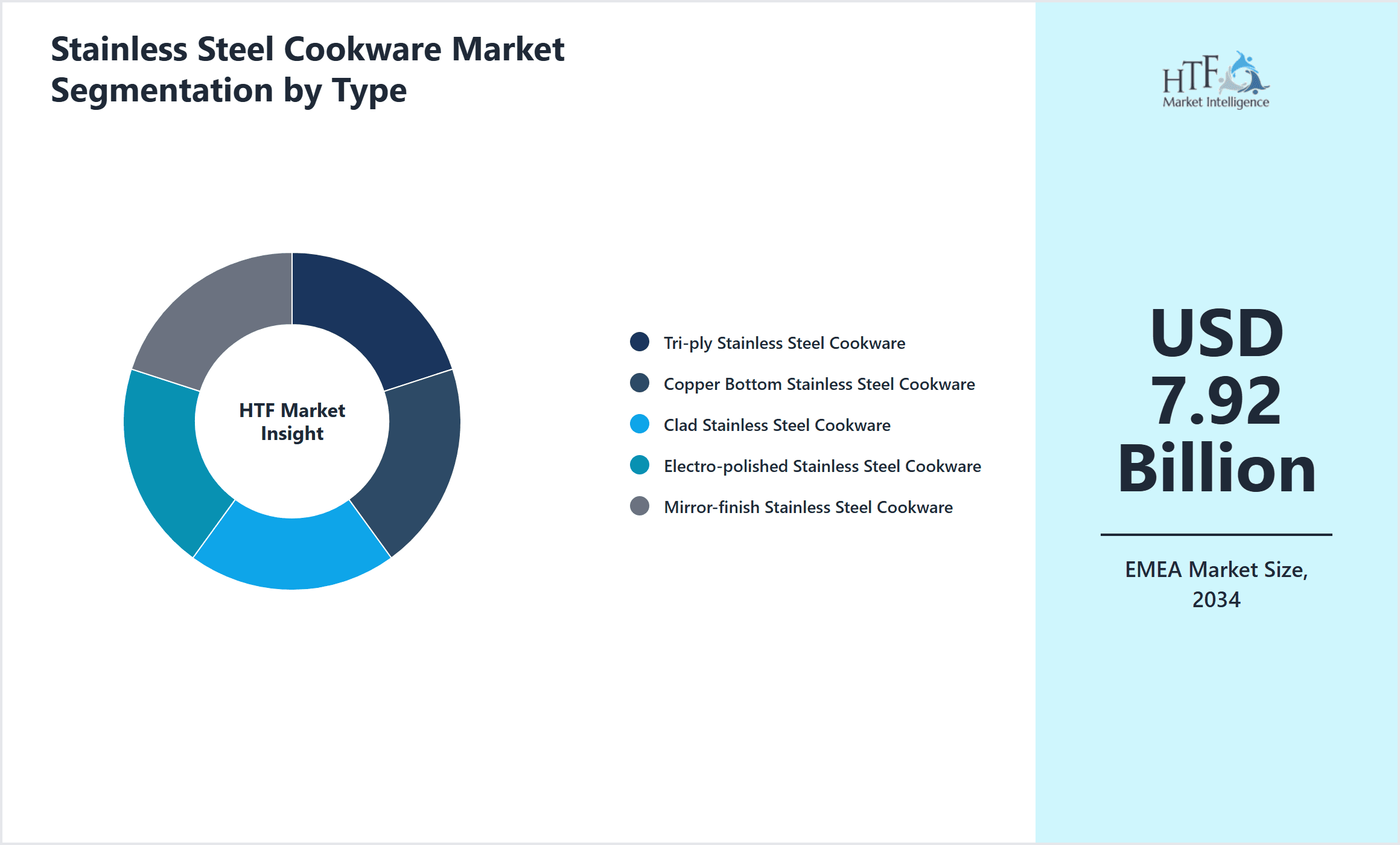

- •By Product Type

- ◦Tri-ply Stainless Steel Cookware

- ◦Copper Bottom Stainless Steel Cookware

- ◦Clad Stainless Steel Cookware

- ◦Electro-polished Stainless Steel Cookware

- ◦Mirror-finish Stainless Steel Cookware

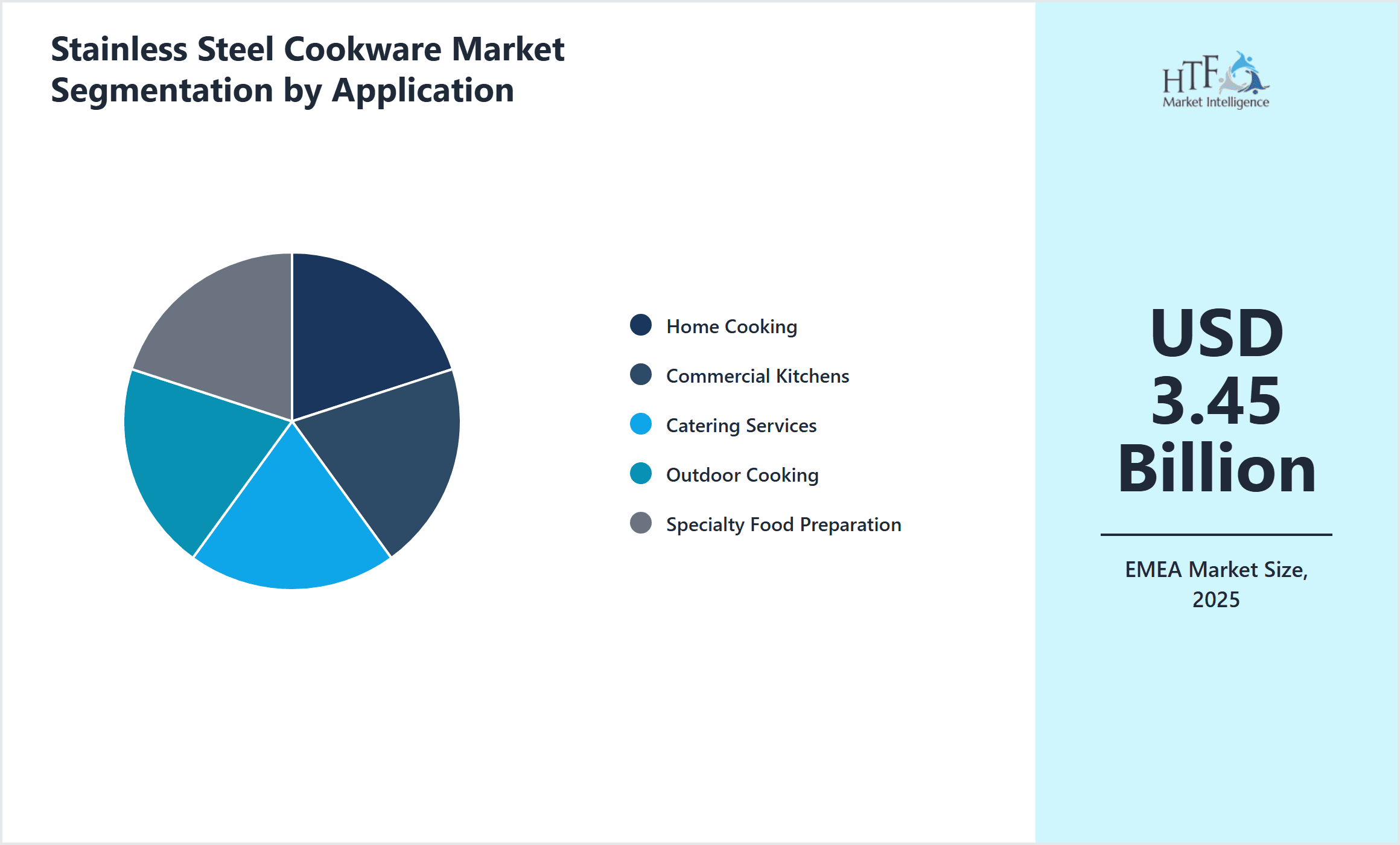

- •By Application

- ◦Home Cooking

- ◦Commercial Kitchens

- ◦Catering Services

- ◦Outdoor Cooking

- ◦Specialty Food Preparation

- •By Surface Treatment

- ◦Polished Finish

- ◦Brushed Finish

- ◦Electro-polished Finish

- ◦Mirror Finish

- •By Distribution Channel

- ◦Specialty Kitchenware Retailers

- ◦E-commerce Platforms

- ◦Department Stores

- ◦Wholesale Distributors

Growth Dynamics

- •Rising consumer preference for durable and health-safe cookware drives the market, as stainless steel offers corrosion resistance and non-reactive cooking surfaces, meeting modern cooking demands while ensuring food safety.

- •Increasing urbanization and disposable incomes in EMEA countries boost demand for premium cookware, with consumers seeking high-performance products for both domestic and professional use.

- •Technological advancements such as tri-ply construction and electro-polishing enhance cookware functionality and aesthetics, attracting a broader customer base and facilitating market expansion.

- •Growing awareness about sustainability and eco-friendly manufacturing encourages manufacturers to innovate with recyclable materials and energy-efficient production methods, appealing to environmentally conscious buyers.

- •Expanding foodservice industry and rising trend of gourmet cooking in hospitality sectors propel the commercial segment, increasing demand for specialized stainless steel cookware.

Market Trends

- •Adoption of multi-layered cookware technologies improves heat distribution and cooking efficiency, becoming a standard feature in premium product lines.

- •Integration of ergonomic designs and aesthetic enhancements like mirror finishes cater to evolving consumer preferences for both functionality and kitchen décor appeal.

- •E-commerce growth accelerates market reach, with consumers increasingly purchasing stainless steel cookware online due to convenience and wider product availability.

- •Sustainability-focused trends lead to increased use of recycled stainless steel and reduced packaging waste, aligning with global environmental directives.

Market Opportunities

- •Rising demand in emerging EMEA markets presents untapped potential for manufacturers to introduce mid-range and premium cookware products tailored to local tastes and budgets.

- •Innovation in smart cookware integrated with sensors and IoT technology offers avenues for product differentiation and enhanced consumer engagement.

- •Collaborations between cookware brands and culinary institutions can boost product endorsements and credibility, driving adoption among professional chefs and enthusiasts.

- •Expanding online retail infrastructure in EMEA enables manufacturers to reach broader audiences and implement direct-to-consumer models, improving margins and customer insights.

Market Challenges

- •High raw material costs and price volatility for stainless steel components limit profit margins and can affect product pricing strategies.

- •Intense competition from alternative cookware materials such as non-stick and cast iron poses a challenge to stainless steel cookware market penetration.

- •Complex regulatory compliance across multiple EMEA countries increases operational costs and delays market entry for new products.

- •Consumer preference fragmentation and brand loyalty fluctuations necessitate continuous innovation and marketing investments to sustain market share.

Regulatory Framework

- •Between 2020 and 2025, the EU Regulation on Food Contact Materials (EC) No 1935/2004 was rigorously enforced, requiring stainless steel cookware manufacturers to comply with strict safety and material migration limits, ensuring consumer protection and product quality.

- •The REACH regulation (Registration, Evaluation, Authorization and Restriction of Chemicals) updated in 2023 mandated stricter disclosure and use restrictions on certain chemicals used in cookware manufacturing, impacting raw material sourcing and production processes.

- •Germany’s national standards for kitchenware quality and environmental certifications introduced in 2021 require manufacturers to adhere to additional testing protocols, promoting sustainable production and product durability.

- •France implemented updated labeling requirements in 2024 to enhance transparency regarding cookware material composition and recyclability, influencing packaging and marketing strategies.

- •The EU’s Circular Economy Action Plan launched in 2020 encourages manufacturers to adopt eco-design principles and increase the use of recycled materials in stainless steel cookware to reduce environmental impact.

Market Intelligence

- •15th February 2025, Zwilling J.A. Henckels AG announced the launch of its new tri-ply stainless steel cookware series designed specifically for professional chefs and culinary enthusiasts in the EMEA region. The product line features enhanced thermal conductivity and ergonomic handles, targeting premium kitchenware markets in Germany and France. This initiative aligns with growing consumer demand for durable and high-performance cookware, aiming to consolidate Zwilling’s leadership in the region. The company also emphasized its commitment to sustainability by incorporating recycled stainless steel in manufacturing processes. Source: Zwilling Official Press Release

- •10th April 2025, Fissler GmbH introduced an innovative electro-polished stainless steel cookware range that combines superior corrosion resistance with modern aesthetics, tailored for upscale retail and e-commerce channels across Europe. The product integrates advanced surface treatment technology to ensure longevity and ease of cleaning, meeting consumer preferences for both functionality and style. Fissler’s strategic move targets expanding markets in the United Kingdom and Italy, where demand for premium cookware is rapidly increasing. This development is expected to strengthen the company’s market share amid intensifying competition. Source: Fissler Corporate News

- •5th June 2025, WMF Group GmbH completed the acquisition of a regional kitchenware manufacturer in Spain to enhance its product portfolio and distribution network within Southern Europe. This acquisition enables WMF to leverage local market knowledge and expand its reach in emerging segments such as outdoor cooking and catering services. The strategic consolidation is part of WMF’s broader growth plan focused on innovation, digital sales platforms, and sustainability initiatives, reinforcing its competitive position in the EMEA stainless steel cookware market. Source: WMF Investor Relations

- •20th August 2025, Tefal (SEB Group) launched a direct-to-consumer online platform dedicated to stainless steel cookware, offering customization options and exclusive product bundles for consumers across the EMEA region. The platform integrates augmented reality features to assist buyers in visualizing cookware in their kitchens, enhancing engagement and purchase confidence. This digital transformation aligns with increasing e-commerce trends and consumer demand for personalized products, positioning Tefal at the forefront of market innovation. Source: SEB Group Press Release

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Kingdom is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.45 Billion |

| Forecast Year Market Size | USD 7.92 Billion |

| CAGR | 9.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Scope of Report | Market is segmented by Product Type (Tri-ply Stainless Steel Cookware, Copper Bottom Stainless Steel Cookware, Clad Stainless Steel Cookware, Electro-polished Stainless Steel Cookware, Mirror-finish Stainless Steel Cookware), Application (Home Cooking, Commercial Kitchens, Catering Services, Outdoor Cooking, Specialty Food Preparation), Surface Treatment (Polished Finish, Brushed Finish, Electro-polished Finish, Mirror Finish), Distribution Channel (Specialty Kitchenware Retailers, E-commerce Platforms, Department Stores, Wholesale Distributors) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Zwilling J.A. Henckels AG (Germany), Fissler GmbH (Germany), Tefal (SEB Group) (France), WMF Group GmbH (Germany), Scanpan (Denmark) |

EMEA Stainless Steel Cookware Market - Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.