Global Commercial Auto Fleet Insurance Market Size, Growth & Revenue 2024-2034

Global Commercial Auto Fleet Insurance Market is segmented by Insurance Type (Liability Insurance, Physical Damage Insurance, Cargo Insurance, Comprehensive Insurance, Collision Insurance), Fleet Application (Long-Haul Transportation, Last-Mile Delivery, Service Fleets, Construction & Mining, Public Sector Fleets), Distribution Channel (Direct Sales, Insurance Brokers, Online Platforms, Agents and Intermediaries), Technology Adoption (Telematics-based Insurance, Usage-Based Insurance, Traditional Insurance, AI and Data Analytics Enabled Insurance), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global commercial auto fleet insurance market addresses the financial protection needs of businesses operating fleets of commercial vehicles across various sectors including logistics, construction, public services, and delivery. It covers a broad spectrum of insurance products such as liability, physical damage, cargo, comprehensive, and collision insurance, ensuring coverage against accidents, theft, cargo damage, and third-party claims. The market is driven by increasing fleet sizes worldwide, stringent regulatory requirements for commercial vehicles, and rising awareness regarding risk management. Additionally, the adoption of advanced technologies like telematics and usage-based insurance enhances risk assessment and premium calculation, contributing to market growth. The scope includes insurance providers offering tailored policies, claims management services, and risk mitigation solutions globally across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. This market is vital for mitigating operational risks and safeguarding asset investments of fleet operators, making it a cornerstone for the commercial transportation industry.

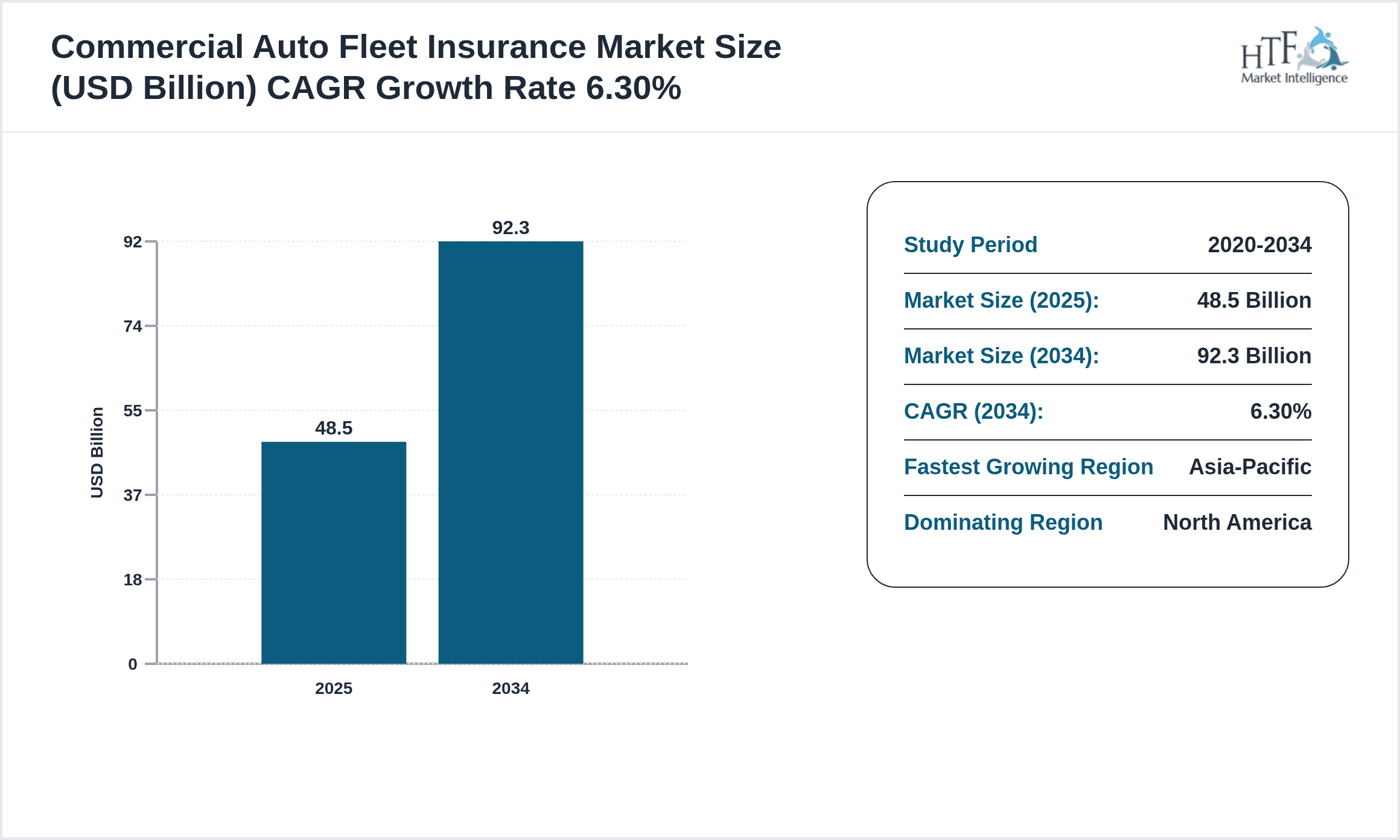

- •Key highlights of the commercial auto fleet insurance market include a projected CAGR of 6.3% from 2024 to 2034, with the market size expected to grow from USD 48.5 Billion in 2024 to USD 92.3 Billion by 2034. Liability insurance dominates the product segment due to regulatory requirements and high claim frequency, while cargo insurance is the fastest-growing segment driven by e-commerce expansion. North America holds the largest market share owing to mature insurance frameworks and extensive commercial fleet operations. Asia-Pacific is the fastest-growing region, fueled by rapid industrialization, urbanization, and increasing fleet adoption in emerging economies. The market is characterized by competitive innovation, strategic collaborations, and evolving insurance models influenced by digital transformation and data analytics.

- •The commercial auto fleet insurance market offers significant value propositions, including risk mitigation, financial security for businesses, and compliance with legal mandates. It enables fleet operators to safeguard against unpredictable losses, optimize insurance costs through technology-driven underwriting, and enhance operational resilience. Stakeholders such as insurers, fleet managers, and regulatory bodies benefit from improved risk visibility and claims efficiency. The strategic importance of this market is underscored by its role in supporting the global transportation and logistics infrastructure, ensuring continuity of services, and fostering sustainable commercial mobility. As fleets grow and evolve, insurance solutions adapt to meet emerging risks, making this market a critical component of the global commercial vehicle ecosystem.

Competitive Landscape

The competitive environment in the global commercial auto fleet insurance market is intense, characterized by the presence of multinational insurers, regional players, and niche specialists. Market participants leverage innovation in telematics, data analytics, and AI-driven underwriting to differentiate their offerings and improve risk assessment accuracy. Strategic partnerships with technology firms, fleet operators, and regulatory bodies enhance market positioning, fostering ecosystem collaboration and service integration. Rivalry centers on pricing strategies, coverage customization, claims handling efficiency, and digital platform capabilities. Mergers and acquisitions are common to consolidate market share and expand geographic reach. Additionally, emerging entrants introduce disruptive insurance models such as pay-as-you-drive and usage-based insurance, challenging traditional frameworks. The market's competitive dynamics are shaped by regulatory compliance, evolving customer expectations, and technological advancement, driving continuous innovation and strategic agility among players.

Prominent Players in Commercial Auto Fleet Insurance Market

- •Allianz SE (Germany)

- •AXA XL (France)

- •The Travelers Companies, Inc. (United States)

- •Zurich Insurance Group (Switzerland)

- •Chubb Limited (United States)

- •Berkshire Hathaway Inc. (United States)

- •Liberty Mutual Insurance (United States)

- •The Hanover Insurance Group (United States)

- •MAPFRE S.A. (Spain)

- •CNA Financial Corporation (United States)

- •Tokio Marine Holdings, Inc. (Japan)

- •MS&AD Insurance Group Holdings, Inc. (Japan)

- •Sompo Holdings, Inc. (Japan)

- •Hiscox Ltd (United Kingdom)

- •QBE Insurance Group Limited (Australia)

- •AXIS Capital Holdings Limited (Bermuda)

- •Hanwha General Insurance Co., Ltd. (South Korea)

- •RSA Insurance Group (United Kingdom)

- •Fairfax Financial Holdings Limited (Canada)

- •Sompo International Holdings Ltd. (Bermuda)

- •Mercury General Corporation (United States)

- •The Hartford Financial Services Group (United States)

- •The Progressive Corporation (United States)

- •W. R. Berkley Corporation (United States)

- •Allied World Assurance Company Holdings, AG (Switzerland)

Market Breakdown

- •By Insurance Type

- ◦Liability Insurance

- ◦Physical Damage Insurance

- ◦Cargo Insurance

- ◦Comprehensive Insurance

- ◦Collision Insurance

- •By Fleet Application

- ◦Long-Haul Transportation

- ◦Last-Mile Delivery

- ◦Service Fleets

- ◦Construction & Mining

- ◦Public Sector Fleets

- •By Distribution Channel

- ◦Direct Sales

- ◦Insurance Brokers

- ◦Online Platforms

- ◦Agents and Intermediaries

- •By Technology Adoption

- ◦Telematics-based Insurance

- ◦Usage-Based Insurance

- ◦Traditional Insurance

- ◦AI and Data Analytics Enabled Insurance

Growth Dynamics

- •The increasing size of commercial vehicle fleets globally, driven by rapid urbanization and e-commerce growth, is a primary growth driver for the commercial auto fleet insurance market. Larger fleets necessitate comprehensive insurance solutions to manage heightened exposure to risks and liabilities.

- •Technological advancements such as telematics and AI-powered risk assessment tools enable insurers to offer customized, usage-based insurance products, improving underwriting accuracy and customer satisfaction, thereby propelling market expansion.

- •Regulatory mandates enforcing compulsory commercial vehicle insurance across most countries have significantly boosted demand, ensuring compliance and protecting third parties, thereby expanding the insured fleet base.

- •The rise of green and electric commercial fleets introduces new risks and insurance requirements, encouraging innovation in product offerings and creating new market segments for insurers to explore.

- •Strategic partnerships between insurers, fleet management companies, and technology providers facilitate integrated solutions that streamline claims processing and risk management, enhancing market attractiveness and growth prospects.

Market Trends

- •The adoption of telematics and IoT devices in commercial vehicles is increasingly prevalent, allowing real-time monitoring of driving behavior and vehicle health, which insurers use to tailor premiums and reduce fraudulent claims.

- •There is a growing shift towards usage-based insurance models, which assess risk dynamically based on actual vehicle usage, promoting fairness in premium pricing and encouraging safer driving practices among fleet operators.

- •Sustainability trends are influencing insurers to develop products that support electric and hybrid commercial fleets, including coverage for battery-related risks and infrastructure damage.

- •Digital platforms for policy management and claims processing are gaining traction, enhancing customer experience and operational efficiency within the commercial auto fleet insurance sector.

- •Insurers are increasingly incorporating AI and machine learning to predict risk patterns, optimize pricing strategies, and detect fraudulent claims, thereby improving profitability and service quality.

Market Opportunities

- •Emerging markets in Asia-Pacific and Latin America present substantial growth opportunities due to expanding logistics sectors and increasing regulatory enforcement of commercial vehicle insurance.

- •Innovation in telematics-driven insurance products offers avenues for insurers to differentiate offerings and penetrate price-sensitive segments with customized risk profiles.

- •The growing electric commercial vehicle segment demands specialized insurance products addressing unique risks such as battery degradation, offering potential for new product development.

- •Collaborations with fleet management and technology companies enable insurers to offer integrated risk management solutions, enhancing customer retention and expanding service portfolios.

- •Digital transformation initiatives present opportunities to streamline claims processing, reduce operational costs, and improve customer engagement through user-friendly digital interfaces.

Market Challenges

- •The complexity of underwriting heterogeneous fleets with diverse vehicle types and usage patterns poses significant challenges in risk assessment and premium setting for insurers.

- •High claim frequency and severity in certain fleet applications, such as construction and long-haul transport, increase loss ratios and pressure profitability margins.

- •Data privacy and cybersecurity concerns related to telematics and usage-based insurance hinder widespread adoption and can affect customer trust.

- •Regulatory discrepancies and varying insurance requirements across global regions complicate standardization of products and operational scalability for multinational insurers.

- •Intense competition and price sensitivity in mature markets drive pressures on premium rates, challenging insurers to balance competitiveness with sustainable underwriting practices.

Regulatory Framework

- •Between 2019 and 2024, numerous countries implemented stricter mandatory commercial auto insurance regulations focusing on minimum coverage limits and claims processing transparency, enhancing policyholder protection and market stability.

- •Data protection laws introduced during this period mandate secure handling of telematics and driver data, requiring insurers to comply with rigorous privacy standards and obtain explicit consent from fleet operators.

- •Environmental regulations encouraging the adoption of electric and hybrid commercial vehicles have led to the development of insurance guidelines specifically addressing these new vehicle types and associated risks.

- •Regional regulatory bodies have introduced frameworks to standardize insurance product disclosures, ensuring greater clarity and comparability across commercial fleet insurance offerings.

- •Government incentives and subsidies supporting fleet modernization and safety technology adoption indirectly influence insurance underwriting practices and premium structures.

Market Intelligence

- •15th January 2025, Allianz SE launched an advanced telematics-based insurance platform designed for commercial fleets, integrating AI-driven risk assessment and real-time monitoring capabilities. This innovative solution aims to reduce claims costs by enabling proactive risk mitigation and customized pricing models, targeting logistics and delivery fleet operators globally. Allianz's strategic focus on digital transformation strengthens its competitive positioning and aligns with increasing demand for usage-based insurance products in emerging markets. The platform supports multi-region compliance and offers scalable integration with fleet management systems, enhancing operational efficiency for clients. Source: Allianz Official Press Release

- •10th March 2025, AXA XL introduced a comprehensive cargo insurance product tailored for e-commerce and last-mile delivery fleets, featuring flexible coverage options and digital claim submission processes. This product leverages blockchain technology to enhance transparency and expedite claims settlement, addressing rising demand driven by global e-commerce growth. The launch signifies AXA XL's commitment to innovation and customer-centric solutions, expanding its portfolio to capture high-growth segments. The offering is currently available in North America, Europe, and Asia-Pacific, with plans for further geographic expansion. Source: AXA XL Corporate News

- •5th February 2025, Chubb Limited announced a strategic partnership with a leading fleet telematics provider to co-develop insurance products that integrate real-time data analytics for risk management. This collaboration enhances Chubb’s underwriting precision and enables dynamic premium adjustments based on driving behavior and vehicle usage. The initiative is part of Chubb’s digital strategy to cater to evolving fleet insurance needs and improve customer engagement. The partnership is expected to drive growth in Asia-Pacific and Latin America markets where telematics adoption is accelerating. Source: Chubb Press Release

- •20th April 2025, The Travelers Companies, Inc. completed the acquisition of a regional commercial auto fleet insurer specializing in electric vehicle coverage, expanding its product offerings in sustainable fleet insurance. This acquisition enhances Travelers’ capabilities in underwriting emerging risks associated with electric commercial vehicles and aligns with its sustainability goals. The expanded portfolio supports commercial fleets transitioning to green technologies, offering tailored risk solutions and value-added services. The transaction solidifies Travelers’ presence in North America and provides a foundation for future innovation in fleet insurance products. Source: Travelers Corporate Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 48.5 Billion |

| Forecast Year Market Size | USD 92.3 Billion |

| CAGR | 6.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.1% |

| Scope of Report | Market is segmented by Insurance Type (Liability Insurance, Physical Damage Insurance, Cargo Insurance, Comprehensive Insurance, Collision Insurance), Fleet Application (Long-Haul Transportation, Last-Mile Delivery, Service Fleets, Construction & Mining, Public Sector Fleets), Distribution Channel (Direct Sales, Insurance Brokers, Online Platforms, Agents and Intermediaries), Technology Adoption (Telematics-based Insurance, Usage-Based Insurance, Traditional Insurance, AI and Data Analytics Enabled Insurance) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Allianz SE (Germany), AXA XL (France), The Travelers Companies, Inc. (United States), Zurich Insurance Group (Switzerland), Chubb Limited (United States), Berkshire Hathaway Inc. (United States), Liberty Mutual Insurance (United States), The Hanover Insurance Group (United States), MAPFRE S.A. (Spain), CNA Financial Corporation (United States), Tokio Marine Holdings, Inc. (Japan), MS&AD Insurance Group Holdings, Inc. (Japan), Sompo Holdings, Inc. (Japan), Hiscox Ltd (United Kingdom), QBE Insurance Group Limited (Australia), AXIS Capital Holdings Limited (Bermuda), Hanwha General Insurance Co., Ltd. (South Korea), RSA Insurance Group (United Kingdom), Fairfax Financial Holdings Limited (Canada), Sompo International Holdings Ltd. (Bermuda), Mercury General Corporation (United States), The Hartford Financial Services Group (United States), The Progressive Corporation (United States), W. R. Berkley Corporation (United States), Allied World Assurance Company Holdings, AG (Switzerland) |

Global Commercial Auto Fleet Insurance Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.