EMEA Refined Coconut Oil Market - Outlook 2025-2034

EMEA Refined Coconut Oil Market is segmented by Refined Coconut Oil Type (Virgin Refined Coconut Oil, Bleached Coconut Oil, Deodorized Coconut Oil, Fractionated Coconut Oil, Organic Refined Coconut Oil), Application Sector (Food Industry, Cosmetics, Pharmaceuticals, Industrial Use, Others), Distribution Channel (Retail, Wholesale, Online, Direct Industrial Supply), Production Technology (Steam Refining, Chemical Refining, Physical Refining), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Refined Coconut Oil Market encompasses the processing and commercialization of various refined coconut oil types, including virgin refined, bleached, deodorized, fractionated, and organic variants. This market caters to a broad spectrum of applications such as the food industry, cosmetics, pharmaceuticals, and diverse industrial uses. The refining process enhances oil purity, stability, and sensory attributes, making it suitable for end-use products requiring high-quality coconut oil. The market scope extends across importation of raw materials, refining technologies, quality control standards, and distribution channels within Europe, the Middle East, and Africa. Key drivers include rising consumer awareness of health and wellness, increased demand for natural and organic personal care products, and expanding industrial applications in lubricants and biofuels. The market operates within a complex regulatory landscape emphasizing food safety, organic certification, and environmental sustainability. Strategic importance is underscored by the market’s contribution to local economies, supply chain diversification, and innovation in refining processes, positioning it as a vital segment within the broader edible oils and specialty fats industry in the EMEA region.

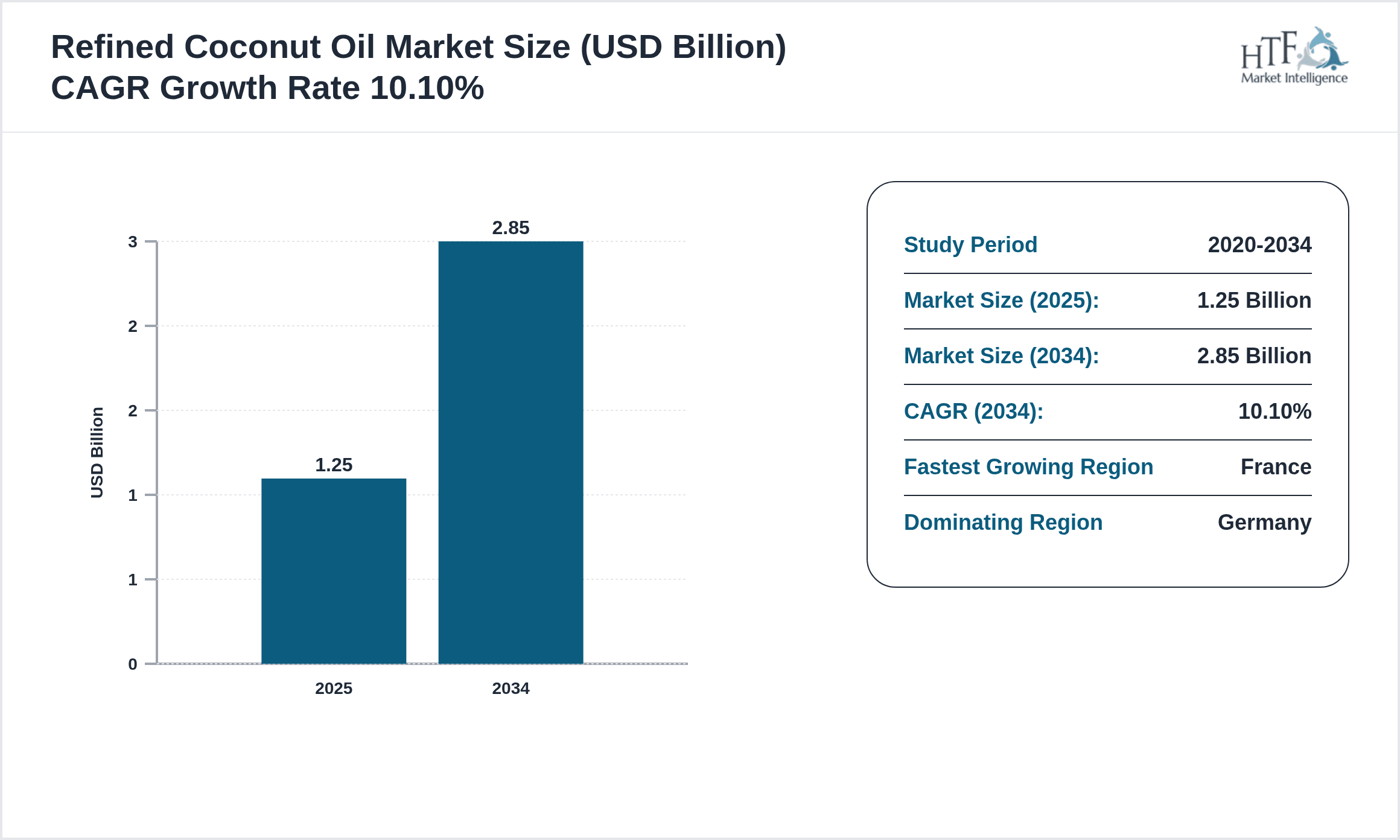

- •Significant highlights of the EMEA Refined Coconut Oil Market include a projected CAGR of 10.1% from 2025 to 2034, with the market size expected to grow from USD 1.25 billion to USD 2.85 billion. Virgin refined coconut oil holds the largest share, supported by its versatile use in food and personal care products. The cosmetics and pharmaceutical sectors exhibit robust growth, driven by consumer preference for natural ingredients. Germany dominates the market due to its advanced industrial infrastructure and consumer base, while France emerges as the fastest-growing country, propelled by increasing organic product demand. Market dynamics reveal a trend towards organic and fractionated oils, reflecting innovation and sustainability focus. These factors collectively position the market for sustained expansion and competitive innovation across EMEA.

- •The refined coconut oil market in EMEA offers strategic value to food manufacturers, cosmetics producers, pharmaceutical companies, and industrial users by supplying a high-quality, stable oil ingredient. Its refined variants enable product consistency, enhanced shelf life, and compliance with stringent quality standards. Stakeholders benefit from the expanding consumer interest in health-oriented and eco-friendly products, which fuels product development and market penetration. The regional market supports economic diversification through import and refining activities, fostering trade and employment. Additionally, the push for organic certification and green refining technologies aligns with global sustainability goals, enhancing brand equity and consumer loyalty across EMEA markets. Consequently, refined coconut oil is positioned as a crucial commodity within the evolving natural ingredient supply chain of the region.

Competitive Landscape

The EMEA refined coconut oil market exhibits a competitive landscape characterized by a mix of multinational corporations and regional players focusing on product innovation, quality enhancement, and sustainability. Market participants deploy diverse competitive strategies including strategic partnerships, capacity expansions, and technological advancements in refining processes to improve product purity and reduce environmental impact. Innovation centers on developing organic and fractionated variants to meet evolving consumer preferences and regulatory requirements. Rivalry is intensified by the entry of new players leveraging local sourcing and niche marketing, while established companies maintain dominance through brand equity and extensive distribution networks. Pricing strategies reflect raw material volatility and operational efficiencies, with premium positioning for organic and specialty oils. The market also experiences consolidation through mergers and acquisitions, which enhance scale and geographic reach. Distribution channels vary from direct industrial supply to retail-focused packaging, emphasizing omnichannel presence. Overall, competition drives continuous improvement in product offerings, regulatory compliance, and market responsiveness within the EMEA refined coconut oil sector.

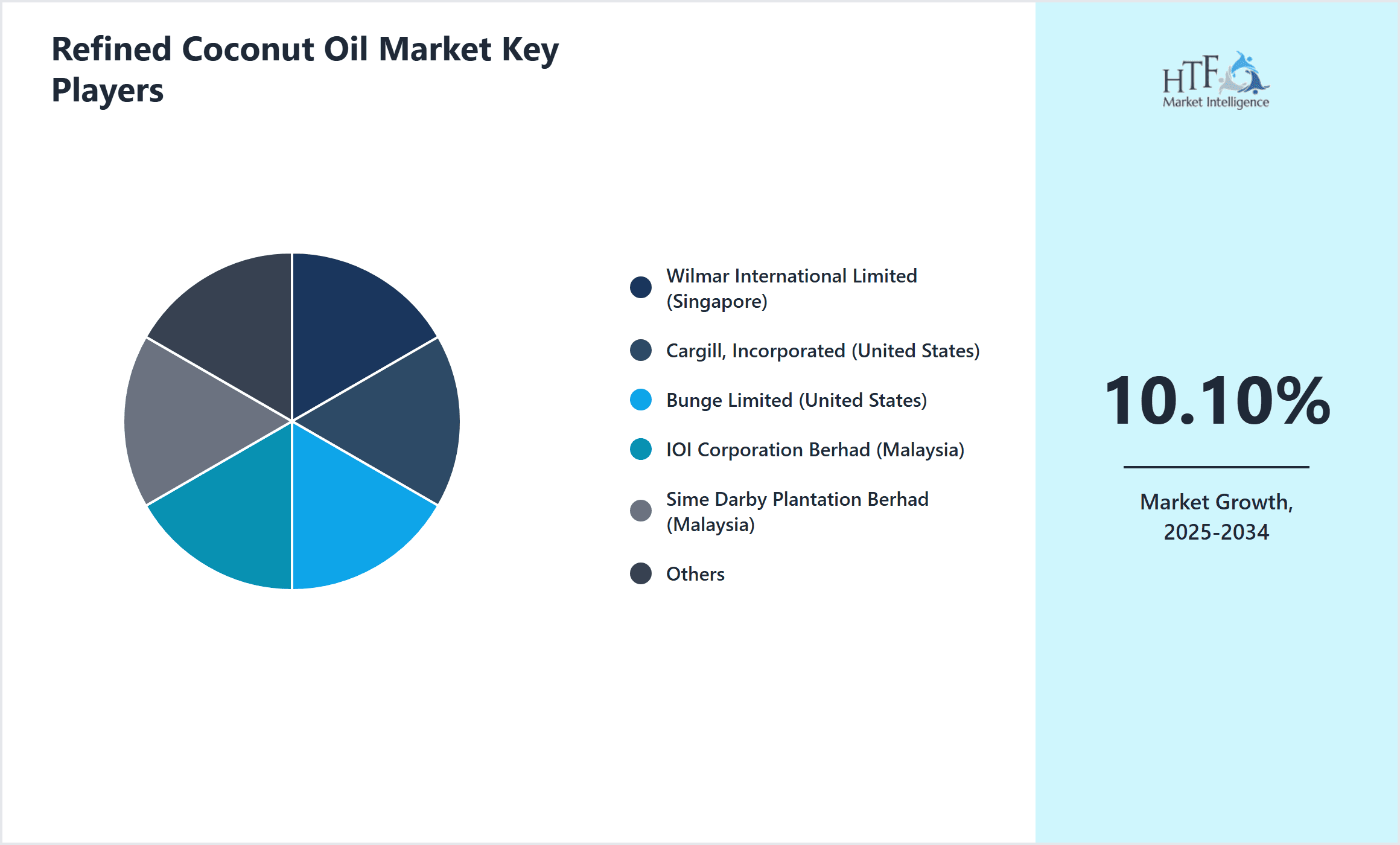

Leading Companies in Refined Coconut Oil Market

- •Wilmar International Limited (Singapore)

- •Cargill, Incorporated (United States)

- •Bunge Limited (United States)

- •IOI Corporation Berhad (Malaysia)

- •Sime Darby Plantation Berhad (Malaysia)

- •Olam International Ltd. (Singapore)

- •Musim Mas Holdings Pte Ltd. (Singapore)

- •Ruchi Soya Industries Ltd. (India)

- •Kraft Heinz Company (United States)

- •Golden Agri-Resources Ltd. (Singapore)

- •AAK AB (Sweden)

- •The J.M. Smucker Company (United States)

- •Marico Limited (India)

- •Coconut Oil Company Limited (United Kingdom)

- •Sundrop Fuels, Inc. (United States)

- •Hainan Yedao Group Co., Ltd. (China)

- •Kirkman Group (United Kingdom)

- •Desmet Ballestra Group (Belgium)

- •Oleon NV (Belgium)

- •Barco NV (Belgium)

- •Lesieur Cristal (France)

- •Corman SA (Belgium)

- •Ben & Anna GmbH (Germany)

- •Naturally Splendid Enterprises Ltd. (Canada)

- •Alfa Laval AB (Sweden)

Market Breakdown

- •By Refined Coconut Oil Type

- ◦Virgin Refined Coconut Oil

- ◦Bleached Coconut Oil

- ◦Deodorized Coconut Oil

- ◦Fractionated Coconut Oil

- ◦Organic Refined Coconut Oil

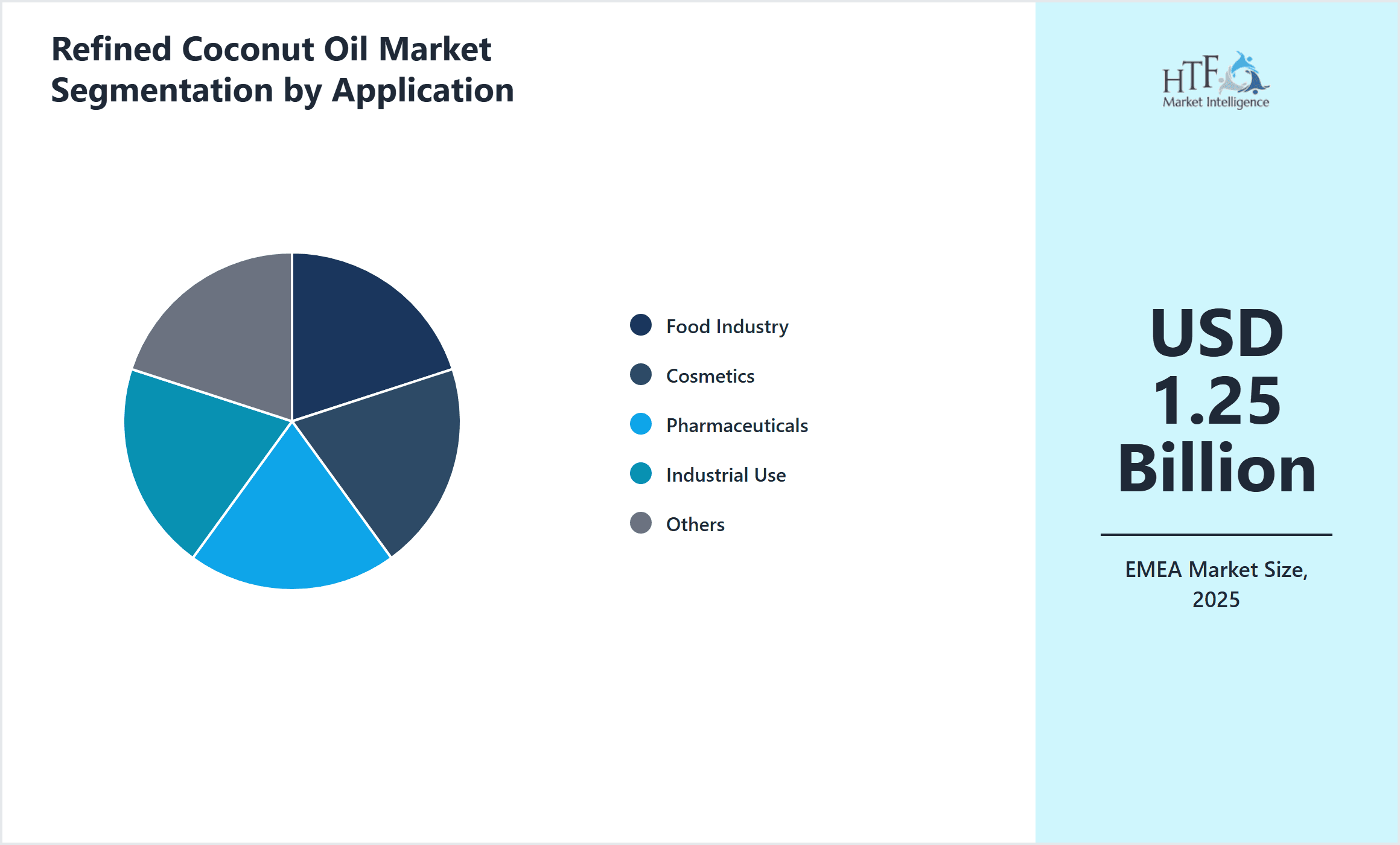

- •By Application Sector

- ◦Food Industry

- ◦Cosmetics

- ◦Pharmaceuticals

- ◦Industrial Use

- ◦Others

- •By Distribution Channel

- ◦Retail

- ◦Wholesale

- ◦Online

- ◦Direct Industrial Supply

- •By Production Technology

- ◦Steam Refining

- ◦Chemical Refining

- ◦Physical Refining

Growth Dynamics

The EMEA refined coconut oil market growth is driven by rising health awareness among consumers, leading to increased demand for natural and functional oils in food products. The expanding cosmetics sector leverages refined coconut oil for its moisturizing and antimicrobial properties, boosting market penetration. Technological advancements in refining processes enhance oil quality and shelf life, attracting industrial users seeking stable and odorless oils. Additionally, growing demand for organic and sustainably sourced oils aligns with consumer preference shifts, supporting premium product segments. Government initiatives promoting renewable resources and bio-based products further stimulate industrial applications, driving overall market growth.

Market Trends

A prominent trend in the EMEA refined coconut oil market is the surge in organic and fractionated coconut oil products, reflecting consumer preference for health-conscious and specialty oils. Companies are increasingly adopting green refining technologies to reduce environmental impact and meet sustainability goals. The cosmetics industry is innovating with coconut oil-based formulations, capitalizing on natural ingredient trends. Digital transformation in supply chain and e-commerce channels is expanding market reach and consumer access. Furthermore, collaborations between raw material suppliers and refiners are strengthening to ensure quality and traceability, enhancing market credibility.

Market Opportunities

EMEA presents substantial opportunities in the refined coconut oil market through untapped organic product segments and emerging cosmetic applications. The increasing consumer inclination towards vegan and cruelty-free products opens avenues for coconut oil derivatives. Expansion in the pharmaceutical sector, utilizing refined coconut oil for drug delivery and topical formulations, offers growth potential. Geographic expansion into developing EMEA countries with rising disposable incomes can drive demand. Investment in advanced refining infrastructure and R&D for novel fractions and blends can create competitive advantages and new product categories.

Market Challenges

Key challenges in the EMEA refined coconut oil market include supply chain volatility due to raw coconut availability and geopolitical factors affecting import logistics. High costs associated with organic certification and premium refining technologies can limit market accessibility. Regulatory heterogeneity across EMEA countries complicates compliance and market entry strategies. Intense competition from alternative vegetable oils and synthetic substitutes exerts pricing pressure. Additionally, consumer skepticism regarding product authenticity and quality necessitates stringent quality assurance and transparent labeling, posing operational challenges for market participants.

Regulatory Framework

Between 2020 and 2025, the EMEA refined coconut oil market has been shaped by evolving food safety and organic certification regulations, including compliance with EU Regulation No 2018/848 on organic production effective from 2021. These regulations require rigorous sourcing documentation and processing standards to ensure product integrity. Additionally, REACH regulations govern chemical usage in refining processes, mandating safety assessments and environmental protection. The Cosmetic Products Regulation (EC) No 1223/2009 enforces ingredient safety standards for coconut oil in personal care applications. Import tariffs and trade agreements within EMEA countries impact cost structures and market access. Governments also promote sustainability initiatives encouraging green refining technologies and renewable resource utilization, influencing investment and operational practices in the market.

Market Intelligence

- •15th February 2025, Wilmar International Limited announced the launch of an advanced organic refined coconut oil product tailored for the European cosmetics market. The product features enhanced purity and certification compliant with EU organic standards, targeting premium skincare formulations. This launch aims to capture growing demand for natural personal care ingredients, reinforcing Wilmar's leadership in sustainable oil production within EMEA. The initiative includes strategic partnerships with local suppliers to ensure traceable and ethical sourcing of coconuts, aligning with consumer expectations. Source: Wilmar International Official Press Release.

- •10th October 2024, AAK AB expanded its refining capacity in Germany by commissioning a new state-of-the-art physical refining unit designed to improve yield and reduce environmental impact. This facility upgrade supports AAK’s strategy to enhance high-quality fractionated coconut oil production for the food and pharmaceutical sectors. The investment bolsters supply chain resilience and positions the company to meet increasing demand for specialty oils in EMEA. The expansion reflects growing industry emphasis on sustainable processing technologies and product innovation. Source: AAK AB Corporate Announcement.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.25 Billion |

| Forecast Year Market Size | USD 2.85 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.1% |

| Scope of Report | Market is segmented by Refined Coconut Oil Type (Virgin Refined Coconut Oil, Bleached Coconut Oil, Deodorized Coconut Oil, Fractionated Coconut Oil, Organic Refined Coconut Oil), Application Sector (Food Industry, Cosmetics, Pharmaceuticals, Industrial Use, Others), Distribution Channel (Retail, Wholesale, Online, Direct Industrial Supply), Production Technology (Steam Refining, Chemical Refining, Physical Refining) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Wilmar International Limited (Singapore), Cargill, Incorporated (United States), Bunge Limited (United States), IOI Corporation Berhad (Malaysia), Sime Darby Plantation Berhad (Malaysia) |

EMEA Refined Coconut Oil Market - Outlook 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.