North America Single-cell Analysis Market Size, Growth & Revenue 2025-2034

North America Single-cell Analysis Market is segmented by Type (Flow Cytometry, Microfluidics, Imaging, Sequencing, Mass Cytometry), Application (Cancer Research, Immunology, Drug Discovery, Developmental Biology, Stem Cell Research), Product Category (Instruments, Consumables, Software), End-User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Hospitals & Diagnostic Laboratories), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Single-cell Analysis market comprises cutting-edge technologies and instruments that enable researchers to investigate individual cells with high precision and throughput. This market includes platforms such as flow cytometry, microfluidics, imaging, sequencing, and mass cytometry, which provide detailed cellular and molecular insights essential for understanding disease mechanisms and biological processes. Applications primarily focus on cancer research, immunology, drug discovery, developmental biology, and stem cell research to facilitate personalized medicine and targeted therapeutics. The market covers a broad range of products including hardware, consumables, and software solutions, which collectively enhance analytical capabilities and data interpretation. North America dominates this sector due to its advanced research infrastructure, substantial funding from governmental and private sectors, and the presence of numerous biotech and pharmaceutical companies adopting single-cell technologies. Growing demand for precise diagnostics and the integration of AI and machine learning in single-cell data analysis further expand the market’s scope and significance.

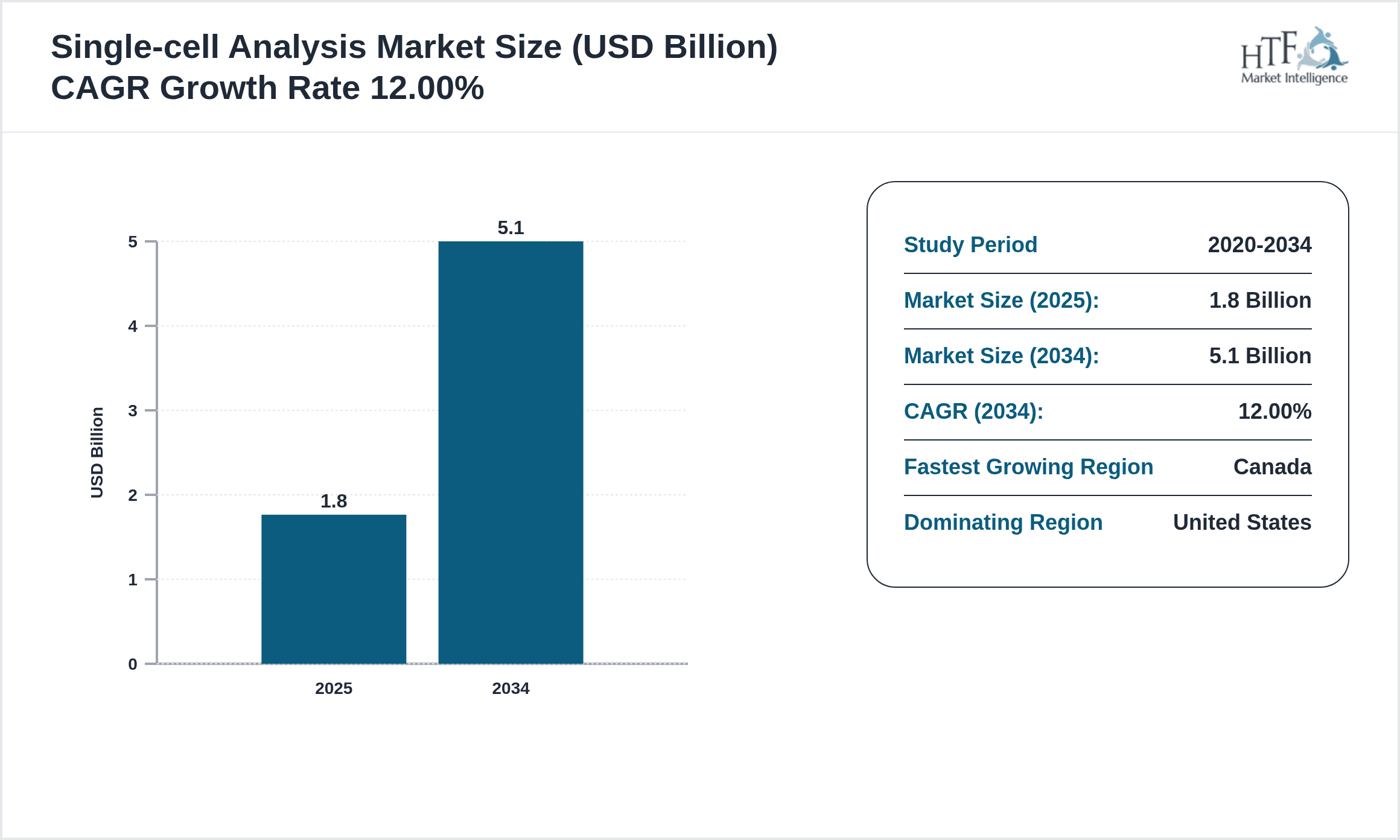

- •Key market highlights include a robust CAGR of 12.0% forecasted from 2025 to 2034, with the market size expected to grow from USD 1.8 billion in 2025 to USD 5.1 billion by 2034. Flow cytometry remains the leading product type due to its widespread adoption and versatility, while microfluidics is the fastest-growing technology, driven by miniaturization and automation trends. The United States holds the dominant regional market share supported by strong R&D activities, whereas Canada is exhibiting the highest growth rate due to increasing investments in precision medicine and academic research. The market’s expansion is fueled by advances in single-cell sequencing technologies and increasing collaborations between academia and industry to develop novel diagnostics and therapies.

- •The single-cell analysis market offers significant value to pharmaceutical companies, research institutes, and healthcare providers by enabling detailed cellular profiling and improved understanding of disease heterogeneity. Its strategic importance lies in supporting drug development pipelines, biomarker discovery, and personalized treatment approaches, which are critical in oncology and immunotherapy fields. Stakeholders benefit from enhanced data resolution and reproducibility, fostering innovation and accelerating translational research. The growing integration of computational biology and bioinformatics tools further enhances the market’s impact by enabling comprehensive multi-omics data analysis. Overall, the North America market’s maturity, coupled with technological innovation and increasing healthcare expenditures, positions single-cell analysis as a transformative tool in life sciences and clinical research.

Competitive Landscape

The competitive environment in the North America Single-cell Analysis market is characterized by intense innovation, strategic partnerships, and technology-driven growth. Companies focus on expanding their product portfolios through the development of integrated platforms that combine sequencing, imaging, and cytometry technologies to offer comprehensive cellular analysis solutions. Collaborations with academic institutions and pharmaceutical companies enable co-development of application-specific tools and enhance market penetration. Firms invest heavily in R&D to improve throughput, sensitivity, and automation capabilities, addressing the demand for faster and more accurate analysis. Global expansion strategies target increasing presence in emerging biotechnology hubs within North America and beyond. Pricing strategies balance high-end technological features with scalability to capture both research institutions and clinical markets. Furthermore, acquisitions of niche technology providers foster portfolio diversification and consolidation of expertise. The adoption of AI and machine learning in data analytics differentiates market leaders and creates competitive advantages. Regulatory compliance and intellectual property management also play critical roles in sustaining market presence and barriers to entry. Future competition will likely revolve around integrated multi-omics platforms and personalized medicine applications.

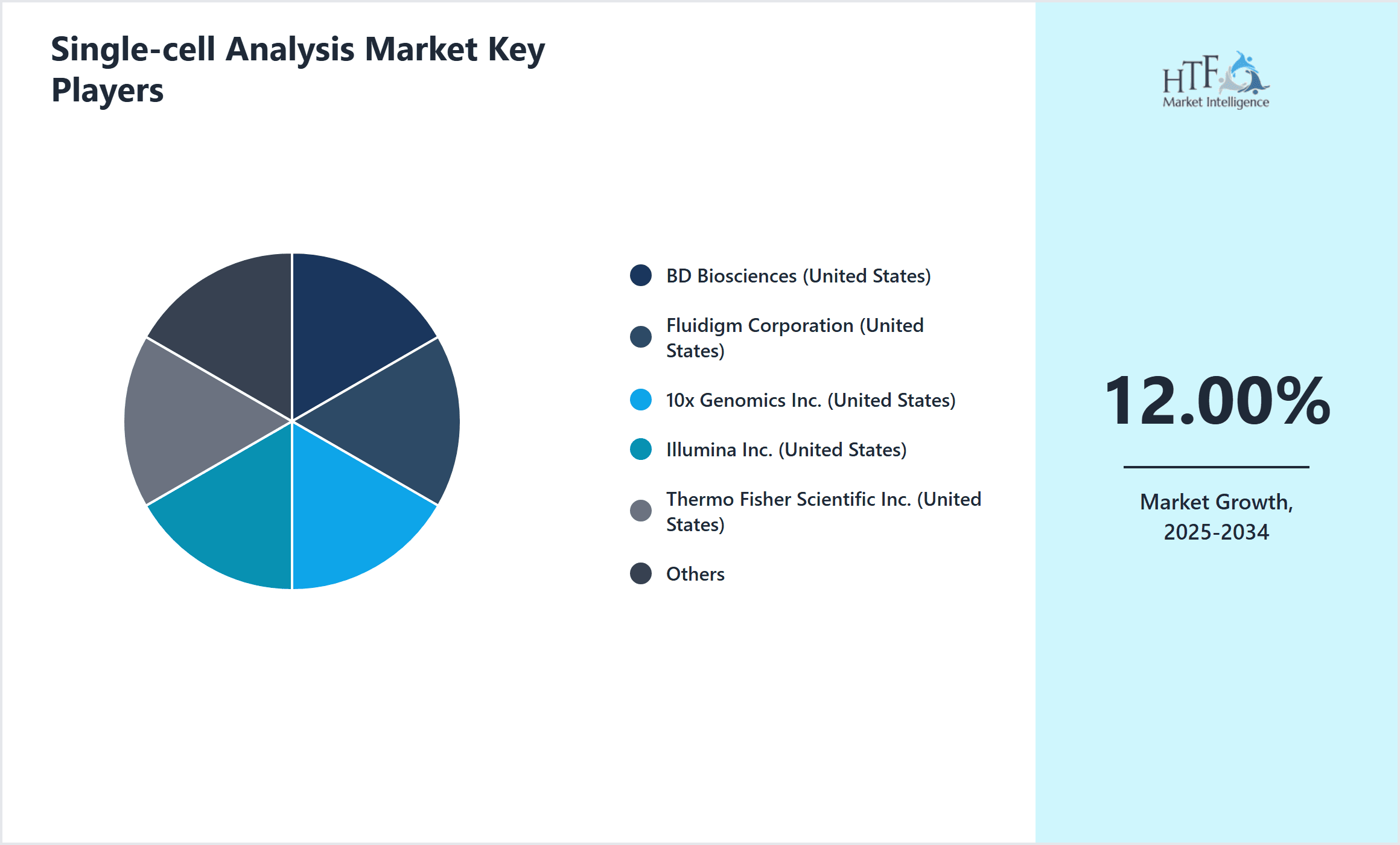

Leading Companies in Single-cell Analysis Market

- •BD Biosciences (United States)

- •Fluidigm Corporation (United States)

- •10x Genomics Inc. (United States)

- •Illumina Inc. (United States)

- •Thermo Fisher Scientific Inc. (United States)

- •Sony Biotechnology Inc. (United States)

- •Bio-Rad Laboratories, Inc. (United States)

- •Danaher Corporation (United States)

- •Miltenyi Biotec (United States)

- •Celsee Diagnostics (United States)

- •Roche Diagnostics (United States)

- •NanoString Technologies, Inc. (United States)

- •Parse Biosciences (United States)

- •Singleron Biotechnologies (United States)

- •Bio-Techne Corporation (United States)

- •Takara Bio Inc. (United States)

- •Sphere Fluidics Ltd. (United Kingdom)

- •Abcam plc (United Kingdom)

- •Berkeley Lights, Inc. (United States)

- •Mission Bio, Inc. (United States)

Market Breakdown

- •By Type

- ◦Flow Cytometry

- ◦Microfluidics

- ◦Imaging

- ◦Sequencing

- ◦Mass Cytometry

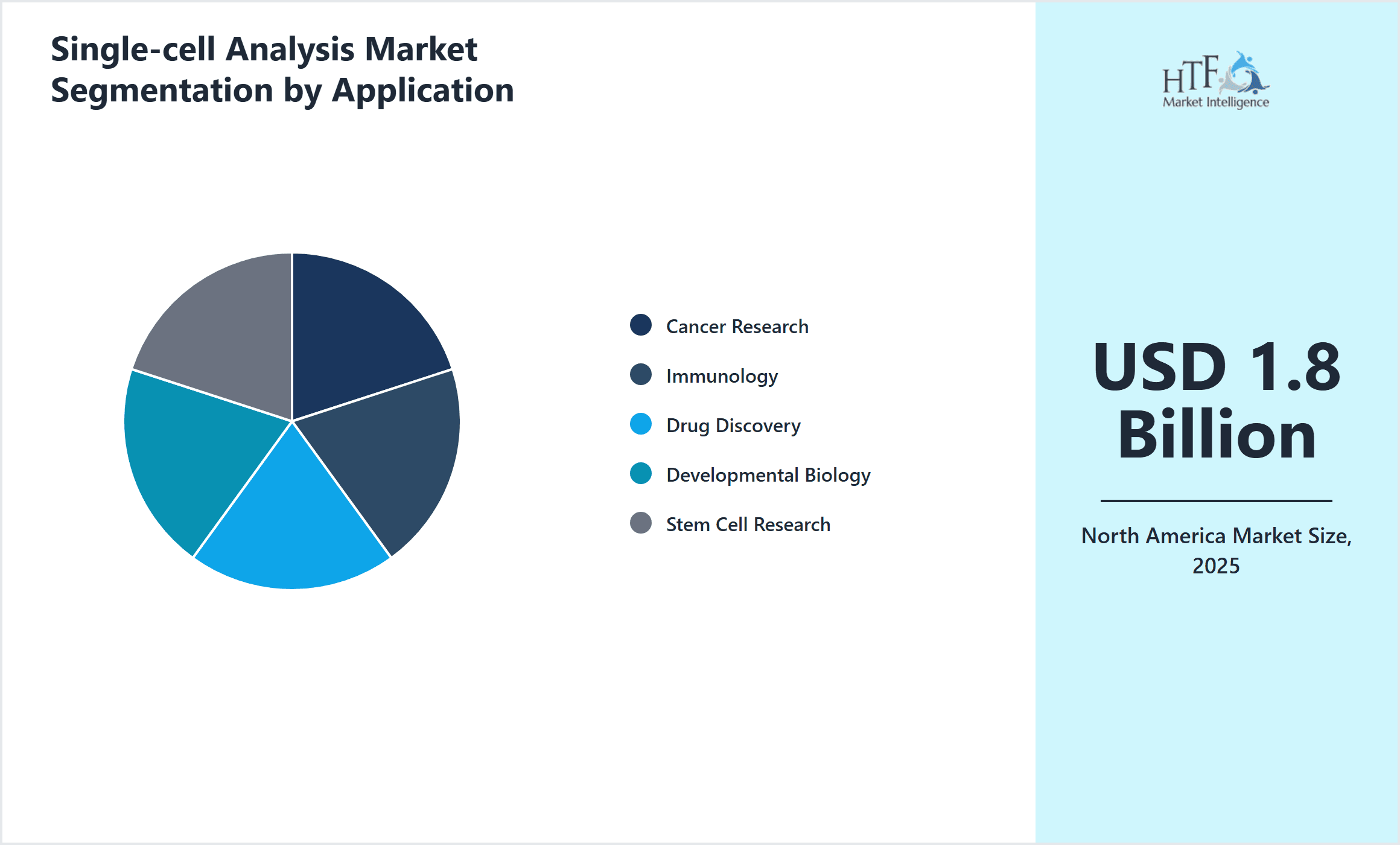

- •By Application

- ◦Cancer Research

- ◦Immunology

- ◦Drug Discovery

- ◦Developmental Biology

- ◦Stem Cell Research

- •By Product Category

- ◦Instruments

- ◦Consumables

- ◦Software

- •By End-User

- ◦Pharmaceutical & Biotechnology Companies

- ◦Academic & Research Institutes

- ◦Hospitals & Diagnostic Laboratories

Growth Dynamics

The North America Single-cell Analysis market experiences significant growth driven by increasing adoption of precision medicine and personalized therapeutics. The rising prevalence of cancer and autoimmune diseases necessitates detailed cellular profiling, fueling demand for advanced single-cell technologies such as flow cytometry and microfluidics. Technological advancements, including automation and integration of multi-omics data, enhance analytical throughput and data accuracy, attracting pharmaceutical companies to invest in these platforms. Government funding and private investments in genomics research further accelerate market expansion. Recent collaborations, such as between 10x Genomics and leading cancer research centers, exemplify the strategic push towards developing novel diagnostic tools. Additionally, the COVID-19 pandemic emphasized the importance of understanding immune response at the single-cell level, boosting research activities and technology adoption. The growing availability of single-cell analysis consumables and software for data processing supports end-users in overcoming analytical complexities, reinforcing market growth.

Market Trends

Emerging trends in the North America Single-cell Analysis market include the convergence of single-cell multi-omics technologies and artificial intelligence-driven data analytics. Companies are developing integrated platforms that simultaneously analyze transcriptomics, proteomics, and epigenomics at the single-cell level, enabling comprehensive biological insights. The rise of spatial transcriptomics adds a new dimension by preserving tissue architecture while profiling individual cells, facilitating advanced cancer and neuroscience research. Industry leaders are increasingly adopting cloud-based bioinformatics solutions to handle large-scale single-cell data, promoting collaborative research and accelerating discoveries. The expansion of single-cell analysis into clinical diagnostics and companion diagnostics presents new revenue streams. Furthermore, miniaturization and cost reduction efforts are democratizing access to single-cell technologies beyond large research institutions. The trend toward automation and high-throughput screening aligns with pharmaceutical industry demands for efficient drug discovery pipelines. These advancements position the market for sustained innovation and broader application adoption.

Market Opportunities

The North America Single-cell Analysis market offers substantial opportunities in expanding applications beyond oncology and immunology into areas such as neurology, infectious diseases, and regenerative medicine. Increasing investments in single-cell sequencing and microfluidics by key players enable the development of novel diagnostic assays and therapeutic targets. Integration of single-cell analysis with CRISPR gene editing technologies creates pathways for functional genomics studies and precision therapies. Emerging startups are introducing cost-effective and portable single-cell platforms, opening access to smaller laboratories and clinical settings. Government initiatives supporting genomics research and data-sharing frameworks enhance collaboration and innovation potential. Additionally, growing interest in spatial and temporal single-cell profiling presents opportunities for new product development. Partnerships between technology providers and pharmaceutical companies to co-develop companion diagnostics further expand the market. Expanding reimbursement policies for advanced diagnostics and personalized therapies in North America also drive adoption and investment, making the market attractive for newcomers and established firms alike.

Market Challenges

High costs associated with single-cell analysis instruments and consumables limit adoption, especially among smaller research institutions and diagnostic laboratories. The complexity of data generated requires advanced bioinformatics expertise and computational infrastructure, posing barriers for end-users lacking such resources. Standardization issues across platforms and variability in sample preparation affect data reproducibility and comparability, challenging regulatory acceptance and clinical translation. Supply chain disruptions and shortages of key reagents during recent global events have impacted market growth and delivery timelines. Intellectual property disputes and patent litigations among technology providers create uncertainties, potentially delaying product launches. Additionally, stringent regulatory requirements for clinical applications slow the integration of single-cell technologies into routine diagnostics. Companies face challenges in educating the market about the benefits and applications of single-cell analysis, impacting demand generation. These factors collectively restrain market expansion and require strategic mitigation by stakeholders.

Regulatory Framework

In the last five years, North America has seen the implementation of key regulatory guidelines impacting the single-cell analysis market. The U.S. Food and Drug Administration introduced updated policies for laboratory-developed tests emphasizing analytical validation and clinical evidence, affecting companion diagnostics developed using single-cell technologies. Compliance with the Clinical Laboratory Improvement Amendments ensures quality standards for diagnostic laboratories employing these advanced tools. Data privacy regulations under HIPAA govern the handling of patient genomic information, necessitating robust data security measures by providers. The FDA's breakthrough device designation pathway facilitates expedited review for innovative single-cell diagnostic platforms, encouraging innovation. Additionally, the National Institutes of Health has issued guidelines on genomic data sharing promoting transparency and collaboration while protecting patient confidentiality. These evolving regulations shape product development, market entry strategies, and operational compliance for stakeholders in the North America single-cell analysis industry.

Market Intelligence

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 5.1 Billion |

| CAGR | 12% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.1% |

| Scope of Report | Market is segmented by Type (Flow Cytometry, Microfluidics, Imaging, Sequencing, Mass Cytometry), Application (Cancer Research, Immunology, Drug Discovery, Developmental Biology, Stem Cell Research), Product Category (Instruments, Consumables, Software), End-User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Hospitals & Diagnostic Laboratories) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | BD Biosciences (United States), Fluidigm Corporation (United States), 10x Genomics Inc. (United States), Illumina Inc. (United States), Thermo Fisher Scientific Inc. (United States) |

North America Single-cell Analysis Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.