Global Engineering Materials Market Size, Growth & Revenue 2025-2034

Global Engineering Materials Market is segmented by Application (Automotive, Aerospace, Construction, Electronics, Energy), Type (Metals, Polymers, Ceramics, Composites, Elastomers), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global engineering materials market constitutes a diverse portfolio of materials engineered to meet rigorous functional requirements across multiple end-use sectors such as automotive, aerospace, construction, electronics, and energy. This market includes metals, polymers, ceramics, composites, and elastomers that are fundamental to manufacturing and infrastructure development worldwide. The materials are characterized by their mechanical strength, thermal stability, corrosion resistance, and lightweight properties, enabling enhanced product performance and longevity. Technological innovations such as additive manufacturing and nanomaterials integration have accelerated the evolution of this market, offering superior material properties and customization capabilities. The increasing focus on sustainability and eco-friendly materials, driven by stringent environmental regulations, further shapes market dynamics by promoting recyclable and low-impact materials. The market is driven by rapid industrialization, growing demand from emerging economies, and the need for advanced materials in high-performance applications. Strategic investments in R&D and manufacturing capabilities are enhancing product portfolios and expanding application horizons. Key players focus on innovation, partnerships, and geographic expansion to consolidate their positions. This comprehensive analysis covers market size, growth trends, competitive landscape, regulatory environment, and regional performance, providing stakeholders with actionable insights for strategic decision-making and long-term value creation.

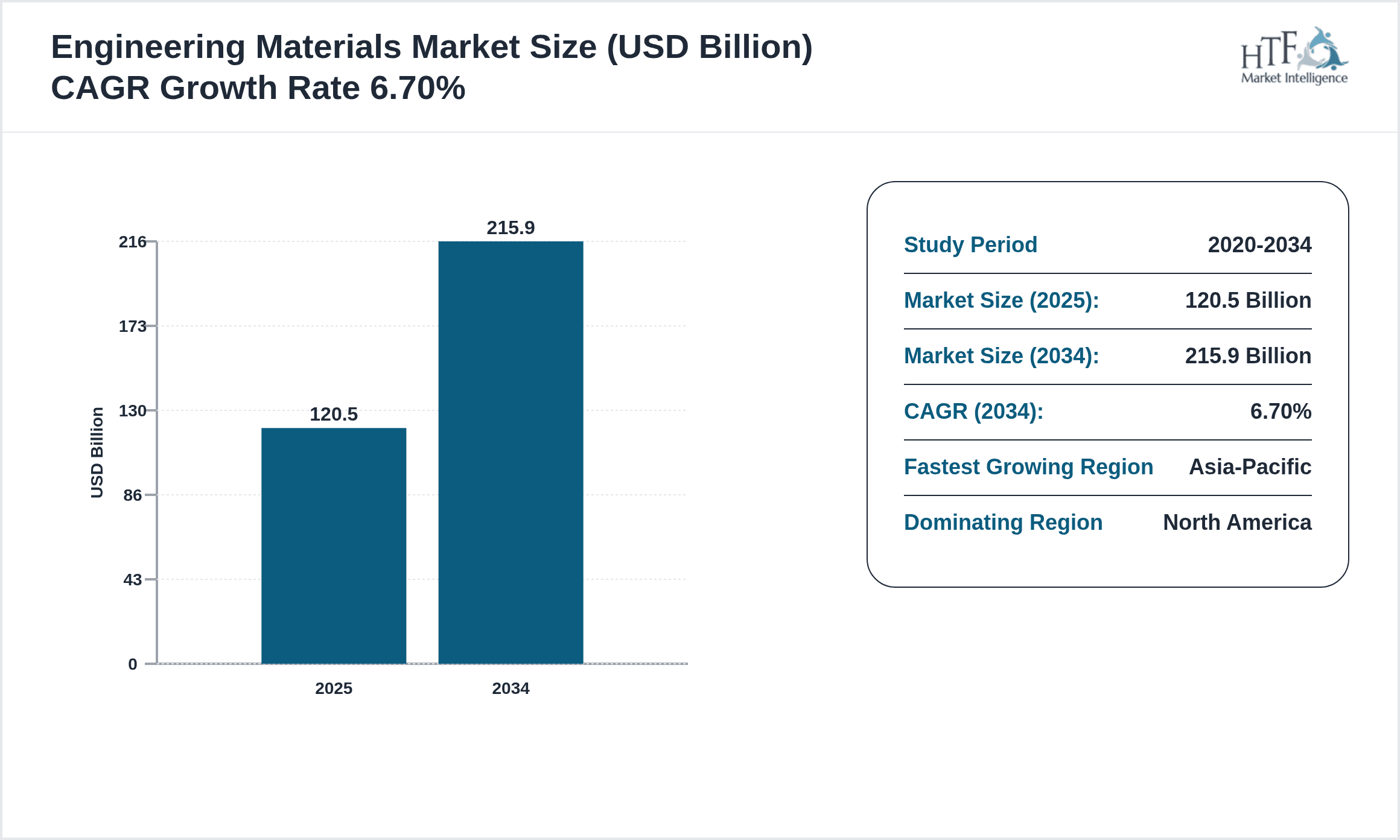

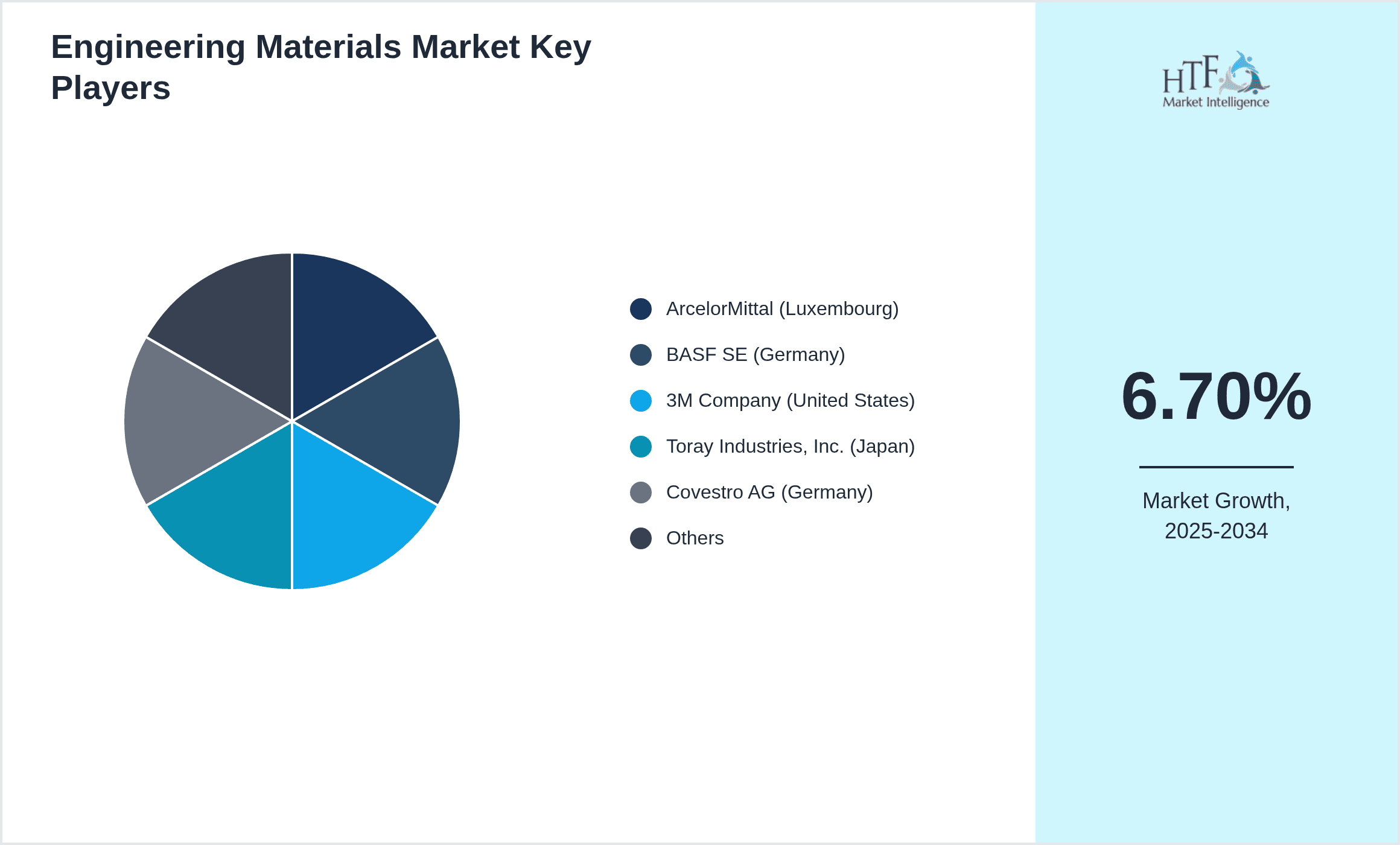

- •Key highlights of the market indicate a robust growth trajectory with a base market size of USD 120.5 Billion in 2025, expected to reach USD 215.9 Billion by 2034, reflecting a CAGR of 6.7%. North America leads the market in terms of revenue and technological advancement, while Asia-Pacific emerges as the fastest-growing region owing to rapid industrial expansion and infrastructure development. Metals remain the dominant product type due to their widespread use, whereas composites exhibit the fastest growth, driven by demand for lightweight and high-strength materials in aerospace and automotive sectors. The market benefits from increasing investments in sustainable materials and digital manufacturing techniques. However, challenges such as raw material price volatility and stringent regulatory compliances persist, necessitating adaptive strategies. Emerging opportunities in electric vehicles, renewable energy, and advanced electronics present significant growth avenues. The competitive landscape is marked by innovation, strategic collaborations, and mergers, fostering a dynamic and evolving market environment.

- •This market report delivers strategic value to manufacturers, suppliers, investors, and policy makers by providing a thorough understanding of market segmentation, growth drivers, competitive dynamics, and regional performance. It equips stakeholders with data-driven insights to identify promising application areas, optimize product development, and navigate regulatory complexities. The analysis highlights the importance of adopting advanced materials and sustainable practices to meet future industrial demands and environmental goals. By leveraging emerging technologies and responding to evolving customer requirements, market participants can enhance competitiveness and capitalize on growth opportunities in the global engineering materials domain.

Competitive Landscape

The global engineering materials market exhibits a competitive environment characterized by the presence of multinational corporations and specialized regional players focusing on innovation, product diversification, and strategic partnerships. Market leaders deploy advanced research and development initiatives to enhance material properties and application versatility, integrating cutting-edge technologies such as nanotechnology and additive manufacturing. Competitive strategies include mergers and acquisitions to consolidate market share, expansion into emerging markets to leverage industrial growth, and collaborations for technology sharing and co-development. Pricing strategies are influenced by raw material availability, production costs, and value-added features. Distribution channels encompass direct sales, distributors, and online platforms, enabling broad market reach. The market faces entry barriers including high capital requirements, stringent quality standards, and regulatory compliance. Regional competition is intensified by localized manufacturing capabilities and government policies promoting domestic industries. Future competitive trends involve increased emphasis on sustainability, digital transformation of supply chains, and customization of material solutions to meet sector-specific demands, fostering a dynamic landscape that continuously evolves to address technological and market challenges.

Prominent Players in Engineering Materials Market

- •ArcelorMittal (Luxembourg)

- •BASF SE (Germany)

- •3M Company (United States)

- •Toray Industries, Inc. (Japan)

- •Covestro AG (Germany)

- •DuPont de Nemours, Inc. (United States)

- •Novelis Inc. (United States)

- •SGL Carbon SE (Germany)

- •Celanese Corporation (United States)

- •Mitsubishi Chemical Holdings Corporation (Japan)

- •Evonik Industries AG (Germany)

- •Hexcel Corporation (United States)

- •Solvay S.A. (Belgium)

- •Wacker Chemie AG (Germany)

- •Coventya Group (France)

- •Teijin Limited (Japan)

- •Sumitomo Chemical Co., Ltd. (Japan)

- •LG Chem Ltd. (South Korea)

- •Akzo Nobel N.V. (Netherlands)

- •Sabic (Saudi Arabia)

- •Hitachi Chemical Company, Ltd. (Japan)

- •Ube Industries, Ltd. (Japan)

- •Celanese Corporation (United States)

- •Evonik Industries AG (Germany)

- •Eastman Chemical Company (United States)

Market Segmentation of Global Engineering Materials

- •By Material Type

- ◦Metals (Steel, Aluminum, Titanium)

- ◦Polymers (Thermoplastics, Thermosets)

- ◦Ceramics (Advanced, Traditional)

- ◦Composites (Fiber-reinforced, Particle-reinforced)

- ◦Elastomers (Synthetic, Natural)

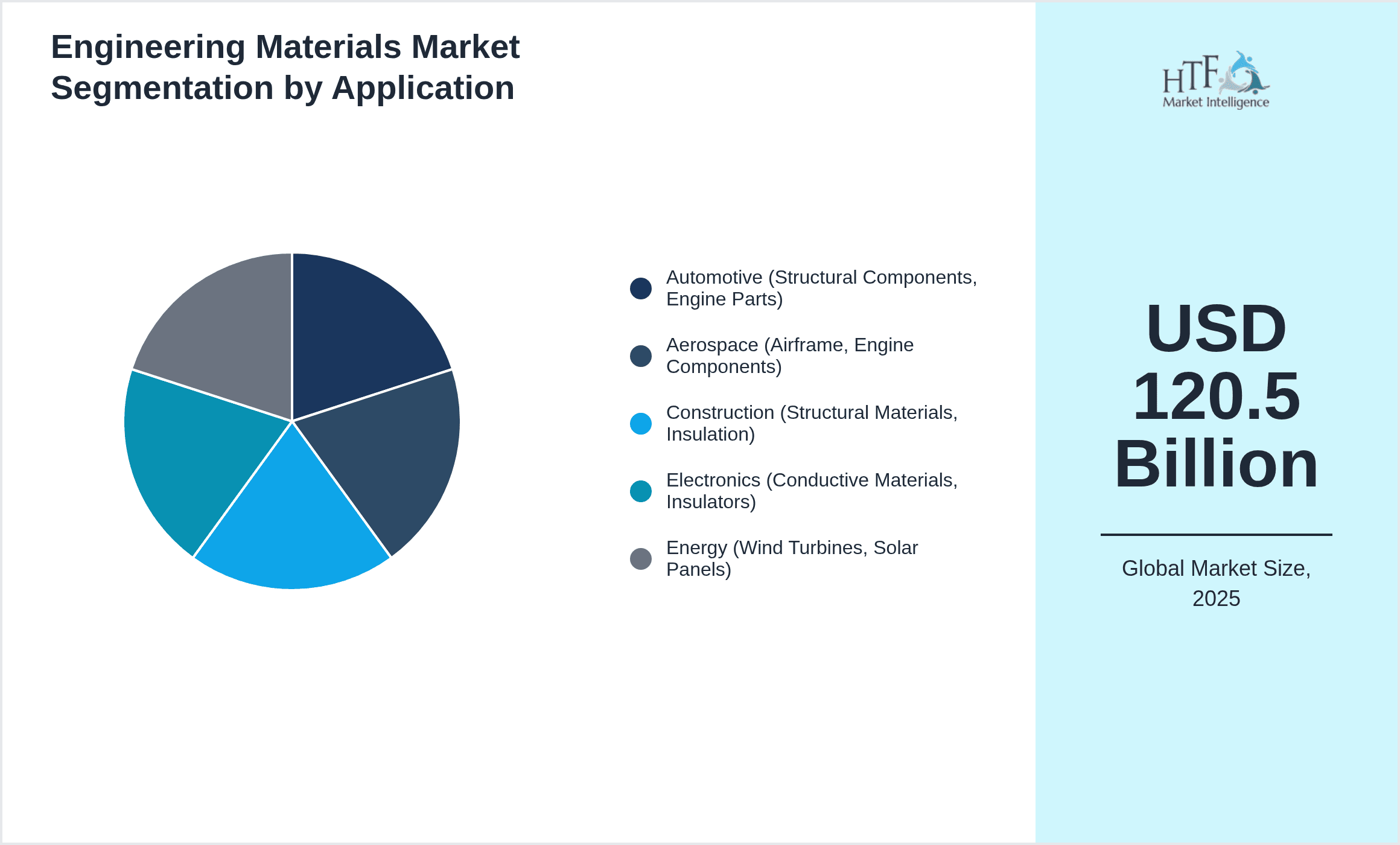

- •By Application Sector

- ◦Automotive (Structural Components, Engine Parts)

- ◦Aerospace (Airframe, Engine Components)

- ◦Construction (Structural Materials, Insulation)

- ◦Electronics (Conductive Materials, Insulators)

- ◦Energy (Wind Turbines, Solar Panels)

- •By Manufacturing Process

- ◦Casting

- ◦Forging

- ◦Additive Manufacturing

- ◦Extrusion

- ◦Molding

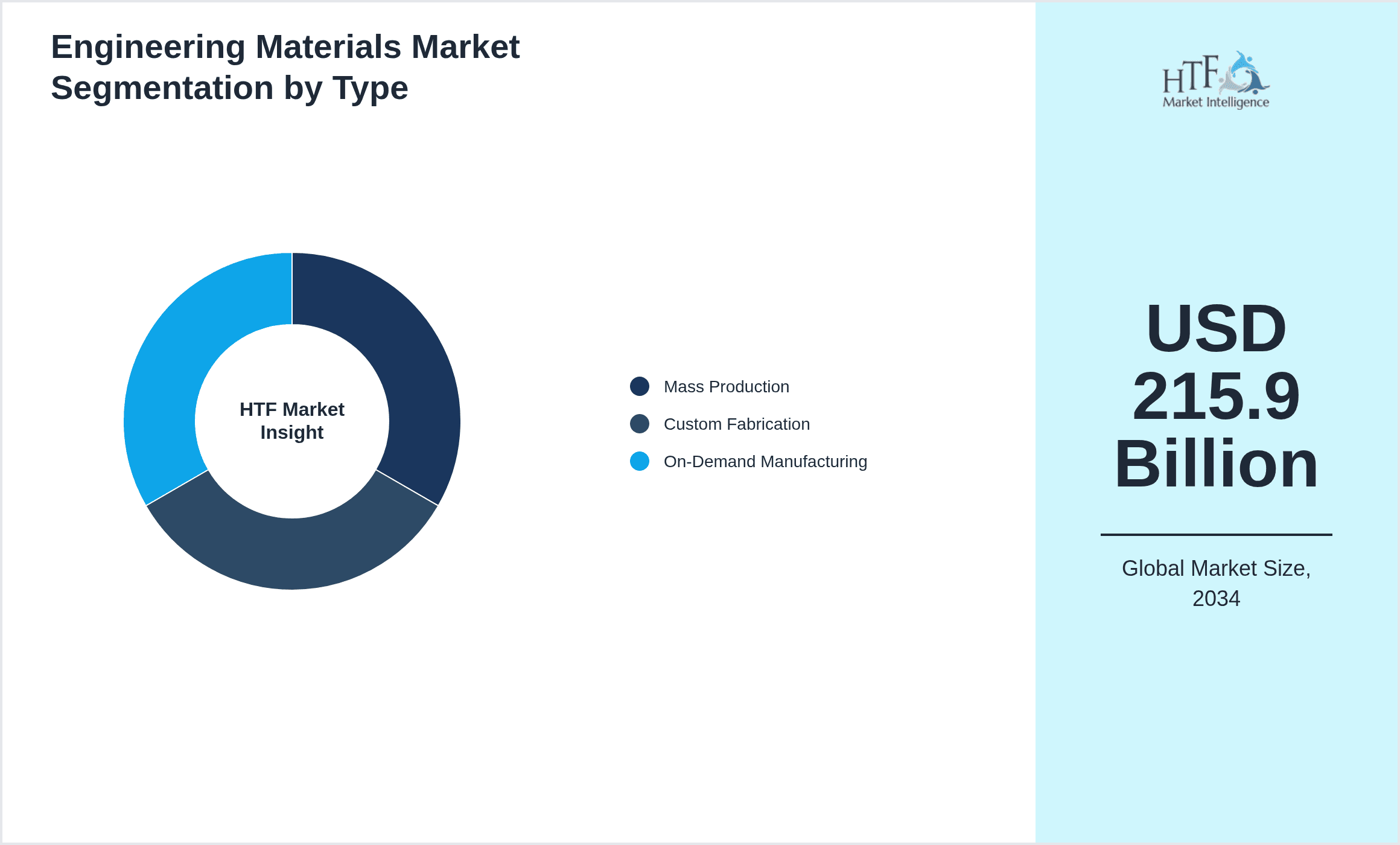

- •By Deployment Model

- ◦Mass Production

- ◦Custom Fabrication

- ◦On-Demand Manufacturing

Growth Dynamics of Global Engineering Materials Market

The global engineering materials market is propelled by growing industrialization and infrastructure development, especially in emerging economies, which drives demand for high-performance materials in automotive, aerospace, and construction sectors. Increasing focus on lightweight materials to improve fuel efficiency and reduce carbon emissions further accelerates growth. Technological advancements such as additive manufacturing enable complex geometries and material customization, expanding application possibilities. Additionally, stringent environmental regulations promote the adoption of sustainable and recyclable materials, encouraging innovation in green engineering materials. The rising demand for advanced electronics and renewable energy technologies also fuels the need for specialized materials with superior electrical and thermal properties, creating new growth avenues in the market.

Emerging Market Trends in Engineering Materials

A significant trend in the engineering materials market is the increasing integration of nanotechnology to enhance mechanical strength, thermal resistance, and electrical conductivity of materials. Innovations in bio-based polymers and recyclable composites reflect growing environmental consciousness and regulatory pressure. The adoption of digital manufacturing technologies, including Industry 4.0 and AI-driven process optimization, is transforming material production, enabling cost efficiency and precision. Furthermore, hybrid materials combining metals and polymers are gaining traction for their unique property combinations, catering to specialized applications. Collaboration among material manufacturers and end-users is intensifying to accelerate product development cycles and meet evolving performance requirements.

Opportunities in Global Engineering Materials Market

The global engineering materials market presents opportunities in electric vehicle manufacturing, where lightweight composites and advanced polymers can significantly improve battery efficiency and vehicle range. Expansion into renewable energy sectors such as wind and solar power offers demand for durable and corrosion-resistant materials. Emerging economies with infrastructure development projects offer untapped markets for construction materials with enhanced durability and sustainability profiles. Technological advancements in additive manufacturing create prospects for customized materials catering to aerospace and medical applications. Strategic partnerships and investments in R&D for bio-based and recyclable materials align with global sustainability goals, unlocking new business potential.

Challenges Facing the Global Engineering Materials Market

Market growth is constrained by fluctuations in raw material prices, which impact manufacturing costs and pricing strategies. Complex regulatory landscapes across regions impose compliance burdens, especially concerning environmental and safety standards. Limited availability of high-purity raw materials and supply chain disruptions pose operational challenges. Technological barriers in scaling novel materials such as nanocomposites and bio-polymers restrict widespread adoption. Additionally, intense competition and market saturation in mature regions pressure profit margins. The need for skilled workforce and high capital investment in advanced manufacturing infrastructure further challenge new entrants and smaller players.

Regulatory Framework Influencing Engineering Materials Market

Between 2020 and 2025, several key regulations have shaped the engineering materials market by enforcing environmental compliance and safety standards globally. The European Union’s REACH regulation mandates rigorous chemical safety assessments and reporting, influencing material formulations and supply chains. The U.S. Environmental Protection Agency (EPA) has implemented stricter emission standards impacting manufacturing processes and material selection. International standards such as ISO 9001 and ISO 14001 have become prerequisites for quality and environmental management, driving adoption of sustainable practices. Region-specific regulations in Asia-Pacific, including China’s new environmental protection laws, have accelerated demand for eco-friendly materials. Governments worldwide have introduced incentives and subsidies to promote green technologies and recycling initiatives, fostering innovation and market growth. Compliance with these frameworks requires robust testing, certification, and continuous monitoring, shaping product development and market entry strategies.

Market Intelligence Updates on Engineering Materials

- •15th January 2025, BASF SE launched a new range of bio-based polymers designed for automotive and packaging applications, featuring enhanced biodegradability and mechanical performance. This product line aims to reduce carbon footprint and comply with emerging environmental regulations in Europe and North America. The launch is expected to strengthen BASF’s position in sustainable materials and cater to growing demand for eco-friendly alternatives. Strategic collaborations with automotive manufacturers are underway to integrate these polymers into next-generation vehicle components. Source: BASF official press release

- •23rd March 2025, Toray Industries, Inc. announced the commercial introduction of advanced carbon fiber composites with improved tensile strength and thermal stability for aerospace and wind energy sectors. These composites enable weight reduction and enhance fuel efficiency in aircraft, supporting global sustainability goals. Toray's innovation is backed by extensive R&D investment and collaboration with leading aerospace companies. The new materials are anticipated to drive market growth in high-performance applications and expand the company's global footprint. Source: Toray Industries corporate news

- •10th May 2025, ArcelorMittal completed acquisition of a specialty steel producer in Southeast Asia, aiming to increase its product portfolio in high-strength steel for automotive and construction industries. This strategic move enhances ArcelorMittal’s market presence in the Asia-Pacific region and supports its growth strategy in emerging markets. The acquisition is projected to generate synergies in manufacturing and distribution, enabling competitive pricing and innovation acceleration. Integration plans include technology transfer and capacity expansion to meet rising regional demand. Source: ArcelorMittal press release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 120.5 Billion |

| Forecast Year Market Size | USD 215.9 Billion |

| CAGR | 6.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.5% |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | ArcelorMittal (Luxembourg), BASF SE (Germany), 3M Company (United States), Toray Industries, Inc. (Japan), Covestro AG (Germany), DuPont de Nemours, Inc. (United States), Novelis Inc. (United States), SGL Carbon SE (Germany), Celanese Corporation (United States), Mitsubishi Chemical Holdings Corporation (Japan), Evonik Industries AG (Germany), Hexcel Corporation (United States), Solvay S.A. (Belgium), Wacker Chemie AG (Germany), Coventya Group (France), Teijin Limited (Japan), Sumitomo Chemical Co., Ltd. (Japan), LG Chem Ltd. (South Korea), Akzo Nobel N.V. (Netherlands), Sabic (Saudi Arabia), Hitachi Chemical Company, Ltd. (Japan), Ube Industries, Ltd. (Japan), Celanese Corporation (United States), Evonik Industries AG (Germany), Eastman Chemical Company (United States) |

Global Engineering Materials Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.