Global Software Defined Everything Market Size, Growth & Revenue 2024-2034

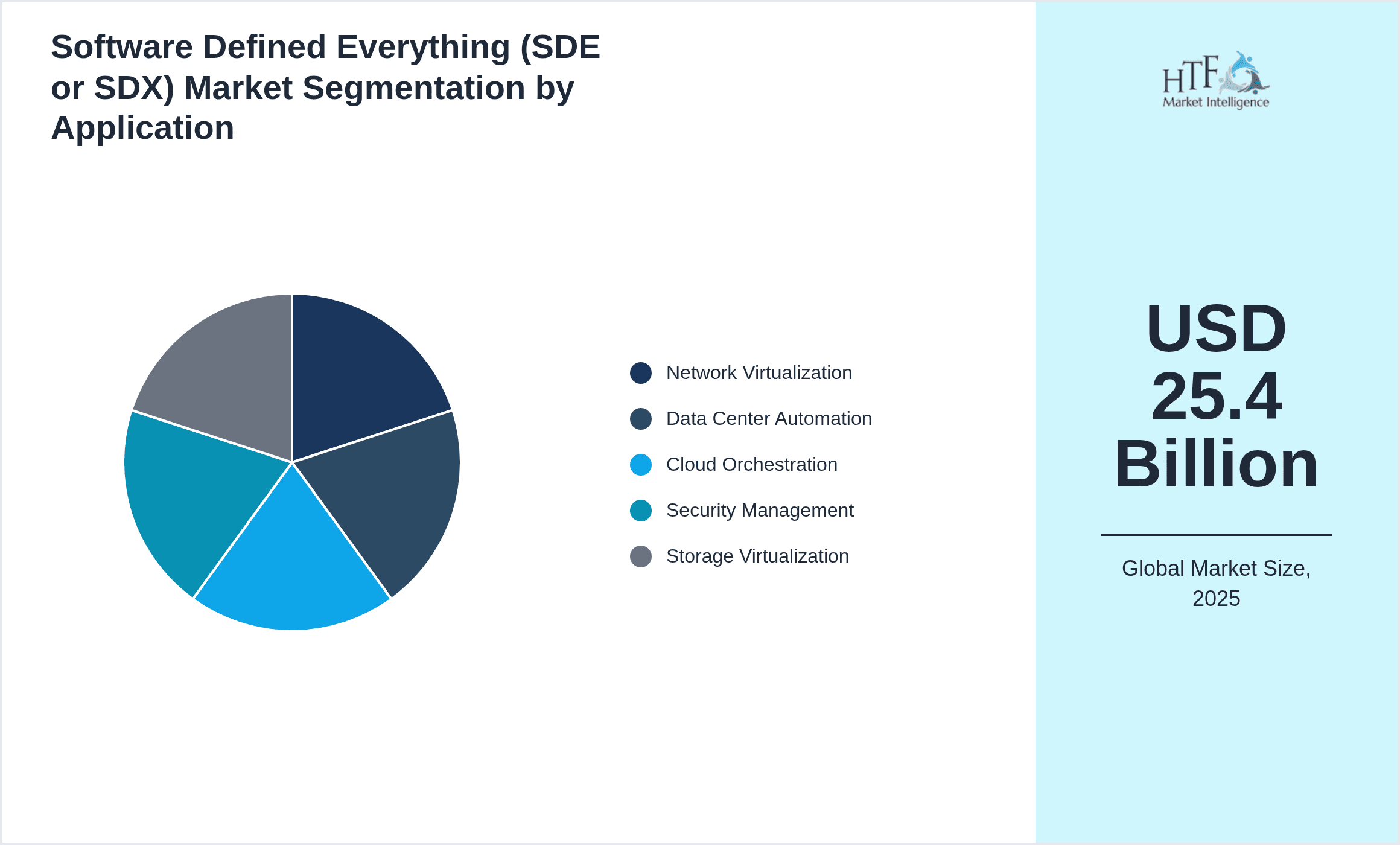

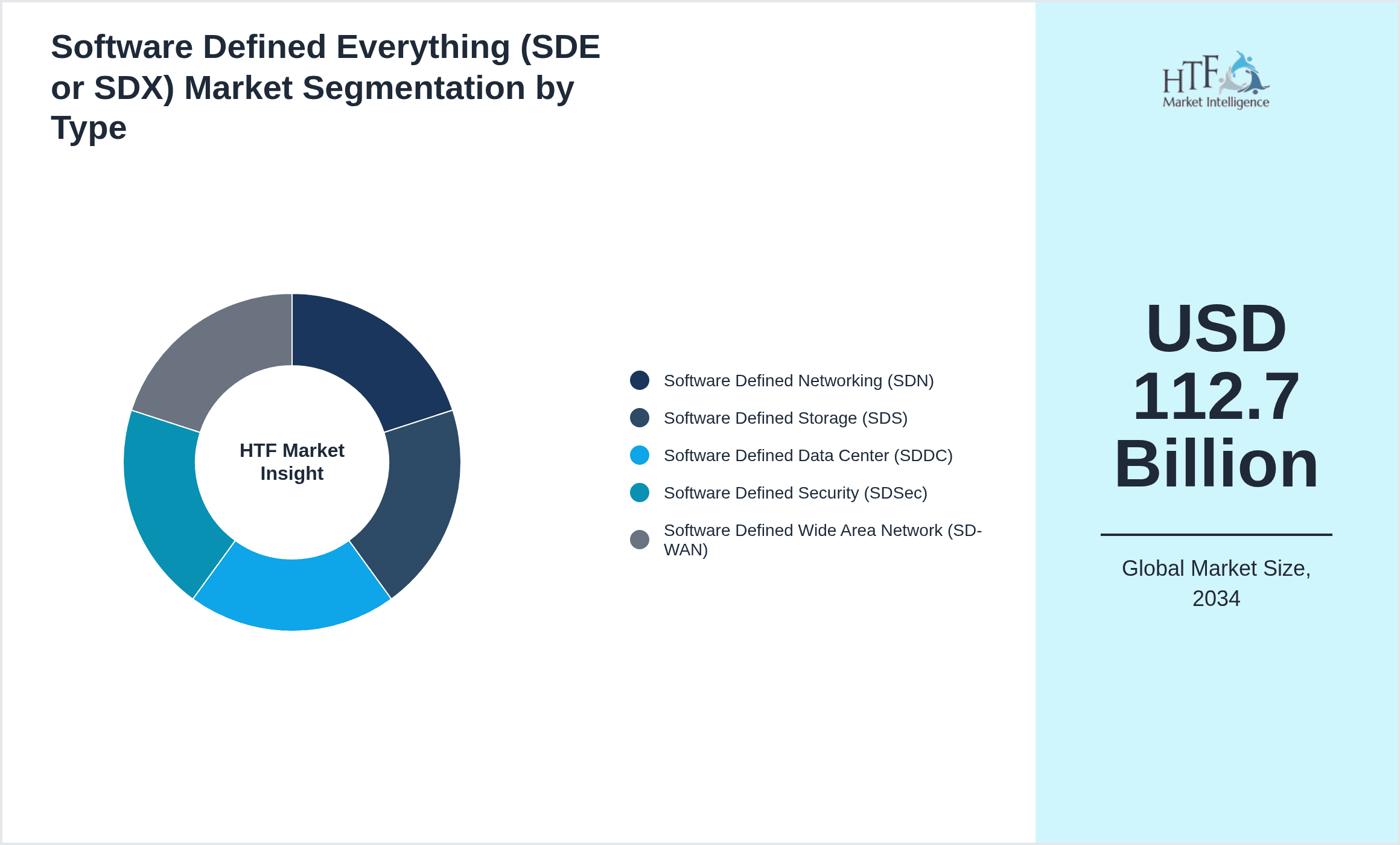

Global Software Defined Everything Market is segmented by Product Type (Software Defined Networking (SDN), Software Defined Storage (SDS), Software Defined Data Center (SDDC), Software Defined Security (SDSec), Software Defined Wide Area Network (SD-WAN)), Application (Network Virtualization, Data Center Automation, Cloud Orchestration, Security Management, Storage Virtualization), Deployment Model (Cloud-based, On-premise, Hybrid), Industry Vertical (Telecommunications, IT & Cloud Service Providers, Finance & Banking, Healthcare, Manufacturing), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

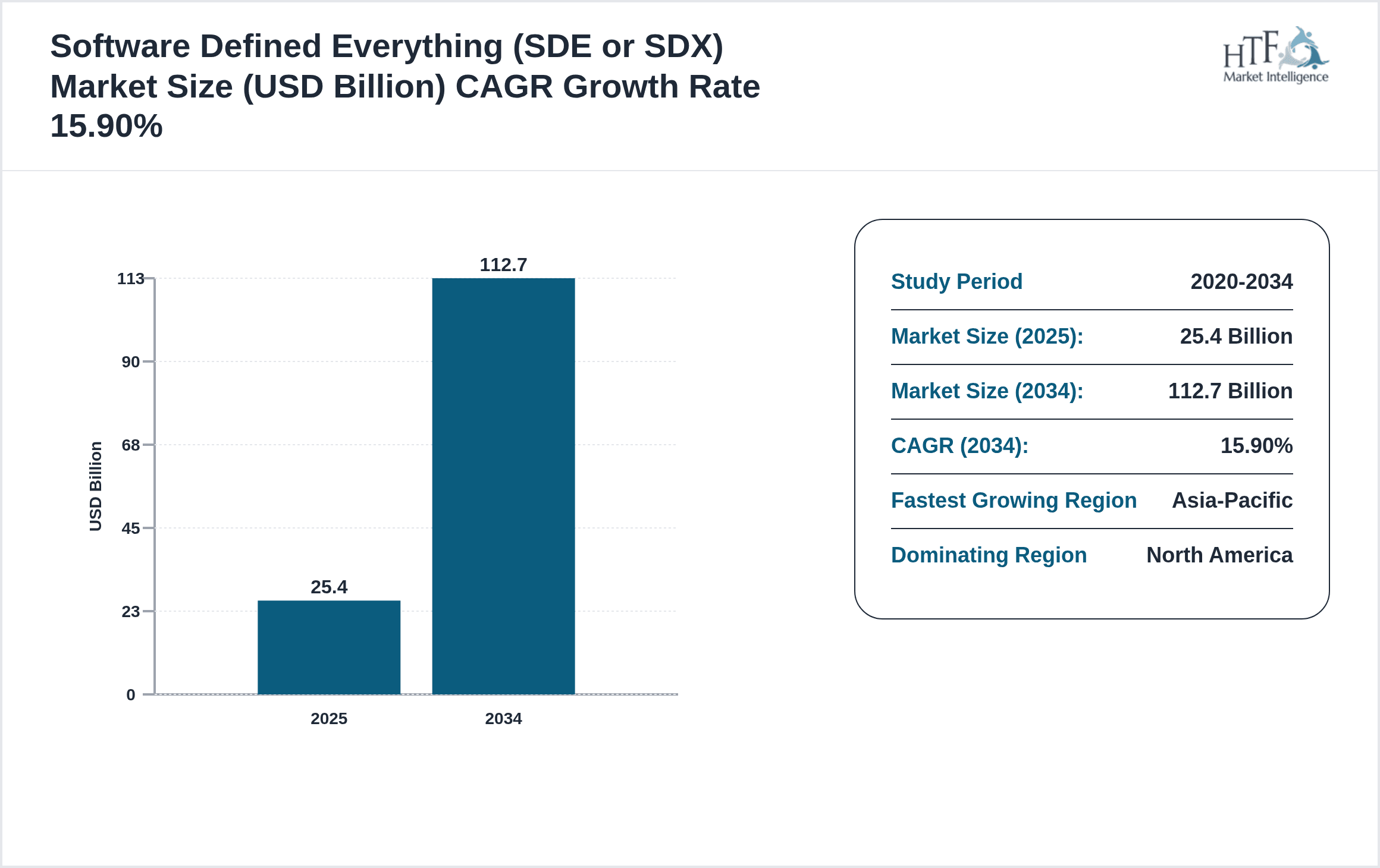

- •The global Software Defined Everything (SDE or SDX) market represents a transformative shift in IT infrastructure management by decoupling hardware from software control. This market includes key sub-segments such as software defined networking (SDN), software defined storage (SDS), software defined data centers (SDDC), software defined security, and SD-WAN. These technologies enable enterprises and service providers to achieve enhanced agility, centralized management, and efficient resource utilization across networks, storage, and compute environments. The market serves diverse applications including network virtualization, data center automation, cloud orchestration, security management, and storage virtualization, catering to verticals like telecommunications, cloud service providers, finance, and healthcare. Growth in this market is propelled by increasing demand for cloud services, edge computing, and the need for dynamic security frameworks. The market is geographically widespread with dominant adoption in North America, rapid growth in Asia-Pacific, and expanding interest across Europe, Latin America, and the Middle East & Africa. Strategic investments, technological innovations, and evolving regulatory landscapes continue to shape the competitive environment and growth trajectory of the SDE market globally.

- •Key market highlights include a current valuation of USD 25.4 Billion in 2024, with projections reaching USD 112.7 Billion by 2034, reflecting a strong CAGR of approximately 15.9%. Software Defined Networking remains the leading product type by market share, supported by robust demand from telecommunications and enterprise networking sectors. Software Defined Security is emerging as the fastest growing segment, driven by escalating cybersecurity needs and regulatory compliance requirements. Network virtualization holds the largest application share, while cloud orchestration follows as a rapidly expanding use case. North America continues to dominate due to advanced IT infrastructure and early technology adoption, whereas Asia-Pacific is the fastest growing region fueled by expanding digital economies and government initiatives promoting cloud and 5G deployments.

- •The value proposition of the Software Defined Everything market lies in its ability to deliver cost efficiencies, operational agility, and enhanced security. By abstracting physical hardware into programmable software layers, organizations can rapidly deploy, manage, and scale IT resources in alignment with dynamic business needs. This is particularly critical for industries undergoing digital transformation and adopting hybrid cloud or multi-cloud strategies. Stakeholders including technology vendors, system integrators, and end-users benefit from reduced complexity, improved service quality, and accelerated innovation cycles. The strategic importance of SDE technologies is underscored by increasing investments, partnerships, and a competitive landscape focused on delivering integrated, AI-enabled, and automated solutions to meet evolving enterprise demands globally.

Competitive Landscape

The competitive landscape of the global Software Defined Everything market is characterized by intense rivalry among established technology giants and innovative startups focusing on software-driven infrastructure solutions. Companies compete by leveraging advanced R&D capabilities to develop scalable, secure, and interoperable platforms. Strategies include broadening product portfolios through acquisitions, forming strategic partnerships to enhance service offerings, and investing in AI and machine learning to enable intelligent automation. Market positioning hinges on technological innovation, customer service excellence, and the ability to offer comprehensive end-to-end solutions that integrate networking, storage, security, and cloud orchestration seamlessly. Pricing strategies are influenced by the commoditization of software components and the demand for subscription-based models. Regional competition varies with North America and Europe dominated by mature players focusing on enterprise-grade solutions, while Asia-Pacific witnesses aggressive growth from both global players and local vendors catering to emerging digital infrastructure needs. Future trends include increased ecosystem collaboration and expansion into edge computing domains, intensifying competitive dynamics worldwide.

Leading Companies in Software Defined Everything Market

- •Cisco Systems, Inc. (United States)

- •VMware, Inc. (United States)

- •IBM Corporation (United States)

- •Microsoft Corporation (United States)

- •Juniper Networks, Inc. (United States)

- •Dell Technologies Inc. (United States)

- •Hewlett Packard Enterprise (United States)

- •Nokia Corporation (Finland)

- •Arista Networks, Inc. (United States)

- •Fortinet, Inc. (United States)

- •Huawei Technologies Co., Ltd. (China)

- •Citrix Systems, Inc. (United States)

- •Broadcom Inc. (United States)

- •Palo Alto Networks, Inc. (United States)

- •F5 Networks, Inc. (United States)

- •Extreme Networks, Inc. (United States)

- •Micro Focus International plc (United Kingdom)

- •Silver Peak Systems, Inc. (United States)

- •Citrix Systems, Inc. (United States)

- •Riverbed Technology, Inc. (United States)

- •Red Hat, Inc. (United States)

- •NetApp, Inc. (United States)

- •Ciena Corporation (United States)

- •Check Point Software Technologies Ltd. (Israel)

- •VMware Tanzu (United States)

Market Breakdown

- •By Product Type

- ◦Software Defined Networking (SDN)

- ◦Software Defined Storage (SDS)

- ◦Software Defined Data Center (SDDC)

- ◦Software Defined Security (SDSec)

- ◦Software Defined Wide Area Network (SD-WAN)

- •By Application

- ◦Network Virtualization

- ◦Data Center Automation

- ◦Cloud Orchestration

- ◦Security Management

- ◦Storage Virtualization

- •By Deployment Model

- ◦Cloud-based

- ◦On-premise

- ◦Hybrid

- •By Industry Vertical

- ◦Telecommunications

- ◦IT & Cloud Service Providers

- ◦Finance & Banking

- ◦Healthcare

- ◦Manufacturing

Growth Dynamics

- •Increasing cloud adoption globally drives the demand for flexible and scalable software-defined infrastructure, enabling enterprises to optimize network and compute resources efficiently. Leading cloud service providers are integrating SDE solutions to support hybrid and multi-cloud environments, enhancing operational agility and cost savings.

- •Rising cybersecurity threats and regulatory compliance requirements fuel the growth of software defined security solutions. Enterprises are prioritizing dynamic security frameworks that integrate seamlessly with network and data center automation to safeguard critical assets in real-time.

- •Technological advancements in virtualization, AI-powered orchestration, and edge computing are catalyzing the expansion of software defined everything solutions. These innovations enable intelligent resource management and low-latency processing, crucial for 5G deployments and IoT applications.

- •Growing demand from telecommunications and enterprise sectors for network virtualization and SD-WAN solutions facilitates enhanced connectivity and cost-effective bandwidth management. Providers are leveraging SDE to offer differentiated services and improve customer experience.

- •Government initiatives promoting digital infrastructure modernization and smart city projects across Asia-Pacific and Europe are creating substantial growth opportunities for software defined everything technologies, accelerating adoption in public sector and utilities.

Market Trends

- •The integration of AI and machine learning within SDE platforms is becoming prevalent, enabling predictive analytics, automated fault detection, and self-healing networks that enhance reliability and reduce operational costs.

- •Hybrid deployment models combining on-premise and cloud-based software defined solutions are gaining traction, as organizations seek flexible infrastructure that balances control and scalability.

- •There is an increasing shift towards open-source software defined platforms, promoting interoperability and reducing vendor lock-in, supported by communities and industry alliances.

- •Edge computing integration with software defined data centers is emerging to address latency-sensitive applications in manufacturing, healthcare, and autonomous vehicles.

- •SDE vendors are focusing on delivering turnkey solutions that combine networking, security, and storage virtualization to provide unified management and reduce complexity for enterprises.

Market Opportunities

- •Expanding adoption of 5G networks globally opens opportunities for software defined networking and security solutions tailored for high-speed, low-latency connectivity requirements.

- •Growing small and medium enterprise (SME) segment demand for cost-effective cloud orchestration and SD-WAN services presents untapped market potential, especially in emerging economies.

- •Advancements in containerization and microservices architectures enable integration with software defined data centers, offering opportunities for innovative orchestration and automation tools.

- •Increasing focus on green IT and energy-efficient data centers drives development of software defined storage and compute solutions that optimize resource utilization.

- •Strategic partnerships between technology vendors and cloud providers facilitate co-innovation and faster go-to-market of comprehensive SDE solutions addressing diverse customer needs.

Market Challenges

- •Complexity in integrating disparate software defined components across network, storage, and security domains poses challenges for seamless orchestration and management.

- •High initial investment costs and requirement for skilled personnel limit adoption among smaller enterprises, especially in developing regions.

- •Interoperability issues between legacy infrastructure and new software defined technologies create barriers to smooth migration and scalability.

- •Regulatory uncertainties and varying compliance standards across regions complicate deployment of software defined security and data management solutions.

- •Rapid technological advancements require continuous innovation and product updates, challenging vendors to maintain competitive differentiation.

Regulatory Framework

- •The period from 2022 to 2024 saw the implementation of data privacy regulations such as GDPR in Europe and CCPA in North America, mandating stringent data protection measures that directly impact software defined security solutions and cloud orchestration practices.

- •New cybersecurity directives introduced in 2023 require enterprises to adopt advanced threat detection and response mechanisms, driving compliance-focused software defined security adoption globally.

- •International standards for network virtualization and interoperability, including those from IEEE and IETF, were updated between 2022-2024 to support standardized deployment of SDN and SD-WAN technologies.

- •Regional mandates in Asia-Pacific and Europe emphasize energy efficiency and carbon footprint reduction in data centers, influencing software defined storage and data center automation solutions to align with green IT policies.

- •Government incentives and funding programs launched in 2023 for digital infrastructure modernization in emerging markets have facilitated accelerated adoption of software defined everything platforms, especially in public sector deployments.

Market Intelligence

- •15th February 2025, Cisco Systems, Inc. launched a next-generation software defined networking platform integrated with AI-driven analytics and automation capabilities targeted at large enterprise and service provider segments. The platform aims to simplify network management, enhance security posture, and enable rapid service deployment across multi-cloud environments. This innovation supports hybrid cloud architectures and responds to increasing demands for intelligent network orchestration. The launch strengthens Cisco’s leadership in the SDN space while expanding its software-defined portfolio to meet evolving market needs. Source: Cisco Official Press Release

- •8th April 2025, VMware, Inc. introduced an advanced software defined data center solution featuring enhanced container orchestration and edge computing support. This product facilitates seamless hybrid cloud integration and accelerates application deployment with native Kubernetes support. VMware aims to capitalize on growing cloud-native workloads and edge infrastructure requirements, offering enterprises a unified platform for managing virtualized resources with improved scalability and security. The update reflects VMware’s strategic focus on cloud and edge convergence within the SDE market. Source: VMware Corporate Announcement

- •22nd January 2025, IBM Corporation announced a strategic alliance with leading cloud providers to co-develop software defined security frameworks that leverage AI and blockchain technologies for real-time threat intelligence sharing. This initiative is designed to bolster enterprise cybersecurity across hybrid and multi-cloud environments, addressing regulatory compliance and advanced persistent threats. The collaboration aims to deliver integrated security automation and enhanced visibility, positioning IBM as a pioneer in next-generation security solutions within the software defined everything ecosystem. Source: IBM Newsroom

- •30th March 2025, Microsoft Corporation completed the acquisition of a cloud-native SD-WAN startup to enhance its Azure networking portfolio. This acquisition enables Microsoft to offer scalable, secure, and automated WAN connectivity solutions optimized for cloud-first enterprises. The integration is expected to accelerate customer adoption of hybrid cloud networking services and strengthen Microsoft’s competitive positioning against other cloud providers offering software defined network services. Source: Microsoft Investor Relations

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 25.4 Billion |

| Forecast Year Market Size | USD 112.7 Billion |

| CAGR | 15.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 15.9% |

| Scope of Report | Market is segmented by Product Type (Software Defined Networking (SDN), Software Defined Storage (SDS), Software Defined Data Center (SDDC), Software Defined Security (SDSec), Software Defined Wide Area Network (SD-WAN)), Application (Network Virtualization, Data Center Automation, Cloud Orchestration, Security Management, Storage Virtualization), Deployment Model (Cloud-based, On-premise, Hybrid), Industry Vertical (Telecommunications, IT & Cloud Service Providers, Finance & Banking, Healthcare, Manufacturing) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Cisco Systems, Inc. (United States), VMware, Inc. (United States), IBM Corporation (United States), Microsoft Corporation (United States), Juniper Networks, Inc. (United States) |

Global Software Defined Everything Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.