EMEA Customer Relationship Management Software Market - Outlook 2025-2034

EMEA Customer Relationship Management Software Market is segmented by CRM Software Type (On-Premise CRM, Cloud-Based CRM, Hybrid CRM, Open Source CRM, Social CRM), Application (Sales Automation, Customer Service & Support, Marketing Automation, Analytics & Reporting, Customer Data Management), Deployment Model (Cloud Deployment, On-Premise Deployment, Hybrid Deployment), Industry Vertical (Banking, Financial Services and Insurance (BFSI), Retail and Consumer Goods, Telecommunications and IT, Healthcare and Pharmaceuticals, Manufacturing and Industrial), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Customer Relationship Management (CRM) Software Market is a dynamic sector involving comprehensive software solutions designed to optimize customer interactions, sales processes, marketing automation, and customer support across a wide array of industries. This market includes multiple CRM types such as on-premise, cloud-based, hybrid, open source, and social CRM, catering to the evolving needs of enterprises seeking to enhance customer engagement and operational efficiency. With applications spanning sales automation, customer service, marketing automation, analytics, and customer data management, the market is pivotal for businesses aiming to foster long-term customer loyalty and data-driven decision-making. The EMEA region, comprising major economies like Germany, France, the UK, Italy, and Spain, exhibits significant CRM adoption driven by digital transformation initiatives, increasing focus on customer-centric strategies, and regulatory compliance requirements. As companies strive to deliver personalized experiences, the CRM software market continues to evolve with innovations in AI, cloud computing, and analytics, making it a critical element of business infrastructure across sectors such as BFSI, retail, telecommunications, and manufacturing.

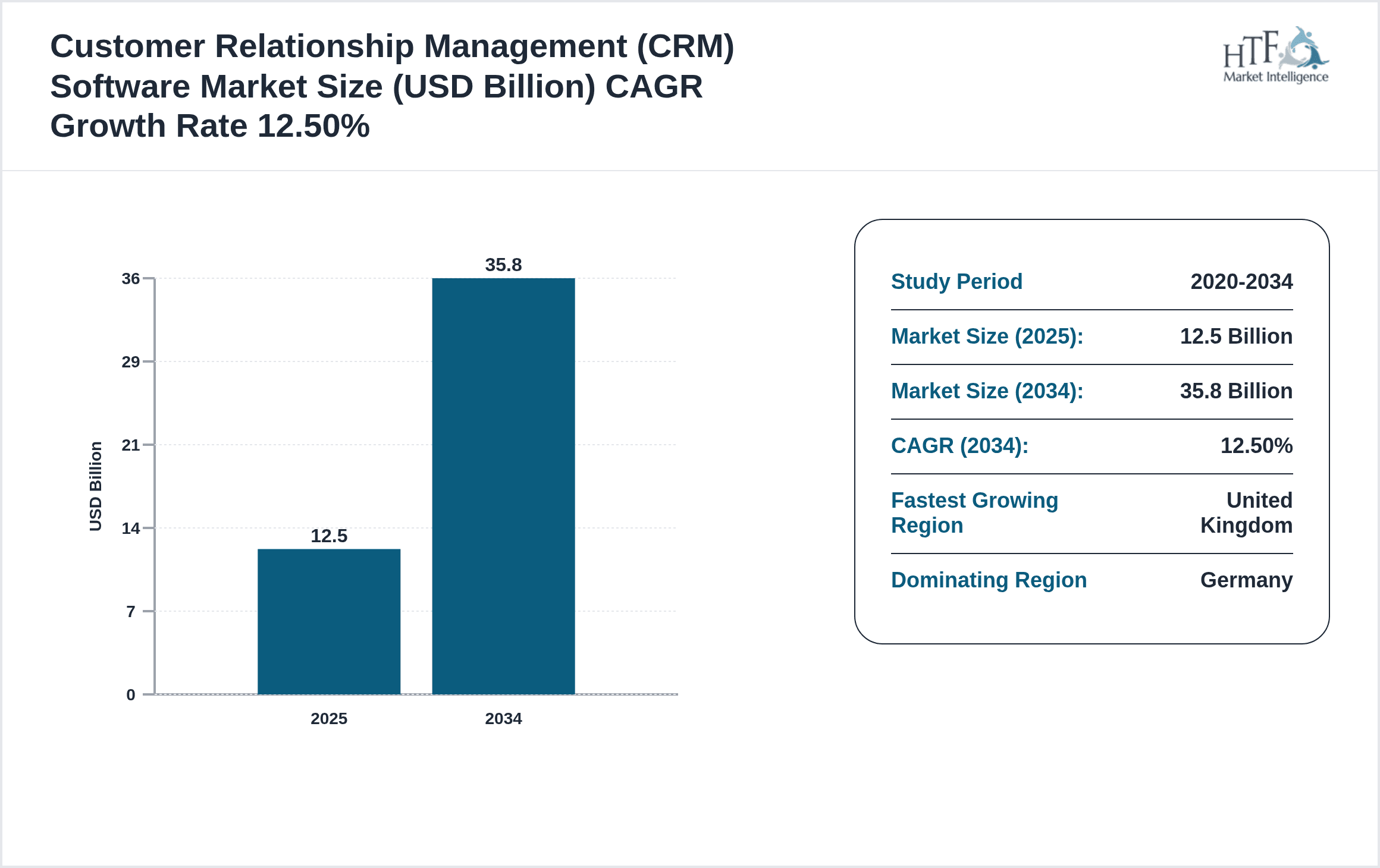

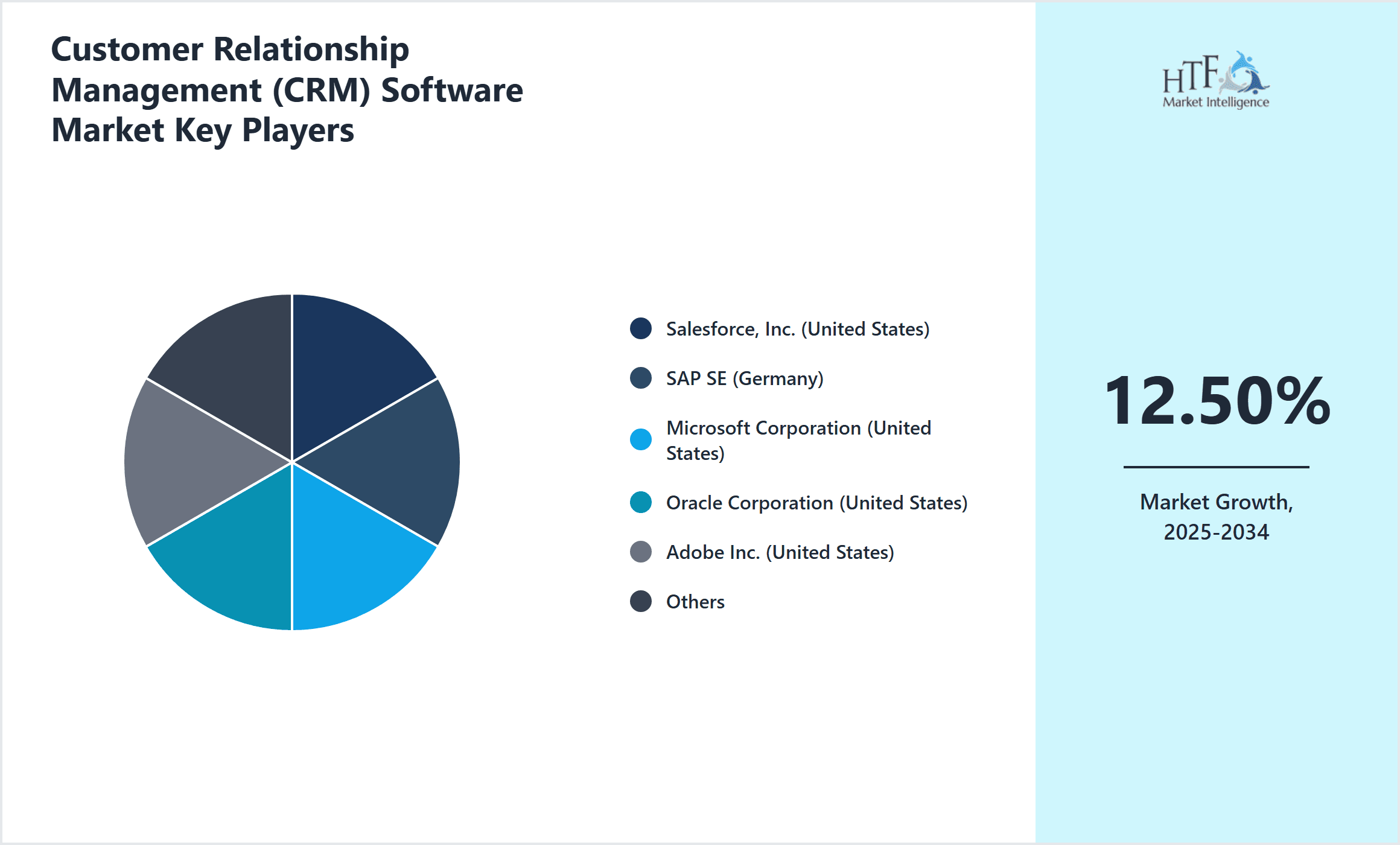

- •Key market highlights include a robust CAGR of approximately 12.5% projected through 2034, with market size expected to nearly triple from USD 12.5 Billion in 2025 to USD 35.8 Billion by 2034. Cloud-Based CRM emerges as the dominant product type, reflecting the growing preference for scalable and flexible solutions, while Social CRM is identified as the fastest growing segment, propelled by increased social media integration. Sales automation leads the application segment, followed closely by customer service and support, underscoring the emphasis on improving sales efficiency and customer satisfaction. Germany stands as the dominating regional market within EMEA, with the United Kingdom identified as the fastest growing country, indicative of varying adoption rates and market maturity across geographies. The market growth is accelerated by technological advancements, rising customer expectations, and increased investment in digital infrastructure across the region.

- •The value proposition of the EMEA CRM software market lies in its strategic importance for enterprises aiming to streamline customer interactions, enhance operational efficiency, and gain competitive advantage through data-driven customer insights. CRM solutions enable businesses to automate critical processes, personalize marketing efforts, and improve customer retention, thereby directly impacting revenue growth and brand loyalty. With the increasing adoption of cloud technologies and AI-powered analytics, CRM platforms offer scalable, cost-effective, and innovative tools that support digital transformation agendas. These solutions also help organizations comply with stringent data protection regulations prevalent in the EMEA region, such as GDPR, ensuring secure and transparent customer data handling. Overall, the CRM software market is a cornerstone for business growth, innovation, and customer experience management in the EMEA region.

Competitive Landscape

The EMEA Customer Relationship Management Software Market is characterized by intense competition among a mix of global technology giants and agile regional players. Market participants compete primarily on innovation, product capabilities, cloud adoption, and customer-centric features. Companies are investing heavily in AI, machine learning, and analytics integration to differentiate their offerings and address complex customer needs. Strategic partnerships, mergers and acquisitions, and geographic expansion are common tactics to increase market share and enhance service portfolios. Pricing strategies vary from subscription-based models for cloud solutions to license fees for on-premise deployments, catering to diverse customer preferences. Competitive advantages are often driven by the ability to provide customizable, scalable, and user-friendly platforms that comply with stringent regional data regulations. The rivalry also extends to service quality, integration capabilities, and after-sales support, shaping the evolving competitive dynamics within the EMEA CRM software landscape.

Leading Companies in Customer Relationship Management Software Market

- •Salesforce, Inc. (United States)

- •SAP SE (Germany)

- •Microsoft Corporation (United States)

- •Oracle Corporation (United States)

- •Adobe Inc. (United States)

- •HubSpot, Inc. (United States)

- •Zoho Corporation (India)

- •Sage Group plc (United Kingdom)

- •Freshworks Inc. (United States)

- •SugarCRM Inc. (United States)

- •Pegasystems Inc. (United States)

- •NICE Ltd. (Israel)

- •Netsuite Inc. (United States)

- •Creatio (United States)

- •Insightly Inc. (United States)

- •Bitrix24 (Russia)

- •Infor (United States)

- •SAP Customer Experience (Germany)

- •Oracle NetSuite (United States)

- •Zendesk, Inc. (United States)

- •Salesforce Europe Limited (Ireland)

- •BMC Software (United States)

- •Workday, Inc. (United States)

- •Cegid Group (France)

- •TIBCO Software Inc. (United States)

Market Breakdown

- •By CRM Software Type

- ◦On-Premise CRM

- ◦Cloud-Based CRM

- ◦Hybrid CRM

- ◦Open Source CRM

- ◦Social CRM

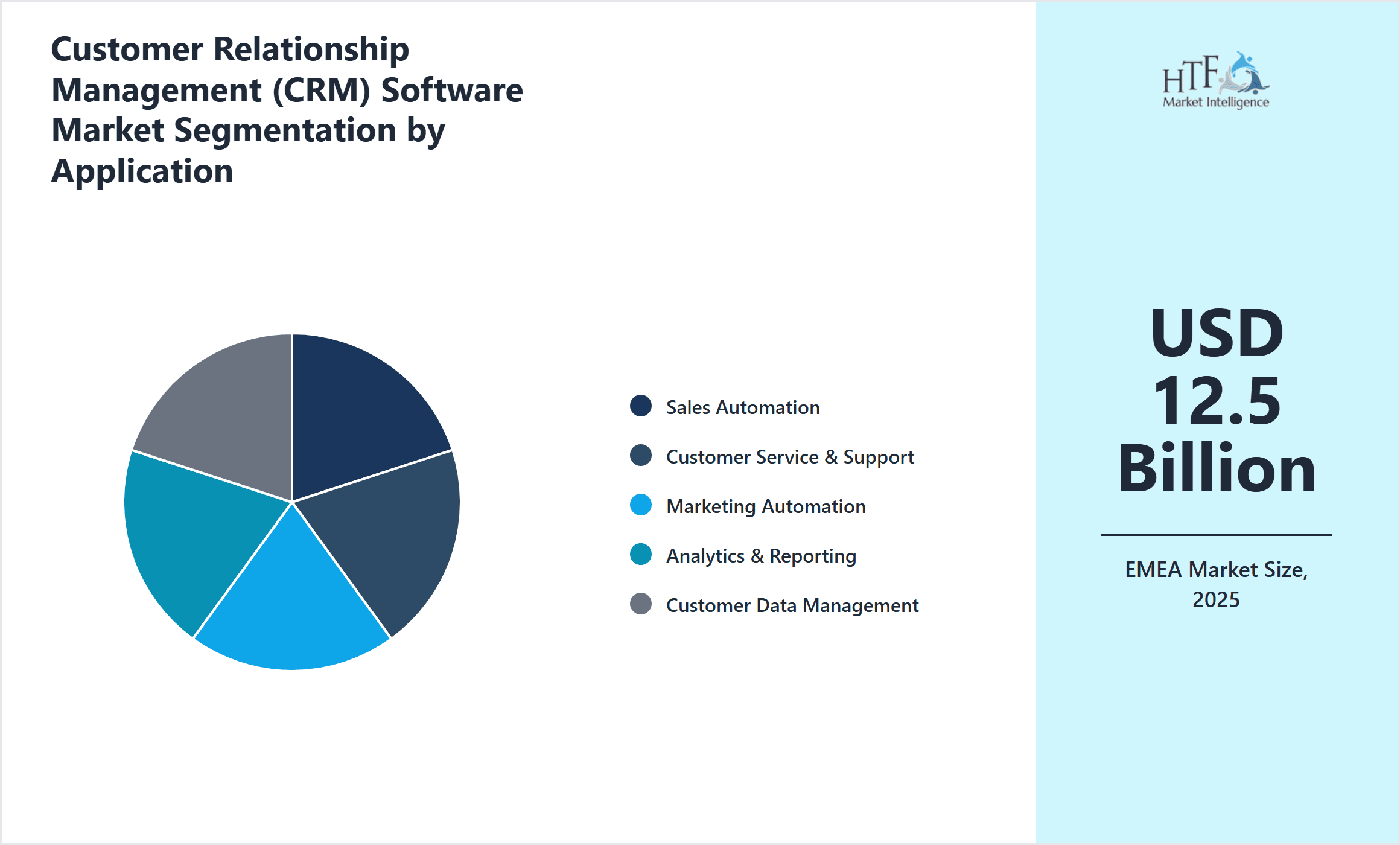

- •By Application

- ◦Sales Automation

- ◦Customer Service & Support

- ◦Marketing Automation

- ◦Analytics & Reporting

- ◦Customer Data Management

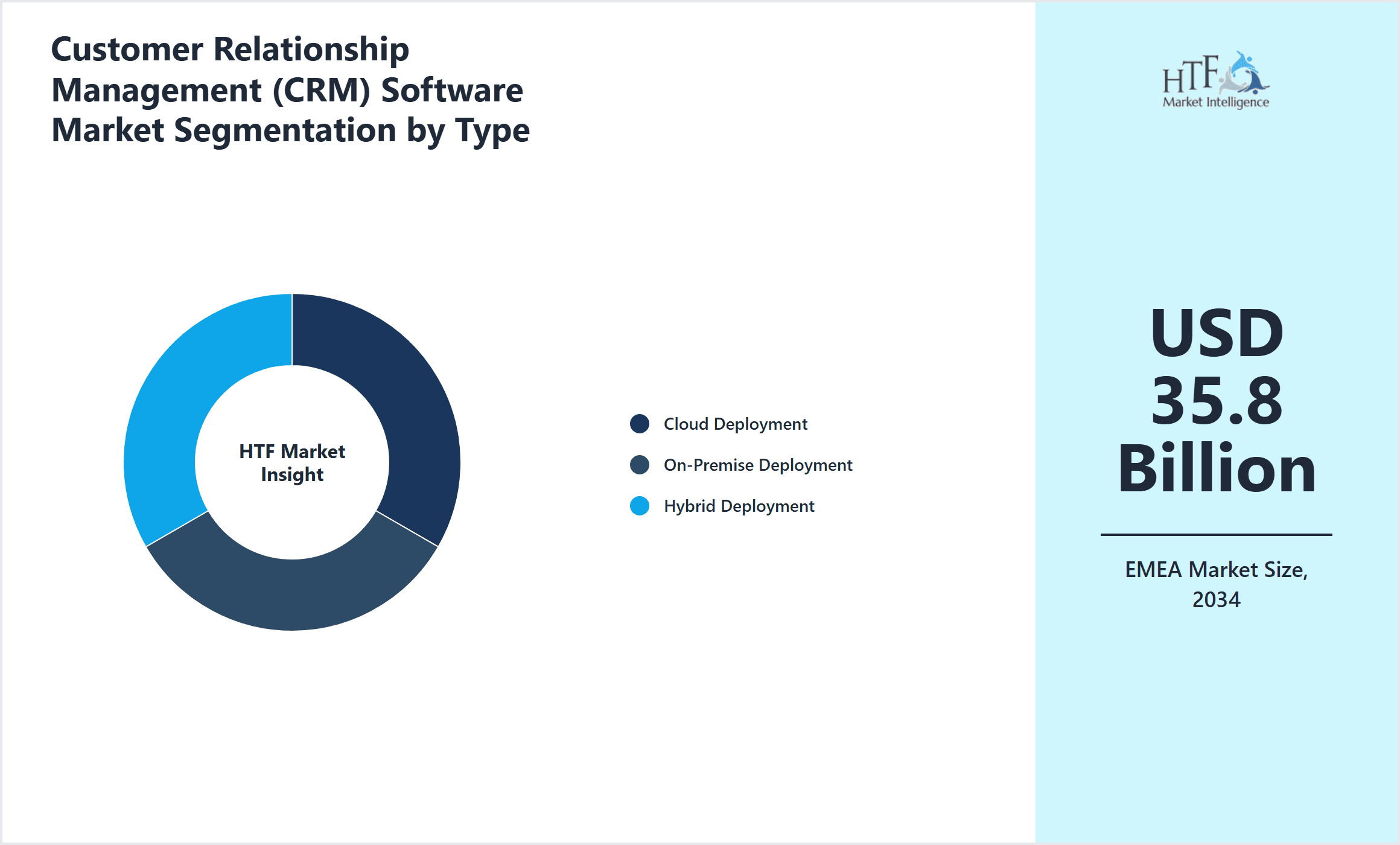

- •By Deployment Model

- ◦Cloud Deployment

- ◦On-Premise Deployment

- ◦Hybrid Deployment

- •By Industry Vertical

- ◦Banking, Financial Services and Insurance (BFSI)

- ◦Retail and Consumer Goods

- ◦Telecommunications and IT

- ◦Healthcare and Pharmaceuticals

- ◦Manufacturing and Industrial

Growth Dynamics

- •The rapid adoption of cloud computing in the EMEA region is a primary growth driver, providing scalable and cost-effective CRM solutions that accommodate both SMEs and large enterprises. This shift supports enhanced accessibility and collaboration, facilitating robust customer engagement strategies.

- •Increasing digital transformation initiatives across sectors such as banking, retail, and telecommunications are fueling demand for integrated CRM platforms that offer automation, analytics, and personalized marketing capabilities, thereby driving market expansion.

- •The proliferation of mobile devices and increasing internet penetration in emerging EMEA markets enable real-time customer interaction and data collection, further accelerating the adoption of advanced CRM software.

- •Stringent data protection regulations, including GDPR, create a demand for CRM solutions with strong compliance features, prompting vendors to innovate and adapt their products for secure data management, which propels market growth.

- •Rising customer expectations for personalized experiences and omnichannel engagement compel businesses to invest in sophisticated CRM tools that enhance customer insights and service delivery, thereby stimulating market development.

Market Trends

- •The integration of artificial intelligence and machine learning into CRM systems is becoming prevalent, enabling predictive analytics, automated customer interactions, and enhanced decision-making, which are transforming traditional CRM functionalities.

- •A notable trend is the growing preference for cloud-based CRM solutions due to their flexibility, reduced upfront costs, and ease of deployment, which is reshaping the CRM software landscape in the EMEA region.

- •Social CRM adoption is rising as companies increasingly leverage social media platforms to engage customers, manage reputation, and gather real-time feedback, fostering more dynamic customer relationships.

- •CRM vendors are expanding their offerings to include enhanced analytics and reporting features that provide deeper customer insights and marketing effectiveness measurement, driving smarter business strategies.

- •Collaborative CRM platforms facilitating cross-departmental synergy are gaining traction, promoting unified sales, marketing, and customer service workflows to improve overall customer experience and operational efficiency.

Market Opportunities

- •Emerging economies within the EMEA region present significant untapped potential for CRM adoption, especially among SMEs seeking affordable and scalable cloud-based solutions tailored to local business environments.

- •Integration of CRM software with IoT devices and big data analytics offers opportunities to deliver advanced customer insights and proactive service models, opening new avenues for innovation and growth.

- •The increasing demand for industry-specific CRM solutions, particularly in healthcare, manufacturing, and BFSI sectors, provides vendors with opportunities to develop customized offerings that address unique business challenges.

- •Strategic partnerships between CRM providers and telecommunication companies can facilitate bundled offerings and enhanced connectivity, accelerating CRM penetration in remote and underserved markets.

- •Expanding capabilities in social CRM and mobile CRM applications enable companies to capitalize on evolving consumer behaviors, improving engagement and loyalty across digital channels.

Market Challenges

- •High initial investment and integration complexity of CRM systems, especially in large enterprises with legacy infrastructure, pose significant adoption barriers and extend implementation timelines.

- •Concerns over data privacy and security compliance with regulations such as GDPR increase the complexity of CRM deployment, requiring continuous monitoring and updates to prevent breaches and penalties.

- •Fragmented market with a plethora of CRM vendors creates confusion among buyers, complicating the selection process and leading to suboptimal purchasing decisions.

- •Limited technical expertise and change management challenges within organizations hinder effective CRM utilization and reduce the realization of expected benefits.

- •Rapid technological changes require continuous investment in product upgrades and staff training, which can strain budgets and resources, particularly for small and medium-sized enterprises.

Regulatory Framework

- •Between 2020 and 2025, the European Union's General Data Protection Regulation (GDPR) has mandated stringent data privacy and protection standards, requiring CRM vendors and users in the EMEA region to implement robust data security measures and ensure customer consent management, significantly impacting product design and operational compliance.

- •The ePrivacy Directive, enforced alongside GDPR, governs electronic communications and marketing activities, imposing strict rules on data collection through cookies and electronic messaging, compelling CRM providers to integrate compliance capabilities into their platforms to manage opt-in/opt-out mechanisms effectively.

- •Country-specific data sovereignty laws enacted in nations like Germany and France require CRM data to be stored and processed within national borders, influencing the deployment models and data center locations for CRM providers operating in these countries.

- •Regulations on cybersecurity, such as the NIS Directive, have increased the need for CRM software to incorporate advanced security features and incident response protocols to protect customer data against cyber threats prevalent in digital business environments.

- •Government initiatives promoting digital transformation and data protection awareness have led to funding and incentives for organizations adopting compliant CRM solutions, fostering market growth and innovation across the EMEA region.

Market Intelligence

- •15th February 2025, Salesforce, Inc. expanded its EMEA cloud-based CRM portfolio by launching an AI-powered analytics module tailored for the retail sector, enabling enhanced customer insights and predictive sales forecasting. This innovation aims to bolster the digital transformation efforts of retailers across Germany, France, and the UK, driving efficiency and personalized customer engagement. The latest module integrates seamlessly with existing Salesforce platforms and complies fully with GDPR requirements, strengthening data privacy protections. Salesforce’s strategic focus on AI and industry-specific solutions underscores its commitment to maintaining market leadership in EMEA’s rapidly evolving CRM landscape. Source: Salesforce official press release

- •22nd October 2024, SAP SE unveiled a new hybrid CRM solution integrating on-premise and cloud capabilities designed to cater to large enterprises in regulated industries within EMEA. The product emphasizes data security and compliance, addressing concerns prevalent in BFSI and healthcare sectors. SAP’s innovation facilitates smoother data migration and customization while enhancing automation and analytics functionalities. This launch strengthens SAP’s position in the competitive CRM market by targeting organizations with complex infrastructure needs and stringent regulatory obligations. The hybrid model offers flexibility and scalability, appealing to a broad client base across multiple EMEA countries. Source: SAP corporate announcement

- •30th June 2024, Microsoft Corporation introduced an updated Dynamics 365 CRM suite featuring enhanced social CRM integration tools, aiming to improve customer engagement through social media analytics and sentiment tracking across EMEA markets. The update supports multilingual capabilities and regional compliance frameworks, enabling companies to better engage with diverse customer bases. Microsoft’s focus on social CRM reflects shifting market trends towards omnichannel customer service and real-time interaction, positioning Dynamics 365 as a versatile platform for enterprises seeking comprehensive CRM solutions. The rollout included targeted marketing campaigns in the UK, France, and Italy to boost adoption. Source: Microsoft press release

- •10th April 2025, HubSpot, Inc. announced a strategic partnership with Vodafone Group to integrate HubSpot’s CRM software with Vodafone’s 5G network services, aiming to deliver enhanced mobile CRM experiences for customers in Europe and the Middle East. This collaboration is expected to accelerate the deployment of mobile-first CRM solutions, enabling real-time data access and improved customer service responsiveness, particularly benefiting SMEs. The partnership also focuses on developing joint marketing initiatives and bundled offerings to increase CRM penetration in emerging EMEA markets. This initiative highlights the growing synergy between telecommunications and CRM technology providers in the region. Source: HubSpot official announcement

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Kingdom is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 35.8 Billion |

| CAGR | 12.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.3% |

| Scope of Report | Market is segmented by CRM Software Type (On-Premise CRM, Cloud-Based CRM, Hybrid CRM, Open Source CRM, Social CRM), Application (Sales Automation, Customer Service & Support, Marketing Automation, Analytics & Reporting, Customer Data Management), Deployment Model (Cloud Deployment, On-Premise Deployment, Hybrid Deployment), Industry Vertical (Banking, Financial Services and Insurance (BFSI), Retail and Consumer Goods, Telecommunications and IT, Healthcare and Pharmaceuticals, Manufacturing and Industrial) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Salesforce, Inc. (United States), SAP SE (Germany), Microsoft Corporation (United States), Oracle Corporation (United States), Adobe Inc. (United States), HubSpot, Inc. (United States), Zoho Corporation (India), Sage Group plc (United Kingdom), Freshworks Inc. (United States), SugarCRM Inc. (United States), Pegasystems Inc. (United States), NICE Ltd. (Israel), Netsuite Inc. (United States), Creatio (United States), Insightly Inc. (United States), Bitrix24 (Russia), Infor (United States), SAP Customer Experience (Germany), Oracle NetSuite (United States), Zendesk, Inc. (United States), Salesforce Europe Limited (Ireland), BMC Software (United States), Workday, Inc. (United States), Cegid Group (France), TIBCO Software Inc. (United States) |

EMEA Customer Relationship Management Software Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.