Global Orthopedic Device Market - Outlook 2025-2034

Global Orthopedic Device Market is segmented by Application (Joint Reconstruction, Spine, Trauma Fixation, Sports Medicine, Dental Implants), Type (Orthobiologics, Prosthetics, Surgical Instruments, Implants, Biodegradable Devices), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Orthopedic Device Market represents a dynamic and expanding sector focused on medical devices that aid in musculoskeletal health management. It includes various product categories such as orthobiologics, prosthetics, surgical instruments, implants, and biodegradable devices, serving applications in joint reconstruction, spine, trauma fixation, sports medicine, and dental implants. This market addresses the rising incidence of musculoskeletal disorders globally, fueled by aging demographics, increasing sports-related injuries, and advancements in surgical techniques. The integration of cutting-edge technologies like 3D printing and biomaterials has significantly enhanced device performance and patient outcomes. The market is segmented by product type, application, and geography, covering major regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Key stakeholders include hospitals, orthopedic clinics, and ambulatory surgical centers. The market's growth trajectory is shaped by innovation, regulatory frameworks, and evolving healthcare infrastructure, positioning it as a vital component in global healthcare delivery systems.

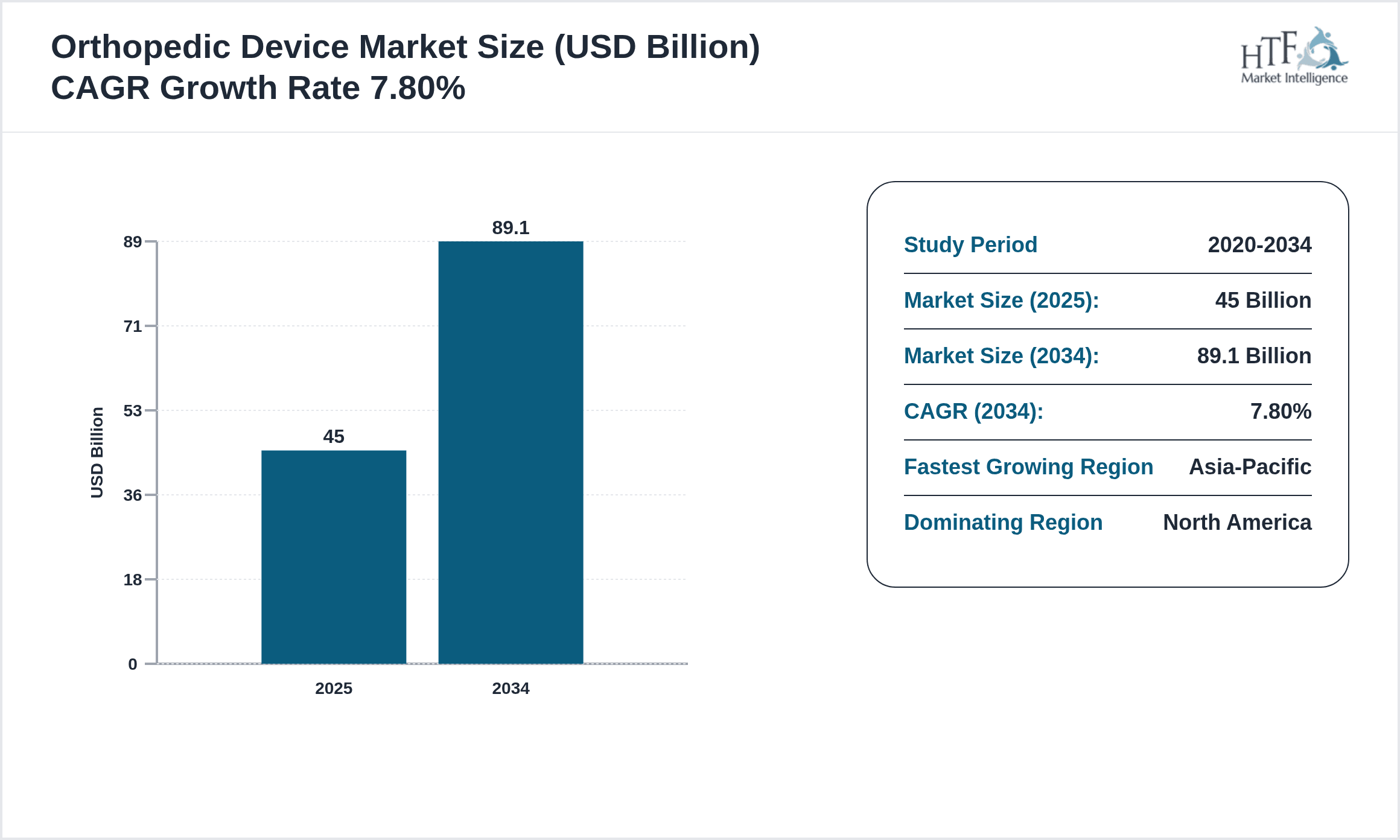

- •The market is expected to grow from USD 45.0 Billion in 2025 to USD 89.1 Billion by 2034, exhibiting a CAGR of 7.8%. Growth is primarily driven by technological advancements, rising orthopedic surgeries, and increasing prevalence of chronic diseases affecting bones and joints. North America currently dominates the market, supported by established healthcare infrastructure and high adoption rates of advanced orthopedic devices. Meanwhile, Asia-Pacific is the fastest-growing region due to improving healthcare access and rising investments in medical infrastructure. The leading product segment is orthobiologics, benefiting from their enhanced healing properties, while biodegradable devices are emerging as the fastest-growing category, propelled by demand for minimally invasive treatments. Joint reconstruction remains the largest application segment, followed closely by spinal implants, reflecting the high incidence of degenerative joint diseases and spinal disorders globally.

- •The orthopedic device market offers significant value to healthcare providers, device manufacturers, and patients by enabling improved mobility, reduced recovery times, and enhanced quality of life. With increasing orthopedic conditions worldwide, healthcare systems leverage these devices to reduce long-term disability and healthcare costs. Manufacturers invest in R&D to develop innovative solutions such as smart implants and personalized prosthetics, which align with precision medicine trends. Strategic importance lies in the market's capacity to address an aging global population's needs and the growing demand for minimally invasive surgeries. Additionally, emerging markets present untapped opportunities for expansion, making the orthopedic device sector a critical growth area within the broader medical devices industry.

Competitive Landscape

The competitive environment in the global orthopedic device market is characterized by intense rivalry among established multinational corporations and emerging regional players. Companies differentiate themselves through continuous innovation, strategic partnerships, and robust R&D investments aimed at developing advanced materials, minimally invasive surgical technologies, and patient-specific devices. Market leaders focus on expanding product portfolios and enhancing distribution channels to strengthen market presence globally. Mergers and acquisitions are frequent as firms seek to consolidate capabilities, broaden geographic reach, and access new technologies. Pricing strategies are influenced by reimbursement policies and the need to balance affordability with high-quality standards. Additionally, regulatory compliance and intellectual property protection play crucial roles in sustaining competitive advantages. The evolving market dynamics emphasize agility in responding to technological disruptions and shifting customer preferences, with companies increasingly adopting digital tools and data analytics to optimize operations and customer engagement. As a result, the landscape remains highly competitive, fostering innovation and driving market growth.

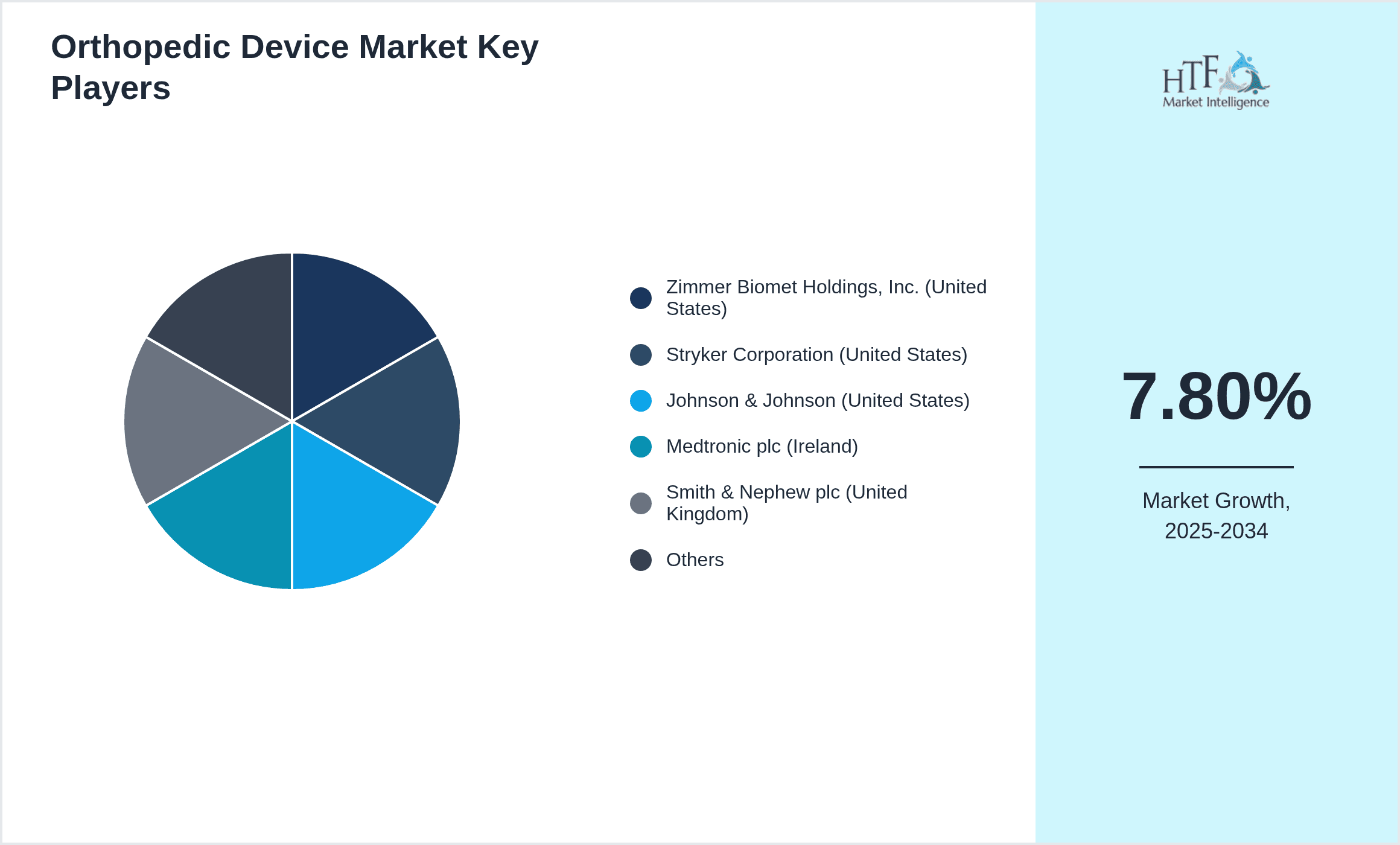

Leading Companies in Orthopedic Device Market

- •Zimmer Biomet Holdings, Inc. (United States)

- •Stryker Corporation (United States)

- •Johnson & Johnson (United States)

- •Medtronic plc (Ireland)

- •Smith & Nephew plc (United Kingdom)

- •DePuy Synthes (Johnson & Johnson Subsidiary) (United States)

- •DJO Global, Inc. (United States)

- •NuVasive, Inc. (United States)

- •B. Braun Melsungen AG (Germany)

- •Conformis, Inc. (United States)

- •Medacta International SA (Switzerland)

- •Orthofix International N.V. (United States)

- •Wright Medical Group N.V. (United States)

- •LimaCorporate S.p.A. (Italy)

- •Globus Medical, Inc. (United States)

- •Surgical Implant Generation Network (United States)

- •Exactech, Inc. (United States)

- •Aesculap Implant Systems LLC (Germany)

- •Ortho Clinical Diagnostics (United States)

- •Zimmer Biomet Robotics (United States)

- •DJ Orthopaedics, LLC (United States)

- •Integra LifeSciences Holdings Corporation (United States)

- •Smith & Nephew Endoscopy (United Kingdom)

- •Arthrex, Inc. (United States)

- •Baxter International Inc. (United States)

Orthopedic Device Market Segmentation

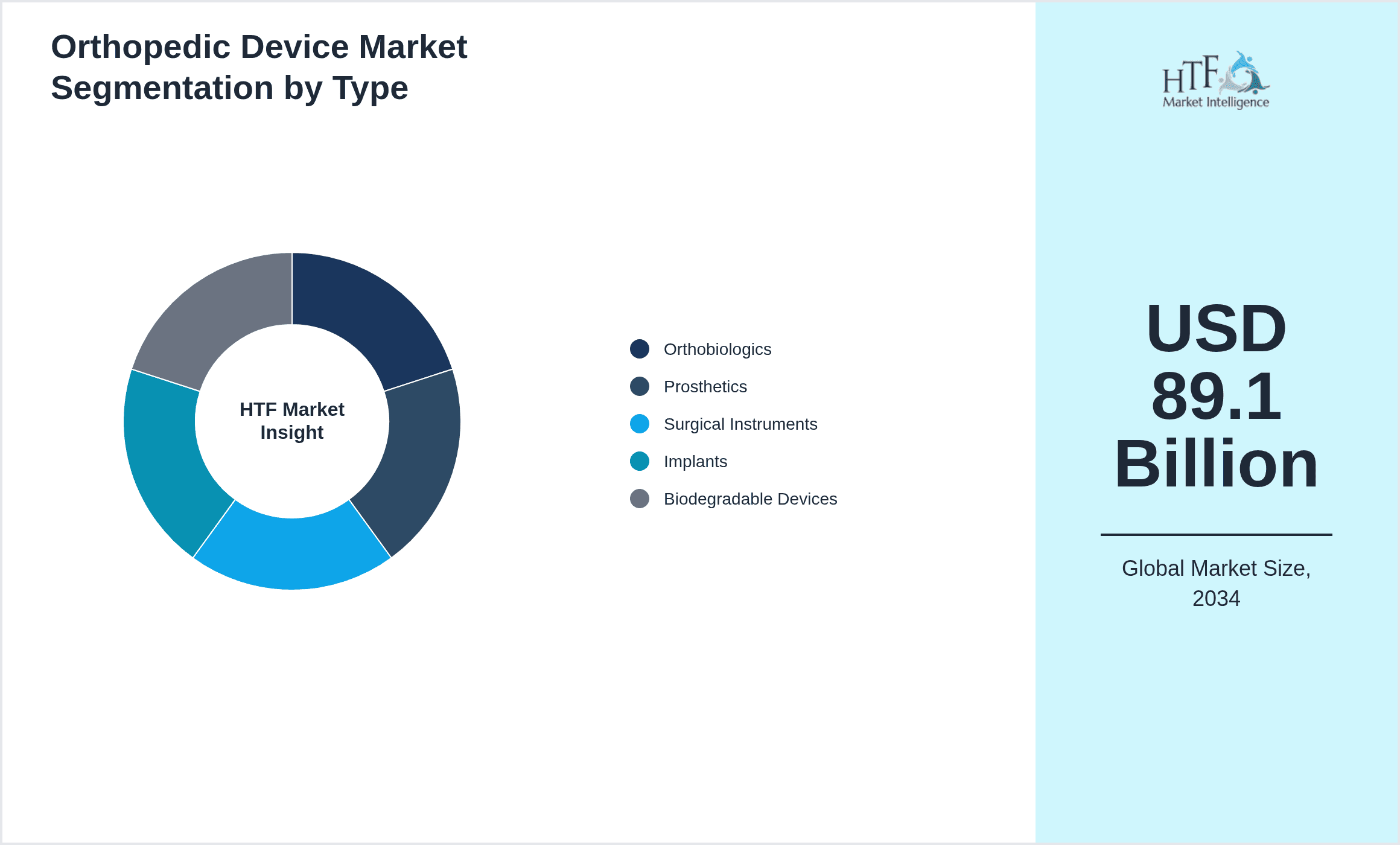

- •By Product Type

- ◦Orthobiologics

- ◦Prosthetics

- ◦Surgical Instruments

- ◦Implants

- ◦Biodegradable Devices

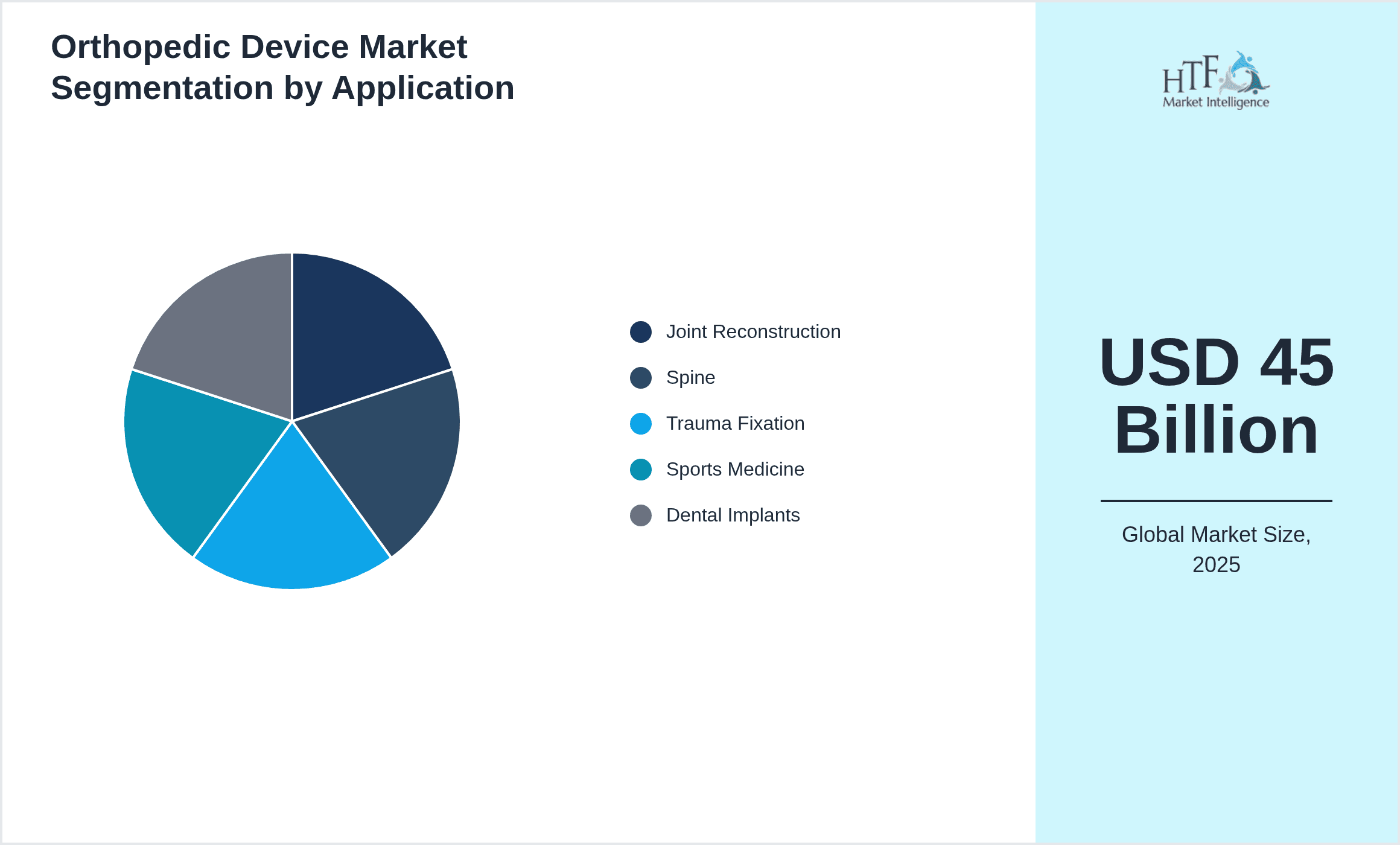

- •By Application

- ◦Joint Reconstruction

- ◦Spine

- ◦Trauma Fixation

- ◦Sports Medicine

- ◦Dental Implants

- •By End-User Facility

- ◦Hospitals

- ◦Orthopedic Clinics

- ◦Ambulatory Surgical Centers

- ◦Rehabilitation Centers

- •By Distribution Channel

- ◦Direct Sales

- ◦Third-Party Distributors

- ◦Online Sales Platforms

Growth Dynamics

- •The global orthopedic device market growth is propelled by the rising prevalence of musculoskeletal disorders, particularly among aging populations worldwide. Chronic conditions such as osteoarthritis and osteoporosis require advanced treatment solutions, boosting demand for implants and orthobiologics. Technological innovations, including 3D-printed prosthetics and smart surgical instruments, enhance surgical outcomes and patient recovery. Increased healthcare expenditure and growing awareness about orthopedic health further stimulate market expansion. Moreover, rising sports-related injuries and the preference for minimally invasive surgeries open new avenues for market growth. The integration of digital technology in orthopedic procedures improves precision and reduces complications, making devices more appealing to healthcare providers globally.

- •Investment in research and development is accelerating, leading to novel biomaterials and personalized implants that cater to specific patient needs. Governments and private organizations are funding orthopedic healthcare infrastructure, especially in emerging economies, which drives demand for advanced devices. The expansion of healthcare insurance coverage in various regions also enhances accessibility to orthopedic treatments. Additionally, increasing adoption of robotic-assisted surgeries and navigation systems is transforming the orthopedic surgical landscape, contributing to market growth. These dynamics collectively enhance treatment efficacy, reduce hospital stays, and lower overall healthcare costs, further incentivizing the use of orthopedic devices.

- •The growing geriatric population globally is a significant factor, as age-related degenerative diseases increase the need for joint replacements and spine surgeries. Rising incidence of road accidents and trauma cases also contribute to higher demand for trauma fixation devices. Furthermore, the sports medicine segment is expanding due to higher participation in athletic activities and awareness about injury prevention. Emerging markets are witnessing rapid urbanization and lifestyle changes, increasing orthopedic device adoption. Enhanced patient education and digital health platforms support early diagnosis and timely intervention, facilitating market growth. These factors combine to create a robust demand pipeline for orthopedic devices worldwide.

- •Regulatory approvals and streamlined clinical trial processes have accelerated product launches, aiding market expansion. Collaborations between device manufacturers and healthcare providers foster innovation and improve device relevance. The integration of artificial intelligence and machine learning in device design and surgical planning is emerging as a key growth driver. Environmental sustainability concerns are prompting the development of biodegradable and eco-friendly orthopedic devices, attracting a new segment of environmentally conscious consumers and institutions. Overall, these multifaceted growth drivers position the orthopedic device market for sustained expansion over the forecast period.

- •The rising demand for personalized and precision orthopedic devices is reshaping market dynamics. Customized implants and patient-specific surgical tools reduce complications and enhance recovery rates. Telemedicine and digital monitoring tools are increasingly integrated with orthopedic care to provide continuous patient support post-surgery. These technological advancements improve patient outcomes and satisfaction, which in turn drive adoption rates. Strategic partnerships and collaborations between technology firms and orthopedic device manufacturers are facilitating the development of innovative solutions, further propelling market growth globally.

Market Trends

- •One prominent trend in the orthopedic device market is the increasing adoption of minimally invasive surgical techniques supported by advanced instruments and implants. This shift reduces patient trauma and recovery time, improving overall care quality. Companies are investing in developing robotic-assisted surgery platforms that enhance precision and reduce surgeon fatigue. The integration of digital imaging and navigation systems is also gaining traction, enabling better surgical planning and execution.

- •The rise of 3D printing technology is revolutionizing the production of orthopedic implants and prosthetics. Customized devices tailored to individual anatomical requirements improve fit and function, leading to better clinical outcomes. Several manufacturers have introduced 3D-printed implants that offer enhanced durability and biocompatibility, which is reshaping the competitive landscape.

- •Sustainability and eco-friendly product development are emerging as strategic trends. Biodegradable implants and environmentally responsible manufacturing processes are increasingly prioritized to address environmental concerns. This trend aligns with growing regulatory pressures and consumer demand for sustainable healthcare solutions.

- •Digital health integration, including wearable sensors and remote monitoring, is becoming a key market driver. These technologies facilitate continuous patient monitoring and post-operative care, reducing hospital readmissions and enhancing recovery. Companies are collaborating with tech firms to develop comprehensive orthopedic care ecosystems.

- •Collaborative innovation through partnerships between medical device companies, research institutions, and healthcare providers is accelerating product development cycles. Such collaborations foster knowledge sharing and resource pooling, enabling faster commercialization of cutting-edge orthopedic technologies and expanding market reach.

- •There is an increased focus on emerging markets, with manufacturers tailoring solutions to regional needs and cost sensitivities. This localization strategy helps capture growth opportunities in Asia-Pacific, Latin America, and the Middle East & Africa, where demand for orthopedic devices is rapidly rising due to improving healthcare infrastructure.

- •The evolution of artificial intelligence and machine learning applications in diagnostics and surgical assistance is predicted to disrupt traditional orthopedic device manufacturing. These technologies enhance decision-making, patient-specific treatment planning, and predictive maintenance of devices, offering a competitive edge to early adopters.

Market Opportunities

- •Emerging markets present significant opportunities due to rising healthcare expenditure and increasing incidence of orthopedic conditions. Companies can capitalize on growing urban populations and expanding insurance coverage to introduce affordable and innovative devices tailored to local needs. These regions offer untapped potential for growth beyond traditional developed markets.

- •Innovation in biodegradable and smart orthopedic implants offers a promising avenue for market expansion. These devices reduce the risk of long-term complications and facilitate better integration with biological tissues, attracting adoption from leading healthcare providers focused on advanced patient care.

- •The integration of digital technologies into orthopedic care such as teleorthopedics, remote monitoring, and AI-powered diagnostics opens new service models. Companies can develop comprehensive care solutions that extend beyond devices to patient management platforms, enhancing customer loyalty and market penetration.

- •Strategic partnerships and collaborations with technology firms and healthcare providers can accelerate innovation and market access. These alliances enable joint development of next-generation orthopedic solutions and facilitate entry into new geographic markets with established local expertise.

- •Growing demand for personalized medicine creates opportunities for customized implants and surgical tools. Advances in 3D printing and biomaterials allow manufacturers to offer patient-specific solutions, improving surgical outcomes and expanding addressable market segments.

- •The increasing focus on preventive orthopedic care and rehabilitation services generates demand for supportive devices and wearable technologies. Companies can diversify portfolios to include these complementary products, broadening revenue streams and enhancing patient engagement.

- •Government initiatives promoting healthcare digitization and medical device innovation provide funding and regulatory support. Leveraging these programs can reduce development costs and accelerate time-to-market for orthopedic device manufacturers, fostering competitive advantage.

Market Challenges

- •High costs associated with advanced orthopedic devices and surgeries restrict market access in price-sensitive regions, limiting penetration in emerging economies. Affordability remains a critical barrier despite growing demand, necessitating cost-effective innovation and flexible pricing strategies to expand reach.

- •Complex and stringent regulatory requirements across different countries create challenges in product approvals and market entry. Navigating diverse compliance frameworks demands significant resources and expertise, potentially delaying product launches and increasing costs for manufacturers.

- •Intense competition and market saturation in developed regions drive pricing pressures and margin erosion. Companies face challenges differentiating products and maintaining profitability amid aggressive pricing and commoditization of standard orthopedic devices.

- •Limited reimbursement policies in certain markets impede patient access to orthopedic treatments, affecting overall device demand. Uncertainty regarding coverage and payment models complicates market forecasting and investment decisions for stakeholders.

- •Technological complexity and the need for skilled healthcare professionals to operate advanced devices slow adoption rates in some regions. Training requirements and resistance to change among practitioners can hinder the uptake of innovative orthopedic solutions.

- •Supply chain disruptions and raw material shortages, exacerbated by global events, affect production continuity and cost stability. Dependence on specialized materials and components exposes manufacturers to volatility and operational risks.

- •Intellectual property challenges and counterfeit products pose risks to market integrity and company revenues. Protecting innovations while combating unauthorized replicas requires robust legal frameworks and enforcement mechanisms.

Regulatory Framework

- •Between 2020 and 2025, the global orthopedic device market has seen evolving regulatory standards emphasizing patient safety, clinical efficacy, and post-market surveillance. The U.S. FDA has updated its guidance on orthopedic implant approvals, incorporating more rigorous clinical trial data requirements and real-world evidence to ensure device reliability and performance. The EU’s Medical Device Regulation (MDR), enforced since 2021, has introduced stricter conformity assessments and traceability obligations, impacting manufacturers’ compliance strategies worldwide.

- •Several countries have harmonized their medical device frameworks with international standards such as ISO 13485 and IMDRF guidelines, facilitating smoother global market entry. Regulatory bodies have also accelerated review processes for breakthrough orthopedic technologies to promote innovation while maintaining safety standards. These developments have increased the complexity of regulatory landscapes but provide clearer pathways for novel device commercialization.

- •Environmental and sustainability regulations are influencing orthopedic device manufacturing, encouraging the adoption of eco-friendly materials and waste reduction practices. Compliance with these regulations requires investments in sustainable product design and manufacturing processes, aligning with global initiatives to reduce healthcare environmental footprints.

- •Data privacy and cybersecurity regulations have become increasingly relevant as orthopedic devices integrate digital components and connectivity features. Regulatory agencies now mandate robust data protection measures and vulnerability assessments to safeguard patient information and device integrity.

- •Government incentives and reimbursement policy reforms in several regions aim to improve access to advanced orthopedic treatments. These policies support innovative device adoption by providing financial coverage and encouraging value-based care models, thus shaping market growth dynamics.

Market Intelligence

- •15th March 2025, Zimmer Biomet Holdings, Inc. unveiled a new line of biodegradable orthopedic implants designed to accelerate bone healing and reduce the need for secondary surgeries. These implants leverage advanced biomaterials that safely degrade within the body, minimizing long-term complications. The launch targets joint reconstruction and trauma fixation segments, aiming to improve patient outcomes and reduce healthcare costs. Zimmer Biomet’s initiative reflects growing industry focus on sustainable and patient-friendly device solutions, positioning the company as an innovator in the orthopedic device market. This product line is expected to gain rapid adoption, particularly in regions emphasizing minimally invasive surgical options. Source: Official Zimmer Biomet Press Release

- •10th July 2024, Stryker Corporation introduced an AI-powered surgical navigation platform integrated with its orthopedic implant systems. The platform enhances surgical precision by providing real-time imaging and analytics, reducing operative times and improving implant placement accuracy. Designed for spine and joint reconstruction surgeries, this innovation aligns with trends towards digital healthcare and personalized treatment. Stryker’s launch underscores the growing convergence of AI technology and orthopedic care, offering surgeons enhanced decision-making tools and improving patient recovery trajectories. This strategic move strengthens Stryker’s competitive position in the global market by addressing evolving clinical needs. Source: Stryker Official Website

- •22nd January 2025, Medtronic plc expanded its orthopedic portfolio through a strategic partnership with a leading 3D printing firm to develop customized prosthetics and implants. The collaboration aims to accelerate the production of patient-specific devices, leveraging additive manufacturing to improve fit and function. This initiative targets the growing demand for personalized orthopedic solutions and supports Medtronic’s commitment to innovation and patient-centric care. The partnership is expected to enhance operational efficiencies and market responsiveness, particularly in the spine and trauma fixation segments. Source: Medtronic Corporate Announcement

- •5th September 2025, Smith & Nephew plc completed the acquisition of a sports medicine device startup specializing in advanced arthroscopic instruments. This acquisition expands Smith & Nephew’s capabilities in minimally invasive surgical technologies and strengthens its foothold in the sports medicine market segment. The integration of the startup’s proprietary technology accelerates product development cycles and enhances the company’s competitive edge. This strategic acquisition aligns with Smith & Nephew’s growth objectives and market demand for innovative, patient-friendly orthopedic solutions. Source: Smith & Nephew Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45 Billion |

| Forecast Year Market Size | USD 89.1 Billion |

| CAGR | 7.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.5% |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Zimmer Biomet Holdings, Inc. (United States), Stryker Corporation (United States), Johnson & Johnson (United States), Medtronic plc (Ireland), Smith & Nephew plc (United Kingdom), DePuy Synthes (Johnson & Johnson Subsidiary) (United States), DJO Global, Inc. (United States), NuVasive, Inc. (United States), B. Braun Melsungen AG (Germany), Conformis, Inc. (United States), Medacta International SA (Switzerland), Orthofix International N.V. (United States), Wright Medical Group N.V. (United States), LimaCorporate S.p.A. (Italy), Globus Medical, Inc. (United States), Surgical Implant Generation Network (United States), Exactech, Inc. (United States), Aesculap Implant Systems LLC (Germany), Ortho Clinical Diagnostics (United States), Zimmer Biomet Robotics (United States), DJ Orthopaedics, LLC (United States), Integra LifeSciences Holdings Corporation (United States), Smith & Nephew Endoscopy (United Kingdom), Arthrex, Inc. (United States), Baxter International Inc. (United States) |

Global Orthopedic Device Market - Outlook 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.