Europe Inferior Vena Cava (IVC) Filters Market - Europe Industry Size & Growth Analysis 2025-2034

Europe Inferior Vena Cava (IVC) Filters Market is segmented by Type (Permanent Inferior Vena Cava Filters, Retrievable Inferior Vena Cava Filters, Convertible Inferior Vena Cava Filters, Bioconvertible Inferior Vena Cava Filters, Coated Inferior Vena Cava Filters), Application (Deep Vein Thrombosis, Pulmonary Embolism, Trauma Patients, Cancer Patients, Others), Service Type (Implantation Procedures, Filter Retrieval Procedures, Follow-up and Monitoring Services, Device Maintenance and Support), Deployment Model (Hospital-based Implantation, Ambulatory Surgical Centers, Specialized Vascular Clinics), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Inferior Vena Cava (IVC) Filters market is a specialized medical device sector focusing on devices designed to prevent life-threatening pulmonary embolisms by capturing emboli migrating through the inferior vena cava. These filters play a crucial role in managing patients with deep vein thrombosis, trauma, cancer, and other high-risk conditions requiring thromboembolism prevention. The market covers various product types including permanent, retrievable, convertible, bioconvertible, and coated filters, each catering to specific clinical needs and patient safety profiles. Europe’s healthcare infrastructure, coupled with rising prevalence of venous thromboembolic disorders and increasing awareness of minimally invasive interventions, propels the demand for advanced IVC filters. Regulatory support and technological advancements in materials and design enhance device efficacy and patient outcomes. The market is characterized by significant innovation, robust competition, and evolving clinical guidelines shaping device adoption across Germany, France, the UK, Italy, and Spain, which collectively dominate the regional landscape.

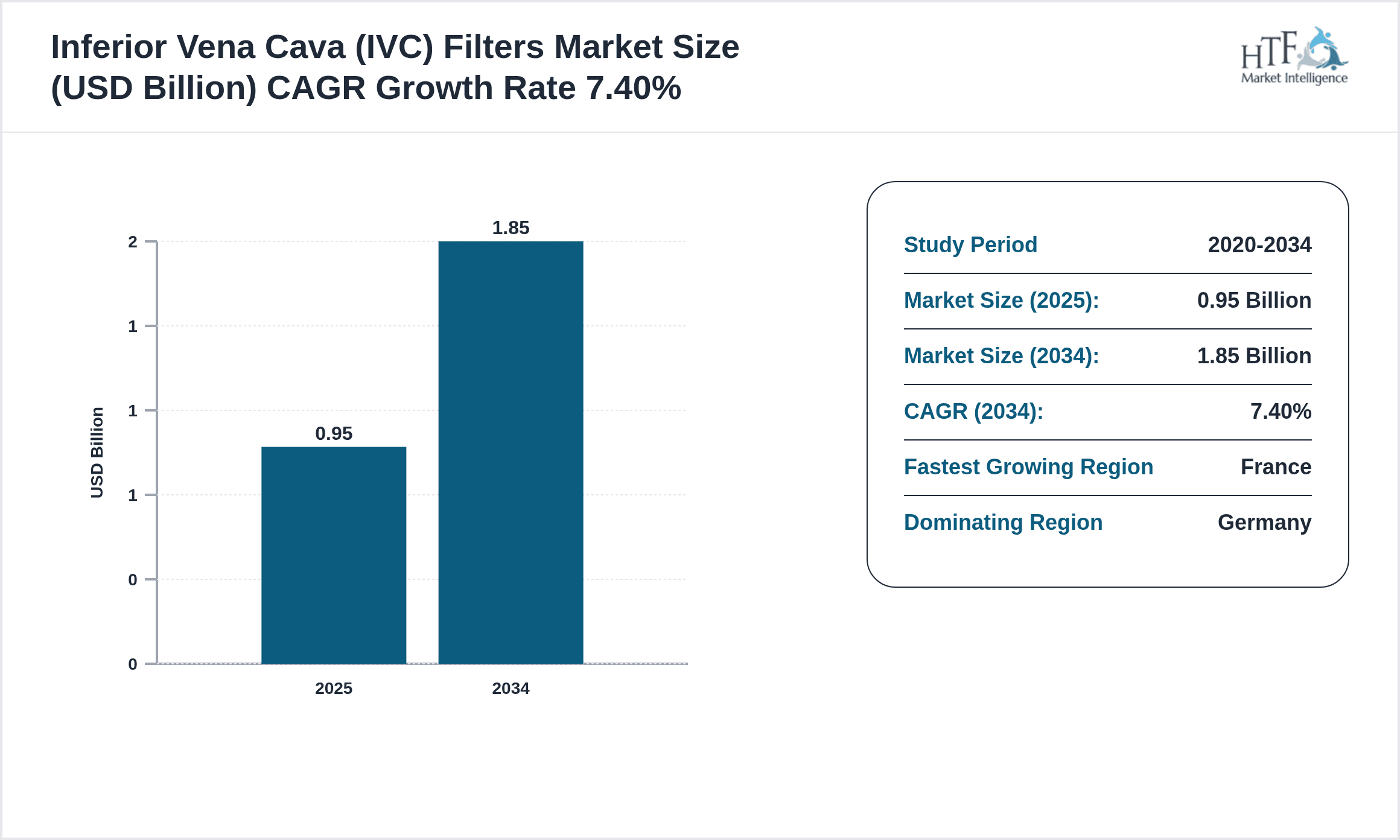

- •In 2025, the Europe IVC filters market is estimated at USD 0.95 Billion and is forecasted to reach USD 1.85 Billion by 2034, growing at a robust CAGR of 7.4%. This growth reflects increasing patient populations susceptible to thromboembolic events, expanding healthcare expenditures, and the rising adoption of retrievable and bioconvertible filters due to their safety and flexibility benefits. Germany leads the market share owing to advanced healthcare infrastructure and high awareness, while France emerges as the fastest-growing country driven by favorable reimbursement policies and innovative clinical practices. Key market drivers include rising incidence of deep vein thrombosis, technological advancements in filter designs, and increasing geriatric population. Challenges include concerns regarding filter-related complications and stringent regulatory requirements. However, opportunities lie in expanding indications, product innovations, and penetration into emerging European countries.

- •The Europe Inferior Vena Cava Filters market offers significant strategic value to medical device manufacturers, healthcare providers, and investors focusing on minimally invasive vascular interventions. The evolving clinical guidelines and technological innovations provide avenues for differentiated product development and enhanced patient safety profiles. Stakeholders benefit from the expanding patient base, rising awareness of venous thromboembolism risks, and supportive reimbursement frameworks across major European countries. The market’s growth trajectory underscores the importance of regulatory compliance, clinical evidence generation, and strategic partnerships to capture emerging opportunities. Overall, the market represents a critical component of cardiovascular disease management in Europe with promising long-term growth potential.

Competitive Landscape

The Europe Inferior Vena Cava (IVC) Filters market is highly competitive with a mix of global medical device giants and regional specialized manufacturers striving for technological leadership and market share. Companies focus on innovation through the development of retrievable and bioconvertible filters that minimize complications and improve patient outcomes. Strategic partnerships, acquisitions, and collaborations are common to expand product portfolios and enter new markets. Pricing strategies emphasize balancing cost-effectiveness with premium features to appeal to healthcare providers and payers. Regulatory compliance and clinical trial data play pivotal roles in market positioning. Distribution channels leverage hospital procurement networks and specialized vascular surgery centers. The competitive landscape is shaped by rapid technology adoption, increasing product approvals, and growing emphasis on patient safety, which collectively drive continuous innovation and differentiation among key players.

Prominent Players in Inferior Vena Cava (IVC) Filters Market

- •Cook Medical (United States)

- •C.R. Bard (United States)

- •B. Braun Melsungen AG (Germany)

- •Boston Scientific Corporation (United States)

- •Terumo Corporation (Japan)

- •Cardinal Health, Inc. (United States)

- •Teleflex Incorporated (United States)

- •Becton, Dickinson and Company (United States)

- •Medtronic plc (Ireland)

- •Johnson & Johnson (United States)

- •Sorin Group (Italy)

- •AngioDynamics, Inc. (United States)

- •Vascular Solutions, Inc. (United States)

- •Merit Medical Systems, Inc. (United States)

- •Penumbra, Inc. (United States)

- •Endologix, Inc. (United States)

- •Balt Extrusion (France)

- •LivaNova PLC (United Kingdom)

- •Terumo Europe NV (Belgium)

- •Nipro Corporation (Japan)

- •Hansen Medical, Inc. (United States)

- •Medacta International SA (Switzerland)

- •Smith & Nephew plc (United Kingdom)

- •W.L. Gore & Associates (United States)

- •Cook Group Incorporated (United States)

Market Breakdown

- •By Type

- ◦Permanent Inferior Vena Cava Filters

- ◦Retrievable Inferior Vena Cava Filters

- ◦Convertible Inferior Vena Cava Filters

- ◦Bioconvertible Inferior Vena Cava Filters

- ◦Coated Inferior Vena Cava Filters

- •By Application

- ◦Deep Vein Thrombosis

- ◦Pulmonary Embolism

- ◦Trauma Patients

- ◦Cancer Patients

- ◦Others

- •By Service Type

- ◦Implantation Procedures

- ◦Filter Retrieval Procedures

- ◦Follow-up and Monitoring Services

- ◦Device Maintenance and Support

- •By Deployment Model

- ◦Hospital-based Implantation

- ◦Ambulatory Surgical Centers

- ◦Specialized Vascular Clinics

Growth Dynamics

The Europe Inferior Vena Cava Filters market growth is primarily driven by the increasing prevalence of venous thromboembolism, particularly deep vein thrombosis and pulmonary embolism, fueled by aging populations and rising chronic diseases. Enhanced clinical awareness and adoption of minimally invasive vascular interventions have increased demand for advanced IVC filters. Technological innovations, such as bioconvertible filters that reduce long-term complications, also contribute significantly to market expansion. Furthermore, improving healthcare infrastructure and favorable reimbursement policies across leading European countries like Germany and France bolster device accessibility. Investment in clinical research and rising patient preference for safer, retrievable filters underpin the sustained growth trajectory.

Market Trends

Emerging trends in the Europe IVC filters market include the shift towards retrievable and bioconvertible filters that offer enhanced safety and flexibility by allowing device removal or transformation post-implantation. Increasing integration of advanced biomaterials and coatings to reduce thrombogenicity and enhance biocompatibility is gaining traction. Additionally, growing emphasis on patient-specific device customization and minimally invasive implantation techniques enhances clinical outcomes. The market is witnessing strategic collaborations between device manufacturers and healthcare providers to improve procedural efficiencies. Digital health tools facilitating remote monitoring and follow-up of implanted filters are also emerging, reflecting broader healthcare digitalization trends.

Market Opportunities

Significant opportunities exist in expanding the indications for IVC filters beyond traditional deep vein thrombosis and pulmonary embolism to include prophylaxis in high-risk surgical and oncology patients. The development of bioconvertible and coated filters presents avenues for product differentiation and addressing long-term safety concerns. Geographic expansion into underpenetrated European countries with improving healthcare infrastructure offers growth potential. Collaborations with healthcare providers to enhance clinical education and procedural adoption can accelerate market penetration. Furthermore, integrating digital monitoring solutions presents novel business models that enhance patient management and device lifecycle tracking.

Market Challenges

The Europe IVC filters market faces challenges including concerns over filter-related complications such as migration, fracture, and thrombosis which may limit adoption. Stringent regulatory requirements and lengthy approval processes in Europe increase time-to-market and development costs. The high cost of advanced filter technologies may restrict uptake in cost-sensitive healthcare settings. Additionally, variability in clinical guidelines and physician preferences across countries creates market fragmentation. Limited awareness among some patient groups and the availability of alternative pharmacological therapies pose competitive pressures. Ensuring long-term safety and efficacy data remains a critical hurdle for manufacturers.

Regulatory Framework

Between 2020 and 2025, the Europe Inferior Vena Cava Filters market has been significantly influenced by the implementation of the EU Medical Device Regulation (MDR) 2017/745, which became fully applicable in 2021. This regulation introduced stricter requirements on clinical evaluation, post-market surveillance, and device traceability, impacting product approvals and market entry timelines. Manufacturers must comply with enhanced safety and performance standards, including rigorous clinical evidence demonstrating device efficacy and reduced adverse events. National competent authorities across Germany, France, the UK, Italy, and Spain enforce these regulations with country-specific adaptations, ensuring harmonized yet localized oversight. Regulatory frameworks also emphasize patient safety through mandatory vigilance reporting and periodic device reassessment. Additionally, reimbursement policies are evolving to favor innovative devices demonstrating superior clinical outcomes, further driving regulatory alignment with market dynamics.

Market Intelligence

- •15th January 2025, Cook Medical announced the launch of its next-generation bioconvertible inferior vena cava filter, designed to provide enhanced safety by transforming into a non-thrombogenic implant post-embolism prevention phase. This innovative device incorporates advanced polymer technology enabling gradual bioconversion, reducing the risks associated with permanent implants. Targeted at European markets including Germany, France, and the UK, the product aims to address clinical concerns around filter retrieval complications and long-term device safety. The launch is supported by robust clinical trial data demonstrating improved patient outcomes and procedural efficiency. This strategic innovation positions Cook Medical to strengthen its leadership in the Europe IVC filters market.

- •10th March 2025, B. Braun Melsungen AG introduced a coated inferior vena cava filter incorporating heparin-bonded technology to reduce thrombogenicity and enhance biocompatibility. Aimed at hospitals and specialized vascular clinics across Europe, the device offers improved safety profiles by minimizing clot formation on the filter surface. Clinical studies conducted in Germany and Italy showed significant reductions in filter-related complications compared to conventional devices. The product launch aligns with increasing physician demand for safer, long-term implant solutions and is expected to accelerate adoption in the European vascular intervention market. B. Braun’s strategic focus on innovation and patient safety enhances its competitive positioning.

- •20th May 2024, Boston Scientific Corporation completed the acquisition of a European medical device startup specializing in retrievable IVC filters with proprietary deployment technology. This acquisition expands Boston Scientific’s product portfolio in the vascular intervention segment and strengthens its presence in key European markets including France, Spain, and Italy. The startup’s innovative deployment system improves implantation accuracy and reduces procedure times, offering significant clinical benefits. Boston Scientific plans to integrate this technology into its existing product lines and accelerate clinical adoption through established European distribution networks. This strategic move consolidates Boston Scientific’s position as a leading player in the Europe IVC filters market.

- •5th April 2025, Medtronic plc announced a multi-center European clinical study evaluating the safety and efficacy of its novel convertible IVC filter. The study, conducted across Germany, France, and the UK, aims to generate robust clinical evidence supporting the device’s unique ability to transition from a temporary to a permanent filter based on patient needs. This initiative responds to growing clinical demand for versatile filter options and regulatory expectations for comprehensive safety data. Positive study outcomes are expected to facilitate regulatory approvals and reimbursement in key European countries, enabling broader market access and adoption. Medtronic’s investment in clinical innovation underscores its commitment to advancing vascular intervention therapies.

- •Source: Official press releases from Cook Medical, B. Braun Melsungen AG, Boston Scientific Corporation, Medtronic plc

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.95 Billion |

| Forecast Year Market Size | USD 1.85 Billion |

| CAGR | 7.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Type (Permanent Inferior Vena Cava Filters, Retrievable Inferior Vena Cava Filters, Convertible Inferior Vena Cava Filters, Bioconvertible Inferior Vena Cava Filters, Coated Inferior Vena Cava Filters), Application (Deep Vein Thrombosis, Pulmonary Embolism, Trauma Patients, Cancer Patients, Others), Service Type (Implantation Procedures, Filter Retrieval Procedures, Follow-up and Monitoring Services, Device Maintenance and Support), Deployment Model (Hospital-based Implantation, Ambulatory Surgical Centers, Specialized Vascular Clinics) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Cook Medical (United States), C.R. Bard (United States), B. Braun Melsungen AG (Germany), Boston Scientific Corporation (United States), Terumo Corporation (Japan) |

Europe Inferior Vena Cava (IVC) Filters Market - Europe Industry Size & Growth Analysis 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.