Global Aircraft Management Service Market Size, Growth & Revenue 2025-2034

Global Aircraft Management Service Market is segmented by Service Type (Full-Service Management, Partial Management, On-Demand Management, Consulting Services, Technology Solutions), Application (Charter Services, Maintenance Management, Crew Management, Flight Operations, Asset Management), Client Segment (Private Jet Owners, Corporate Aviation, Charter Operators, Government & Military), Deployment Model (Cloud-based Platforms, On-premise Solutions, Hybrid Models), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Aircraft Management Service market is defined by a comprehensive suite of services that include charter management, flight operations, crew management, maintenance management, and asset management. It caters primarily to private jet owners, commercial operators, and government entities seeking efficient aircraft utilization and regulatory compliance. The market encompasses the entire value chain from aircraft acquisition, maintenance scheduling, crew training, to operational oversight, involving a network of service providers and technology vendors. Increasing demand for managed aviation services is driven by the need for operational efficiency, cost savings, and enhanced safety standards. Technological innovations such as telematics, AI-driven maintenance, and digital platforms for flight scheduling have expanded service capabilities, enabling real-time monitoring and predictive maintenance. Furthermore, growing awareness about environmental regulations and sustainability is influencing market dynamics, pushing providers towards greener, more efficient aircraft management. The market’s global nature spans multiple regions with varying regulatory environments, necessitating adaptive service models to meet localized compliance and customer expectations. Applications range from corporate aviation to fractional ownership and charter services, each with distinct operational challenges and service requirements. The evolving landscape positions aircraft management services as a critical enabler for the aviation sector’s growth, offering scalable solutions that support fleet optimization and risk mitigation across the entire aircraft lifecycle.

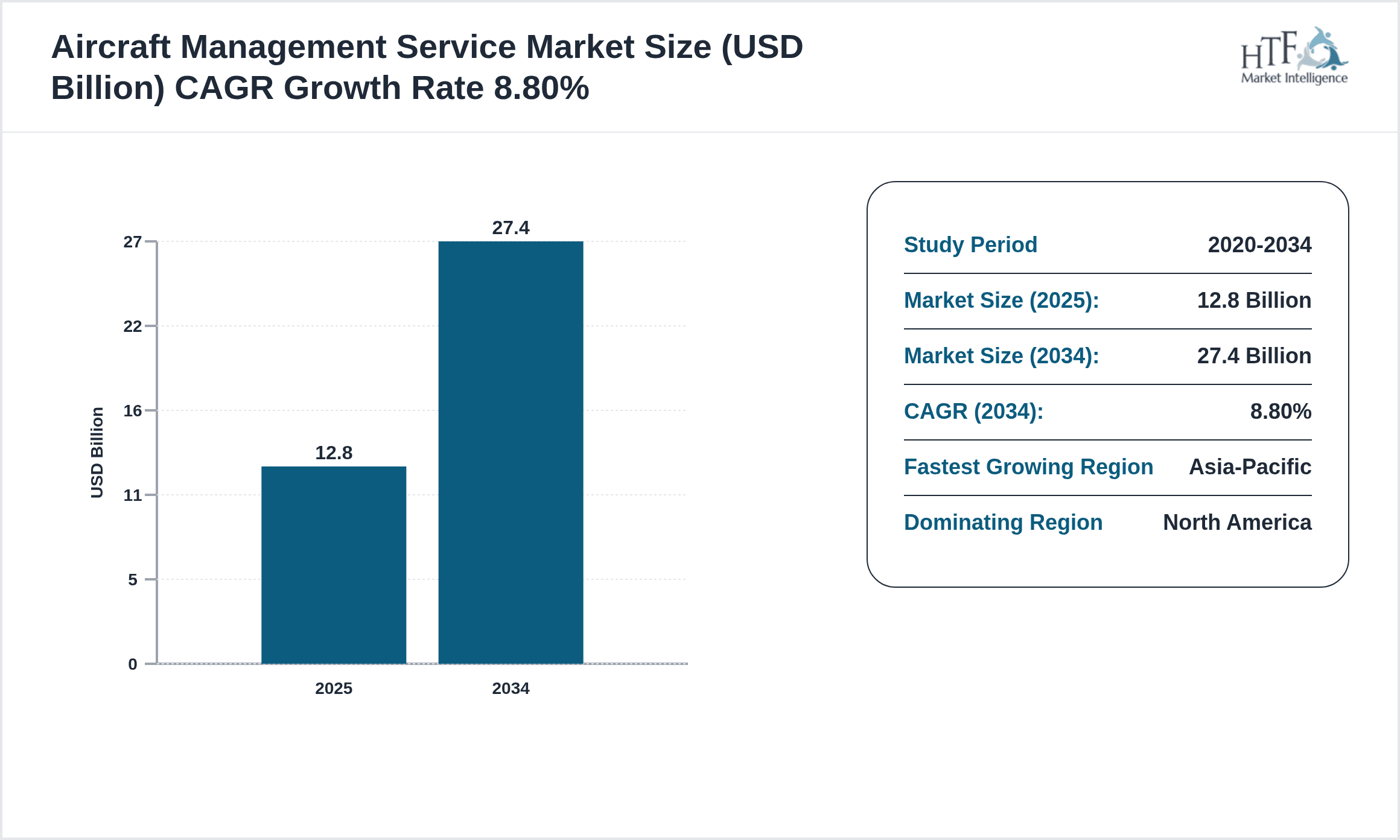

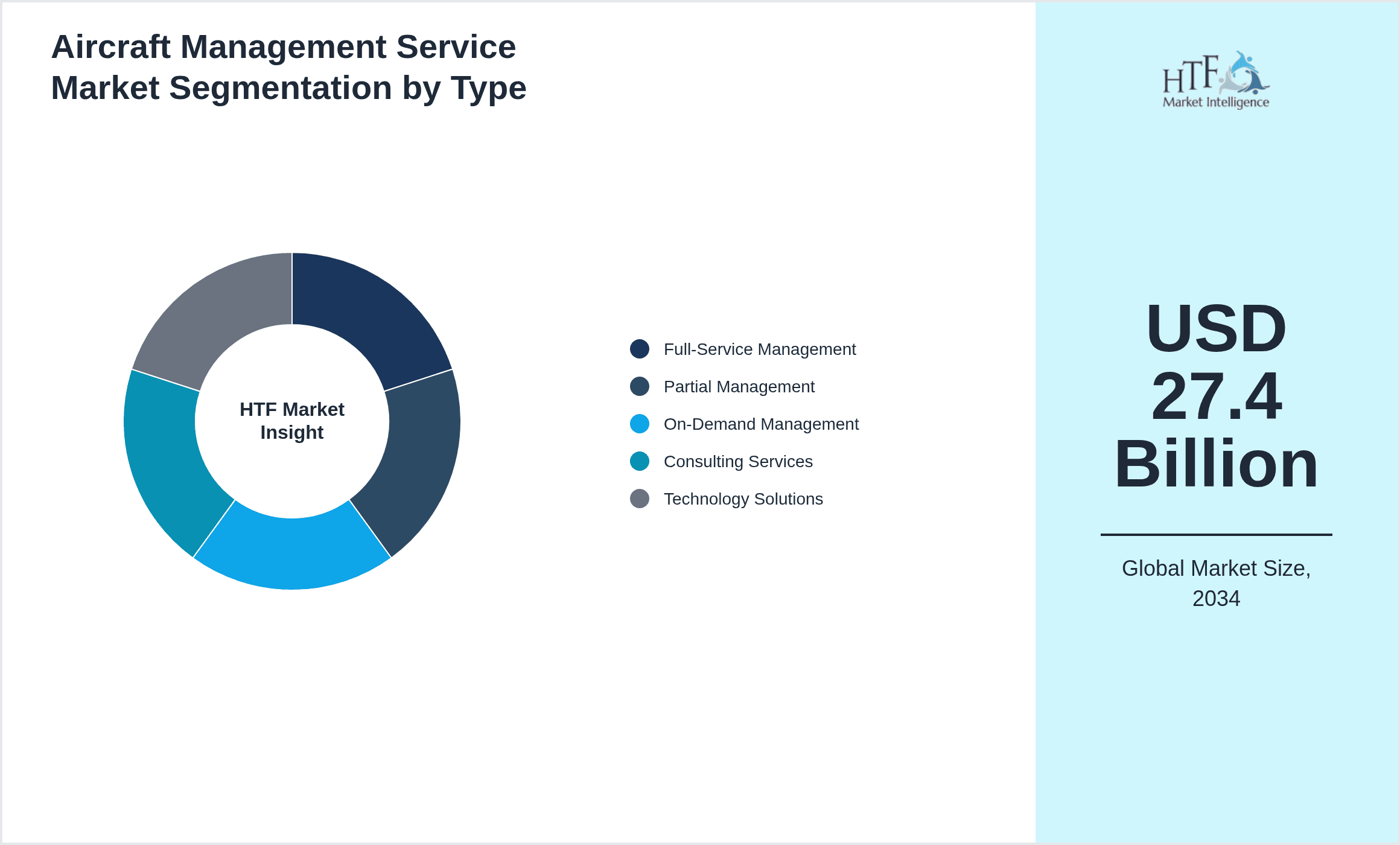

- •Key market highlights include a base market size of USD 12.8 Billion in 2025, with projections indicating growth to USD 27.4 Billion by 2034 at a CAGR of 8.8%. The Asia-Pacific region is the fastest growing, propelled by increasing private jet ownership and expanding charter services in emerging economies. North America maintains dominance due to its mature aviation infrastructure and extensive corporate aviation activities. Full-Service Management remains the leading product type, offering end-to-end solutions that address the complex needs of fleet operators. On-Demand Management services are gaining traction for their flexibility and cost efficiency, particularly among small and mid-sized operators.

- •The aircraft management service market offers significant value propositions to stakeholders by enhancing operational efficiency, reducing administrative burdens, and ensuring regulatory compliance. For aircraft owners, these services enable optimized asset utilization and cost savings through expert maintenance and crew management. Charter operators benefit from streamlined flight operations and customer service enhancements, while technology providers leverage digital platforms to offer innovative solutions. The strategic importance of aircraft management services is underscored by their role in supporting fleet safety, operational scalability, and market expansion across global regions. Investors and industry participants view this market as a high-growth segment with opportunities to capitalize on evolving customer demands and technological advancements.

Competitive Landscape

The global aircraft management service market is characterized by a competitive environment featuring a mix of established aviation service providers and emerging technology-driven companies. Market dynamics are shaped by the strategic focus on operational efficiency, safety compliance, and customer-centric service innovation. Leading players adopt differentiation strategies through comprehensive service portfolios, integration of advanced digital tools, and geographic expansion to enhance market penetration. Strategic partnerships and collaborations are common to leverage complementary strengths, such as combining maintenance expertise with flight operations management technology. Mergers and acquisitions serve as key mechanisms for market consolidation and capability enhancement, enabling companies to offer bundled services with improved scalability. Pricing strategies vary, balancing premium bespoke services with flexible on-demand offerings to cater to diverse customer segments. Distribution channels include direct client relationships, broker networks, and digital platforms, facilitating both B2B and B2C engagements. Adoption of emerging technologies such as AI for predictive maintenance, blockchain for secure documentation, and IoT for real-time monitoring provides competitive advantages. Barriers to entry include stringent regulatory compliance requirements, high capital investments, and the need for specialized expertise. Regional competition dynamics reflect the maturity of aviation infrastructure and regulatory frameworks, with North America and Europe hosting a higher concentration of established players, while Asia-Pacific sees rapid growth from new entrants. Future trends indicate increasing focus on sustainability, digital transformation, and personalized service offerings to maintain competitive positioning.

Leading Companies in Aircraft Management Service Market

- •Jet Aviation International SA (Switzerland)

- •NetJets Inc. (United States)

- •VistaJet Ltd. (Malta)

- •ExecuJet Aviation Group (South Africa)

- •Air Partner plc (United Kingdom)

- •Flexjet LLC (United States)

- •Clay Lacy Aviation (United States)

- •Delta Private Jets (United States)

- •TAG Aviation (United Arab Emirates)

- •Gama Aviation plc (United Kingdom)

- •Solairus Aviation LLC (United States)

- •Jet Linx Aviation (United States)

- •PrivateFly (United Kingdom)

- •Universal Aviation (United States)

- •Sentient Jet (United States)

- •Air Charter Service (United Kingdom)

- •Banyan Air Service (United States)

- •PlaneSense Inc. (United States)

- •AirSprint (Canada)

- •Wheels Up (United States)

- •JetSuite (United States)

- •XOJET Aviation (United States)

- •Mountain Aviation (United States)

- •Executive Jet Management (United States)

- •Bombardier Recreational Products Inc. (Canada)

Market Breakdown

- •By Service Type

- ◦Full-Service Management

- ◦Partial Management

- ◦On-Demand Management

- ◦Consulting Services

- ◦Technology Solutions

- •By Application

- ◦Charter Services

- ◦Maintenance Management

- ◦Crew Management

- ◦Flight Operations

- ◦Asset Management

- •By Client Segment

- ◦Private Jet Owners

- ◦Corporate Aviation

- ◦Charter Operators

- ◦Government & Military

- •By Deployment Model

- ◦Cloud-based Platforms

- ◦On-premise Solutions

- ◦Hybrid Models

Growth Dynamics

- •Rising demand for private and business aviation drives market growth, with increasing numbers of high-net-worth individuals and corporations seeking efficient fleet management services. This trend is amplified by the growing preference for charter services as an alternative to commercial flights, especially in the post-pandemic era where personalized travel safety is prioritized.

- •Technological advancements in aircraft monitoring and maintenance, including AI-powered predictive maintenance and digital flight operations platforms, enhance service offerings and operational efficiency, attracting new customers and reducing downtime.

- •Stringent regulatory requirements globally compel aircraft owners and operators to outsource management functions to specialized service providers who ensure compliance with safety, environmental, and operational standards, thereby driving service demand.

- •Expansion of fractional ownership and shared aircraft usage models increases the complexity of managing fleets, creating demand for sophisticated aircraft management solutions that can handle multi-user operational dynamics.

- •Growing environmental awareness and the shift towards sustainable aviation practices prompt service providers to integrate eco-friendly solutions and optimize fleet operations to reduce carbon footprints, opening new growth avenues.

Market Trends

- •Integration of digital platforms with mobile applications is transforming customer experience by enabling real-time booking, flight tracking, and personalized service management, thus enhancing operational transparency and customer engagement.

- •Emergence of on-demand aircraft management services caters to small fleet owners and occasional flyers, providing flexible, cost-effective management solutions without long-term commitments.

- •Increasing collaboration between aircraft management companies and OEMs fosters innovation in maintenance and operational efficiency, with integrated service contracts becoming more prevalent.

- •Adoption of IoT-enabled devices for real-time aircraft health monitoring is gaining traction, facilitating predictive maintenance and reducing unexpected downtime, thereby improving reliability and service quality.

- •Sustainability-focused initiatives, including carbon offset programs and investment in more fuel-efficient aircraft, are becoming mainstream within aircraft management services as part of broader ESG commitments.

Market Opportunities

- •Expanding business aviation in emerging markets, particularly in Asia-Pacific and Latin America, presents significant growth opportunities for aircraft management service providers willing to establish localized operations and partnerships.

- •Development of AI and machine learning-based predictive analytics for maintenance and flight operations offers potential to reduce costs and improve fleet uptime, attracting investment and adoption.

- •Increasing demand for environmentally friendly aviation solutions encourages service providers to innovate in sustainable fleet management and carbon-neutral operational models, opening new market segments.

- •Growth in fractional ownership and jet card programs creates opportunities for tailored aircraft management services that address the specific needs of shared ownership models.

- •Integration of blockchain technology for secure and transparent documentation, such as maintenance logs and ownership records, presents a novel opportunity to enhance service reliability and trust.

Market Challenges

- •High regulatory complexity and varying compliance standards across global regions impose significant operational challenges, requiring continual adaptation and expertise from service providers to avoid penalties and operational disruptions.

- •The capital-intensive nature of aircraft management infrastructure and technology investments limits market entry for smaller players and constrains the scalability of new entrants.

- •Skill shortages, particularly in specialized aviation maintenance and regulatory compliance roles, hamper service quality and growth potential in certain regions.

- •Volatility in fuel prices and geopolitical uncertainties impact operational costs and demand for aircraft management services, creating challenges in pricing and long-term planning.

- •Data security and privacy concerns associated with digital platforms and connected aircraft systems necessitate robust cybersecurity measures, increasing operational complexity and costs.

Regulatory Framework

- •Between 2020 and 2025, the International Civil Aviation Organization (ICAO) updated safety management system requirements, mandating stricter compliance for flight operations and maintenance procedures, significantly impacting aircraft management practices globally.

- •The European Union Aviation Safety Agency (EASA) introduced new environmental regulations in 2023 focusing on emissions monitoring and reduction, compelling aircraft management providers to incorporate sustainability protocols into their operations.

- •In the United States, the Federal Aviation Administration (FAA) enhanced pilot certification and crew training standards between 2021 and 2024, increasing the demand for advanced crew management services.

- •Several jurisdictions implemented data privacy laws affecting digital aircraft management platforms, necessitating compliance with regulations such as GDPR in Europe and CCPA in North America for handling customer and operational data.

- •Government incentives promoting sustainable aviation, including tax credits and grants for adopting green technologies, have been introduced in various regions, encouraging investment in eco-friendly aircraft management solutions.

Market Intelligence

- •15th January 2025, NetJets Inc. launched a new AI-driven predictive maintenance platform designed to enhance fleet reliability and reduce operational downtime. The platform integrates real-time telemetry data with machine learning algorithms to forecast maintenance needs, enabling proactive servicing schedules. This innovation is expected to improve customer satisfaction by minimizing unexpected aircraft grounding and optimizing maintenance costs. NetJets aims to expand this technology across its global fleet by late 2025, reinforcing its leadership in managed aviation services. Source: NetJets Official Press Release

- •30th March 2025, VistaJet Ltd. introduced an advanced digital booking and management app targeting corporate clients and high-net-worth individuals. The application offers seamless flight scheduling, crew management integration, and real-time operational updates. By leveraging cloud-based infrastructure, VistaJet enhances user experience and operational transparency, positioning itself competitively in the digital transformation of aircraft management. The rollout includes integration with sustainability tracking tools to support clients’ carbon footprint monitoring. This development supports VistaJet's strategic objective to capture growing demand for personalized aviation services. Source: VistaJet Corporate Announcement

- •10th May 2025, Gama Aviation plc announced a strategic partnership with a leading IoT solutions provider to deploy real-time health monitoring systems across its managed aircraft fleet. This collaboration aims to utilize sensor data analytics for predictive maintenance and operational efficiency. The initiative aligns with Gama Aviation’s commitment to innovation and sustainable operations, expected to reduce maintenance costs by up to 15% and enhance aircraft availability. The partnership marks a significant investment in digital transformation within the aircraft management sector. Source: Gama Aviation Investor Relations

- •Market Intelligence: Recent developments and industry insights are being monitored. For latest updates, consult official company announcements and industry publications.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.8 Billion |

| Forecast Year Market Size | USD 27.4 Billion |

| CAGR | 8.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.5% |

| Scope of Report | Market is segmented by Service Type (Full-Service Management, Partial Management, On-Demand Management, Consulting Services, Technology Solutions), Application (Charter Services, Maintenance Management, Crew Management, Flight Operations, Asset Management), Client Segment (Private Jet Owners, Corporate Aviation, Charter Operators, Government & Military), Deployment Model (Cloud-based Platforms, On-premise Solutions, Hybrid Models) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Jet Aviation International SA (Switzerland), NetJets Inc. (United States), VistaJet Ltd. (Malta), ExecuJet Aviation Group (South Africa), Air Partner plc (United Kingdom) |

Global Aircraft Management Service Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.