Global Automotive Industry Consulting Service Market Size, Growth & Revenue 2024-2034

Global Automotive Industry Consulting Service Market is segmented by Type (Management Consulting, Technology Consulting, Strategy Consulting, HR Consulting, Financial Consulting), Application (Product Development, Supply Chain Optimization, Regulatory Compliance, Digital Transformation, Strategic Planning), End User (Automotive OEMs, Tier 1 Suppliers, Aftermarket Service Providers, Fleet Operators), Delivery Model (Onsite Consulting, Remote Consulting, Hybrid Consulting), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global automotive industry consulting service market delivers expert advisory and strategic solutions to automotive OEMs, suppliers, and service providers worldwide. It spans multiple consulting disciplines such as management, technology, strategy, human resources, and financial advisory, all tailored specifically to automotive sector challenges. The market facilitates innovation in product development, streamlines supply chains, ensures regulatory compliance, and drives digital transformation initiatives including electrification and autonomous vehicles adoption. With increasing industry complexity and rapid technological advancements, automotive consulting services are critical in enabling market participants to enhance operational efficiency, reduce costs, and maintain competitive advantage. This dynamic market serves a broad set of applications including strategic planning, regulatory navigation, and technology integration across key regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, reflecting its global footprint and strategic importance.

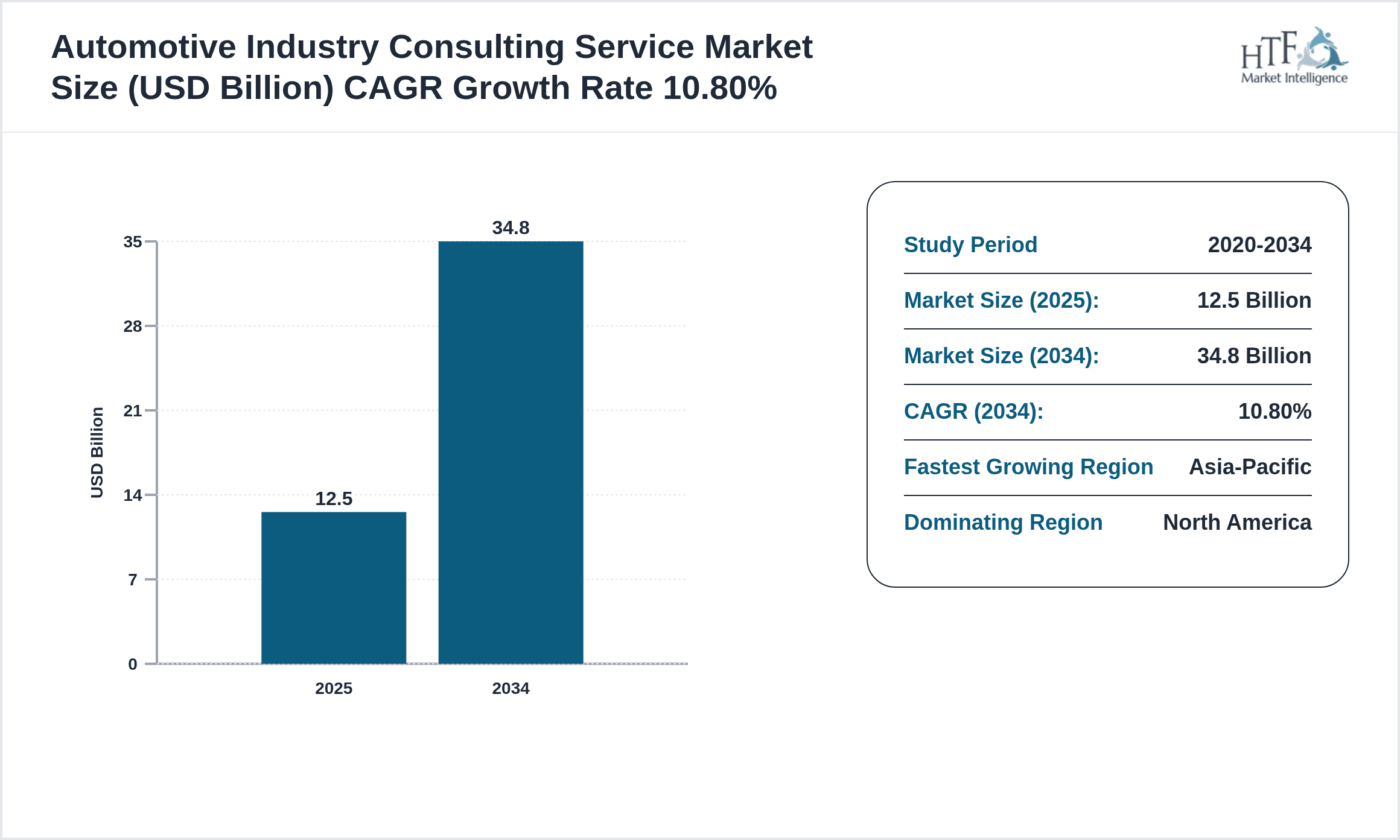

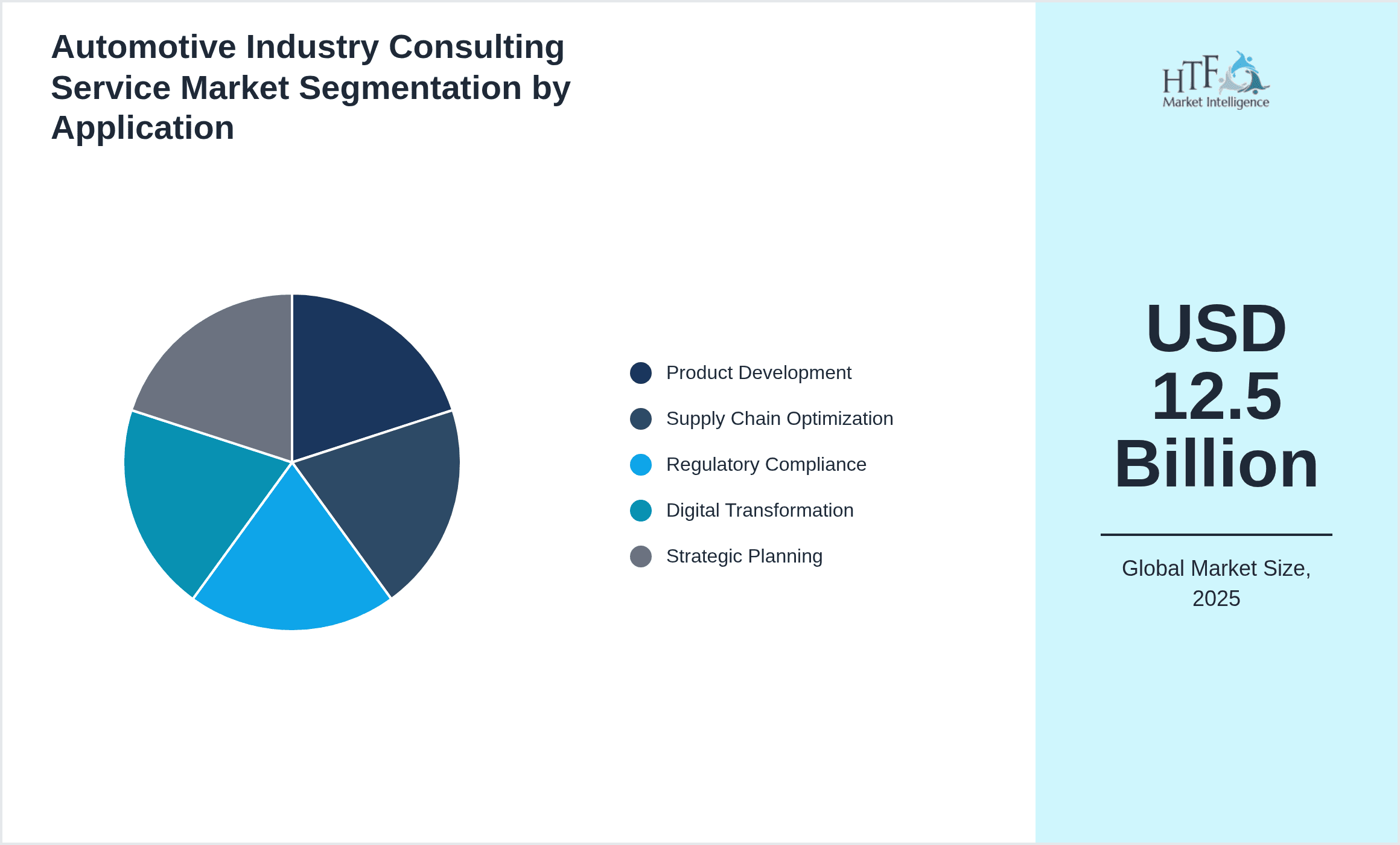

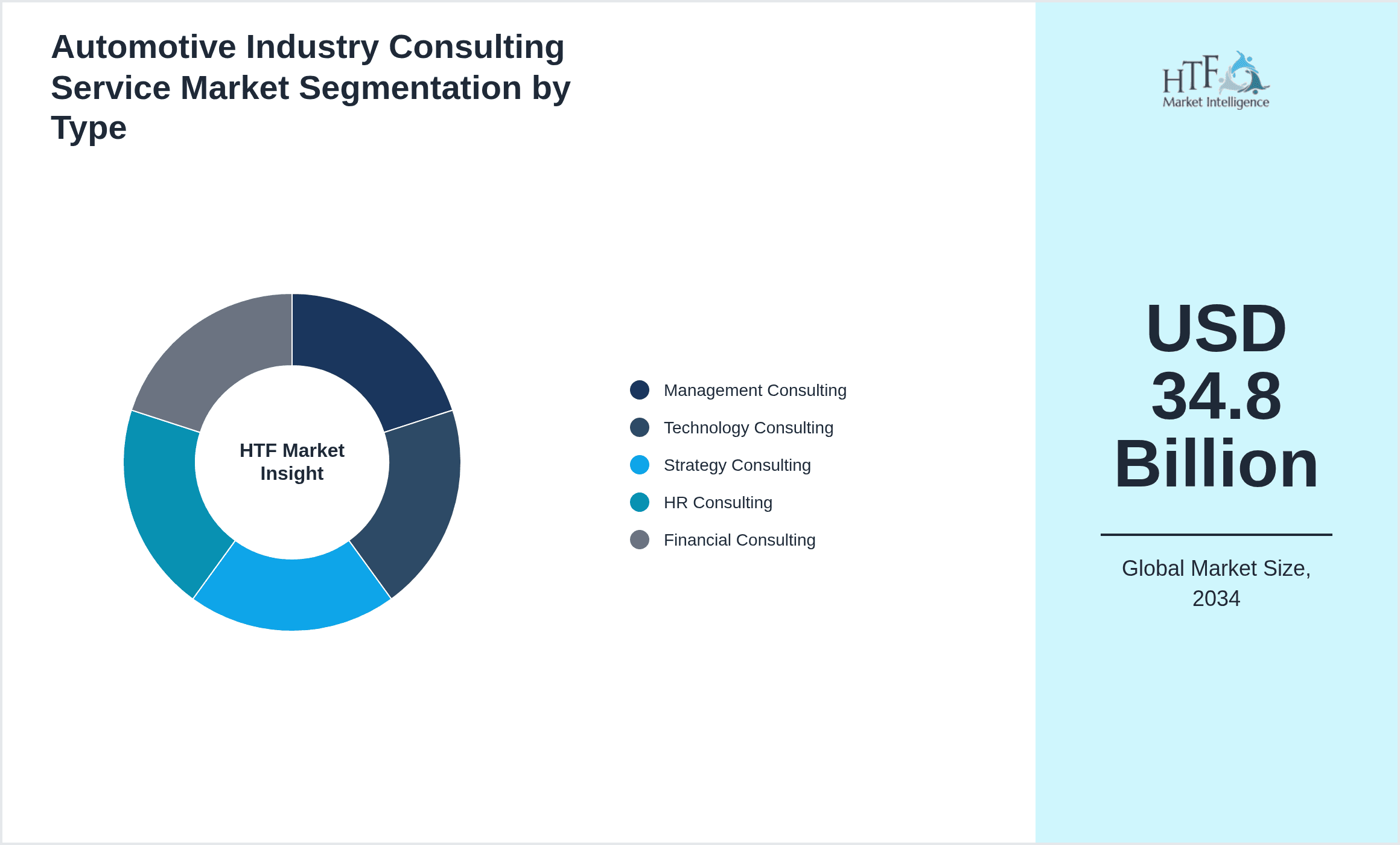

- •Key market highlights include a projected CAGR of 10.8% between 2024 and 2034, with the market size expected to grow from USD 12.5 Billion in 2024 to USD 34.8 Billion by 2034. Management consulting currently dominates the product type segment, while technology consulting is the fastest growing. Among applications, product development services lead the market, closely followed by supply chain optimization. Regionally, North America holds the largest market share, whereas Asia-Pacific is anticipated to witness the highest growth rate fueled by rapid automotive sector expansion and digitalization efforts.

- •The automotive industry consulting service market offers significant value to stakeholders by enabling data-driven decision making, enhancing innovation cycles, and ensuring compliance with stringent regulations. It supports strategic initiatives that drive sustainability, electrification, and smart mobility solutions, thereby playing a pivotal role in the transformation of the global automotive landscape. These services empower manufacturers and suppliers to optimize costs, improve operational agility, and capitalize on emerging market trends, underscoring the market's strategic importance across the automotive value chain.

Competitive Landscape

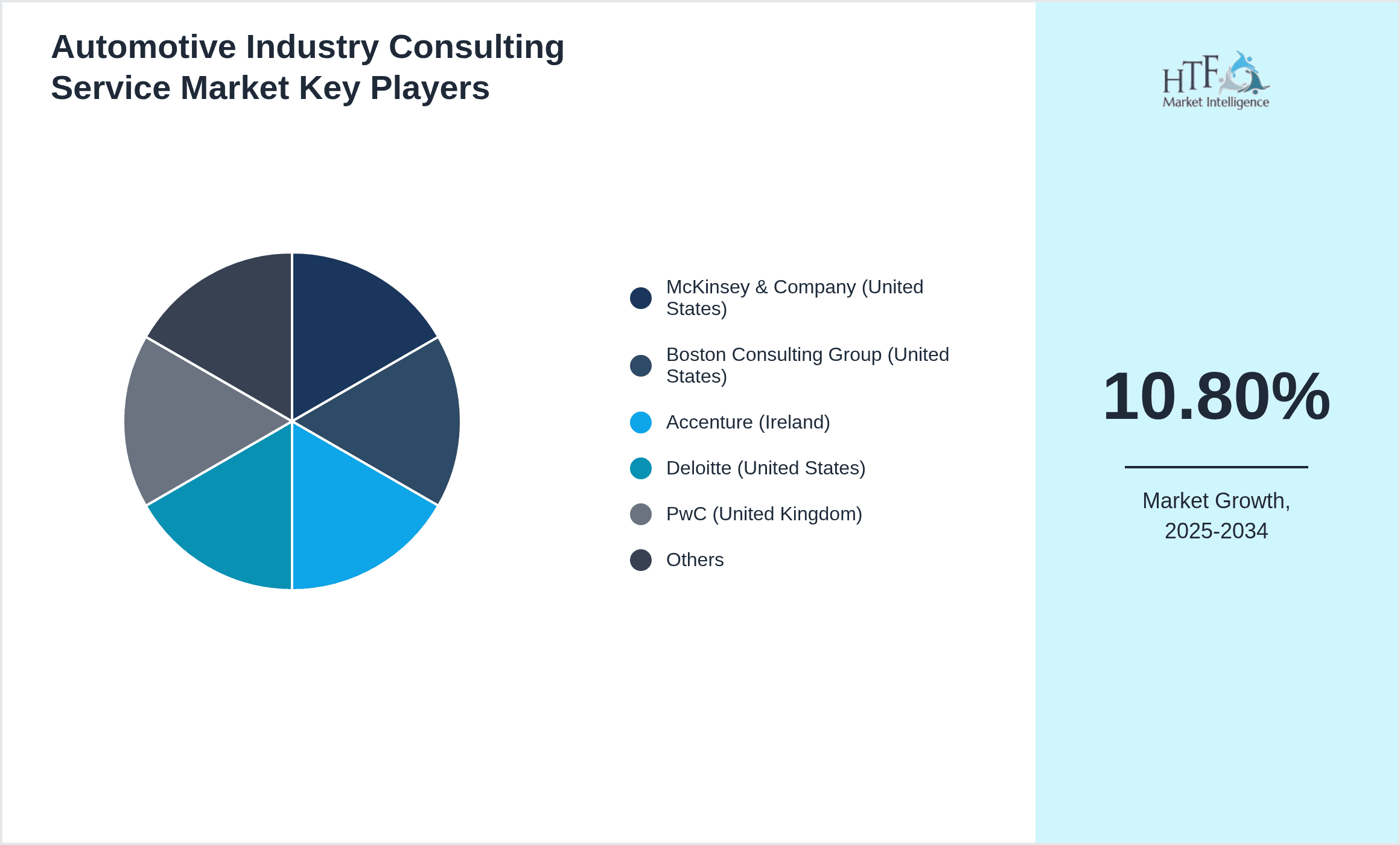

The global automotive industry consulting service market is characterized by intense competition among leading consulting firms and specialized boutique agencies. Market players continuously innovate through digital solutions, advanced analytics, and domain-specific expertise to differentiate their offerings. Strategic partnerships and collaborations with technology providers are common to enhance service portfolios. The competitive environment is shaped by factors such as reputation, global presence, industry knowledge, and the ability to deliver customized solutions addressing evolving automotive trends like electrification and autonomous driving. Pricing strategies and multi-region service capabilities further influence market positioning, while barriers to entry remain high due to the need for deep industry insight and established client relationships. Future competitive trends point towards increased adoption of AI-driven consulting tools and sustainability-focused advisory services, intensifying rivalry and driving continuous market evolution.

Leading Companies in Automotive Industry Consulting Service Market

- •McKinsey & Company (United States)

- •Boston Consulting Group (United States)

- •Accenture (Ireland)

- •Deloitte (United States)

- •PwC (United Kingdom)

- •KPMG (Netherlands)

- •EY (United Kingdom)

- •Bain & Company (United States)

- •Roland Berger (Germany)

- •Capgemini (France)

- •AlixPartners (United States)

- •BearingPoint (Netherlands)

- •Oliver Wyman (United States)

- •Arthur D. Little (United States)

- •ZS Associates (United States)

- •PA Consulting Group (United Kingdom)

- •Frost & Sullivan (United States)

- •Simon-Kucher & Partners (Germany)

- •L.E.K. Consulting (United Kingdom)

- •Capco (United Kingdom)

- •IBM Global Business Services (United States)

- •Infosys Consulting (India)

- •Tata Consultancy Services (India)

- •Cognizant (United States)

- •HCL Technologies (India)

Market Breakdown

- •By Type

- ◦Management Consulting

- ◦Technology Consulting

- ◦Strategy Consulting

- ◦HR Consulting

- ◦Financial Consulting

- •By Application

- ◦Product Development

- ◦Supply Chain Optimization

- ◦Regulatory Compliance

- ◦Digital Transformation

- ◦Strategic Planning

- •By End User

- ◦Automotive OEMs

- ◦Tier 1 Suppliers

- ◦Aftermarket Service Providers

- ◦Fleet Operators

- •By Delivery Model

- ◦Onsite Consulting

- ◦Remote Consulting

- ◦Hybrid Consulting

Growth Dynamics

- •Rising demand for electric and autonomous vehicles is driving the need for specialized consulting services to manage R&D, regulatory adherence, and technology integration, thus accelerating market growth.

- •Digital transformation initiatives across the automotive value chain, including Industry 4.0 adoption and connected car technologies, create extensive opportunities for technology consulting firms.

- •Increasing complexity in global automotive supply chains necessitates expert advisory in logistics, procurement, and risk management to enhance efficiency and resilience.

- •Stringent environmental regulations worldwide compel automotive companies to seek consulting support for compliance, sustainability reporting, and green strategy development.

- •Growing competitive pressure and market volatility push automotive firms to leverage strategic consulting for business model innovation, cost optimization, and market expansion.

Market Trends

- •Integration of AI and big data analytics in consulting services is enabling predictive insights and real-time decision-making for automotive clients, enhancing operational effectiveness.

- •Consulting firms are increasingly offering end-to-end digital transformation services encompassing software platforms, cloud migration, and cybersecurity tailored for automotive manufacturers.

- •Sustainability consulting is gaining prominence as automotive companies pursue carbon neutrality and circular economy initiatives, influencing product design and supply chain strategies.

- •Collaborations between consulting firms and automotive technology startups are fostering innovation and accelerating commercialization of next-generation mobility solutions.

- •Remote consulting models have become widespread post-pandemic, allowing greater flexibility and access to global expertise for automotive clients across regions.

Market Opportunities

- •Expanding electric vehicle markets in emerging economies present significant consulting opportunities in infrastructure planning, technology adoption, and regulatory strategy.

- •Increasing focus on autonomous vehicle development opens avenues for specialized consulting in sensor technologies, software integration, and safety compliance.

- •Growing aftermarket services and connected mobility ecosystems require advisory support in digital platform development and customer experience enhancement.

- •Government incentives for green technologies drive demand for consulting on grant applications, project management, and impact assessment in the automotive sector.

- •Cross-industry partnerships between automotive and tech sectors create new consulting mandates focused on innovation strategy and ecosystem orchestration.

Market Challenges

- •Rapidly evolving technology landscapes require consulting firms to continuously update expertise, posing resource and training challenges to maintain competitiveness.

- •High client expectations for measurable ROI and tangible outcomes increase pressure on consultants to deliver impactful and customized solutions.

- •Data privacy and cybersecurity concerns limit the scope of digital consulting engagements and necessitate stringent compliance measures.

- •Fragmented automotive markets with diverse regulatory environments complicate consulting delivery, particularly in cross-border projects.

- •Intense competition from both large global consultancies and nimble specialized firms compresses margins and challenges client retention.

Regulatory Framework

- •Between 2019 and 2024, the implementation of stricter emissions standards globally, such as Euro 6 and equivalent regulations in North America and Asia-Pacific, has significantly influenced consulting demand in regulatory compliance and environmental strategy.

- •Data protection regulations, including GDPR in Europe and CCPA in North America, introduced compliance complexities requiring consulting support for secure data management and digital transformation.

- •Safety standards related to autonomous vehicle testing and deployment enacted in regions like Europe and Asia have created niche consulting segments focused on regulatory navigation and risk assessment.

- •Government incentives and mandates promoting electric vehicle adoption and green mobility have led to increased consulting engagements for strategy development and funding acquisition.

- •Trade policies and tariffs impacting automotive supply chains have necessitated consulting interventions for risk management and alternative sourcing strategies.

Market Intelligence

- •15th January 2025, Accenture unveiled a comprehensive automotive digital transformation platform integrating AI-powered analytics with supply chain optimization tools targeted at major OEMs. The platform is designed to streamline product development cycles while enhancing regulatory compliance tracking. This initiative positions Accenture as a leader in end-to-end consulting services that facilitate automotive innovation and operational agility in a rapidly evolving industry landscape. The solution's modular architecture enables tailored implementations addressing specific client challenges worldwide. Source: Accenture Official Press Release

- •10th March 2025, McKinsey & Company expanded its automotive consulting footprint by launching a specialized practice focused on electric and autonomous vehicle strategy. This practice emphasizes market entry strategies, technology roadmapping, and ecosystem partnerships to support clients in emerging mobility sectors. McKinsey's initiative reflects growing client demand for expertise in navigating complex regulatory environments and accelerating sustainable automotive innovation. The new practice leverages advanced analytics and industry insights to deliver actionable recommendations globally. Source: McKinsey & Company News

- •22nd May 2025, Deloitte announced a partnership with a leading automotive software provider to co-develop consulting solutions for connected vehicle cybersecurity. This collaboration aims to address increasing threats in automotive digital ecosystems by combining Deloitte’s risk advisory capabilities with cutting-edge security technologies. The joint offering includes vulnerability assessments, compliance audits, and incident response strategies tailored for automotive clients worldwide. This strategic move enhances Deloitte’s consulting portfolio and responds to escalating market concerns over data protection and system integrity. Source: Deloitte Corporate Communication

- •5th July 2025, Boston Consulting Group introduced an AI-driven supply chain analytics service for automotive suppliers to optimize inventory management and demand forecasting. The service harnesses machine learning algorithms to provide real-time insights, reducing costs and enhancing responsiveness to market fluctuations. BCG’s innovative offering supports clients in adapting to global supply chain disruptions and enhancing operational resilience. Early adopters have reported significant efficiency gains and improved decision-making capabilities. Source: Boston Consulting Group Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 34.8 Billion |

| CAGR | 10.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.3% |

| Scope of Report | Market is segmented by Type (Management Consulting, Technology Consulting, Strategy Consulting, HR Consulting, Financial Consulting), Application (Product Development, Supply Chain Optimization, Regulatory Compliance, Digital Transformation, Strategic Planning), End User (Automotive OEMs, Tier 1 Suppliers, Aftermarket Service Providers, Fleet Operators), Delivery Model (Onsite Consulting, Remote Consulting, Hybrid Consulting) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | McKinsey & Company (United States), Boston Consulting Group (United States), Accenture (Ireland), Deloitte (United States), PwC (United Kingdom), KPMG (Netherlands), EY (United Kingdom), Bain & Company (United States), Roland Berger (Germany), Capgemini (France), AlixPartners (United States), BearingPoint (Netherlands), Oliver Wyman (United States), Arthur D. Little (United States), ZS Associates (United States), PA Consulting Group (United Kingdom), Frost & Sullivan (United States), Simon-Kucher & Partners (Germany), L.E.K. Consulting (United Kingdom), Capco (United Kingdom), IBM Global Business Services (United States), Infosys Consulting (India), Tata Consultancy Services (India), Cognizant (United States), HCL Technologies (India) |

Global Automotive Industry Consulting Service Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.