Europe Aviation Consulting Service Market - Outlook 2025-2034

Europe Aviation Consulting Service Market is segmented by Type (Strategic Consulting, Operational Consulting, Technical Consulting, Financial Advisory, Risk Management), Application (Airline Operations, Airport Management, Aircraft Maintenance, Regulatory Compliance, Safety Management), End User (Airlines, Airport Authorities, Aircraft Manufacturers, Government & Regulatory Bodies, Maintenance, Repair, and Overhaul (MRO) Providers), Deployment Model (Onsite Consulting, Remote Consulting, Hybrid Consulting), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Aviation Consulting Service market represents a vital segment of the broader aviation industry, focusing on delivering expert advisory solutions that address strategic, operational, financial, and technical challenges faced by airlines, airports, and associated stakeholders. This market covers a wide range of services including airline operations optimization, airport infrastructure management, regulatory compliance consulting, aircraft maintenance planning, and safety management. Consulting providers in Europe offer tailored services to enhance efficiency, profitability, and sustainability amidst increasing environmental regulations and evolving passenger expectations. The scope extends beyond traditional advisory to encompass digital transformation initiatives and risk mitigation strategies in response to geopolitical shifts and technological disruptions. With aviation being a crucial driver of the European economy, consulting firms play a pivotal role in helping organizations navigate competitive pressures, regulatory complexities, and innovation demands, ensuring robust growth and operational excellence over the forecast period.

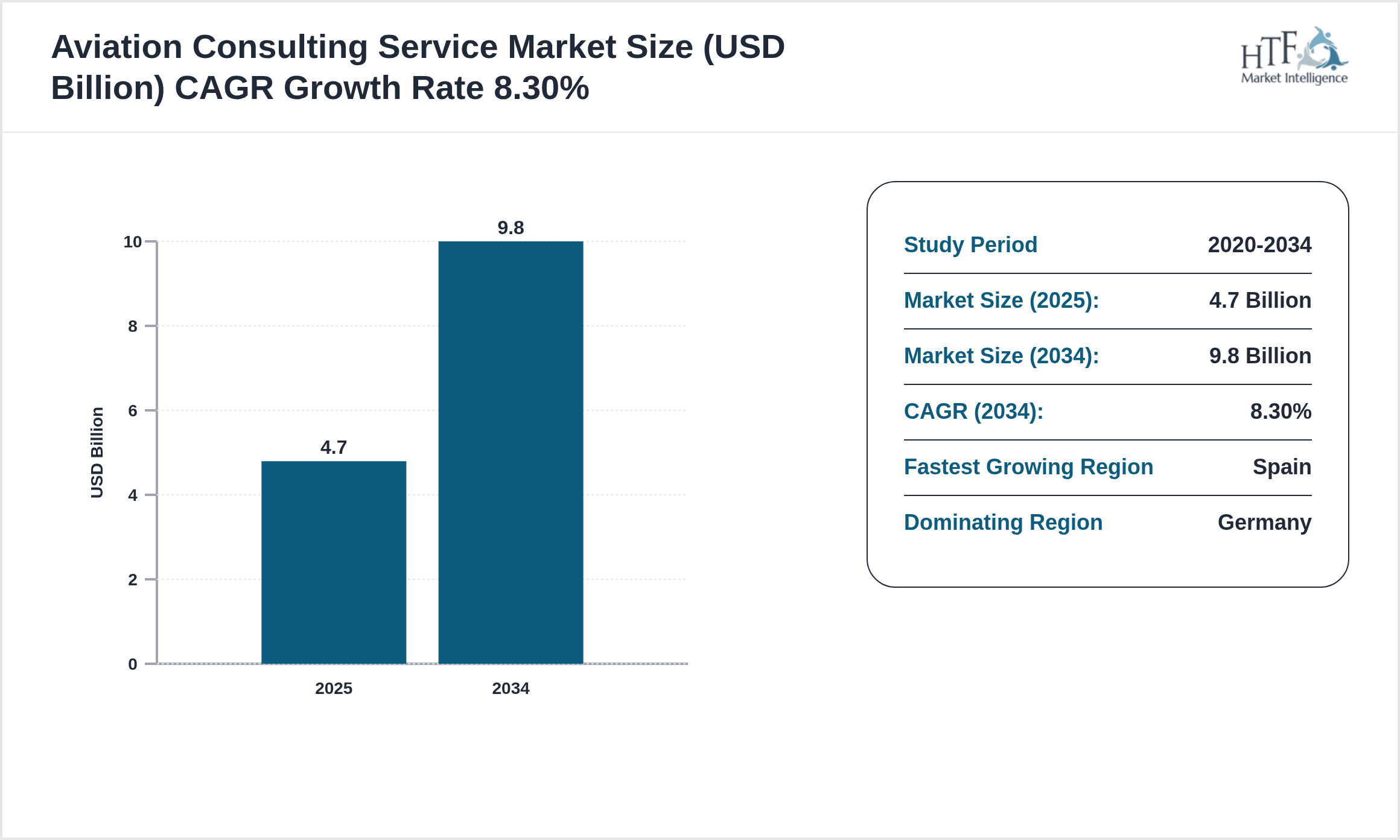

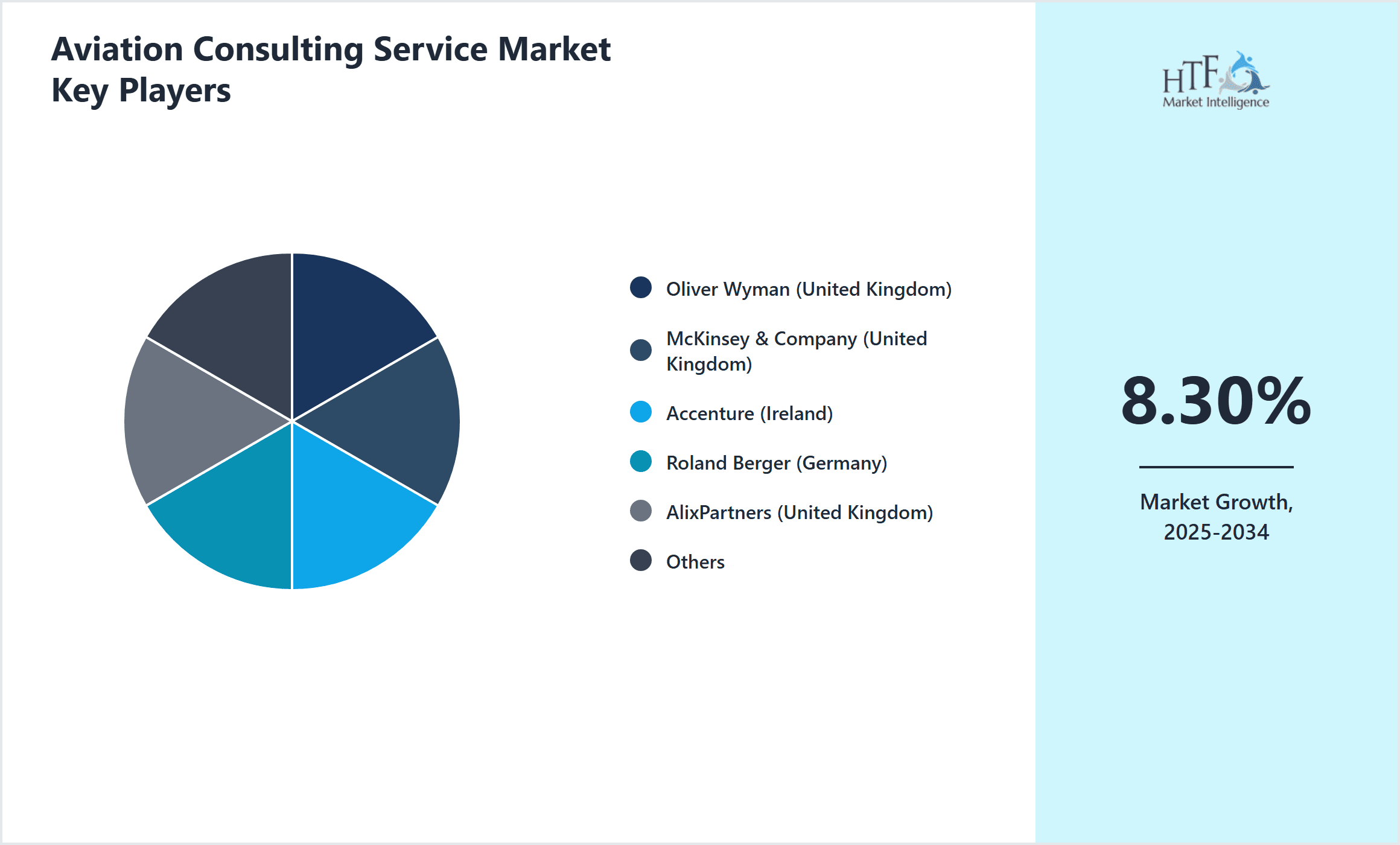

- •Key highlights include a robust CAGR of approximately 8.3% projected from 2025 to 2034, driven by increasing airline fleet expansions, airport modernization programs, and stringent safety and environmental regulations. The market size is estimated at USD 4.7 Billion in 2025, expanding to nearly USD 9.8 Billion by 2034. Germany leads the market in revenue share due to its extensive aviation infrastructure and industry expertise, while Spain is anticipated to exhibit the fastest growth fueled by rising low-cost carrier operations and airport development. Strategic consulting remains the dominant service type, with risk management services emerging rapidly amid growing cybersecurity and operational risk concerns. Applications such as airline operations and airport management are critical revenue drivers, reflecting the sector’s focus on operational efficiency and regulatory adherence.

- •The value proposition of aviation consulting in Europe lies in its ability to provide actionable insights, foster innovation, and enable compliance within a complex and competitive landscape. Stakeholders including airline executives, airport authorities, aircraft manufacturers, and regulatory agencies rely on consulting services to optimize resource allocation, implement cutting-edge technologies, and manage risks effectively. The strategic importance of these services is underscored by the ongoing digital transformation, sustainability ambitions, and evolving passenger demands reshaping the European aviation ecosystem. This positions the aviation consulting market as an indispensable enabler of growth, resilience, and long-term value creation across the region’s aviation sector.

Competitive Landscape

The Europe Aviation Consulting Service market is characterized by a highly competitive environment with a mix of global consulting giants and specialized regional firms competing for market share. Players differentiate through innovation in digital aviation technologies, tailored advisory capabilities, and deep industry expertise. The rivalry is intensified by the increasing demand for integrated consulting solutions that combine strategic insight with technical and operational support. Market leaders invest heavily in research and development to offer services addressing emerging trends such as sustainability, cybersecurity, and data analytics. Strategic partnerships and alliances with technology providers and regulatory bodies are common to enhance service portfolios and market reach. Pricing strategies focus on value-based consulting models, while firms seek to expand through geographic penetration and acquisition of niche players. The competitive landscape is expected to evolve with new entrants leveraging AI and big data to disrupt traditional consulting paradigms, challenging incumbents to continuously innovate and customize their offerings.

Leading Companies in Aviation Consulting Service Market

- •Oliver Wyman (United Kingdom)

- •McKinsey & Company (United Kingdom)

- •Accenture (Ireland)

- •Roland Berger (Germany)

- •AlixPartners (United Kingdom)

- •Bain & Company (United Kingdom)

- •Deloitte (United Kingdom)

- •Boston Consulting Group (Germany)

- •PwC (United Kingdom)

- •EY (United Kingdom)

- •KPMG (Netherlands)

- •Capgemini Invent (France)

- •Frost & Sullivan (United Kingdom)

- •A.T. Kearney (Germany)

- •Strategy& (France)

- •BearingPoint (Netherlands)

- •L.E.K. Consulting (United Kingdom)

- •Navigant Consulting (United Kingdom)

- •PA Consulting Group (United Kingdom)

- •Sia Partners (France)

- •Horváth & Partners (Germany)

- •Copenhagen Economics (Denmark)

- •Tata Consultancy Services (United Kingdom)

- •CGI Group (Canada)

- •Altran Technologies (France)

Market Breakdown

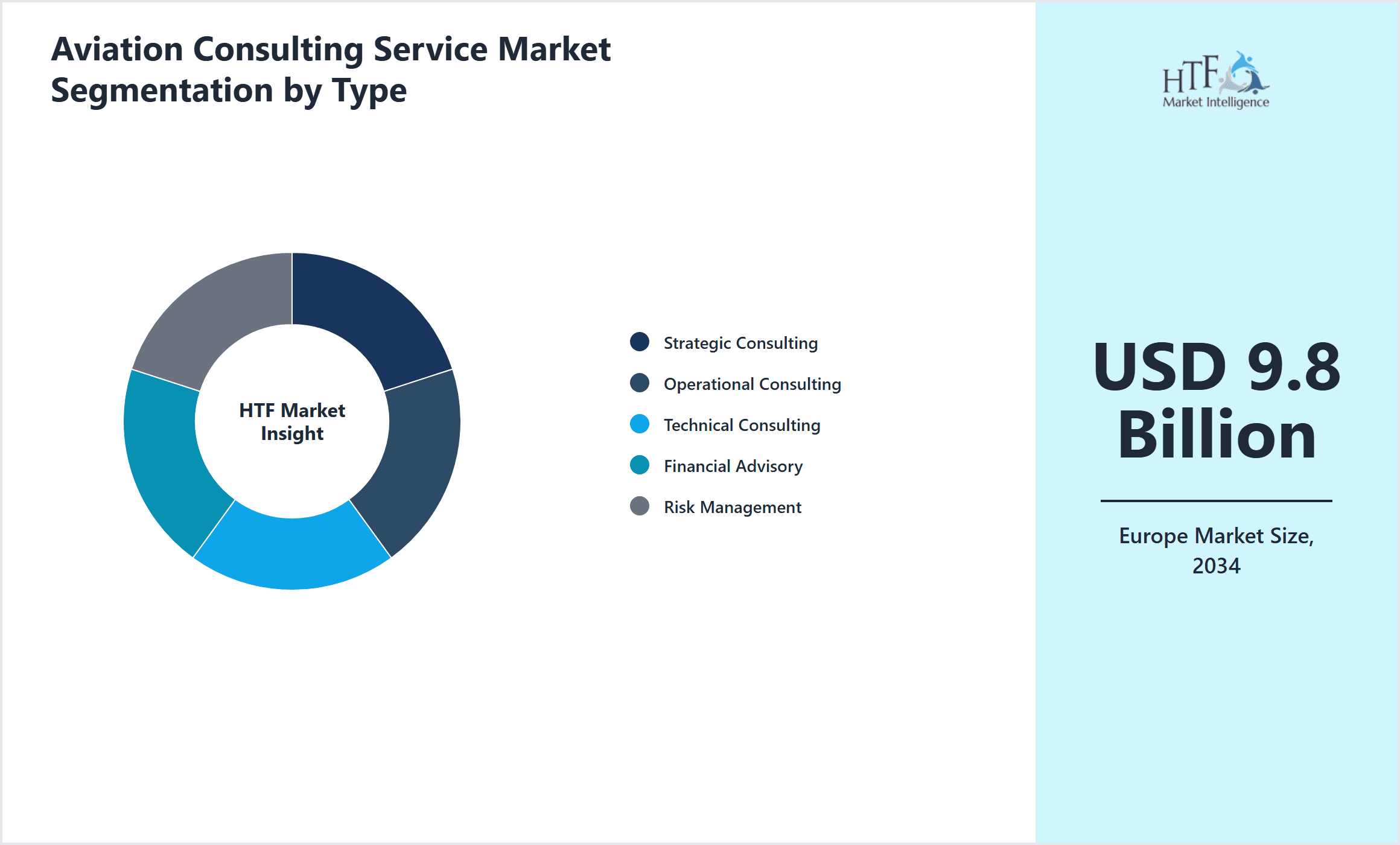

- •By Type

- ◦Strategic Consulting

- ◦Operational Consulting

- ◦Technical Consulting

- ◦Financial Advisory

- ◦Risk Management

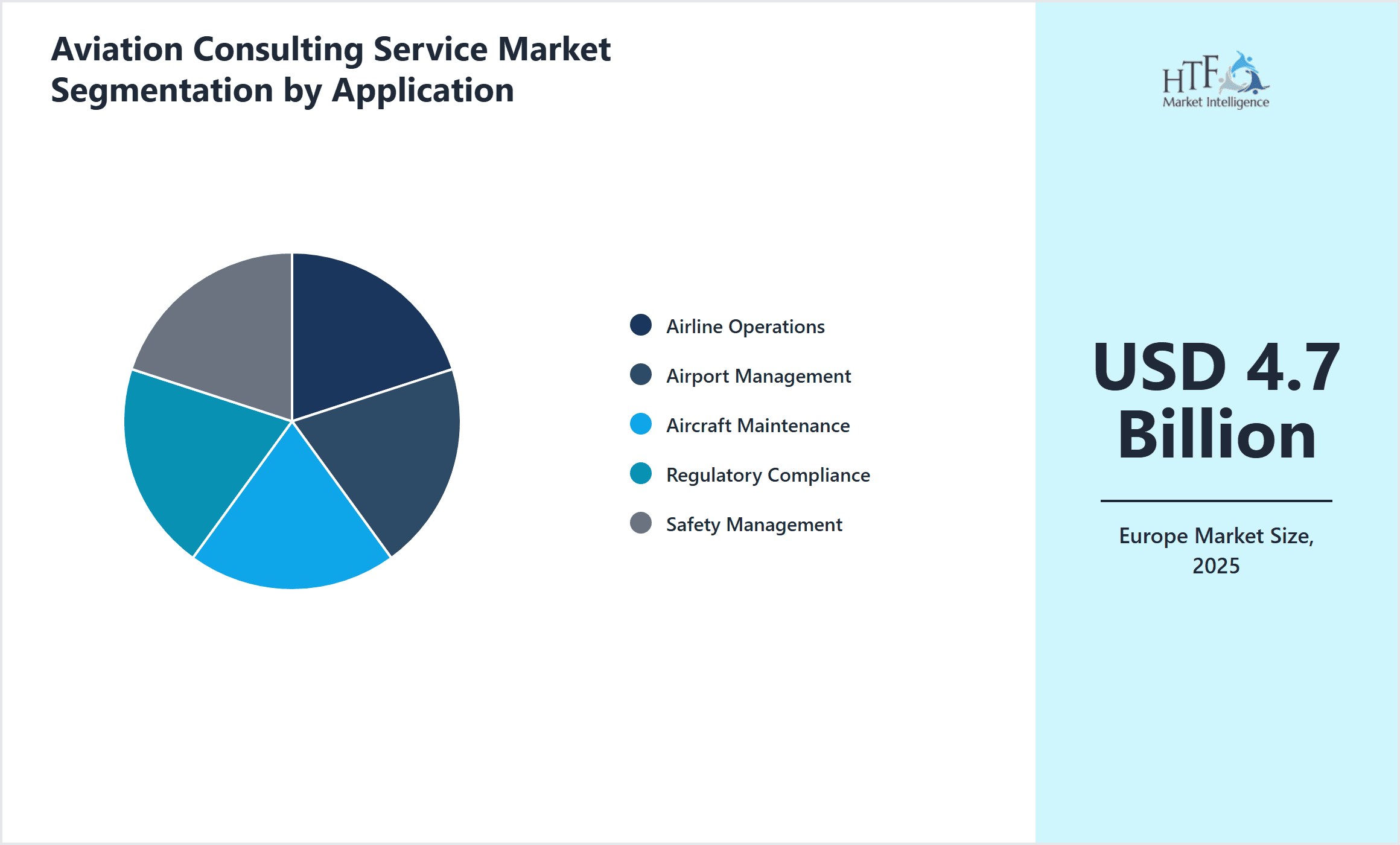

- •By Application

- ◦Airline Operations

- ◦Airport Management

- ◦Aircraft Maintenance

- ◦Regulatory Compliance

- ◦Safety Management

- •By End User

- ◦Airlines

- ◦Airport Authorities

- ◦Aircraft Manufacturers

- ◦Government & Regulatory Bodies

- ◦Maintenance, Repair, and Overhaul (MRO) Providers

- •By Deployment Model

- ◦Onsite Consulting

- ◦Remote Consulting

- ◦Hybrid Consulting

Growth Dynamics

- •The increasing complexity of airline operations, driven by fleet expansion and digital transformation, fuels demand for strategic and operational consulting services. Companies are leveraging aviation consultants to optimize route networks, reduce operational costs, and improve passenger experience through data-driven insights.

- •Stringent regulatory frameworks and growing safety compliance requirements across Europe are propelling demand for specialized advisory in regulatory compliance and safety management. Consulting firms are providing expertise to help aviation stakeholders navigate evolving EU regulations efficiently.

- •The emergence of sustainability and environmental concerns is driving growth in consulting services focused on green aviation practices. Airlines and airports are engaging consultants to develop carbon reduction strategies, integrate alternative fuels, and comply with emission standards.

- •Technological advancements such as AI, IoT, and big data analytics are being incorporated into aviation consulting solutions, enhancing predictive maintenance, operational efficiency, and customer personalization, which boosts market growth.

- •The post-pandemic recovery of air travel demand in Europe is catalyzing investments in airport modernization and airline restructuring, creating ample opportunities for consulting service providers focused on financial advisory and risk management.

Market Trends

- •There is a rising trend of digital transformation consulting with aviation businesses seeking expertise in implementing cloud-based platforms, AI-driven analytics, and automated operational workflows to enhance efficiency and passenger experience.

- •Collaborative partnerships between consulting firms and technology providers are increasing, enabling integrated solutions that combine consulting insights with cutting-edge digital tools tailored to aviation requirements.

- •The adoption of sustainability metrics and ESG (Environmental, Social, and Governance) frameworks by airlines and airports is a significant trend, driving demand for consultancy services specializing in environmental compliance and green strategy development.

- •Growth in low-cost carrier operations across Europe is shaping consulting focus towards cost optimization, network planning, and market expansion strategies tailored to this segment's unique business model.

- •Increased emphasis on cybersecurity consulting is evident as aviation stakeholders invest in safeguarding operational technology and customer data against rising digital threats.

Market Opportunities

- •Expanding opportunities exist in advising on next-generation airport infrastructure projects, including smart airports, automation, and digital twin technologies, which require specialized consulting expertise.

- •Growth in urban air mobility and emerging electric vertical takeoff and landing (eVTOL) aircraft creates a niche for consultancy services focused on regulatory preparation and operational integration within existing aviation ecosystems.

- •The increasing need for integrating sustainability into core business strategies presents opportunities for consulting firms to develop bespoke carbon-neutral roadmaps and compliance frameworks for aviation clients.

- •Consulting opportunities are expanding in crisis management and resilience planning, as airlines and airports seek to mitigate disruptions from geopolitical tensions, pandemics, and climate-related events.

- •Emerging markets within Eastern Europe offer growth potential for aviation consulting providers as these regions invest in airport upgrades and seek expertise to align with Western European standards.

Market Challenges

- •Intense competition from global consulting firms and boutique specialists leads to pricing pressures, challenging new entrants and smaller firms to maintain profitability while delivering high-value services.

- •Navigating the complex and evolving regulatory environment across different European countries requires extensive expertise, posing a barrier for consulting firms to offer pan-European solutions seamlessly.

- •Rapid technological changes necessitate continuous investment in skills and tools, which can strain consultancy resources and affect service delivery consistency across the region.

- •Economic uncertainties and fluctuating air travel demand can impact clients’ consulting budgets, leading to project delays or cancellations and complicating revenue forecasting for service providers.

- •Data privacy and cybersecurity concerns impose additional compliance and operational challenges for consultants handling sensitive aviation data and digital infrastructure.

Regulatory Framework

- •Between 2015 and 2025, the European Union implemented the Single European Sky (SES) regulations to harmonize air traffic management across member states, requiring consulting firms to assist clients in adapting to standardized operational procedures and compliance.

- •The EU Emissions Trading System (EU ETS) for aviation, expanded in 2018, mandates airlines to monitor and reduce carbon emissions, prompting demand for consulting services specializing in environmental accounting and sustainability strategies.

- •The adoption of the European Aviation Safety Agency (EASA) updated rules on aircraft maintenance and certification in 2020 has increased the need for technical consulting to ensure compliance and operational safety.

- •GDPR enforcement from 2018 impacts how aviation companies manage passenger data, requiring consultancy support for data governance, privacy compliance, and cybersecurity frameworks.

- •The European Green Deal, announced in 2019 with progressive enforcement through 2025, drives regulatory incentives and mandates for sustainable aviation fuels and zero-emission targets, creating a regulatory landscape requiring expert advisory services.

Market Intelligence

- •15th February 2025, Oliver Wyman launched a comprehensive digital transformation consulting service tailored for European airlines, integrating AI-powered analytics and operational efficiency tools to enhance route optimization and passenger experience, targeting major carriers undergoing fleet modernization. This new offering aims to capitalize on the increasing demand for data-driven decision-making in aviation operations. Source: Official Oliver Wyman press release

- •3rd May 2025, Accenture expanded its aviation consulting footprint in Europe by acquiring a boutique firm specializing in sustainability and carbon management solutions for airports and airlines. This strategic move enhances Accenture’s capability to support clients in meeting stringent environmental regulations and achieving net-zero targets through innovative advisory services and technology integration. Source: Accenture corporate announcement

- •22nd July 2024, Roland Berger introduced a risk management consulting platform focused on cybersecurity and operational resilience tailored for European aviation stakeholders. The platform combines real-time threat analysis with strategic advisory to mitigate emerging risks in digital aviation environments, reflecting growing client concerns over security and regulatory compliance. Source: Roland Berger news release

- •10th November 2024, Deloitte unveiled an integrated consulting solution for airport modernization projects, emphasizing smart airport technologies, automation, and passenger flow optimization. This initiative targets European airports undergoing infrastructure upgrades to improve operational efficiency and customer satisfaction, driven by rising air traffic and sustainability goals. Source: Deloitte official statement

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Spain is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.7 Billion |

| Forecast Year Market Size | USD 9.8 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Scope of Report | Market is segmented by Type (Strategic Consulting, Operational Consulting, Technical Consulting, Financial Advisory, Risk Management), Application (Airline Operations, Airport Management, Aircraft Maintenance, Regulatory Compliance, Safety Management), End User (Airlines, Airport Authorities, Aircraft Manufacturers, Government & Regulatory Bodies, Maintenance, Repair, and Overhaul (MRO) Providers), Deployment Model (Onsite Consulting, Remote Consulting, Hybrid Consulting) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Oliver Wyman (United Kingdom), McKinsey & Company (United Kingdom), Accenture (Ireland), Roland Berger (Germany), AlixPartners (United Kingdom) |

Europe Aviation Consulting Service Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.