North America Door Hinge and Pivot Market - Outlook 2025-2034

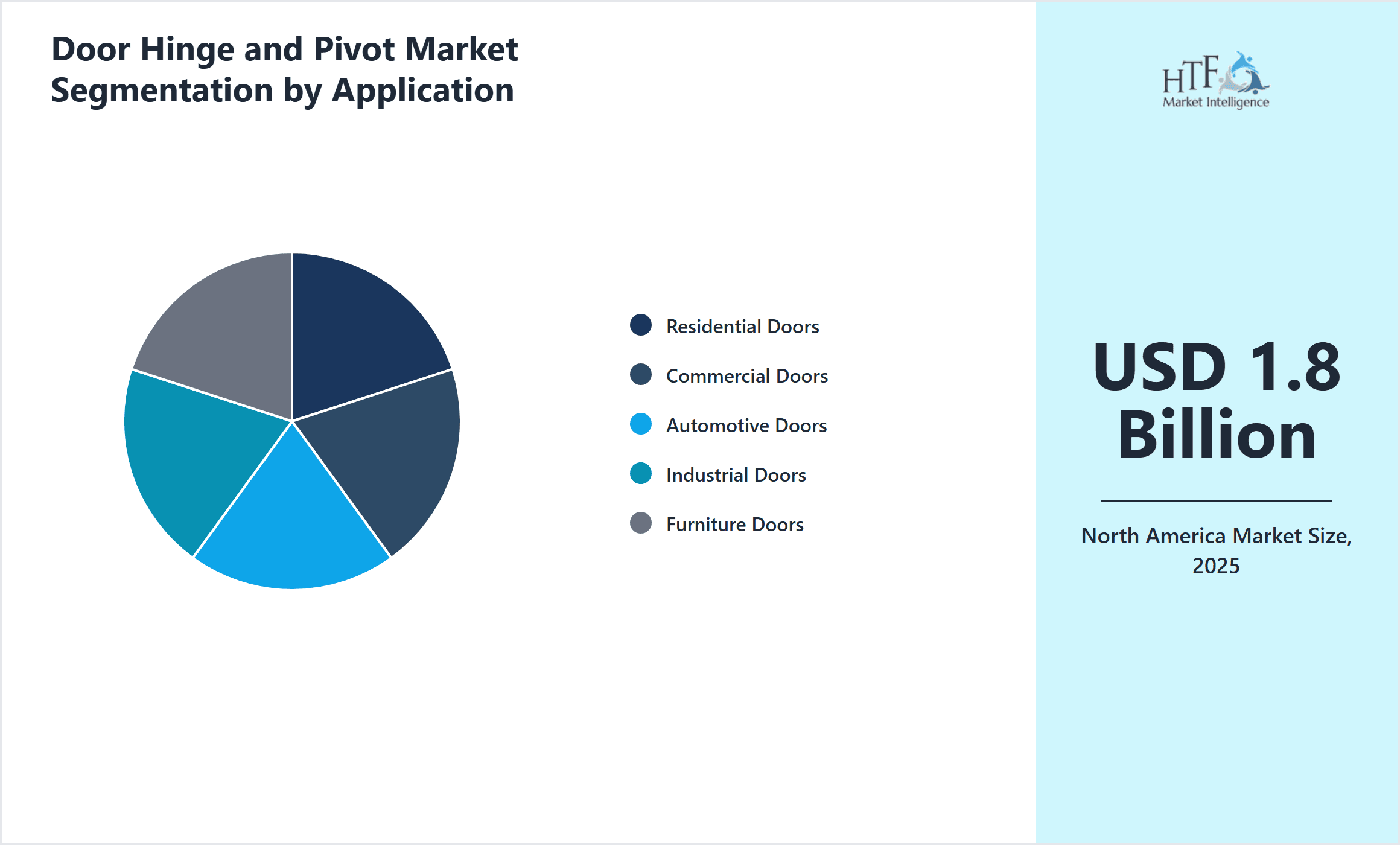

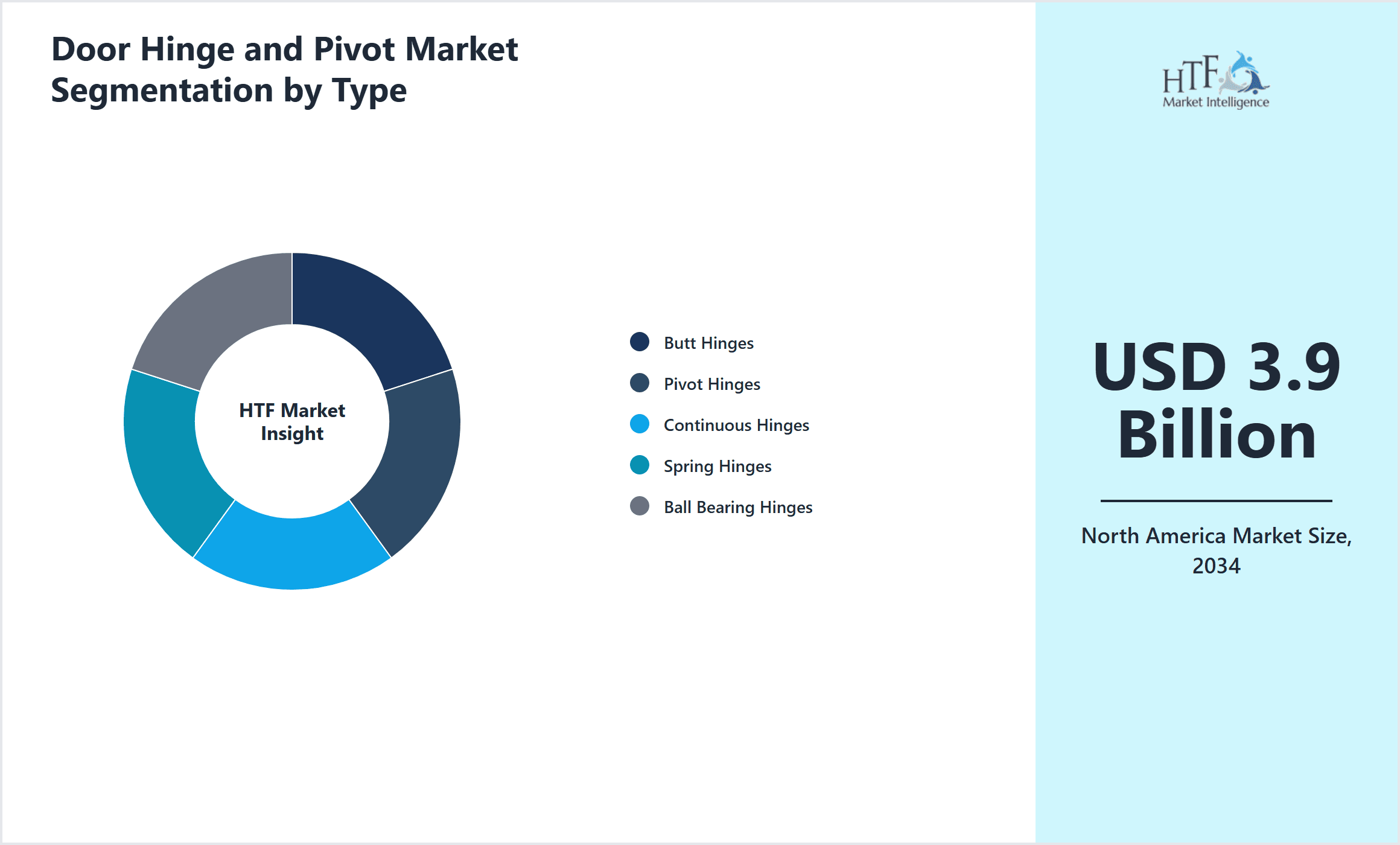

North America Door Hinge and Pivot Market is segmented by Application (Residential Doors, Commercial Doors, Automotive Doors, Industrial Doors, Furniture Doors), Type (Butt Hinges, Pivot Hinges, Continuous Hinges, Spring Hinges, Ball Bearing Hinges), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Door Hinge and Pivot Market is a specialized segment of the broader hardware and construction industry focused on components facilitating door movement and security. This market includes various hinge types such as butt hinges, pivot hinges, continuous hinges, spring hinges, and ball bearing hinges, each designed to meet specific application requirements across residential, commercial, automotive, industrial, and furniture door sectors. The market covers the design, production, and distribution of these components, emphasizing durability, material innovation, and ease of installation. Increasing construction activities, rising automotive production, and growing renovation projects across the United States, Canada, and Mexico drive demand. Technological advancements have introduced smart and corrosion-resistant materials, enhancing product life and performance. Regulatory adherence to safety and fire standards further shapes product development. Over the forecast period to 2034, the market is expected to witness steady growth fueled by infrastructure expansion, urbanization, and evolving consumer preferences for high-quality, reliable door hardware solutions.

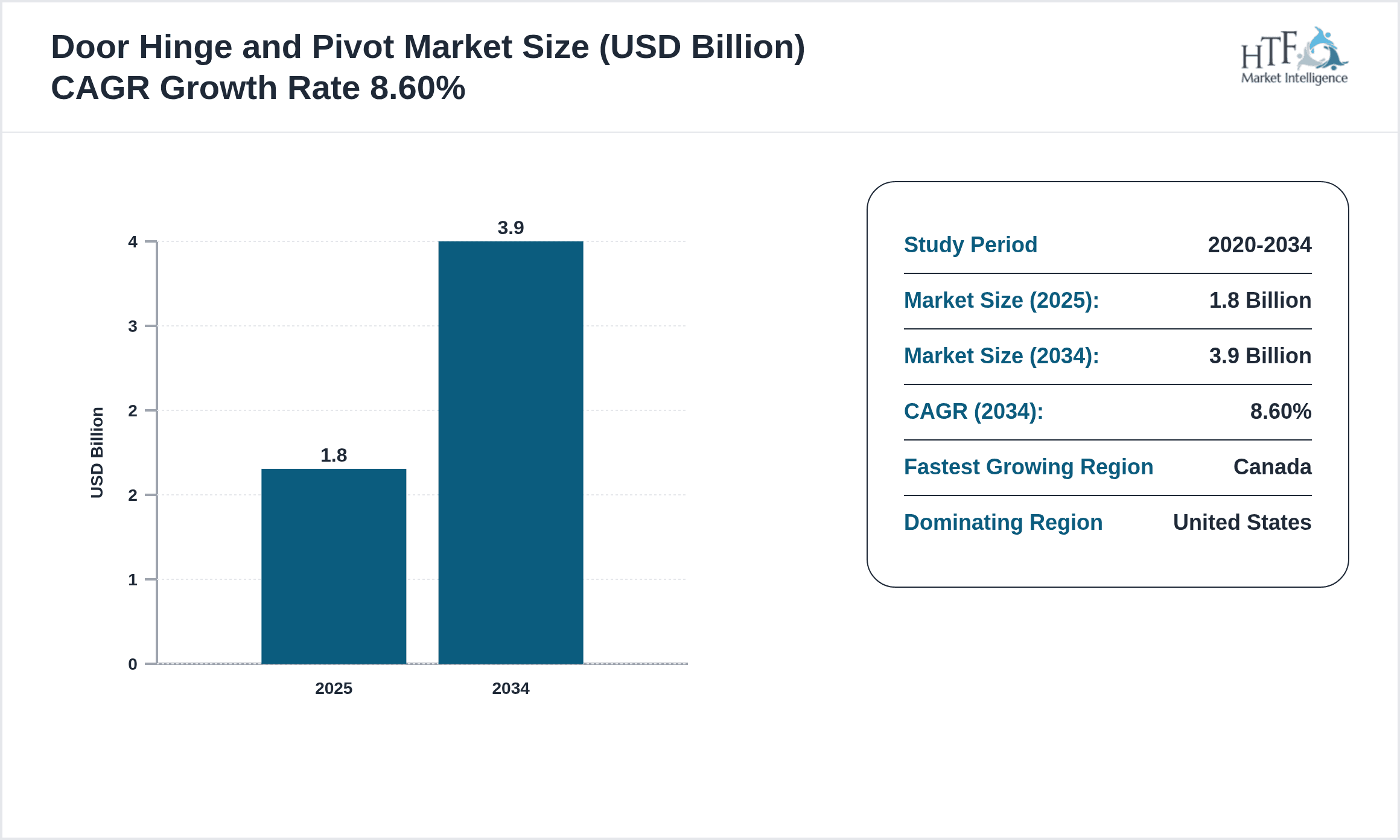

- •Key highlights of the North America Door Hinge and Pivot Market include a base market size of USD 1.8 Billion in 2025, projected to reach USD 3.9 Billion by 2034, reflecting a robust CAGR of 8.6%. Butt hinges dominate the product segment, capturing the largest market share due to their wide applicability, while pivot hinges are the fastest growing type, driven by demand for modern architectural designs. Residential and commercial door applications lead usage, supported by steady construction growth in the region. The United States holds the largest market share, with Canada exhibiting the highest growth rate, indicating expanding opportunities in both mature and emerging markets within North America.

- •This market presents significant strategic value for door hardware manufacturers, distributors, construction firms, and automotive OEMs. Its growth is tightly linked to infrastructure investments, urban development, and trends in door design and functionality. Understanding regional regulatory requirements and material innovations is critical for stakeholders to maintain competitive advantage. The market also offers lucrative opportunities in smart hinge technologies and sustainable materials, aligning with increasing demand for energy-efficient and secure building solutions. Consequently, businesses engaging in this market can capitalize on evolving architectural trends and expanding end-use sectors by leveraging innovation and strategic partnerships.

Competitive Landscape

The North America Door Hinge and Pivot Market is characterized by intense competition among both global conglomerates and regional specialized manufacturers. Market players focus heavily on product innovation, quality enhancement, and strategic distribution to capture and retain market share. Competitive strategies include investing in R&D to develop corrosion-resistant, smart, and durable hinge solutions tailored to diverse applications such as residential, commercial, and automotive doors. Companies also leverage mergers, acquisitions, and strategic partnerships to expand their geographical reach and product portfolios. Pricing strategies vary, with premium products targeting high-end construction and automotive sectors, while cost-effective solutions attract mass-market demand. Distribution channels are diversified, including direct sales, hardware distributors, and e-commerce platforms, increasing market accessibility. Regulatory compliance and certification act as competitive differentiators. Overall, the market rivalry is expected to intensify as demand grows and technological advancements accelerate, compelling players to continuously innovate and optimize operational efficiencies to sustain leadership positions.

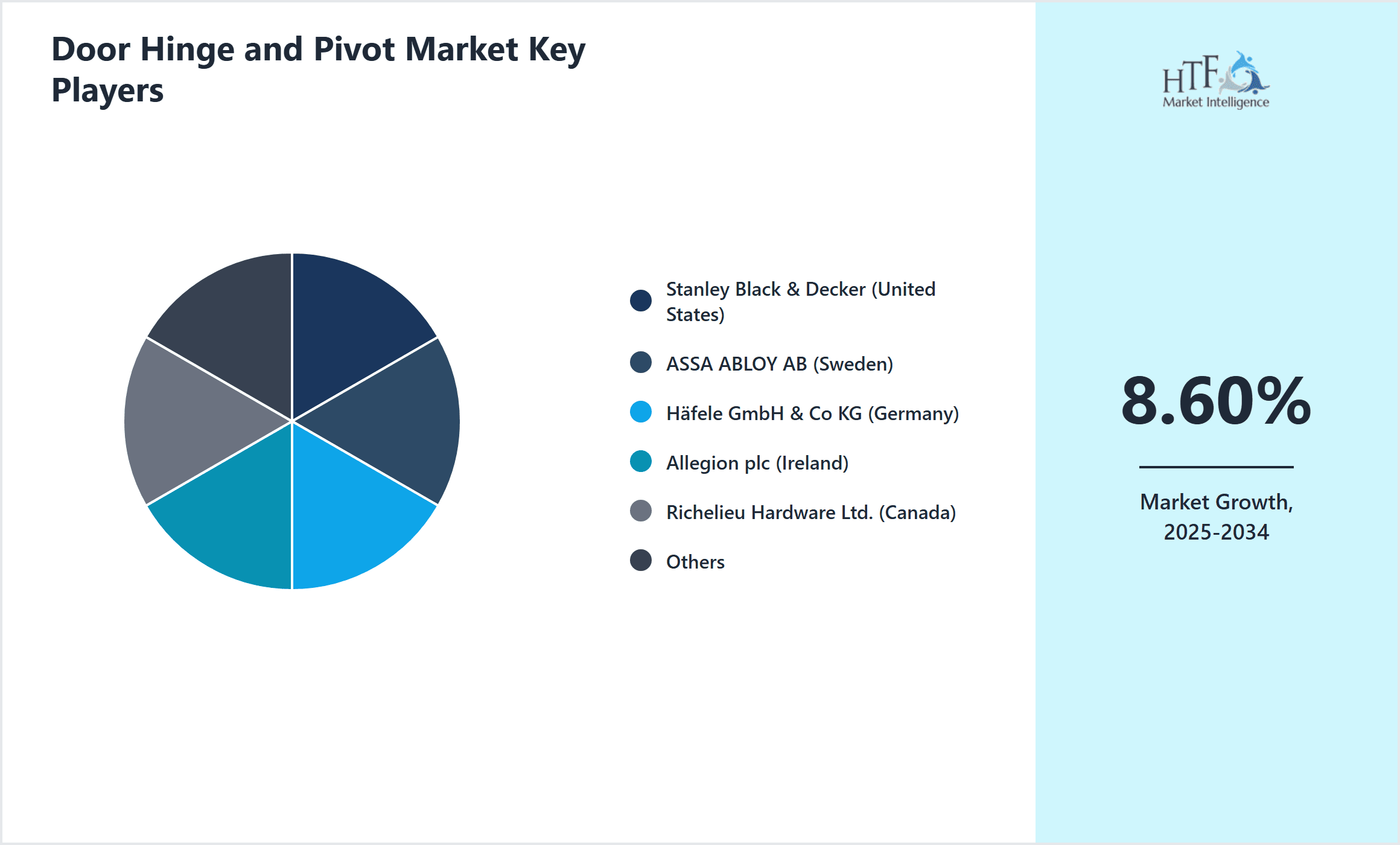

Leading Companies in Door Hinge and Pivot Market

- •Stanley Black & Decker (United States)

- •ASSA ABLOY AB (Sweden)

- •Häfele GmbH & Co KG (Germany)

- •Allegion plc (Ireland)

- •Richelieu Hardware Ltd. (Canada)

- •Sugatsune Kogyo Co., Ltd. (Japan)

- •Hettich Holding GmbH & Co. oHG (Germany)

- •Blum GmbH (Austria)

- •DormaKaba Holding AG (Switzerland)

- •Roto Frank AG (Germany)

- •Southco, Inc. (United States)

- •Hager Companies (United States)

- •Deltana Enterprises, Inc. (United States)

- •Sugatsune America, Inc. (United States)

- •Emtek Products, Inc. (United States)

- •Prime-Line Products (United States)

- •Ives Hardware (United States)

- •Andersen Corporation (United States)

- •Hafele America Co. (United States)

- •Leslie's Hardware & Manufacturing Co. (United States)

- •National Hardware (United States)

- •Kwikset Corporation (United States)

- •Yale Security Inc. (United States)

- •Hollow Metal Solutions (United States)

- •Deltana Hardware (Canada)

Door Hinge and Pivot Market Segmentation Overview

- •By Product Type

- ◦Butt Hinges

- ◦Pivot Hinges

- ◦Continuous Hinges

- ◦Spring Hinges

- ◦Ball Bearing Hinges

- •By Application

- ◦Residential Doors

- ◦Commercial Doors

- ◦Automotive Doors

- ◦Industrial Doors

- ◦Furniture Doors

- •By End User

- ◦Construction Industry

- ◦Automotive Manufacturing

- ◦Furniture Manufacturing

- ◦Renovation & Remodeling

- •By Distribution Channel

- ◦Direct Sales

- ◦Hardware Distributors

- ◦Online Retail

- ◦Specialty Stores

Growth Dynamics

- •The North America Door Hinge and Pivot Market benefits from consistent growth drivers such as rising residential and commercial construction projects, which increase demand for reliable door hardware. Urbanization and population growth fuel new housing developments and infrastructure expansion, thereby creating substantial opportunities. Additionally, the automotive sector's expansion, especially in electric and smart vehicle manufacturing, propels demand for innovative hinges that meet stringent performance standards. Technological advancements in materials, such as corrosion-resistant alloys and smart hinge systems, further boost market growth. Consumer preference for durable, aesthetically pleasing door components also supports adoption. Government incentives for energy-efficient building practices encourage the integration of advanced door hardware solutions. Together, these factors drive steady market expansion, encouraging manufacturers to innovate and invest in product development.

- •Market trends include the increasing incorporation of smart technology in door hinges and pivots, enabling features like automated opening, remote access, and enhanced security. Sustainable and eco-friendly material usage is gaining momentum, reflecting growing environmental awareness among consumers and regulatory bodies. Customization and modular design options are becoming popular, allowing end-users to tailor door hardware to specific aesthetic and functional needs. The surge in e-commerce and digital distribution channels has improved product accessibility and competitive pricing. Furthermore, collaborations between hardware manufacturers and technology firms are fostering innovation in integrated door systems. These evolving trends are shaping the market landscape by enhancing product offerings and expanding customer reach.

- •Market restraints include the volatility of raw material prices, particularly metals like steel and aluminum, which can increase production costs and affect pricing strategies. Supply chain disruptions caused by geopolitical tensions and global events have occasionally led to delays and increased logistics expenses. Additionally, the prevalence of counterfeit or low-quality door hardware in certain distribution channels undermines brand reputation and customer trust. Regulatory compliance with fire safety, security, and environmental standards requires continuous investment in testing and certification, posing challenges for smaller manufacturers. The presence of well-established players with strong brand loyalty also creates barriers for new entrants seeking market penetration.

- •Growth opportunities arise from the expanding smart home market, where integration of intelligent door hinges with home automation systems is highly sought after. There is potential for innovation in energy-efficient hinge designs that contribute to building sustainability goals. Emerging subsectors such as modular construction and prefabricated housing offer new application avenues for specialized door hardware. Geographic expansion within underserved regions of North America, including growing urban centers in Canada and Mexico, presents additional demand prospects. Collaborations with automotive manufacturers for electric and autonomous vehicle doors also offer significant market potential. Furthermore, increasing renovation activities in mature markets provide steady demand for replacement and upgrade products.

- •Key challenges include managing fluctuating raw material costs and mitigating supply chain risks that may impact timely delivery and profitability. Navigating complex regulatory requirements across different countries in North America demands continuous compliance efforts and associated costs. Intense competition from low-cost imports pressures domestic manufacturers to differentiate through innovation and quality. The need for skilled labor and advanced manufacturing capabilities poses operational challenges for smaller companies. Additionally, changing consumer preferences require agile product development strategies to maintain relevance. Addressing counterfeit product infiltration requires robust quality control and brand protection measures to preserve market integrity.

Market Trends

- •The adoption of smart door hinges integrated with IoT technology is transforming the North America market by enhancing security and convenience in residential and commercial sectors. Manufacturers are increasingly offering products with automated locking and remote control features, catering to modern building automation demands. This trend is accelerating due to rising consumer interest in smart home solutions and commercial security enhancements.

- •Sustainability is a significant trend influencing product development, with manufacturers focusing on eco-friendly materials and processes. Recycled metals and biodegradable coatings are gaining traction, aligning with regulatory mandates and consumer environmental consciousness. This shift is also fostering innovation in hinge durability and lifecycle performance.

- •The growth of e-commerce platforms has expanded the availability and variety of door hinges and pivots, enabling easier access for contractors and end-users. This digital transformation supports competitive pricing and rapid product delivery, reshaping traditional distribution models and broadening market reach.

- •Customization and modularity in hinge design are trending, allowing architects and builders to specify hardware that complements unique door styles and functional requirements. This trend supports the demand for aesthetic diversity and tailored performance in both new constructions and renovations.

- •Collaborations between hardware manufacturers and technology companies to develop integrated door systems with enhanced functionality are increasing. Such partnerships foster innovation, combining mechanical engineering with digital solutions to meet evolving market expectations for security and automation.

- •Rising demand for fire-rated and security-enhanced hinges reflects growing regulatory focus on safety standards in commercial and public buildings, influencing product specifications and certification requirements. Compliance with these standards is becoming a key purchasing criterion.

- •The integration of advanced materials like composites and alloys is improving product performance by reducing weight, enhancing corrosion resistance, and extending service life, thereby aligning with industry requirements for durability and maintenance efficiency.

Market Opportunities

- •The expansion of smart home technologies offers significant opportunities for innovative door hinge solutions that enable automation, remote access, and enhanced security features. Manufacturers can capitalize on this growing segment by developing compatible and interoperable products tailored for connected environments.

- •Emerging urban centers in Canada and Mexico present untapped markets for door hinge and pivot products, driven by increasing construction and renovation activities. Targeting these regions with localized strategies can yield substantial growth.

- •Investment in sustainable and energy-efficient hinge designs that contribute to green building certifications can differentiate products and meet increasing regulatory and consumer demands for environmental responsibility.

- •Collaborations and strategic alliances with automotive OEMs focusing on electric and autonomous vehicles open avenues for specialized hinge innovations addressing unique operational and safety requirements of automotive doors.

- •The growing renovation and remodeling market in North America creates recurring demand for replacement hinges and pivots, offering steady revenue streams and opportunities for product upgrades and aftermarket services.

- •Digital transformation in sales channels, including e-commerce and direct-to-consumer platforms, enables broader market access, improved customer engagement, and personalized marketing approaches to enhance sales performance.

- •Development of modular and customizable hinge systems tailored to diverse architectural styles presents opportunities to cater to niche segments seeking unique aesthetic and functional solutions.

Market Challenges

- •Volatility in raw material prices, especially metals, imposes cost pressures on manufacturers, affecting pricing strategies and profit margins. Managing these fluctuations requires efficient procurement and inventory management practices.

- •Supply chain disruptions due to geopolitical tensions and global events can cause delays and increased logistics costs, impacting timely product delivery and customer satisfaction.

- •Compliance with diverse and evolving regulatory standards across the North American countries demands continuous investment in certification and quality assurance, increasing operational complexity for manufacturers.

- •Intense competition from low-cost imports challenges domestic players to maintain market share through innovation, quality differentiation, and cost efficiency.

- •The infiltration of counterfeit and low-quality products in some distribution channels undermines brand reputation and poses safety risks, necessitating stronger quality control and market surveillance.

- •A shortage of skilled labor and advanced manufacturing capabilities limits production scalability and innovation potential for smaller companies in the market.

- •Rapid changes in consumer preferences require agility in product development and marketing strategies to ensure alignment with market demands and avoid obsolescence.

Regulatory Framework

- •Between 2020 and 2025, North America implemented stringent fire safety regulations mandating the use of fire-rated door hardware, including hinges and pivots, to enhance building occupant safety. Compliance requires rigorous product testing and certification, impacting design and material selection.

- •Environmental regulations introduced during 2021-2024 emphasize the reduction of volatile organic compounds (VOCs) in coatings and finishes used on door hardware. Manufacturers have adapted by reformulating products to meet these eco-friendly standards, influencing production processes.

- •The Americans with Disabilities Act (ADA) standards enforced updated accessibility requirements for door hardware, including hinge designs facilitating ease of use and compliance with force and maneuvering criteria. These standards affect product specifications and installation practices.

- •Canada’s National Building Code revisions in 2023 introduced enhanced requirements for durability and security of door hardware in commercial buildings, encouraging adoption of advanced materials and locking mechanisms integrated with hinges and pivots.

- •Mexico enacted regulations in 2022 targeting quality assurance and import controls for construction hardware, including door hinges and pivots, to prevent substandard products from entering the market, strengthening local industry competitiveness.

Market Intelligence

- •15th March 2025, Stanley Black & Decker launched an innovative line of smart butt hinges designed for residential and commercial applications, featuring integrated sensors for automated door status monitoring and remote access control. This product aims to enhance security and convenience in smart buildings and is targeted at the North American market’s growing demand for connected home solutions. The launch reflects the company's strategic focus on digital integration and sustainability by using recycled materials in hinge construction. This advancement positions Stanley Black & Decker as a technology leader in the door hardware sector and is expected to drive significant market adoption.

- •22nd July 2025, Allegion plc introduced a new range of corrosion-resistant pivot hinges engineered specifically for high-moisture environments in commercial and industrial settings. Utilizing advanced stainless steel alloys and proprietary coatings, the product enhances durability and reduces maintenance needs. This innovation addresses the increasing demand driven by infrastructure projects in coastal and humid regions of North America, aligning with regulatory requirements for performance and safety. Allegion's strategic initiative to cater to niche market segments underscores its commitment to product differentiation and environmental resilience.

- •10th January 2025, ASSA ABLOY AB announced a strategic partnership with a leading IoT technology firm to develop next-generation smart door hardware integrating real-time monitoring, access control, and energy efficiency features. This collaboration aims to accelerate innovation in the North American door hinge and pivot market by combining mechanical expertise with cutting-edge digital capabilities. The initiative is expected to cater to rising demand for smart building solutions, providing enhanced security and operational efficiency for commercial and residential customers. The partnership strengthens ASSA ABLOY’s market position and expands its product portfolio in the connected hardware space.

- •30th April 2025, Richelieu Hardware Ltd. completed the acquisition of a regional door hardware manufacturer specializing in custom hinge designs for furniture and cabinetry. This acquisition enhances Richelieu’s product range and manufacturing capacity, enabling better service to the North American renovation and furniture markets. The deal supports Richelieu’s growth strategy focused on expanding its presence in niche segments and improving supply chain efficiencies. The expansion is anticipated to strengthen competitive positioning and accelerate innovation in customizable door hinge solutions.

- •Source: Official press releases and company announcements

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 3.9 Billion |

| CAGR | 8.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.3% |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Stanley Black & Decker (United States), ASSA ABLOY AB (Sweden), Häfele GmbH & Co KG (Germany), Allegion plc (Ireland), Richelieu Hardware Ltd. (Canada), Sugatsune Kogyo Co., Ltd. (Japan), Hettich Holding GmbH & Co. oHG (Germany), Blum GmbH (Austria), DormaKaba Holding AG (Switzerland), Roto Frank AG (Germany), Southco, Inc. (United States), Hager Companies (United States), Deltana Enterprises, Inc. (United States), Sugatsune America, Inc. (United States), Emtek Products, Inc. (United States), Prime-Line Products (United States), Ives Hardware (United States), Andersen Corporation (United States), Hafele America Co. (United States), Leslie's Hardware & Manufacturing Co. (United States), National Hardware (United States), Kwikset Corporation (United States), Yale Security Inc. (United States), Hollow Metal Solutions (United States), Deltana Hardware (Canada) |

North America Door Hinge and Pivot Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.