EMEA Heavy Commercial Vehicle Engine Oil Market - Outlook 2024-2034

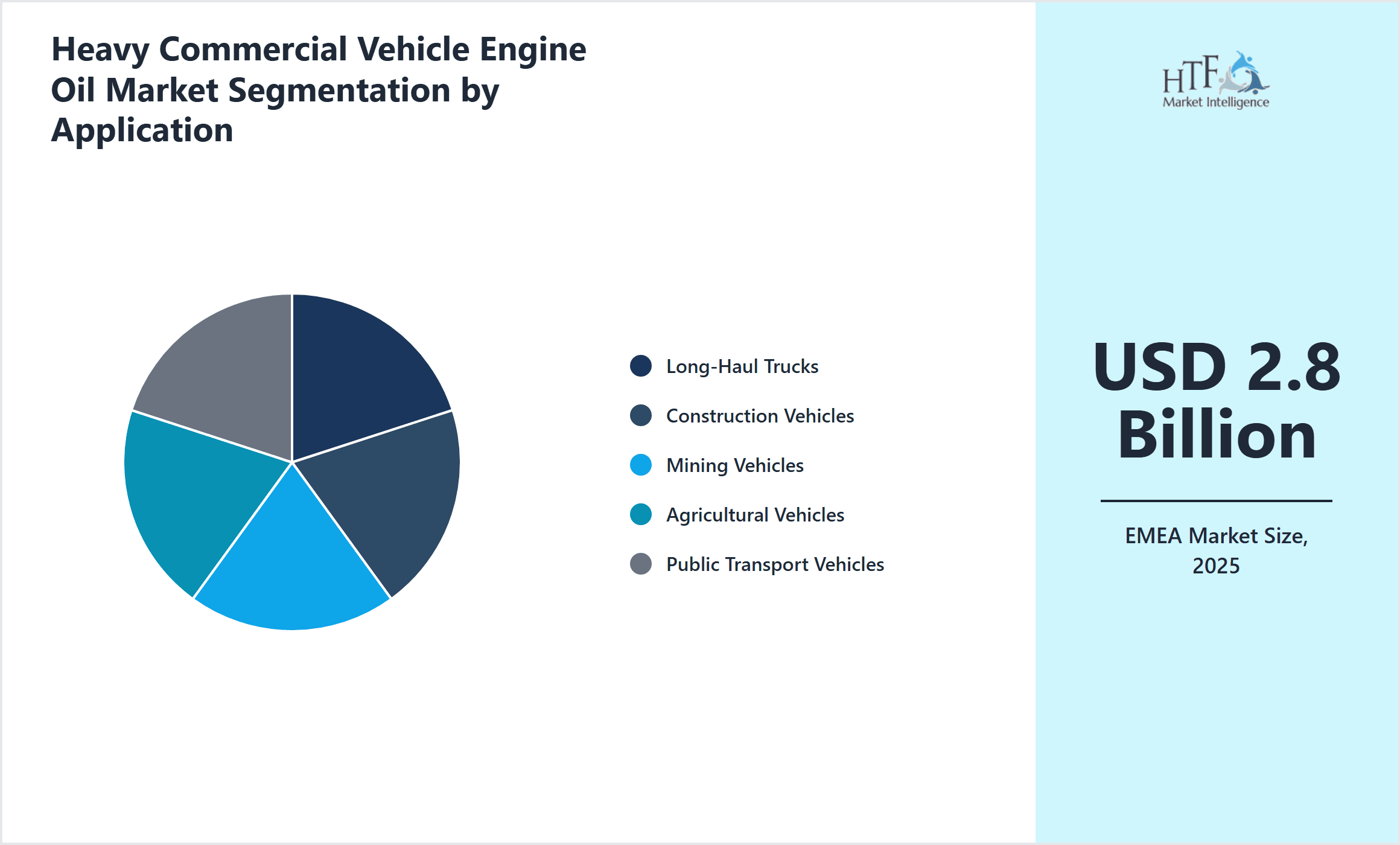

EMEA Heavy Commercial Vehicle Engine Oil Market is segmented by Engine Oil Type (Synthetic Heavy Commercial Vehicle Engine Oil, Semi-Synthetic Heavy Commercial Vehicle Engine Oil, Mineral Heavy Commercial Vehicle Engine Oil, Bio-Based Heavy Commercial Vehicle Engine Oil, Additive-Enhanced Heavy Commercial Vehicle Engine Oil), Application Segment (Long-Haul Trucks, Construction Vehicles, Mining Vehicles, Agricultural Vehicles, Public Transport Vehicles), End-User Industry (Logistics & Freight Companies, Construction & Mining Firms, Agricultural Enterprises, Public Transportation Authorities), Distribution Channel (Direct Sales, Distributors and Wholesalers, Aftermarket Retailers), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Heavy Commercial Vehicle Engine Oil market is dedicated to lubricants engineered for the heavy-duty commercial vehicle sector, including trucks, construction, mining, agricultural, and public transportation vehicles. This market caters to the rigorous demands of heavy engines, emphasizing durability, thermal stability, and emission compliance. Engine oils in this sector are classified into synthetic, semi-synthetic, mineral, bio-based, and additive-enhanced types, each serving specific performance and environmental requirements. The market is shaped by advancements in lubricant technology, evolving emission regulations such as Euro VI standards, and the rising focus on sustainability and fuel economy. Regional dynamics are influenced by industrial growth in Europe, infrastructure expansion in the Middle East, and increasing fleet modernization. The commercial vehicle segment drives demand for high-performance oils that extend engine life and reduce maintenance costs. This market serves various applications, including long-haul freight, urban transit, and heavy equipment operations, reflecting a complex ecosystem of manufacturers, distributors, and end-users across the EMEA region.

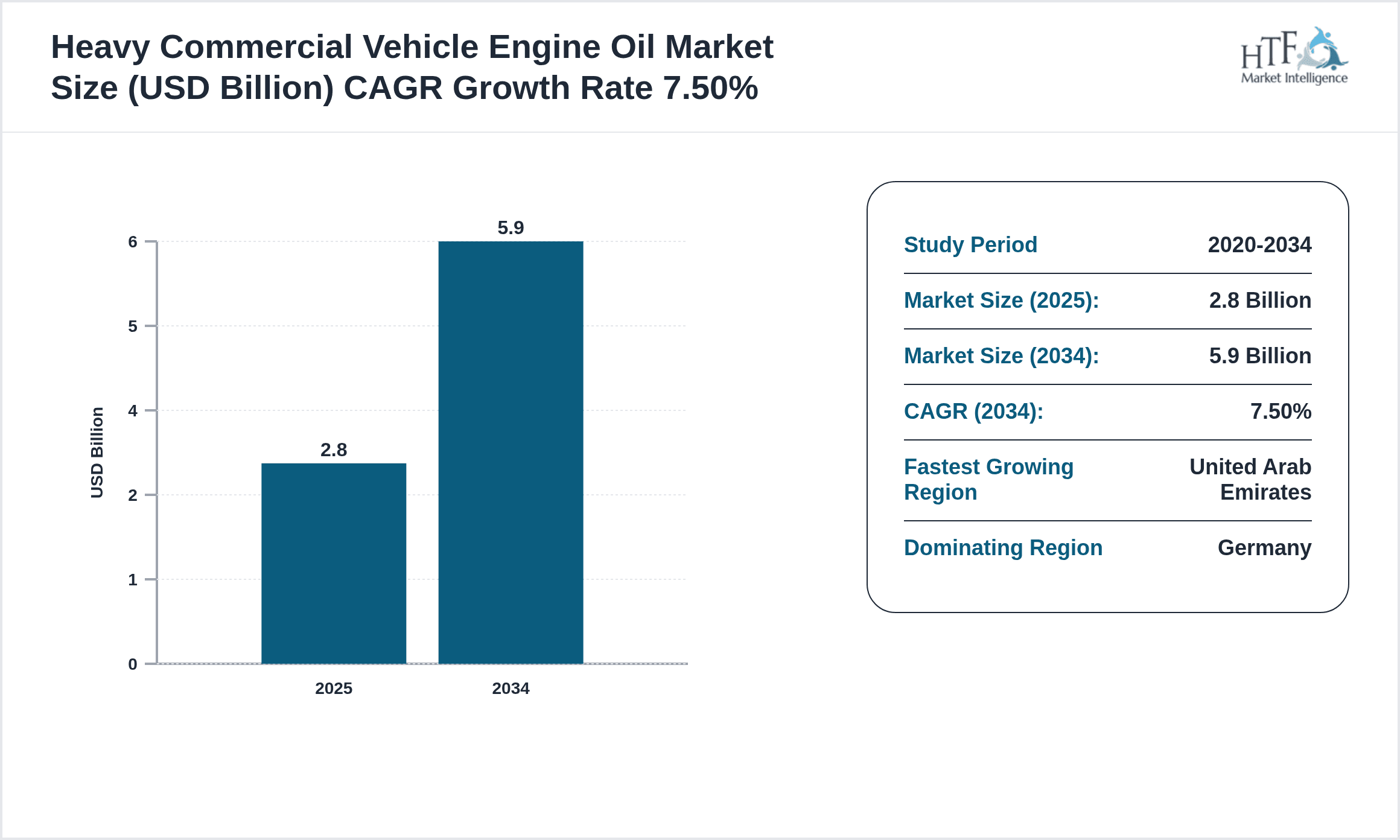

- •Key highlights of the EMEA Heavy Commercial Vehicle Engine Oil market include a base market size of USD 2.8 billion in 2024, projected to reach USD 5.9 billion by 2034, representing a robust CAGR of 7.5%. Synthetic oils dominate the product type segment due to their superior performance and compliance with stringent emission norms. The long-haul trucking application leads in market share, supported by expanding logistics and freight activities across Europe and the Middle East. Germany holds the position of the dominating regional market, benefiting from its advanced automotive industry and stringent environmental regulations. Meanwhile, the United Arab Emirates is the fastest-growing country, driven by infrastructure investments and fleet expansions. Market growth is propelled by increasing demand for fuel-efficient lubricants, technological innovation, and rising environmental consciousness among fleet operators.

- •The strategic importance of the EMEA Heavy Commercial Vehicle Engine Oil market lies in its contribution to sustaining the heavy commercial transport and industrial sectors critical to regional economies. High-quality engine oils enhance operational efficiency, reduce downtime, and help meet evolving emission requirements, aligning with global sustainability goals. For stakeholders including lubricant manufacturers, vehicle OEMs, fleet operators, and regulatory bodies, understanding market dynamics enables informed decisions on product development, investments, and compliance strategies. The market’s evolution reflects broader trends in vehicle electrification, alternative fuels, and digital fleet management, underscoring the need for innovative lubricants that support diverse engine technologies. Consequently, the market serves as a bellwether for advancements in heavy vehicle maintenance and environmental stewardship across EMEA.

Competitive Landscape

The competitive landscape of the EMEA Heavy Commercial Vehicle Engine Oil market is characterized by intense rivalry among global and regional players, each leveraging innovation, strategic partnerships, and expansive distribution networks to consolidate market position. Leading companies focus on developing high-performance synthetic and bio-based lubricants that meet or exceed stringent Euro VI emission standards, thereby gaining a competitive edge. Product differentiation through proprietary additive technologies, extended oil change intervals, and sustainability credentials is central to market competition. Firms invest heavily in R&D to introduce eco-friendly and fuel-efficient formulations, responding to increasing regulatory pressures and consumer demand for green products. Regional players benefit from local market knowledge and tailored products suited to specific climatic and operational conditions. Market entry barriers include high capital requirements, stringent quality certifications, and established brand loyalty among fleet operators. The increasing trend towards digitalization and smart lubricants further intensifies competition, as companies seek to integrate technology for predictive maintenance and enhanced vehicle performance analytics.

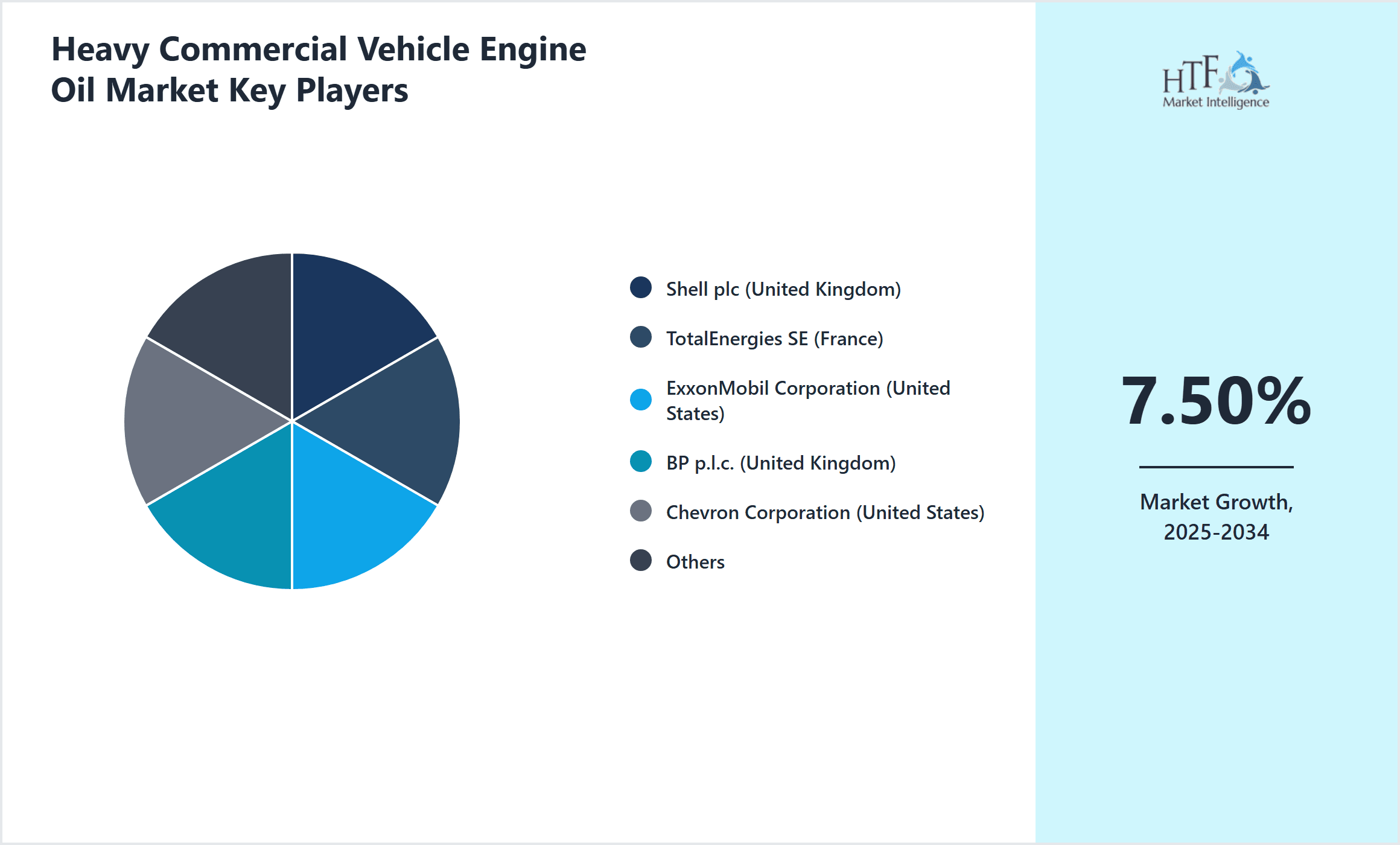

Prominent Players in Heavy Commercial Vehicle Engine Oil Market

- •Shell plc (United Kingdom)

- •TotalEnergies SE (France)

- •ExxonMobil Corporation (United States)

- •BP p.l.c. (United Kingdom)

- •Chevron Corporation (United States)

- •Fuchs Petrolub SE (Germany)

- •Petro-Canada Lubricants Inc. (Canada)

- •Motul (France)

- •Valvoline Inc. (United States)

- •Lukoil Lubricants Europe B.V. (Netherlands)

- •Neste Oyj (Finland)

- •Idemitsu Kosan Co., Ltd. (Japan)

- •Total Lubmarine (France)

- •Petronas Lubricants International (Malaysia)

- •Intertek Group plc (United Kingdom)

- •Kixx Lubricants (South Korea)

- •Chevron Oronite Company LLC (United States)

- •Orlen Oil Sp. z o.o. (Poland)

- •Repsol S.A. (Spain)

- •Caltex (Chevron Corporation) (United Kingdom)

- •ConocoPhillips Company (United States)

- •Nynas AB (Sweden)

- •Havoline (Chevron Corporation) (United Kingdom)

- •Eni S.p.A. (Italy)

- •Petrobras Lubrificantes S.A. (Brazil)

Market Breakdown

- •By Engine Oil Type

- ◦Synthetic Heavy Commercial Vehicle Engine Oil

- ◦Semi-Synthetic Heavy Commercial Vehicle Engine Oil

- ◦Mineral Heavy Commercial Vehicle Engine Oil

- ◦Bio-Based Heavy Commercial Vehicle Engine Oil

- ◦Additive-Enhanced Heavy Commercial Vehicle Engine Oil

- •By Application Segment

- ◦Long-Haul Trucks

- ◦Construction Vehicles

- ◦Mining Vehicles

- ◦Agricultural Vehicles

- ◦Public Transport Vehicles

- •By End-User Industry

- ◦Logistics & Freight Companies

- ◦Construction & Mining Firms

- ◦Agricultural Enterprises

- ◦Public Transportation Authorities

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors and Wholesalers

- ◦Aftermarket Retailers

Growth Dynamics

The EMEA Heavy Commercial Vehicle Engine Oil market is driven by increasing demand for fuel-efficient and low-emission lubricants aligned with stringent Euro VI and similar emission standards across the region. Growing fleet modernization in logistics, construction, and public transport sectors necessitates advanced synthetic lubricants that extend engine life and reduce maintenance costs. Additionally, rising infrastructure investments in Middle Eastern countries fuel demand for heavy-duty construction and mining vehicles, boosting engine oil consumption. Technological advances in additive chemistry enhance oil performance under extreme operating conditions, providing competitive differentiation. The shift towards bio-based and environmentally sustainable oils is also catalyzed by government incentives and corporate sustainability commitments. Together, these factors underpin a resilient growth trajectory for the market, with stakeholders increasingly prioritizing product innovation and compliance to capitalize on expanding commercial vehicle operations.

Market Trends

Emerging trends in the EMEA Heavy Commercial Vehicle Engine Oil market include a significant shift towards synthetic and bio-based lubricants driven by environmental regulations and consumer preference for eco-friendly products. Digital transformation in fleet management facilitates the adoption of smart lubricants that provide real-time engine health monitoring, enabling predictive maintenance and reducing downtime. Companies are investing in developing multi-grade oils that perform well across diverse climatic conditions prevalent in the EMEA region. Furthermore, collaborations between lubricant manufacturers and vehicle OEMs are intensifying to co-develop tailor-made oils optimized for specific engine types. The rise of electric and hybrid commercial vehicles is prompting exploration of new lubricant formulations and service models. These trends collectively contribute to enhanced operational efficiency and sustainability in heavy commercial vehicle maintenance.

Market Opportunities

The EMEA Heavy Commercial Vehicle Engine Oil market offers considerable opportunities in expanding bio-based lubricant segments, propelled by increasing regulatory support and consumer environmental consciousness. Rapid urbanization and infrastructure development in Middle Eastern and African countries present untapped markets for lubricant suppliers. Innovations in high-performance synthetic oils tailored to emerging vehicle technologies, including hybrid and alternative fuel engines, open avenues for product differentiation. Strategic partnerships with fleet operators and OEMs enable deeper market penetration and customization of offerings. Additionally, digitalization and IoT integration in vehicle maintenance services create opportunities for value-added services and subscription-based lubricant supply models. Expanding aftermarket channels and e-commerce platforms further enhance accessibility and growth potential across the EMEA region.

Market Challenges

Challenges facing the EMEA Heavy Commercial Vehicle Engine Oil market include fluctuating raw material prices impacting cost structures and profitability. Compliance with diverse and evolving regulatory requirements across Europe, the Middle East, and Africa increases operational complexity for manufacturers and distributors. Market penetration in developing regions is hindered by limited infrastructure and fragmented supply chains. High competition from established global brands creates pricing pressures and necessitates continuous innovation, which demands significant R&D investments. Additionally, the gradual shift towards electric commercial vehicles may reduce demand for traditional engine oils over the long term, requiring companies to adapt their portfolios. Counterfeit and low-quality lubricants in some markets pose risks to brand reputation and customer trust. Addressing these challenges requires strategic planning, regulatory alignment, and investment in technology and market development.

Regulatory Framework

Between 2019 and 2024, the EMEA Heavy Commercial Vehicle Engine Oil market has been influenced by the implementation of Euro VI emission standards across the European Union, mandating lower particulate matter and NOx emissions for heavy-duty engines. This regulation necessitates the use of advanced synthetic and low SAPS (sulfated ash, phosphorus, sulfur) engine oils to ensure compliance and engine protection. The European Chemicals Agency’s REACH regulation imposes strict chemical safety standards affecting lubricant formulations. In the Middle East, governments have introduced environmental policies aimed at reducing carbon footprints, encouraging bio-based lubricant adoption. Regional directives on waste oil management and recycling further shape market practices. These regulations collectively drive innovation in lubricant technology, requiring manufacturers to invest in R&D and certification processes to maintain market access and competitiveness.

Market Intelligence

- •15th July 2024, Shell plc launched a new line of high-performance synthetic engine oils specifically designed for Euro VI heavy commercial vehicles, featuring enhanced thermal stability and extended drain intervals to reduce maintenance costs and emissions. This product targets long-haul trucking fleets across the EMEA region, aligning with sustainability goals and offering improved fuel economy. Shell’s initiative reinforces its commitment to innovation and regulatory compliance in a competitive market environment. Source: Shell Official Press Release

- •3rd November 2023, TotalEnergies SE introduced a bio-based heavy commercial vehicle engine oil developed to meet stringent environmental standards while delivering superior engine protection. The product uses renewable raw materials and advanced additive technology, aiming to capture growing demand in Europe and the Middle East for sustainable lubricants. This launch positions TotalEnergies as a leader in the green lubricant segment within the EMEA market. Source: TotalEnergies Corporate Announcement

- •20th March 2024, ExxonMobil Corporation announced a strategic partnership with a leading European logistics company to supply premium synthetic engine oils across its heavy vehicle fleet. The collaboration includes joint R&D efforts to optimize lubricants for fleet-specific operating conditions, enhancing engine reliability and reducing environmental impact. This partnership illustrates the trend toward customized lubricant solutions and integrated service models. Source: ExxonMobil Newsroom

- •12th September 2023, BP p.l.c. expanded its distribution network in the Middle East by acquiring a regional lubricant supplier, enhancing its market presence and access to emerging commercial vehicle segments. This acquisition supports BP’s growth strategy in EMEA, focusing on high-demand regions with increasing infrastructure development and fleet modernization. Source: BP Corporate Release

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.8 Billion |

| Forecast Year Market Size | USD 5.9 Billion |

| CAGR | 7.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.25% |

| Scope of Report | Market is segmented by Engine Oil Type (Synthetic Heavy Commercial Vehicle Engine Oil, Semi-Synthetic Heavy Commercial Vehicle Engine Oil, Mineral Heavy Commercial Vehicle Engine Oil, Bio-Based Heavy Commercial Vehicle Engine Oil, Additive-Enhanced Heavy Commercial Vehicle Engine Oil), Application Segment (Long-Haul Trucks, Construction Vehicles, Mining Vehicles, Agricultural Vehicles, Public Transport Vehicles), End-User Industry (Logistics & Freight Companies, Construction & Mining Firms, Agricultural Enterprises, Public Transportation Authorities), Distribution Channel (Direct Sales, Distributors and Wholesalers, Aftermarket Retailers) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Shell plc (United Kingdom), TotalEnergies SE (France), ExxonMobil Corporation (United States), BP p.l.c. (United Kingdom), Chevron Corporation (United States), Fuchs Petrolub SE (Germany), Petro-Canada Lubricants Inc. (Canada), Motul (France), Valvoline Inc. (United States), Lukoil Lubricants Europe B.V. (Netherlands), Neste Oyj (Finland), Idemitsu Kosan Co., Ltd. (Japan), Total Lubmarine (France), Petronas Lubricants International (Malaysia), Intertek Group plc (United Kingdom), Kixx Lubricants (South Korea), Chevron Oronite Company LLC (United States), Orlen Oil Sp. z o.o. (Poland), Repsol S.A. (Spain), Caltex (Chevron Corporation) (United Kingdom), ConocoPhillips Company (United States), Nynas AB (Sweden), Havoline (Chevron Corporation) (United Kingdom), Eni S.p.A. (Italy), Petrobras Lubrificantes S.A. (Brazil) |

EMEA Heavy Commercial Vehicle Engine Oil Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.