Global Mainline Rail Signalling Systems Market Size, Growth & Revenue 2024-2034

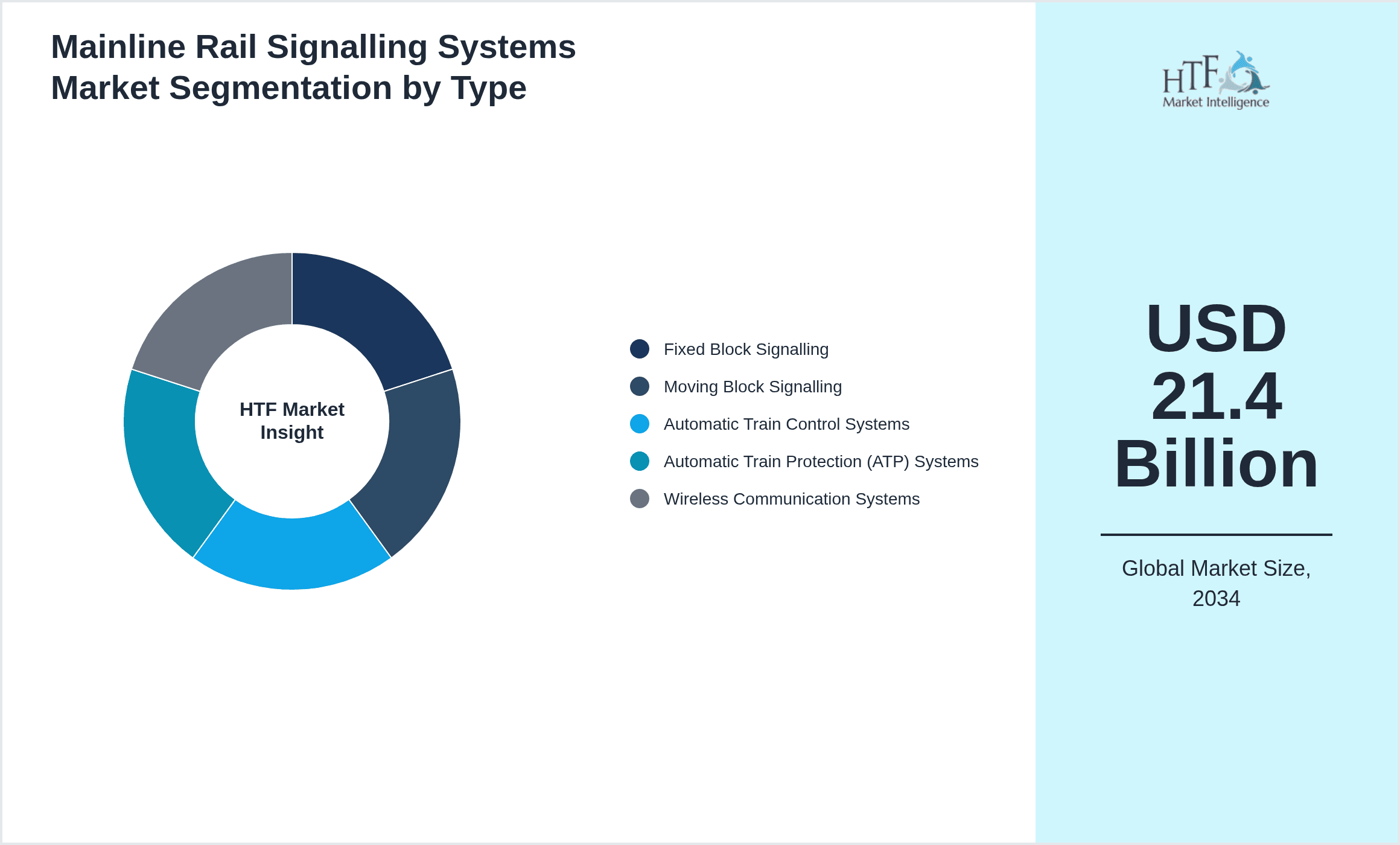

Global Mainline Rail Signalling Systems Market is segmented by Type (Fixed Block Signalling, Moving Block Signalling, Automatic Train Control Systems, Automatic Train Protection (ATP) Systems, Wireless Communication Systems), Application (Interlocking Systems, Train Control, Track Circuit, Level Crossing Protection, Communication-Based Train Control (CBTC)), End User (Freight Rail Operators, Passenger Rail Operators, Urban Rail Transit Authorities, Rail Infrastructure Companies), Deployment Model (On-Premise, Cloud-Based, Hybrid), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Mainline Rail Signalling Systems Market comprises a range of sophisticated signalling technologies designed to ensure the safe and efficient movement of trains on mainline railway networks worldwide. These systems include fixed block and moving block signalling, automatic train control, and wireless communication technologies that collectively improve operational safety, capacity, and reliability in rail transportation. The market covers hardware components such as signals, track circuits, interlocking devices, and communication equipment, along with software solutions for train control and monitoring. With increasing global investments in railway infrastructure modernization and growing demand for high-speed and automated train operations, the market is positioned for robust growth. Key applications include interlocking systems, train control, track circuits, and level crossing safety, serving freight and passenger rail sectors. The integration of digital and wireless signalling technologies is transforming traditional railway signalling towards more adaptive, efficient, and real-time control systems globally.

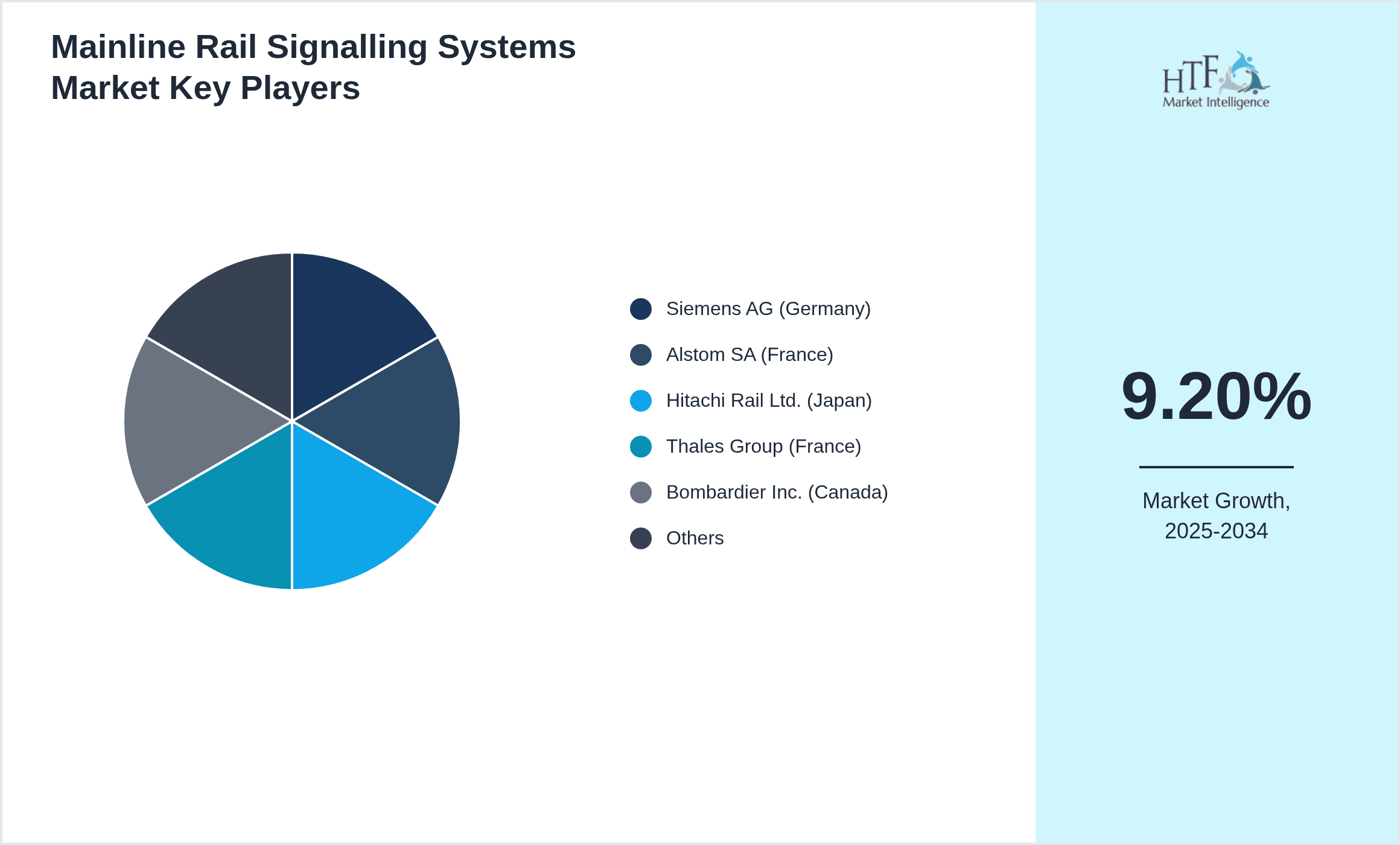

- •Key market highlights include an expected CAGR of 9.2% from 2024 to 2034, with the market size projected to reach USD 21.4 Billion by 2034 from USD 8.7 Billion in 2024. North America currently dominates the market due to extensive rail infrastructure and advanced technological adoption. Asia-Pacific is identified as the fastest-growing region driven by rapid railway expansions and modernization projects in countries like China and India. Fixed block signalling remains the leading technology segment, while wireless communication-based signalling exhibits the fastest growth owing to its enhanced efficiency and safety features. The market's growth is further supported by increasing governmental focus on railway safety standards and investments in intelligent transportation systems.

- •The value proposition of the Global Mainline Rail Signalling Systems Market lies in enabling railway operators to enhance safety, increase network capacity, and reduce operational delays through cutting-edge signalling technologies. These systems are critical for managing rail traffic in increasingly congested networks and are essential for the deployment of high-speed and automated train services. Stakeholders including rail infrastructure providers, signalling equipment manufacturers, and system integrators benefit from rising demand for digital and wireless signalling solutions. The market also supports sustainability goals by facilitating energy-efficient train operations and reducing the need for costly infrastructure expansions. Overall, the market plays a strategic role in advancing global rail transportation towards smarter, safer, and more connected networks.

Competitive Landscape

The competitive environment in the Global Mainline Rail Signalling Systems Market is highly dynamic, characterized by intense rivalry among established multinational corporations and emerging technology innovators. Market players focus on continuous innovation, investing heavily in R&D to develop advanced signalling solutions such as communication-based train control and wireless signalling systems. Strategic partnerships and collaborations with rail operators and infrastructure providers are common to enhance market positioning and expand geographic reach. Companies differentiate themselves through product quality, integration capabilities, and after-sales services. Mergers and acquisitions have been instrumental in consolidating market share and acquiring technological competencies. Pricing strategies vary with project scale and customization requirements, while barriers to entry include stringent regulatory standards and the need for proven safety certifications. Regional competition is influenced by government policies and infrastructure investment priorities. Future trends point to increased adoption of digital and AI-driven signalling systems to maintain competitive advantage.

Leading Companies in Mainline Rail Signalling Systems Market

- •Siemens AG (Germany)

- •Alstom SA (France)

- •Hitachi Rail Ltd. (Japan)

- •Thales Group (France)

- •Bombardier Inc. (Canada)

- •Mitsubishi Electric Corporation (Japan)

- •CAF (Construcciones y Auxiliar de Ferrocarriles) (Spain)

- •Ansaldo STS (Italy)

- •GE Transportation (United States)

- •Wabtec Corporation (United States)

- •Huawei Technologies Co., Ltd. (China)

- •Hyundai Rotem Company (South Korea)

- •Kapsch TrafficCom AG (Austria)

- •Toshiba Corporation (Japan)

- •Indra Sistemas S.A. (Spain)

- •Alfa Laval (Sweden)

- •Siemens Mobility GmbH (Germany)

- •General Electric Company (United States)

- •Bombardier Transportation GmbH (Germany)

- •Thales Rail Signalling Solutions (United Kingdom)

- •CAF Signalling Solutions (Spain)

- •Nokia Corporation (Finland)

- •Ericsson AB (Sweden)

- •Yokogawa Electric Corporation (Japan)

- •Digital Railway Technologies (United Kingdom)

Market Breakdown

- •By Type

- ◦Fixed Block Signalling

- ◦Moving Block Signalling

- ◦Automatic Train Control Systems

- ◦Automatic Train Protection (ATP) Systems

- ◦Wireless Communication Systems

- •By Application

- ◦Interlocking Systems

- ◦Train Control

- ◦Track Circuit

- ◦Level Crossing Protection

- ◦Communication-Based Train Control (CBTC)

- •By End User

- ◦Freight Rail Operators

- ◦Passenger Rail Operators

- ◦Urban Rail Transit Authorities

- ◦Rail Infrastructure Companies

- •By Deployment Model

- ◦On-Premise

- ◦Cloud-Based

- ◦Hybrid

Growth Dynamics

- •Rising investments in railway infrastructure modernization worldwide drive demand for advanced mainline rail signalling systems. Governments and private entities are allocating significant funds to upgrade aging signalling infrastructure, enhancing safety and operational efficiency.

- •The adoption of digital and wireless communication technologies is enabling more flexible and real-time train control, leading to increased network capacity and reduced delays. These innovations are highly favored in high-density rail corridors.

- •Stringent safety regulations and standards globally mandate the implementation of reliable signalling systems, fostering consistent market growth. Compliance requirements push operators to invest in state-of-the-art signalling solutions.

- •Expansion of high-speed rail networks in Asia-Pacific and Europe creates substantial opportunities for the deployment of sophisticated signalling infrastructures capable of supporting faster train operations.

- •Integration of AI, IoT, and big data analytics in signalling systems enhances predictive maintenance and operational decision-making, driving market adoption among technologically advanced rail operators.

Market Trends

- •The market is witnessing a shift towards communication-based train control (CBTC) and moving block signalling systems which provide higher flexibility and improved traffic management compared to traditional fixed block systems.

- •Increasing emphasis on interoperability and standardization of signalling protocols enables seamless integration across diverse rail networks, promoting system scalability and cost savings.

- •Railway operators are leveraging cloud computing platforms for signalling data management and remote monitoring, enhancing operational efficiency and reducing infrastructure costs.

- •Sustainability initiatives are encouraging the adoption of energy-efficient signalling solutions that minimize power consumption and environmental impact across rail operations.

- •Collaborations between signalling equipment manufacturers and technology firms are accelerating innovation cycles and the deployment of next-generation signalling systems globally.

Market Opportunities

- •Emerging economies in Asia-Pacific and Latin America with expanding rail networks present untapped markets for advanced mainline signalling solutions, offering significant growth potential.

- •Development of 5G and dedicated railway communication networks opens avenues for implementing ultra-reliable wireless signalling systems with enhanced safety and speed capabilities.

- •Retrofitting and upgrading legacy signalling infrastructures in mature markets provide recurring revenue streams through system modernization and maintenance contracts.

- •Integration of AI-driven predictive maintenance tools within signalling systems offers opportunities to reduce operational downtime and maintenance costs for rail operators.

- •Public-private partnerships and government incentives aimed at sustainable and smart transportation support investments in innovative rail signalling technologies.

Market Challenges

- •High initial capital expenditure for installing state-of-the-art signalling systems can delay adoption in cost-sensitive markets, particularly among smaller rail operators.

- •Complex integration requirements with existing legacy infrastructure pose technical challenges and can increase project timelines and costs.

- •Cybersecurity risks associated with digital and wireless signalling systems necessitate robust protective measures, increasing system complexity and cost.

- •Regulatory discrepancies across regions complicate the standardization and certification of signalling technologies, limiting cross-border deployments.

- •Skilled workforce shortages in railway signalling technology development and maintenance hamper the timely implementation and servicing of advanced systems.

Regulatory Framework

- •Between 2019 and 2024, the International Union of Railways (UIC) updated global signalling safety standards, emphasizing fail-safe designs and interoperability requirements, affecting system development and certification.

- •The European Railway Agency introduced enhanced technical specifications for interoperability (TSI) in 2022, mandating adoption of communication-based train control systems for new high-speed lines across the EU.

- •In 2021, the U.S. Federal Railroad Administration implemented stricter Positive Train Control (PTC) regulations, accelerating deployment of automatic train protection systems on mainline railroads.

- •Asia-Pacific countries have introduced national railway safety frameworks between 2020 and 2023, focusing on digital signalling adoption and cybersecurity protocols to align with international best practices.

- •Government incentives and funding programs for green and smart transportation infrastructure have been rolled out globally since 2019, supporting investments in advanced rail signalling technologies.

Market Intelligence

- •15th January 2025, Siemens AG launched its next-generation wireless communication-based signalling platform designed to integrate AI for predictive maintenance and real-time network optimization. The new system targets high-speed rail networks and aims to enhance operational safety while reducing maintenance costs. Siemens is positioning this solution to meet increasing demand for digital transformation in railway operations globally. This launch marks a significant step towards fully automated train control and increased network capacity. Source: Siemens Official Press Release

- •2nd March 2025, Alstom SA introduced an innovative interlocking system incorporating blockchain technology to enhance cybersecurity and data integrity in train control. This system offers scalable deployment options for urban and mainline rail networks and supports remote monitoring capabilities. The product is expected to set new standards for secure signalling infrastructure amid rising cyber threats. Alstom plans global rollouts starting in Europe and North America by late 2025. Source: Alstom Corporate Announcement

- •20th May 2025, Hitachi Rail Ltd. announced a strategic partnership with a leading telecommunications provider to develop 5G-enabled moving block signalling solutions. This collaboration focuses on enhancing train control precision and reducing latency in communication links, catering to densely populated rail corridors in Asia-Pacific. The initiative aligns with government smart city projects and aims to facilitate safer, more efficient rail operations. Source: Hitachi Press Release

- •10th July 2025, Thales Group completed the acquisition of a regional signalling technology startup specializing in AI-driven traffic management systems. This acquisition strengthens Thales’ portfolio in intelligent rail signalling and expands its footprint in emerging markets. The deal is expected to accelerate innovation and deployment of smart signalling solutions, leveraging AI and IoT integration for predictive analytics. Source: Thales Corporate News

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.7 Billion |

| Forecast Year Market Size | USD 21.4 Billion |

| CAGR | 9.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.8% |

| Scope of Report | Market is segmented by Type (Fixed Block Signalling, Moving Block Signalling, Automatic Train Control Systems, Automatic Train Protection (ATP) Systems, Wireless Communication Systems), Application (Interlocking Systems, Train Control, Track Circuit, Level Crossing Protection, Communication-Based Train Control (CBTC)), End User (Freight Rail Operators, Passenger Rail Operators, Urban Rail Transit Authorities, Rail Infrastructure Companies), Deployment Model (On-Premise, Cloud-Based, Hybrid) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Siemens AG (Germany), Alstom SA (France), Hitachi Rail Ltd. (Japan), Thales Group (France), Bombardier Inc. (Canada), Mitsubishi Electric Corporation (Japan), CAF (Construcciones y Auxiliar de Ferrocarriles) (Spain), Ansaldo STS (Italy), GE Transportation (United States), Wabtec Corporation (United States), Huawei Technologies Co., Ltd. (China), Hyundai Rotem Company (South Korea), Kapsch TrafficCom AG (Austria), Toshiba Corporation (Japan), Indra Sistemas S.A. (Spain), Alfa Laval (Sweden), Siemens Mobility GmbH (Germany), General Electric Company (United States), Bombardier Transportation GmbH (Germany), Thales Rail Signalling Solutions (United Kingdom), CAF Signalling Solutions (Spain), Nokia Corporation (Finland), Ericsson AB (Sweden), Yokogawa Electric Corporation (Japan), Digital Railway Technologies (United Kingdom) |

Global Mainline Rail Signalling Systems Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.