Global Regenerative Drugs Market Size, Growth & Revenue 2024-2034

Global Regenerative Drugs Market is segmented by Regenerative Drug Type (Cell-based Therapy, Gene Therapy, Tissue Engineering, Biologics, Small Molecules), Medical Application (Orthopedic Disorders, Cardiovascular Diseases, Neurological Disorders, Wound Healing, Others), End User (Hospitals, Specialty Clinics, Research Institutions, Ambulatory Care Centers), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Regenerative Drugs market is a dynamic and rapidly evolving sector focused on innovative therapies designed to regenerate, repair, or replace damaged tissues and organs. This market covers a range of products including cell-based therapies, gene therapies, tissue engineering, biologics, and small molecules that contribute to enhanced healing and functional restoration. It addresses critical medical needs such as orthopedic disorders, cardiovascular diseases, neurological disorders, and wound healing, offering transformative treatment options beyond conventional pharmaceuticals. The industry integrates cutting-edge biotechnological advances with clinical applications, influencing healthcare globally. Key market drivers include the escalating prevalence of chronic diseases, technological breakthroughs in stem cell research, and increasing healthcare expenditure. The market also involves diverse stakeholders from pharmaceutical companies to research institutions working in tandem to innovate and commercialize regenerative solutions, reflecting a broad scope that encompasses R&D, regulatory frameworks, manufacturing, and distribution. These therapies promise to revolutionize patient care by focusing on long-term recovery and quality of life enhancement.

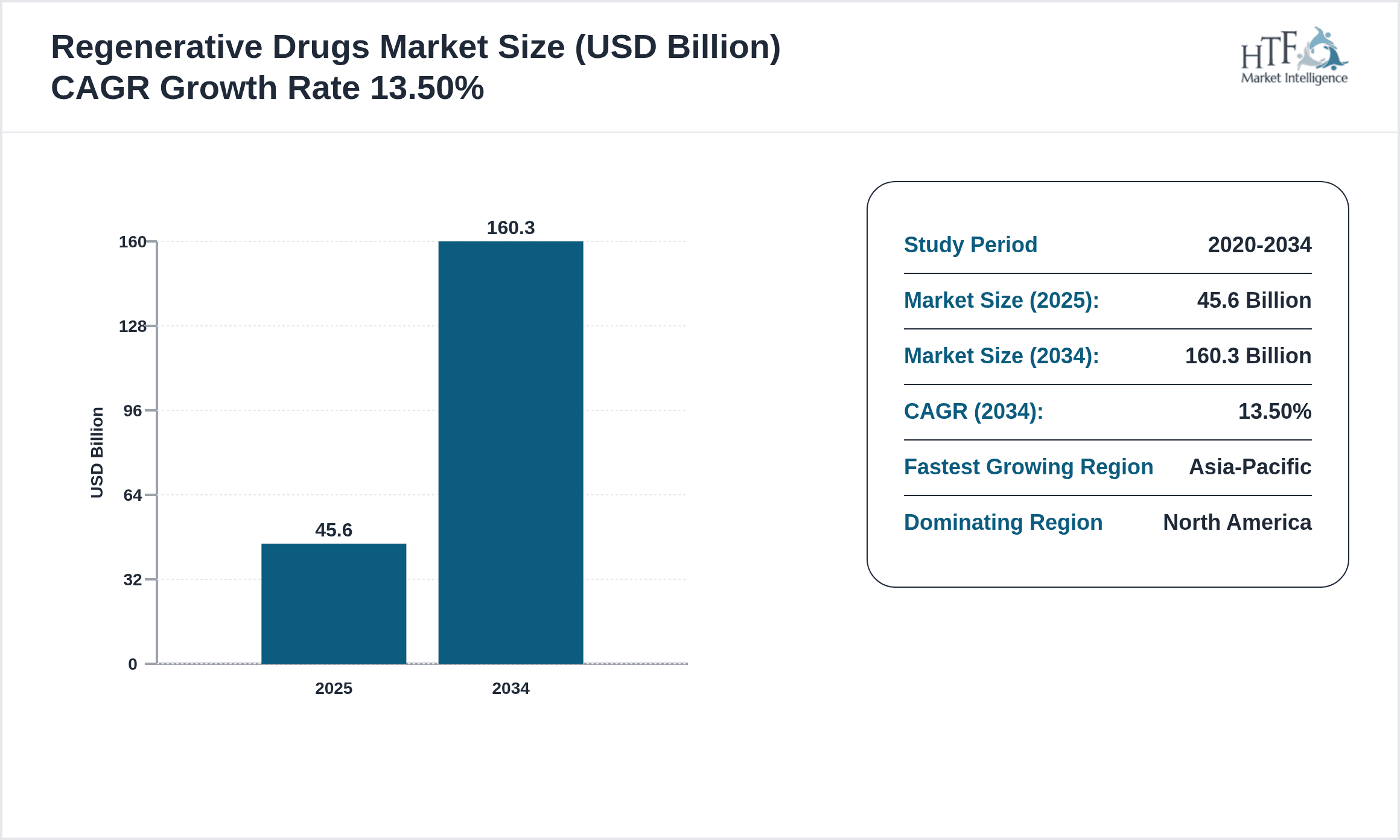

- •The market is projected to grow from USD 45.6 billion in 2024 to USD 160.3 billion by 2034, registering a CAGR of 13.5%. North America currently dominates due to advanced healthcare infrastructure, strong R&D capabilities, and supportive regulatory environments, while Asia-Pacific is the fastest-growing region driven by increasing healthcare investments and rising disease burden. Key segments like cell-based therapies maintain leading market positions, with gene therapies exhibiting the fastest growth trajectory. Market penetration is expanding across applications such as orthopedic and cardiovascular treatments, reflecting increased adoption and clinical validation. Innovations, strategic partnerships, and regulatory approvals are continuously shaping the competitive landscape, presenting lucrative opportunities and driving sustained market momentum.

- •The Global Regenerative Drugs market holds strategic importance across healthcare sectors by providing novel therapeutic options that address unmet medical needs. Its value proposition lies in the potential to reduce long-term treatment costs, improve patient outcomes, and enhance quality of life for individuals with chronic and degenerative conditions. For pharmaceutical companies and biotech innovators, this market offers substantial growth avenues through product innovation and geographic expansion. Healthcare providers benefit from improved treatment efficacy, while patients gain access to personalized medicine approaches. The industry's evolution is supported by increasing government initiatives, rising private investments, and growing awareness about regenerative medicine’s benefits, underscoring its transformative impact on global healthcare delivery.

Competitive Landscape

The competitive environment in the Global Regenerative Drugs market is characterized by intense rivalry among established pharmaceutical giants, biotech firms, and emerging startups focused on innovation. Market leaders leverage substantial R&D investments to develop proprietary technologies and secure intellectual property rights, establishing strong product pipelines with differentiated therapeutic platforms. Strategic collaborations, licensing agreements, and partnerships are common to accelerate product development and expand market reach. Competitors adopt varied strategies including mergers and acquisitions to consolidate market position and enhance capabilities. Innovation-driven differentiation, coupled with regulatory compliance and robust clinical trial data, serves as a critical competitive advantage. Pricing strategies and reimbursement policies also influence market dynamics, with companies striving to balance cost-effectiveness and profitability. Regional competition varies, with North America and Europe showcasing mature markets with advanced infrastructure, while Asia-Pacific presents emerging opportunities fueled by increasing healthcare expenditure and policy support. Future trends suggest a continued focus on personalized regenerative therapies, digital integration, and sustainable production methods shaping competitive strategies.

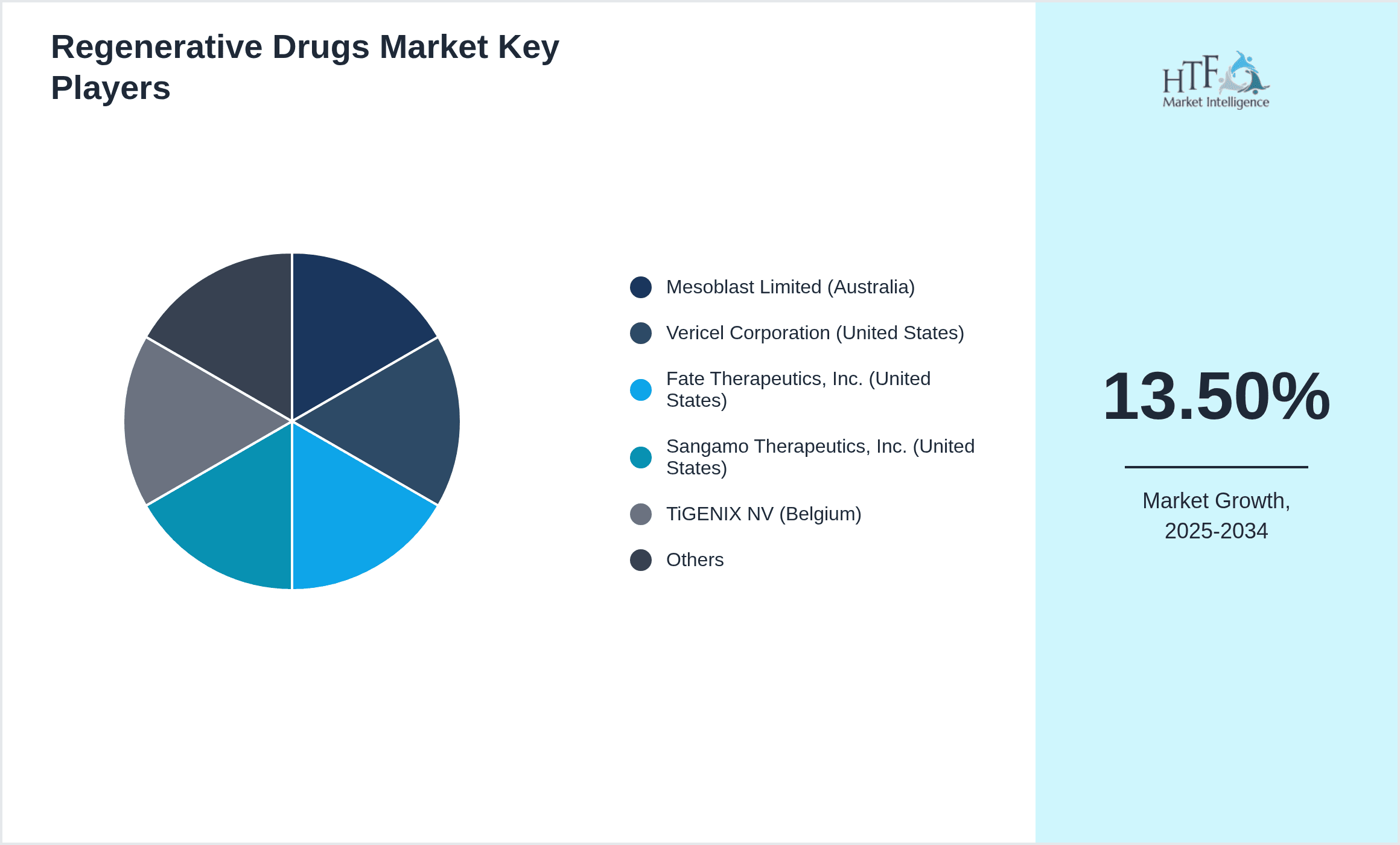

Prominent Players in Regenerative Drugs Market

- •Mesoblast Limited (Australia)

- •Vericel Corporation (United States)

- •Fate Therapeutics, Inc. (United States)

- •Sangamo Therapeutics, Inc. (United States)

- •TiGENIX NV (Belgium)

- •Organogenesis Inc. (United States)

- •Pluristem Therapeutics Inc. (Israel)

- •Athersys, Inc. (United States)

- •BlueRock Therapeutics (Canada)

- •Regen Lab SA (Switzerland)

- •Cytori Therapeutics, Inc. (United States)

- •Celyad Oncology SA (Belgium)

- •Cellular Biomedicine Group, Inc. (United States)

- •Novartis AG (Switzerland)

- •Pfizer Inc. (United States)

- •Johnson & Johnson (United States)

- •Astellas Pharma Inc. (Japan)

- •Bristol-Myers Squibb Company (United States)

- •Regeneron Pharmaceuticals, Inc. (United States)

- •Gilead Sciences, Inc. (United States)

- •Amgen Inc. (United States)

- •Sanofi S.A. (France)

- •Biogen Inc. (United States)

- •Takeda Pharmaceutical Company Limited (Japan)

- •Novavax, Inc. (United States)

Market Breakdown

- •By Regenerative Drug Type

- ◦Cell-based Therapy

- ◦Gene Therapy

- ◦Tissue Engineering

- ◦Biologics

- ◦Small Molecules

- •By Medical Application

- ◦Orthopedic Disorders

- ◦Cardiovascular Diseases

- ◦Neurological Disorders

- ◦Wound Healing

- ◦Others

- •By End User

- ◦Hospitals

- ◦Specialty Clinics

- ◦Research Institutions

- ◦Ambulatory Care Centers

- •By Distribution Channel

- ◦Hospital Pharmacies

- ◦Retail Pharmacies

- ◦Online Pharmacies

Growth Dynamics

The Global Regenerative Drugs market is propelled by rising prevalence of chronic and degenerative diseases such as osteoarthritis, cardiovascular ailments, and neurodegenerative disorders, which create an urgent demand for innovative therapies. Breakthroughs in stem cell research and gene editing technologies have unlocked new therapeutic avenues, enabling targeted and personalized treatments that enhance efficacy and safety. Increasing healthcare expenditure worldwide, coupled with supportive government initiatives and funding in regenerative medicine research, further underpin market expansion. Additionally, growing awareness among clinicians and patients about the benefits of regenerative therapies is accelerating adoption. Collaborations between biotech firms and pharmaceutical companies foster rapid product development and commercialization. The integration of advanced manufacturing technologies and improvements in regulatory frameworks are reducing time-to-market, thereby sustaining high growth momentum across global regions.

Evolving Market Trends

The regenerative drugs industry is witnessing a paradigm shift towards personalized medicine, driven by advancements in genomic profiling and biomarker identification that tailor treatments to individual patient profiles. There is growing integration of artificial intelligence and machine learning in drug discovery and clinical trial design, enhancing precision and reducing development costs. The emergence of allogeneic off-the-shelf cell therapies is transforming treatment accessibility and scalability compared to autologous approaches. Sustainability and eco-friendly manufacturing practices are gaining traction, aligning with global environmental goals. Moreover, strategic partnerships between startups and established pharmaceutical companies are increasing to leverage complementary expertise. Digital health technologies are being incorporated to monitor patient outcomes post-therapy, improving real-world efficacy data. These trends collectively shape a more innovative, patient-centric, and efficient regenerative drugs ecosystem.

Market Constraints

Despite promising growth, the regenerative drugs market faces significant challenges such as complex regulatory pathways and high costs associated with R&D, manufacturing, and clinical trials. Stringent approval requirements and long timelines delay market entry and increase financial burden on companies. Limited scalability and reproducibility of cell-based and gene therapies pose manufacturing hurdles. Furthermore, reimbursement uncertainties and lack of standardized coding impact market penetration and commercialization potential. Ethical concerns and public skepticism regarding genetic manipulation and stem cell use also limit wider acceptance. Additionally, the availability of skilled workforce and infrastructure remains a bottleneck in emerging regions. These factors collectively restrain rapid market expansion and necessitate strategic efforts by stakeholders to overcome operational and regulatory barriers.

Emerging Opportunities

Growing unmet medical needs in developing countries present vast opportunities for market players to expand geographic reach and introduce affordable regenerative therapies. Technological advancements such as CRISPR gene editing, 3D bioprinting, and nanotechnology offer new frontiers for product innovation. Increasing investments in precision medicine and combination therapies further open pathways for diversified treatment portfolios. Partnerships with healthcare providers to facilitate real-world evidence generation and improve reimbursement frameworks enhance commercial viability. Additionally, expanding applications into rare diseases and aesthetic medicine, combined with rising patient awareness, drive demand. Regulatory agencies are progressively adapting frameworks to accommodate regenerative products, creating a conducive environment for faster approvals. These factors collectively present lucrative avenues for companies to innovate, scale, and capture new customer segments globally.

Market Challenges

The regenerative drugs market confronts major challenges including complex supply chains requiring cold storage and specialized logistics, which increase operational costs and risk of product degradation. Variability in patient responses and long-term safety concerns necessitate extensive clinical validation. Intellectual property disputes and high competition for key patents pose legal challenges. Market fragmentation due to diverse regulatory requirements across countries complicates global commercialization strategies. Limited awareness and skepticism among healthcare professionals and patients in certain regions slow adoption rates. Furthermore, reimbursement frameworks remain inconsistent and often inadequate, affecting therapy affordability. These challenges require coordinated efforts from industry stakeholders to streamline operations, enhance education, and engage with regulators and payers to ensure sustainable market growth.

Regulatory Framework

Between 2020 and 2024, regulatory agencies worldwide have implemented comprehensive guidelines to address the unique challenges of regenerative drugs, focusing on safety, efficacy, and quality control. The U.S. FDA introduced expedited pathways such as the Regenerative Medicine Advanced Therapy (RMAT) designation to accelerate approvals. The European Medicines Agency (EMA) updated its Advanced Therapy Medicinal Products (ATMP) framework to harmonize evaluation processes. Additionally, countries in Asia-Pacific have established specialized regulatory bodies to facilitate clinical trials and product registration. Emphasis on post-marketing surveillance and real-world evidence collection has increased to monitor long-term outcomes. These regulatory developments aim to balance innovation with patient safety, providing clearer pathways for developers while ensuring compliance with ethical and manufacturing standards. Government incentives and funding programs further support research and commercialization in the regenerative drugs sector.

Market Intelligence

- •15th February 2024, Novartis AG announced the launch of its novel gene therapy targeting spinal muscular atrophy, featuring enhanced delivery mechanisms and improved efficacy profiles. This product aims to address significant unmet needs in neuromuscular disorders with a scalable manufacturing process to support global distribution. The initiative underscores Novartis’s commitment to expanding its regenerative medicine portfolio and leveraging advanced gene-editing technologies to enhance patient outcomes worldwide. The therapy has received fast-track designation in multiple regions, positioning it for accelerated market entry and broad adoption among clinicians and patients.

- •10th October 2023, Mesoblast Limited entered a strategic collaboration with a leading pharmaceutical company to co-develop allogeneic cell-based therapies for cardiovascular diseases. This partnership integrates Mesoblast’s proprietary mesenchymal stem cell platform with the partner’s clinical development expertise to expedite product commercialization. The alliance aims to advance late-stage clinical trials and expand access to regenerative treatments in key global markets, reflecting a trend toward collaborative innovation in the regenerative drugs industry.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.6 Billion |

| Forecast Year Market Size | USD 160.3 Billion |

| CAGR | 13.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.7% |

| Scope of Report | Market is segmented by Regenerative Drug Type (Cell-based Therapy, Gene Therapy, Tissue Engineering, Biologics, Small Molecules), Medical Application (Orthopedic Disorders, Cardiovascular Diseases, Neurological Disorders, Wound Healing, Others), End User (Hospitals, Specialty Clinics, Research Institutions, Ambulatory Care Centers), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Mesoblast Limited (Australia), Vericel Corporation (United States), Fate Therapeutics, Inc. (United States), Sangamo Therapeutics, Inc. (United States), TiGENIX NV (Belgium), Organogenesis Inc. (United States), Pluristem Therapeutics Inc. (Israel), Athersys, Inc. (United States), BlueRock Therapeutics (Canada), Regen Lab SA (Switzerland), Cytori Therapeutics, Inc. (United States), Celyad Oncology SA (Belgium), Cellular Biomedicine Group, Inc. (United States), Novartis AG (Switzerland), Pfizer Inc. (United States), Johnson & Johnson (United States), Astellas Pharma Inc. (Japan), Bristol-Myers Squibb Company (United States), Regeneron Pharmaceuticals, Inc. (United States), Gilead Sciences, Inc. (United States), Amgen Inc. (United States), Sanofi S.A. (France), Biogen Inc. (United States), Takeda Pharmaceutical Company Limited (Japan), Novavax, Inc. (United States) |

Global Regenerative Drugs Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.