Global Wood Pellets Fuel Market Size, Growth & Revenue 2024-2034

Global Wood Pellets Fuel Market is segmented by Type (Premium Wood Pellets, Standard Wood Pellets, Low-grade Wood Pellets, Torrefied Pellets, Agricultural Pellets), Application (Residential Heating, Industrial Energy, Power Generation, Commercial Heating, Agricultural Use), End User Sector (Households, Manufacturing Plants, Utility Companies, Agricultural Farms), Distribution Channel (Direct Sales, Wholesale Distributors, Online Retail, Energy Service Providers), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Wood Pellets Fuel market is a dynamic sector focused on the production and utilization of biomass-derived wood pellets that serve as a renewable and sustainable energy source across diverse applications. This market includes multiple pellet types such as premium, standard, low-grade, torrefied, and agricultural pellets. These products find extensive use in residential heating, industrial energy generation, power production, commercial heating, and agricultural operations. The industry scope spans raw material sourcing from wood residues, pellet production technologies, supply chain logistics, and end-use demand across global regions. Increasing environmental concerns, governmental policies promoting carbon neutrality, and the transition from fossil fuels to bioenergy significantly influence market growth. Europe currently dominates the market, supported by stringent emission regulations and well-established supply chains, while Asia-Pacific presents the fastest growth trajectory fueled by industrialization and renewable energy adoption. This report delivers a comprehensive analysis of market dynamics, competitive landscape, regulatory environment, and future prospects, offering valuable insights for stakeholders and investors.

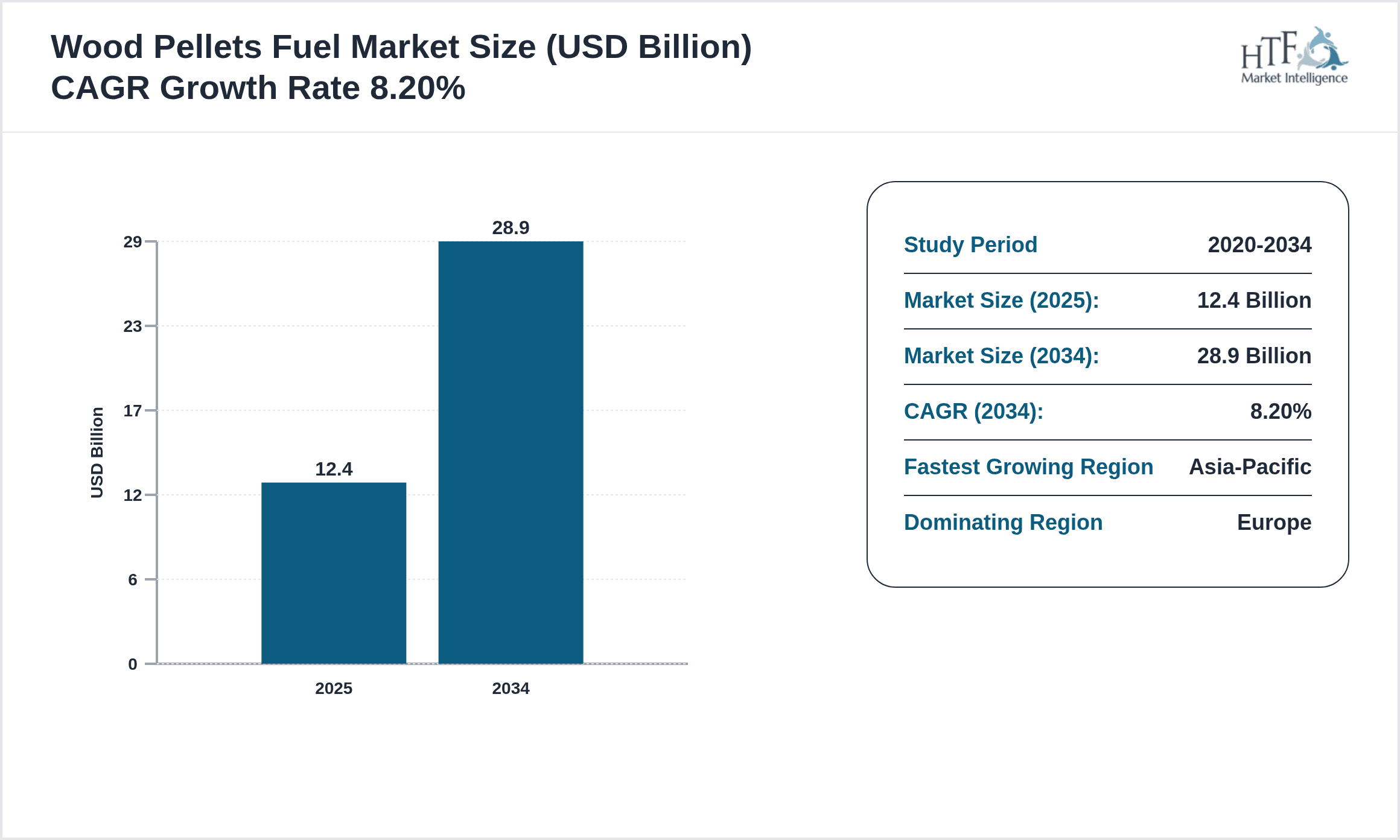

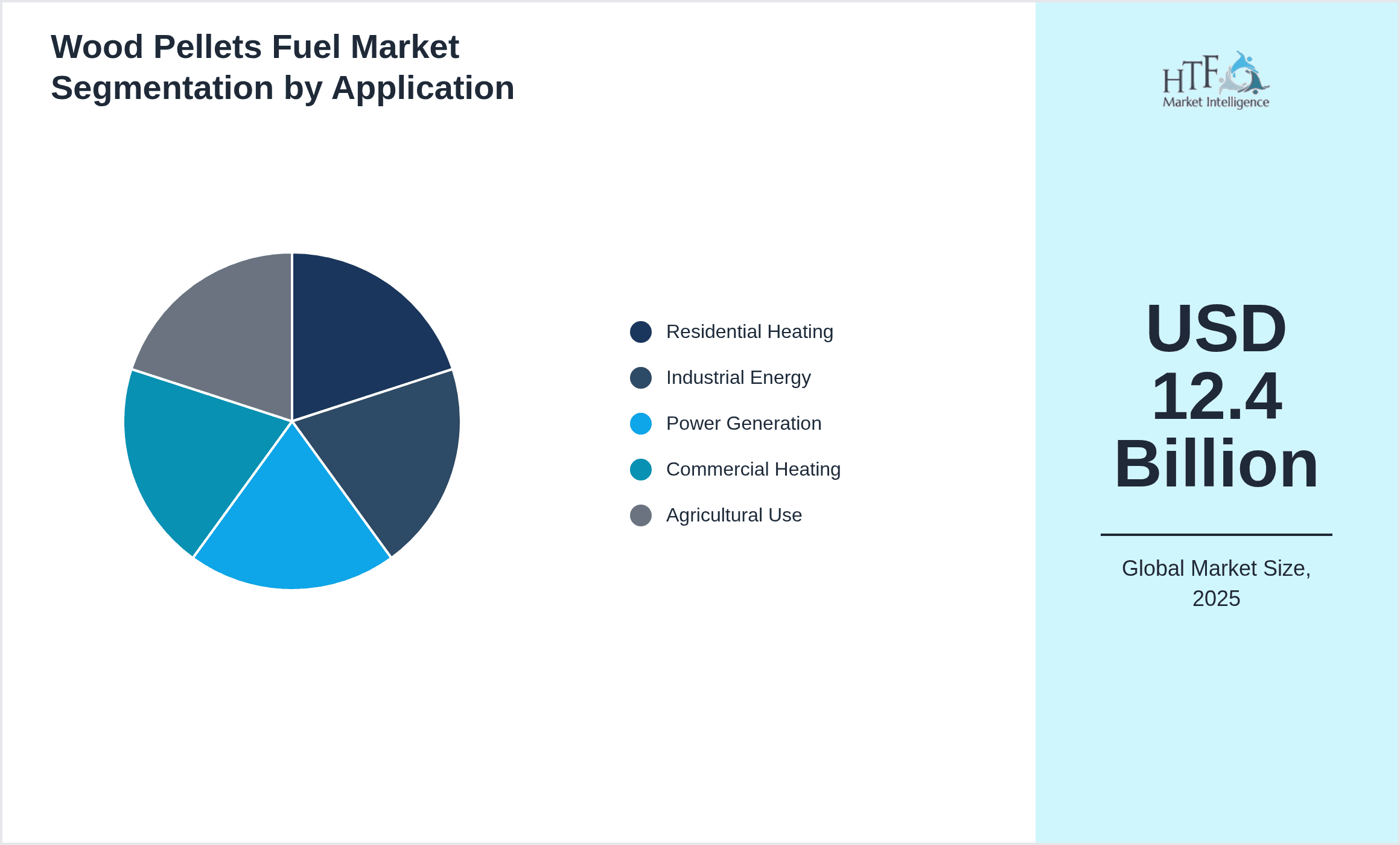

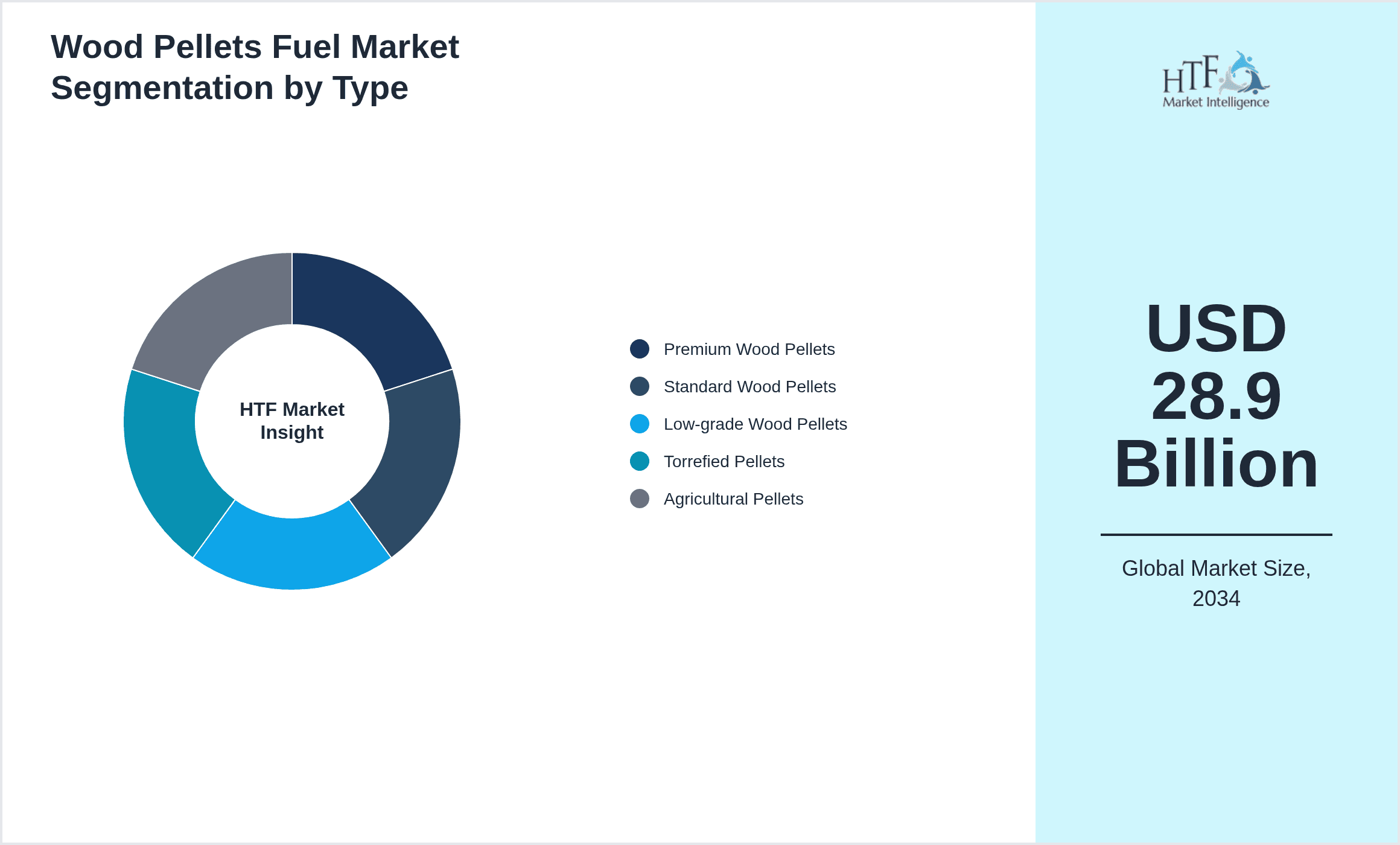

- •Key market highlights include a projected compound annual growth rate (CAGR) of 8.2% from 2024 to 2034, with the market size expected to more than double from USD 12.4 Billion in 2024 to USD 28.9 Billion by 2034. Premium wood pellets emerge as the leading product type due to superior energy content and growing demand in residential and commercial heating sectors. Torrefied pellets are the fastest-growing segment, benefiting from enhanced combustion properties and increasing industrial adoption. Europe maintains its dominance driven by mature biomass policies and infrastructure, while Asia-Pacific leads in growth rate propelled by expanding power generation capacity and energy diversification efforts. The residential heating application commands the largest share, reflecting consumer preference for sustainable heating solutions, followed by industrial energy applications which are rapidly adopting pellet fuel to reduce carbon emissions.

- •The wood pellets fuel market presents significant strategic value to energy producers, equipment manufacturers, distributors, and policy makers aiming to meet renewable energy targets and reduce greenhouse gas emissions. The increasing focus on sustainability, coupled with technological advancements in pellet production and combustion systems, creates new avenues for innovation and market expansion. Stakeholders benefit from understanding regional market nuances, evolving regulatory landscapes, and emerging consumer trends. This market analysis equips businesses with actionable insights to optimize product portfolios, enhance supply chain resilience, and capitalize on growth opportunities in both established and emerging markets worldwide.

Competitive Landscape

The global wood pellets fuel market exhibits a highly competitive environment characterized by numerous players ranging from large integrated biomass companies to regional pellet producers and distributors. Market competition revolves around product quality differentiation, cost-efficiency in production, supply chain optimization, and technological innovation in pellet manufacturing processes. Leading companies focus on expanding their geographic presence, developing premium and torrefied pellet varieties, and forming strategic partnerships to secure raw material supply and enhance market penetration. Competitive strategies also include investments in sustainable forestry, compliance with evolving environmental standards, and enhancing logistics to reduce delivery costs and improve customer service. The market faces moderate entry barriers due to capital intensity and regulatory compliance requirements, shaping a competitive landscape that favors experienced players with established distribution networks and innovation capabilities. Regional competition varies, with Europe dominated by established biomass energy firms, while Asia-Pacific and North America witness rising participation from emerging companies driven by increasing renewable energy mandates.

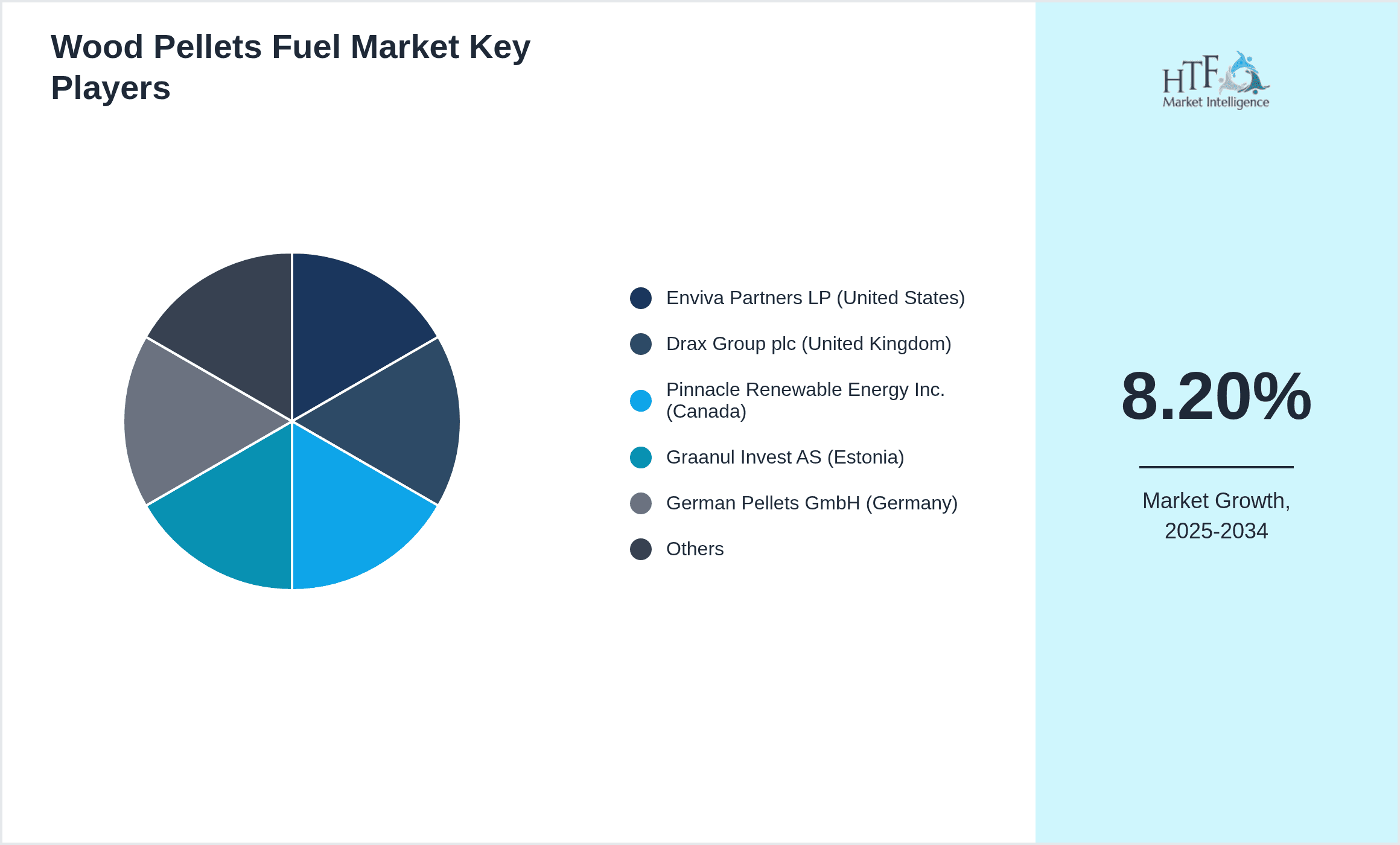

Prominent Players in Wood Pellets Fuel Market

- •Enviva Partners LP (United States)

- •Drax Group plc (United Kingdom)

- •Pinnacle Renewable Energy Inc. (Canada)

- •Graanul Invest AS (Estonia)

- •German Pellets GmbH (Germany)

- •Pacific BioEnergy Corporation (Canada)

- •Zhejiang Longyuan Wood Industry Co., Ltd. (China)

- •Lignetics Inc. (United States)

- •Södra Skogsägarna (Sweden)

- •Burke Energy (United States)

- •Stora Enso Oyj (Finland)

- •Westervelt Renewable Energy (United States)

- •Fram Renewable Fuels (United States)

- •Vapo Oy (Finland)

- •Rentech Inc. (United States)

- •Lignetics Europe GmbH (Germany)

- •Shandong Longquan Wood Industry Co., Ltd. (China)

- •Balcas Timber Ltd. (United Kingdom)

- •Hokuetsu Corporation (Japan)

- •Metsä Group (Finland)

- •Bioenergy DevCo (United States)

- •Scandinavian Biopower AB (Sweden)

- •LJ Pellet (Norway)

- •Terra Energy Group (Canada)

- •Green Circle Bio Energy (United States)

Market Breakdown

- •By Type

- ◦Premium Wood Pellets

- ◦Standard Wood Pellets

- ◦Low-grade Wood Pellets

- ◦Torrefied Pellets

- ◦Agricultural Pellets

- •By Application

- ◦Residential Heating

- ◦Industrial Energy

- ◦Power Generation

- ◦Commercial Heating

- ◦Agricultural Use

- •By End User Sector

- ◦Households

- ◦Manufacturing Plants

- ◦Utility Companies

- ◦Agricultural Farms

- •By Distribution Channel

- ◦Direct Sales

- ◦Wholesale Distributors

- ◦Online Retail

- ◦Energy Service Providers

Growth Dynamics

- •The global wood pellets fuel market growth is primarily driven by increasing environmental regulations aimed at reducing carbon emissions and promoting renewable energy sources. Governments worldwide have implemented policies and subsidies encouraging biomass fuel adoption, which has significantly boosted demand, especially in developed regions such as Europe and North America. Additionally, technological advancements in pellet production, including improved quality and energy efficiency, have enhanced market acceptance. The rising cost and volatility of fossil fuels further incentivize industries and households to shift towards sustainable alternatives like wood pellets. Moreover, expanding industrialization and urbanization in emerging economies fuel the demand for reliable and cleaner energy, positioning wood pellets as a feasible solution. These factors collectively stimulate market expansion, supported by growing consumer awareness about climate change and energy security.

- •Current trends highlight a rising preference for premium and torrefied wood pellets due to their superior combustion properties and lower emissions, facilitating their use in high-efficiency boilers and power plants. The integration of wood pellets in co-firing with coal in thermal power plants is gaining traction, promoting a gradual transition towards cleaner energy. Additionally, supply chain enhancements, including better pellet storage and transportation technologies, are improving market logistics. The increasing penetration of smart heating systems in residential and commercial settings supports the adoption of wood pellet heating solutions. Furthermore, industry players are increasingly investing in sustainable forestry and circular economy practices, aligning with global sustainability goals. These trends underscore a shift towards higher quality products and innovative applications, enabling the wood pellets fuel market to evolve dynamically.

- •Market restraints include the high initial capital investment required for pellet production facilities and heating system conversions, which can deter small-scale producers and consumers. Limited availability and seasonal variability of raw materials such as wood residues and sawdust pose significant supply challenges, potentially leading to price volatility. The competition from alternative renewable energy sources like solar and wind, which benefit from decreasing costs and widespread adoption, restricts the wood pellets market growth. Additionally, logistical complexities and transportation costs, especially for export-oriented producers, impact profitability and market expansion. Environmental concerns related to deforestation and land use change also create regulatory and social challenges. These factors collectively restrain market growth and necessitate strategic planning by industry stakeholders to mitigate risks.

- •Significant opportunities arise from expanding industrial energy applications in developing economies where energy demand is escalating rapidly. The development of next-generation torrefied pellets offers enhanced energy density and hydrophobic properties, opening new markets in power generation and industrial processes. Integration of wood pellet fuel in combined heat and power (CHP) systems provides efficiency gains, presenting attractive investment avenues. Governments’ increasing commitment to carbon neutrality targets creates a favorable policy environment, incentivizing adoption across sectors. The rising trend of green building initiatives supports the incorporation of pellet-based heating solutions in construction and infrastructure projects. Moreover, digitalization of distribution channels and supply chain management through IoT and blockchain technology improves market transparency and efficiency, enabling better customer engagement and operational optimization.

- •Challenges confronting the wood pellets fuel market include fluctuating raw material costs influenced by forestry management practices and competing uses for wood biomass such as paper and furniture manufacturing. Supply chain disruptions due to geopolitical tensions and transportation bottlenecks can lead to inconsistent pellet availability. The market also faces technological challenges related to pellet combustion efficiency and emissions control to meet stringent environmental standards. Consumer hesitation regarding the transition from conventional fuels and lack of awareness in certain regions limit market penetration. Additionally, regulatory uncertainties and evolving compliance requirements across different countries create complexity for multinational operators. Addressing these challenges requires coordinated efforts in innovation, policy alignment, and stakeholder education to sustain market growth and competitiveness.

Market Trends

- •The wood pellets fuel market is witnessing an increasing integration of torrefied pellets, which offer advantages such as higher calorific value and water resistance, making them suitable for industrial and power generation applications. This trend reflects a shift towards advanced biomass fuels that improve combustion efficiency and reduce emissions. Leading manufacturers are investing in torrefaction technology to capture emerging market demand and enhance product differentiation. The adoption of automated pellet heating systems in residential and commercial buildings is also gaining momentum, driven by consumer preference for convenience and energy efficiency. Additionally, green certifications and sustainability labeling are becoming more prevalent, influencing purchasing decisions and promoting responsible sourcing practices. These trends collectively drive innovation and elevate the market's environmental credentials.

- •Emerging trends include the expansion of co-firing initiatives where wood pellets are blended with coal in existing power plants to reduce carbon footprints without major infrastructure changes. This approach is gaining regulatory and financial support in several regions, enabling gradual energy transition. The market also sees growing digitization in supply chain management, utilizing blockchain and IoT for traceability and quality assurance. Furthermore, partnerships between pellet producers and energy utilities are strengthening to secure long-term supply contracts. The promotion of circular economy models, where forestry waste and agricultural residues are repurposed into pellets, is enhancing raw material sustainability. These developments illustrate evolving industry practices aimed at efficiency, transparency, and sustainability.

- •Strategic trend shifts include increasing mergers and acquisitions to consolidate the fragmented wood pellets fuel industry, improving economies of scale and market reach. Companies are prioritizing sustainability investments to align with global ESG standards, attracting green financing opportunities. There is also a notable emphasis on product innovation targeting lower emissions and compatibility with advanced combustion technologies. Geographic expansion into emerging markets with growing energy demand forms part of growth strategies. Additionally, collaborations with technology providers to develop smart pellet heating solutions enhance customer experience. These trends underscore a maturing market adapting to regulatory pressures and consumer expectations through innovation and strategic alliances.

- •Digitalization and automation are transforming pellet production and distribution, with manufacturers adopting Industry 4.0 technologies to optimize efficiency and reduce operational costs. Predictive maintenance, real-time quality monitoring, and advanced logistics software enable superior product consistency and supply reliability. Sustainability remains a core focus, with increasing efforts to certify pellets under internationally recognized standards such as ENplus. The rise of e-commerce platforms specifically for renewable energy products facilitates easier access to wood pellets for end-users. Moreover, renewable energy policies continue to evolve, encouraging the integration of biomass fuels within national energy mixes. This convergence of technology and policy fosters a resilient and innovative market environment.

- •Collaborative ecosystems are developing between pellet producers, technology innovators, and energy utilities to co-create advanced solutions and expand market penetration. Strategic partnerships facilitate knowledge sharing, joint R&D, and coordinated market entry, enhancing competitive advantage. Consumer preferences are shifting towards cleaner, carbon-neutral energy sources, driving segmentation and product customization. The value chain is increasingly focusing on transparency and sustainability, responding to stakeholder demands. These multifaceted trends reflect a market moving towards integrated, customer-centric solutions that support global decarbonization goals while enhancing operational performance.

- •Looking forward, the wood pellets fuel market is expected to embrace disruptive innovations such as bio-coal pellets and hybrid biomass solutions that combine multiple feedstocks for optimized performance. The proliferation of smart grid technologies will enable better integration of pellet-based energy into decentralized energy systems. Regulatory frameworks are anticipated to tighten further, incentivizing low-emission technologies and penalizing unsustainable practices. Consumer education campaigns and government programs will likely accelerate adoption in residential and commercial sectors. The evolving landscape presents opportunities for new entrants and existing players to reshape the market through transformative business models and technological breakthroughs.

Market Opportunities

- •The rising industrialization in emerging economies offers substantial growth opportunities for wood pellets fuel by addressing increasing energy demands with renewable alternatives. Expanding power generation capacities seeking to reduce carbon emissions create a favorable environment for pellet adoption. Development of high-quality torrefied pellets enables penetration into more demanding energy markets, including co-firing and CHP applications. Government incentives for biomass energy infrastructure and carbon reduction targets provide financial support for market expansion. Additionally, innovations in pellet storage and transportation improve supply chain efficiency, reducing operational costs and increasing accessibility. These factors collectively open new avenues for market growth and investment.

- •Untapped residential heating markets in regions with cold climates but low biomass adoption represent significant potential for wood pellets fuel expansion. Offering clean, efficient heating solutions aligned with sustainability goals can attract environmentally conscious consumers. Leveraging digital sales platforms and subscription models enhances customer reach and retention. Furthermore, collaborations with local forestry sectors enable sustainable raw material sourcing, fostering circular economy benefits. The integration of wood pellets fuel in green building certification schemes presents opportunities for product differentiation and premium pricing. These market gaps provide strategic entry points for companies seeking to diversify and scale operations globally.

- •Investment opportunities abound in next-generation pellet technologies such as bio-coal and torrefied products which offer enhanced energy densities and lower emissions. Research and development focusing on improving pellet durability, combustion efficiency, and feedstock flexibility can drive competitive advantage. Geographic expansion into Latin America, Middle East & Africa, and parts of Asia-Pacific with growing renewable energy initiatives can unlock new revenue streams. Strategic alliances with energy utilities and technology providers facilitate market penetration and innovation adoption. Additionally, increasing regulatory support for bioenergy creates favorable conditions for capital inflows and project financing, accelerating industry growth.

- •Expanding applications of wood pellets fuel in commercial heating and agricultural sectors represent promising growth areas. Adoption in greenhouse heating, crop drying, and livestock housing offers sustainable energy solutions reducing reliance on fossil fuels. Tailored pellet formulations for specific applications enhance product appeal. Geographic diversification through local partnerships and joint ventures enables market access and cultural adaptation. Enhancing value proposition through service offerings such as pellet delivery and maintenance further strengthens customer loyalty and market share. These opportunities support long-term sustainability and profitability in the wood pellets fuel market.

- •Partnerships and acquisitions present opportunities to consolidate market positions, expand product portfolios, and enter new geographic markets. Aligning with technology innovators accelerates product development and deployment of advanced pellet-based energy systems. Government-backed programs for renewable energy infrastructure development offer financial and regulatory support for expansion projects. Monitoring evolving consumer preferences and regulatory changes enables agile market responses and strategic positioning. These combined opportunities foster a robust growth environment and enhance competitive advantage for stakeholders in the wood pellets fuel sector.

- •Emerging regulatory frameworks focusing on carbon neutrality and sustainability reporting incentivize companies to innovate and adopt cleaner energy sources like wood pellets. Early movers in compliance and certification gain market trust and preferential access to projects and funding. The growing trend towards corporate sustainability commitments by large energy consumers generates demand for verified renewable biomass fuels, creating niche market segments. These regulatory and market dynamics offer strategic opportunities to differentiate and capitalize on expanding demand for sustainable energy solutions globally.

- •The digital transformation of supply chains through blockchain and IoT technologies offers opportunities to enhance transparency, traceability, and operational efficiency in the wood pellets fuel market. This digitalization supports compliance with sustainability standards, reduces fraud, and improves customer confidence. Additionally, leveraging big data analytics enables demand forecasting and inventory optimization, reducing costs and improving service levels. These technological advancements present avenues for competitive differentiation and improved market responsiveness.

Market Challenges

- •Volatility in raw material supply, influenced by forestry management policies, climate change impacts, and competing uses of wood biomass, poses significant challenges to consistent pellet production and pricing stability. Disruptions in supply chains due to geopolitical tensions, transportation inefficiencies, and fluctuating demand complicate operational planning. These factors contribute to market unpredictability and increased costs, affecting profitability and investment decisions.

- •The high capital expenditure required for establishing pellet production plants and upgrading existing heating infrastructure limits market entry, particularly for small and medium-sized enterprises. Long payback periods and uncertain regulatory environments in some regions further deter investment, restricting market expansion and innovation diffusion.

- •Technical challenges related to pellet combustion efficiency, ash content, and emissions control require continuous research and development. Meeting diverse regional environmental standards demands tailored product formulations and testing, increasing operational complexity and costs. Failure to comply risks regulatory penalties and market exclusion.

- •Consumer awareness and acceptance remain uneven globally, with some regions lacking sufficient education on the benefits and operational requirements of wood pellets fuel. Resistance to transitioning from conventional fossil fuels is compounded by limited availability of pellet-compatible heating systems and services, slowing market penetration.

- •Regulatory uncertainties and frequent changes in subsidy schemes and environmental policies create a complex compliance landscape. Navigating these evolving frameworks requires significant resources and expertise, posing barriers especially for smaller market participants and new entrants.

- •Competition from other renewable energy sources such as solar, wind, and biogas, which often benefit from lower costs and higher public visibility, challenges the wood pellets fuel market’s growth prospects. Differentiating product offerings and demonstrating clear sustainability benefits are necessary to maintain market relevance.

- •Infrastructure limitations, including inadequate storage facilities, transportation networks, and distribution channels, particularly in developing regions, hinder reliable supply and scalability. Addressing these bottlenecks is critical for sustained market growth and customer satisfaction.

Regulatory Framework

- •Between 2019 and 2024, the implementation of the European Union’s Renewable Energy Directive (RED II) mandated increased biomass fuel usage targets, including wood pellets, with strict sustainability criteria and certification requirements to ensure responsible sourcing and emissions reductions. Compliance has been critical for market participants operating in or exporting to Europe.

- •In the United States, the 2021 Bipartisan Infrastructure Law included incentives and funding to support bioenergy projects, promoting wood pellet fuel adoption in power generation and heating sectors. The law also emphasized research into advanced pellet technologies and supply chain improvements.

- •China’s National Energy Administration updated biomass energy policies in 2022, prioritizing the development of torrefied and agricultural pellets to diversify energy sources and reduce coal dependency. These regulations promote local pellet production and consumption with environmental standards aligned to national carbon neutrality goals.

- •Canada’s Clean Fuel Standard, revised in 2023, set new greenhouse gas emission reduction targets for renewable fuels, including wood pellets. The policy incentivizes low-carbon pellet production and utilization across residential and industrial applications, shaping market dynamics.

- •Globally, increasing alignment with International Sustainability and Carbon Certification (ISCC) standards between 2019 and 2024 has fostered uniformity in biomass fuel sustainability reporting, enabling cross-border trade and investment in wood pellets fuel markets with reduced regulatory friction.

Market Intelligence

- •15th March 2024, Enviva Partners LP announced the launch of its new ultra-premium wood pellet product designed for high-efficiency residential heating systems, featuring enhanced energy density and reduced ash content. This product aims to meet the increasing consumer demand for cleaner, more efficient biomass solutions in North America and Europe, positioning Enviva as a leader in innovation in the wood pellets fuel market. The company also expanded its production capacity through a recently commissioned plant in the southeastern United States, improving supply chain resilience and responsiveness to market needs. Source: Official Enviva Press Release

- •10th August 2023, Drax Group plc introduced a strategic partnership with a leading European utility company to develop large-scale torrefied pellet production facilities. This initiative targets industrial and power generation sectors seeking to reduce carbon emissions by substituting coal with advanced biomass fuels. The partnership leverages Drax’s expertise in pellet technology and utility’s market access, accelerating the transition to sustainable energy. The collaboration also includes research on improving pellet combustion efficiency and supply logistics. Source: Drax Group Corporate Announcement

- •22nd November 2022, Pinnacle Renewable Energy Inc. completed the acquisition of a regional pellet producer in Southeast Asia, expanding its footprint into the rapidly growing Asia-Pacific market. This acquisition enhances Pinnacle’s access to agricultural residue feedstocks and enables localized production of specialized pellet types suitable for industrial applications. The move aligns with Pinnacle’s growth strategy targeting emerging markets with high renewable energy demand and supports diversification of its product portfolio. Source: Pinnacle Renewable Energy Investor Update

- •5th May 2023, Graanul Invest AS announced the commissioning of a state-of-the-art pellet plant in Estonia with increased automation and energy efficiency. The facility focuses on producing premium and torrefied pellets for export to European and Asian markets. This technological upgrade reduces production costs and environmental footprint, reinforcing Graanul Invest’s position as a sustainable biomass leader. The company also launched a new digital distribution platform to streamline customer orders and logistics. Source: Graanul Invest Corporate Website

Regional Outlook

The Europe currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.4 Billion |

| Forecast Year Market Size | USD 28.9 Billion |

| CAGR | 8.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.9% |

| Scope of Report | Market is segmented by Type (Premium Wood Pellets, Standard Wood Pellets, Low-grade Wood Pellets, Torrefied Pellets, Agricultural Pellets), Application (Residential Heating, Industrial Energy, Power Generation, Commercial Heating, Agricultural Use), End User Sector (Households, Manufacturing Plants, Utility Companies, Agricultural Farms), Distribution Channel (Direct Sales, Wholesale Distributors, Online Retail, Energy Service Providers) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Enviva Partners LP (United States), Drax Group plc (United Kingdom), Pinnacle Renewable Energy Inc. (Canada), Graanul Invest AS (Estonia), German Pellets GmbH (Germany), Pacific BioEnergy Corporation (Canada), Zhejiang Longyuan Wood Industry Co., Ltd. (China), Lignetics Inc. (United States), Södra Skogsägarna (Sweden), Burke Energy (United States), Stora Enso Oyj (Finland), Westervelt Renewable Energy (United States), Fram Renewable Fuels (United States), Vapo Oy (Finland), Rentech Inc. (United States), Lignetics Europe GmbH (Germany), Shandong Longquan Wood Industry Co., Ltd. (China), Balcas Timber Ltd. (United Kingdom), Hokuetsu Corporation (Japan), Metsä Group (Finland), Bioenergy DevCo (United States), Scandinavian Biopower AB (Sweden), LJ Pellet (Norway), Terra Energy Group (Canada), Green Circle Bio Energy (United States) |

Global Wood Pellets Fuel Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.