Europe Cellulose Ether & Its Derivatives Market - Europe Size & Outlook 2025-2034

Europe Cellulose Ether & Its Derivatives Market is segmented by Cellulose Ether Type (Methyl Cellulose, Hydroxypropyl Methylcellulose, Carboxymethyl Cellulose, Ethyl Cellulose, Hydroxyethyl Cellulose), Application Sector (Construction, Pharmaceuticals, Food & Beverages, Personal Care, Paints & Coatings), End-Use Industry (Building & Infrastructure, Healthcare & Pharmaceuticals, Food Processing, Cosmetics & Hygiene, Industrial Coatings), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Sales), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

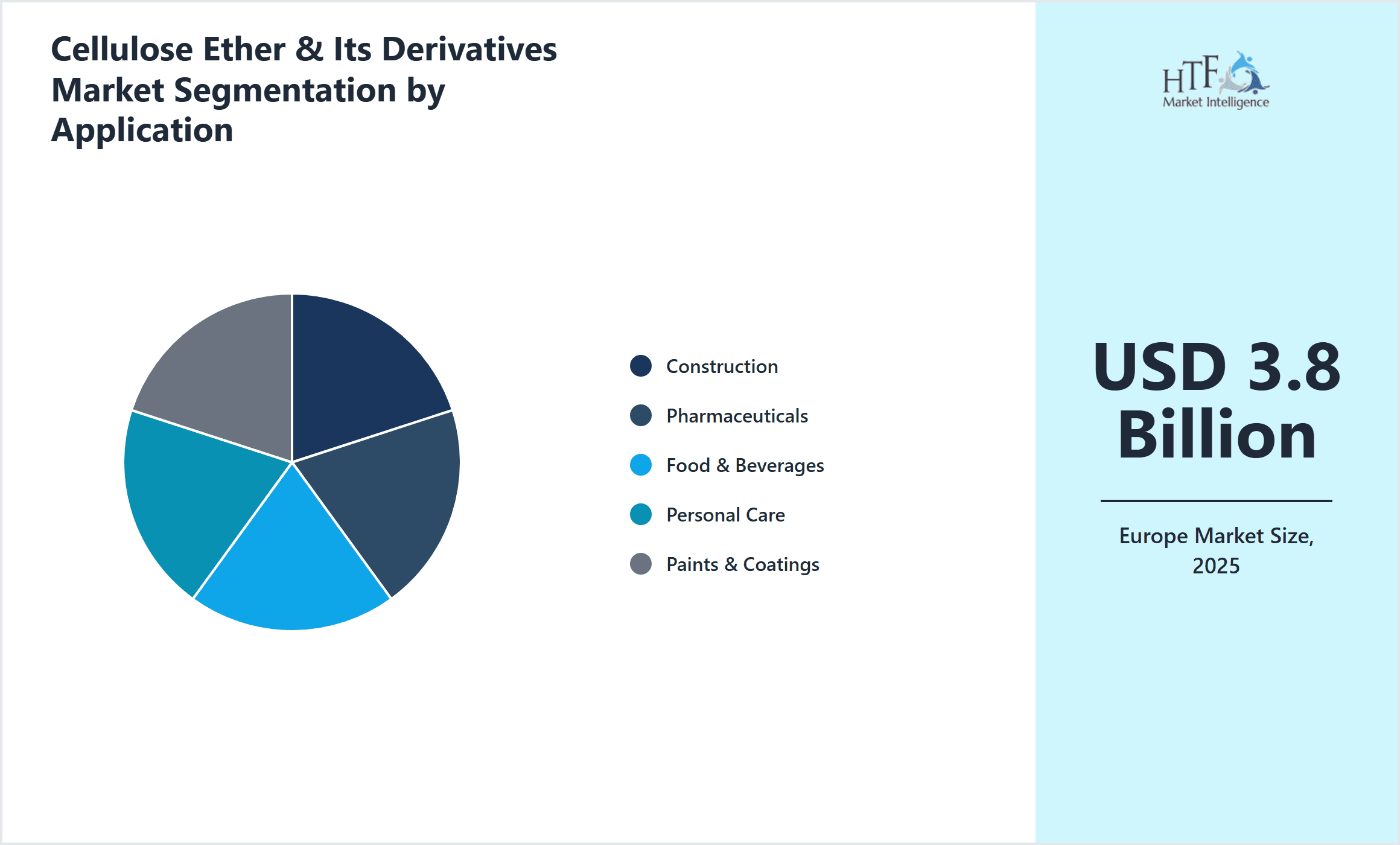

- •The Europe Cellulose Ether & Its Derivatives market comprises a variety of cellulose-based polymers including methyl cellulose, hydroxypropyl methylcellulose, carboxymethyl cellulose, ethyl cellulose, and hydroxyethyl cellulose. These materials are widely applied as functional additives across multiple industries such as construction, pharmaceuticals, food & beverages, personal care, and paints & coatings. Their roles range from thickening and binding to emulsifying and film-forming. The market scope includes production, formulation, and distribution within Europe, with a focus on innovation, sustainability, and regulatory compliance. The demand is driven by end-use industries seeking eco-friendly solutions and enhanced product performance. Development of new derivatives tailored for specific applications continues to expand the market boundaries. Additionally, European environmental regulations encourage adoption of bio-based and biodegradable cellulose ethers, further enlarging the market potential and promoting technological advancements.

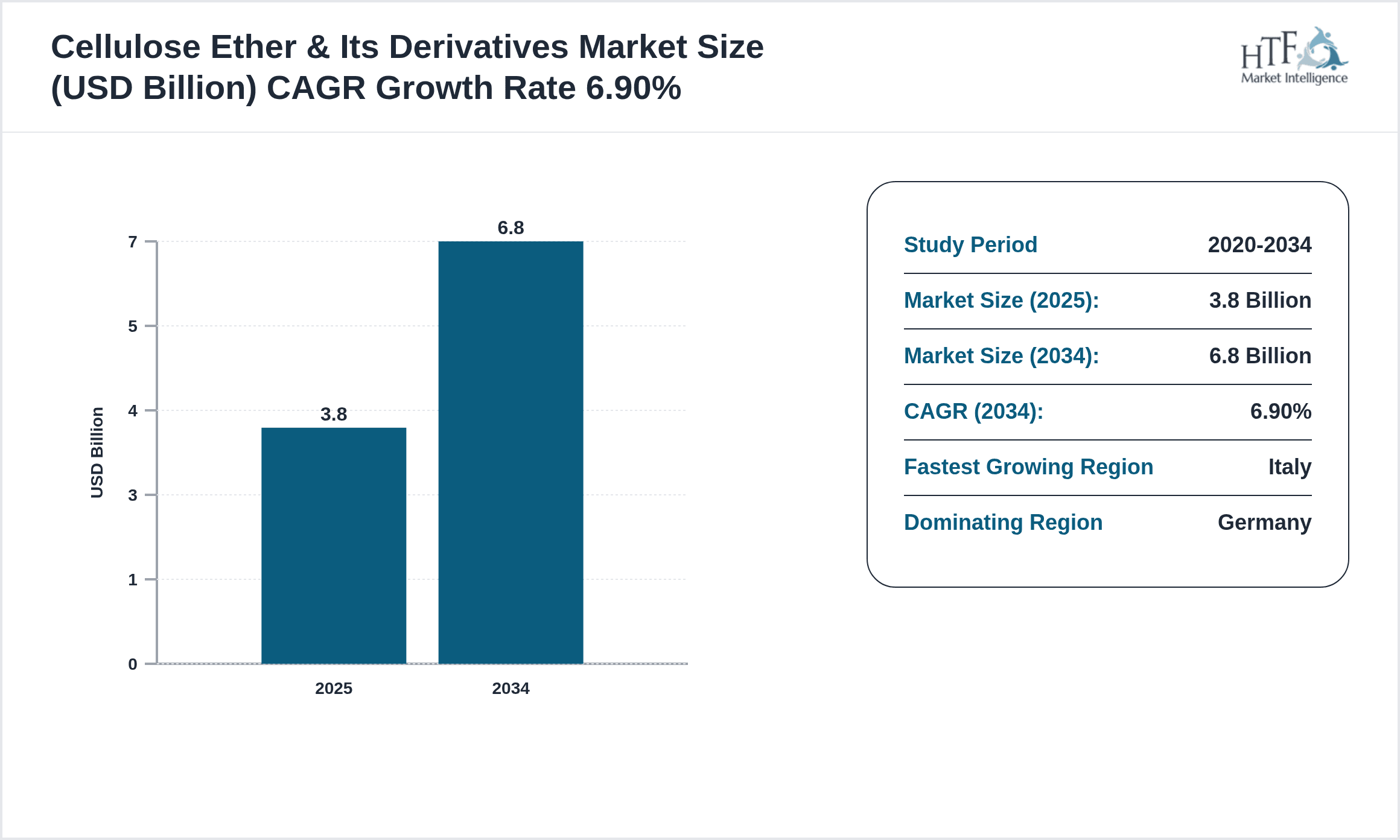

- •Key highlights reveal a base market size of USD 3.8 Billion in 2025, forecasted to reach USD 6.8 Billion by 2034, growing at a CAGR of 6.9%. Germany dominates the market regionally, supported by its strong industrial base and advanced R&D capabilities. Italy is identified as the fastest-growing country driven by increasing investments in pharmaceuticals and construction sectors. Hydroxypropyl methylcellulose leads the product types due to its versatile applications, while hydroxyethyl cellulose is the fastest growing segment, reflecting rising demand in personal care and specialty coatings. The construction sector remains the largest application, with pharmaceuticals and food & beverages rapidly expanding their share. The market is witnessing steady year-over-year growth, supported by technological innovation and sustainability trends.

- •The value proposition of cellulose ethers lies in their multifunctional properties that enhance product quality, stability, and environmental compliance across industries. For construction, they improve workability and durability of materials. In pharmaceuticals, they act as excipients enhancing drug delivery. Food & beverages benefit from texture stabilization and shelf-life extension. Personal care formulations utilize cellulose ethers for rheology control and sensory improvements. Paints and coatings gain improved viscosity and film formation. Stakeholders including manufacturers, distributors, and end-users gain strategic advantage by leveraging the adaptability and eco-friendly nature of cellulose ethers. The market’s growth potential aligns with Europe’s regulatory push for sustainable materials, making cellulose ether derivatives a critical ingredient in the region’s industrial evolution.

Competitive Landscape

The Europe Cellulose Ether & Its Derivatives market is characterized by intense competition among established chemical manufacturers and specialty polymer producers. Market players focus on innovation-driven growth strategies by investing in R&D to develop novel cellulose ether derivatives with enhanced functionality and sustainability credentials. Competition is also fueled by strategic partnerships, collaborations, and capacity expansions to strengthen regional presence and meet growing demand. Companies compete on product differentiation, quality, and regulatory compliance, while also emphasizing cost optimization and supply chain resilience. The market exhibits moderate entry barriers due to technical expertise and regulatory requirements, but ongoing innovation and tailored solutions enable new entrants to gain foothold. Regional competition is influenced by the industrial capabilities of countries like Germany, France, and Italy, with emerging players in Eastern Europe gradually increasing market share. Future competitive trends will likely focus on bio-based product lines, digitalization of manufacturing processes, and circular economy integration.

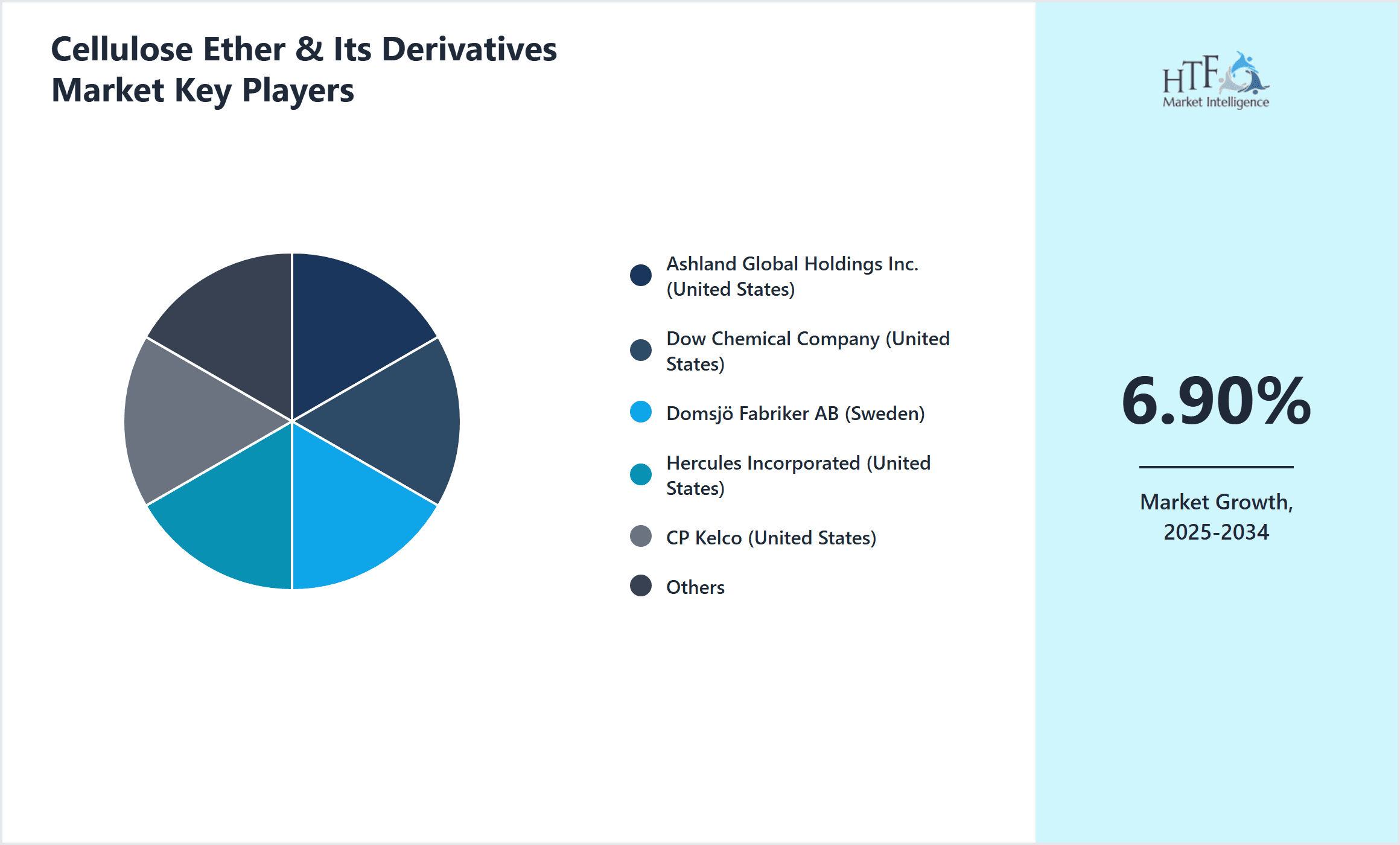

Leading Companies in Cellulose Ether & Its Derivatives Market

- •Ashland Global Holdings Inc. (United States)

- •Dow Chemical Company (United States)

- •Domsjö Fabriker AB (Sweden)

- •Hercules Incorporated (United States)

- •CP Kelco (United States)

- •Shin-Etsu Chemical Co., Ltd. (Japan)

- •Akzo Nobel N.V. (Netherlands)

- •Lotte Fine Chemical (South Korea)

- •CelluComp Ltd. (United Kingdom)

- •J. Rettenmaier & Söhne GmbH + Co KG (Germany)

- •Süd-Chemie AG (Germany)

- •Biesterfeld AG (Germany)

- •Cargill, Incorporated (United States)

- •Akzo Nobel Chemicals GmbH (Germany)

- •Nouryon (Netherlands)

- •Lamberti S.p.A. (Italy)

- •Celanese Corporation (United States)

- •Noviant (France)

- •Sappi Limited (South Africa)

- •FMC Corporation (United States)

- •Sinopec (China)

- •BASF SE (Germany)

- •Evonik Industries AG (Germany)

- •Nippon Paper Industries Co., Ltd. (Japan)

- •Mitsubishi Chemical Corporation (Japan)

Market Breakdown

- •By Cellulose Ether Type

- ◦Methyl Cellulose

- ◦Hydroxypropyl Methylcellulose

- ◦Carboxymethyl Cellulose

- ◦Ethyl Cellulose

- ◦Hydroxyethyl Cellulose

- •By Application Sector

- ◦Construction

- ◦Pharmaceuticals

- ◦Food & Beverages

- ◦Personal Care

- ◦Paints & Coatings

- •By End-Use Industry

- ◦Building & Infrastructure

- ◦Healthcare & Pharmaceuticals

- ◦Food Processing

- ◦Cosmetics & Hygiene

- ◦Industrial Coatings

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Sales

Growth Dynamics

- •The increasing demand for sustainable and eco-friendly construction materials drives growth in the cellulose ether market, particularly methyl cellulose and hydroxypropyl methylcellulose, which improve workability and durability of cement and plaster applications. Regulatory pressure in Europe to reduce carbon footprints incentivizes adoption of these bio-based additives.

- •Pharmaceutical applications are expanding rapidly as cellulose ethers serve as excipients for controlled drug release and improved bioavailability, particularly in oral and topical formulations. Aging populations and rising chronic diseases in Europe support this trend, increasing demand for specialized cellulose derivatives.

- •Innovation in personal care products emphasizes natural and biodegradable ingredients, boosting demand for hydroxyethyl cellulose in lotions, shampoos, and cosmetics. Consumer preference towards clean-label products and strict EU cosmetic regulations further stimulate this segment’s growth.

- •Food & beverage manufacturers increasingly adopt carboxymethyl cellulose and methyl cellulose as texture stabilizers and emulsifiers to meet consumer expectations for natural ingredients and improved shelf life, aided by technological advancements in cellulose ether formulations tailored for food safety.

- •Paints and coatings sectors benefit from cellulose ethers’ rheological control and film-forming properties, enhancing product performance and sustainability. Demand for low-VOC and water-based paints in Europe, driven by environmental legislation, fosters growth of cellulose ether derivatives in this application.

Market Trends

- •The market is witnessing a shift towards bio-based and biodegradable cellulose ethers as European regulations heighten focus on sustainability. Manufacturers invest in green chemistry processes and renewable raw materials to align with circular economy principles.

- •Digitalization and Industry 4.0 adoption in manufacturing enable improved process control and product consistency for cellulose ether production, reducing waste and enhancing quality assurance.

- •Collaborations between chemical producers and downstream industries facilitate development of customized cellulose ether solutions addressing specific application challenges, fostering innovation and market differentiation.

- •Expanding use of cellulose ethers in emerging pharmaceutical technologies such as 3D printed drugs and advanced drug delivery systems marks a growing trend, supported by increasing R&D investments.

- •The rise of water-based and environmentally friendly paints and coatings in Europe propels demand for cellulose ethers with enhanced rheological and film-forming properties, aligning with consumer and regulatory requirements.

Market Opportunities

- •Growing demand for sustainable construction materials offers opportunities to develop advanced cellulose ether formulations that improve energy efficiency and durability, particularly in green building projects.

- •Pharmaceutical industry expansion in Europe presents opportunities for cellulose ether producers to supply specialized excipients for controlled release and novel drug delivery platforms.

- •Innovation in personal care and cosmetic products with a focus on natural ingredients creates openings for cellulose ethers tailored to meet clean-label and biodegradability standards.

- •Emerging markets within Eastern Europe offer growth prospects due to increasing industrialization and infrastructure development, which will heighten demand for construction-grade cellulose ethers.

- •Strategic partnerships with food manufacturers enable cellulose ether suppliers to co-develop texture and stability enhancers aligned with evolving consumer preferences for healthier and natural products.

Market Challenges

- •Stringent European regulations on chemical safety and environmental impact impose compliance costs and operational constraints on cellulose ether manufacturers, potentially delaying product launches and increasing expenses.

- •Raw material price volatility, particularly in cellulose pulp and derivatives, affects production costs and profitability, complicating long-term pricing strategies for market players.

- •Technical challenges in tailoring cellulose ether properties to meet diverse and evolving application requirements demand significant R&D investment and specialized expertise.

- •Competition from alternative synthetic polymers and new bio-based materials with similar functionalities exerts pressure on market share and necessitates continuous innovation.

- •Supply chain disruptions caused by geopolitical tensions and logistics constraints in Europe may affect timely availability of raw materials and finished products, impacting customer satisfaction.

Regulatory Framework

- •Between 2020 and 2025, the European Chemicals Agency (ECHA) implemented the REACH regulation updates requiring enhanced safety data and usage restrictions for certain cellulose ether derivatives, impacting formulation and compliance workflows.

- •The EU Biocidal Products Regulation (BPR) introduced stricter approval processes for cellulose ethers used in antimicrobial applications, necessitating additional testing and documentation.

- •New EU regulations on cosmetic product safety (Cosmetics Regulation EC 1223/2009 amendments) have tightened ingredient disclosure and banned certain synthetic polymers, increasing demand for cellulose ethers in personal care.

- •The Construction Products Regulation (CPR) mandates performance and environmental standards for building materials, influencing cellulose ether formulations used in cement and plaster additives.

- •Government initiatives promoting circular economy and bio-based products provide incentives and subsidies for cellulose ether manufacturers investing in sustainable production technologies.

Market Intelligence

- •15th January 2025, BASF SE launched a new line of eco-friendly hydroxypropyl methylcellulose products designed specifically for sustainable construction applications. These products offer enhanced water retention and workability while reducing environmental impact. BASF aims to strengthen its position in the European market by addressing growing demand for green building materials, supported by regulatory incentives and customer interest in sustainable solutions. The launch includes technical support and collaborative development programs with construction firms to optimize product performance in real-world applications. This initiative underscores BASF’s commitment to innovation aligned with Europe’s environmental goals.

- •20th March 2025, Nouryon announced the commercialization of a next-generation carboxymethyl cellulose tailored for food and beverage industries. The product enhances texture stability and shelf life while complying with stringent EU food safety standards. Nouryon’s innovation focuses on clean-label formulations responding to consumer demand for natural and plant-based ingredients. The company partnered with leading European food manufacturers to validate performance in bakery, dairy, and beverage applications. This launch positions Nouryon to capture increasing market share in the growing natural additives segment.

- •10th July 2025, Akzo Nobel N.V. expanded its cellulose ether production capacity in its Netherlands facility to meet rising demand from pharmaceutical and personal care sectors. The expansion includes state-of-the-art manufacturing lines equipped with advanced process controls to ensure product consistency and sustainability. Akzo Nobel plans to leverage this increased capacity to support new product developments and strengthen supply chain resilience across Europe. The move reflects strategic investment to capitalize on market growth driven by regulatory and consumer trends favoring bio-based polymers.

- •5th September 2025, Lamberti S.p.A. entered a strategic partnership with CelluComp Ltd. to co-develop innovative hydroxyethyl cellulose derivatives for advanced personal care formulations. This collaboration combines Lamberti’s large-scale manufacturing expertise with CelluComp’s proprietary cellulose technology to create high-performance, biodegradable ingredients. The partnership aims to accelerate product development cycles and expand market reach across Europe’s personal care industry, addressing consumer preferences for natural and sustainable products while complying with evolving EU regulations.

- •Source: Official company press releases, Industry publications

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Italy is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 6.8 Billion |

| CAGR | 6.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.7% |

| Scope of Report | Market is segmented by Cellulose Ether Type (Methyl Cellulose, Hydroxypropyl Methylcellulose, Carboxymethyl Cellulose, Ethyl Cellulose, Hydroxyethyl Cellulose), Application Sector (Construction, Pharmaceuticals, Food & Beverages, Personal Care, Paints & Coatings), End-Use Industry (Building & Infrastructure, Healthcare & Pharmaceuticals, Food Processing, Cosmetics & Hygiene, Industrial Coatings), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Sales) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Ashland Global Holdings Inc. (United States), Dow Chemical Company (United States), Domsjö Fabriker AB (Sweden), Hercules Incorporated (United States), CP Kelco (United States), Shin-Etsu Chemical Co., Ltd. (Japan), Akzo Nobel N.V. (Netherlands), Lotte Fine Chemical (South Korea), CelluComp Ltd. (United Kingdom), J. Rettenmaier & Söhne GmbH + Co KG (Germany), Süd-Chemie AG (Germany), Biesterfeld AG (Germany), Cargill, Incorporated (United States), Akzo Nobel Chemicals GmbH (Germany), Nouryon (Netherlands), Lamberti S.p.A. (Italy), Celanese Corporation (United States), Noviant (France), Sappi Limited (South Africa), FMC Corporation (United States), Sinopec (China), BASF SE (Germany), Evonik Industries AG (Germany), Nippon Paper Industries Co., Ltd. (Japan), Mitsubishi Chemical Corporation (Japan) |

Europe Cellulose Ether & Its Derivatives Market - Europe Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.