Global Bonding Films Market Size, Growth & Revenue 2024-2034

Global Bonding Films Market is segmented by Application (Electronics, Automotive, Construction, Packaging, Medical), Type (Adhesive Films, Heat Seal Films, Pressure Sensitive Films, UV Cure Films, Others), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Bonding Films market is a dynamic sector focused on the production and application of specialized adhesive films used to bond materials in electronics, automotive, construction, packaging, and medical industries. This market covers a broad spectrum of product types, including adhesive films, heat seal films, pressure-sensitive films, and UV cure films, each designed to meet specific industrial requirements for durability, flexibility, and efficiency. The films serve as essential components for lightweight assemblies, enhanced product aesthetics, and improved manufacturing processes, positioning them as critical in advanced technology adoption and sustainable manufacturing practices. Increasing demand for miniaturization in electronics, lightweight automotive components, and eco-friendly packaging solutions drives market expansion. Furthermore, regional growth dynamics are shaped by technological innovation, regulatory frameworks, and supply chain optimization. The market's competitive landscape is marked by continuous R&D, strategic collaborations, and mergers & acquisitions, ensuring rapid evolution aligned with global industrial trends and consumer needs.

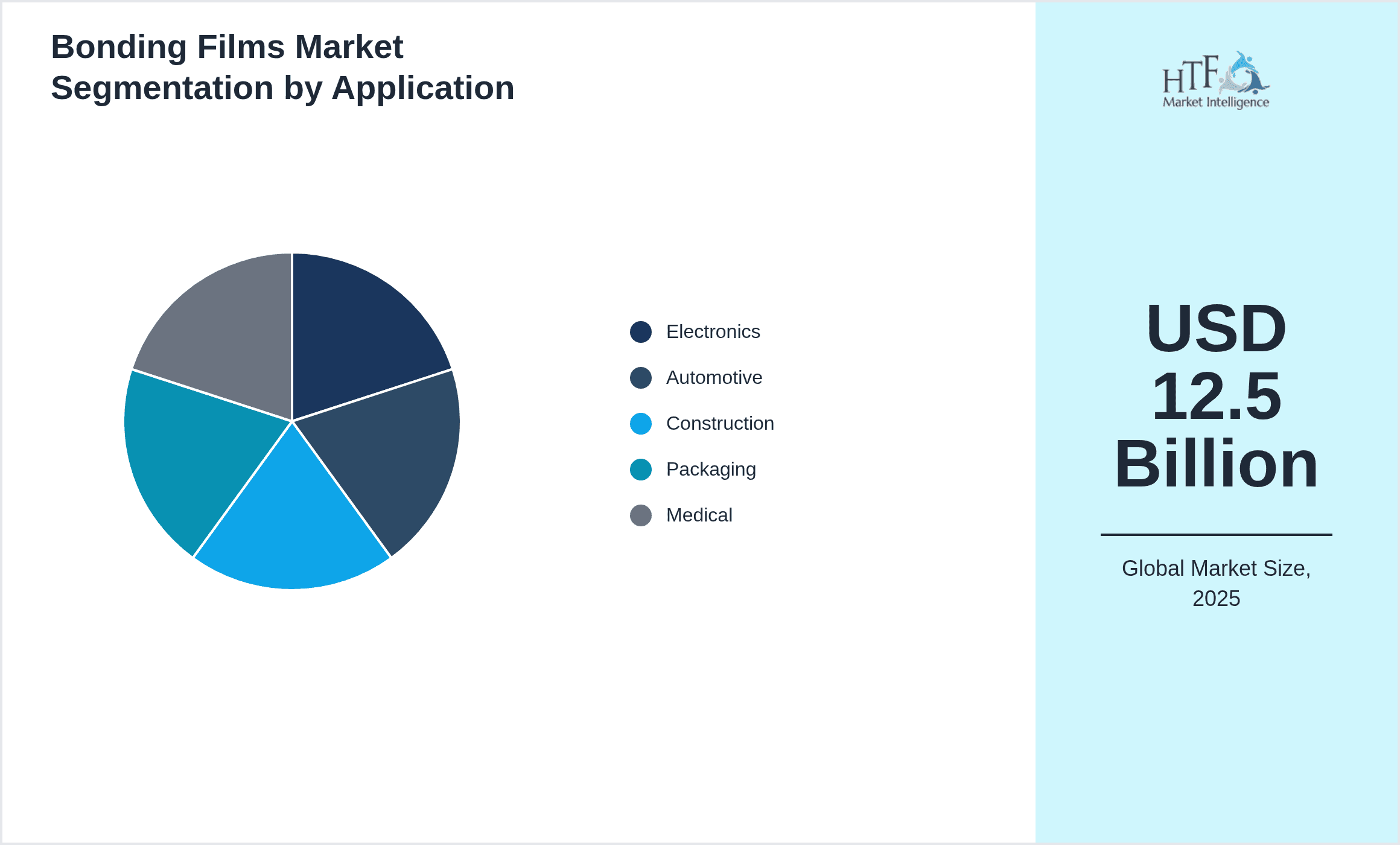

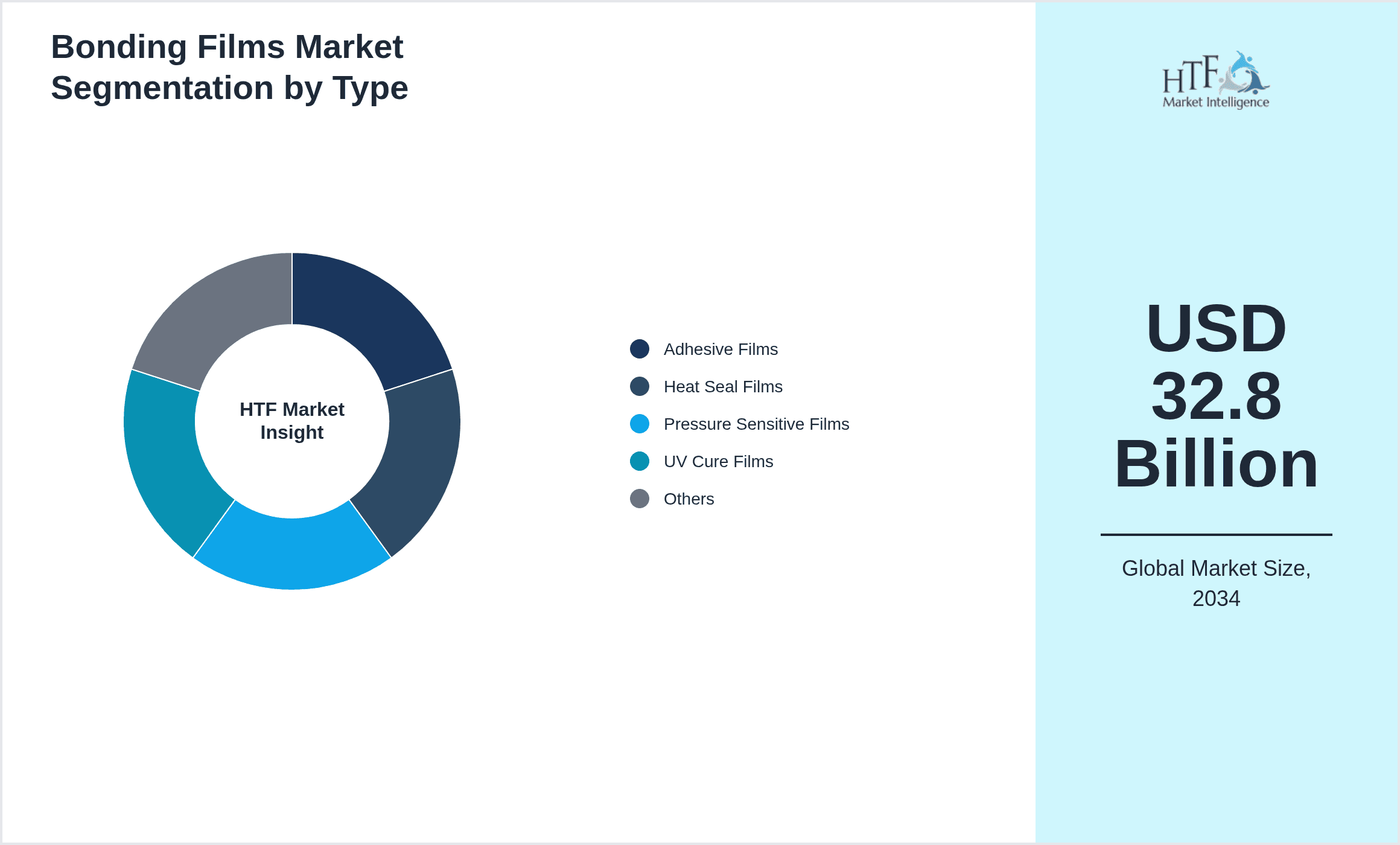

- •Key highlights reveal that the global Bonding Films market, valued at USD 12.5 Billion in 2024, is projected to reach USD 32.8 Billion by 2034, demonstrating a robust CAGR of 10.3%. North America dominates the market due to advanced manufacturing infrastructure and high adoption in electronics and automotive sectors, while Asia-Pacific emerges as the fastest-growing region propelled by expanding industrialization and automotive production. Adhesive films maintain the leading product type status, accounting for the largest market share, whereas UV cure films exhibit the highest growth rate driven by their superior bonding performance and environmental benefits. Market trends indicate increasing emphasis on sustainable materials, digital printing integration, and customization capabilities. Despite growth opportunities, challenges such as raw material price volatility and stringent regulatory requirements persist. Overall, the market presents significant investment potential, with innovation and strategic partnerships underpinning future expansion.

- •The value proposition of bonding films lies in their ability to provide reliable, efficient, and versatile bonding solutions that address the evolving needs of multiple industries. Their strategic importance is evident in enhancing product design flexibility, reducing assembly times, and improving durability and environmental compliance. Key stakeholders—including manufacturers, raw material suppliers, and end-users—benefit from continuous innovation that enables lightweighting, sustainability, and cost-effectiveness. The market facilitates cross-sector advancements, supporting the development of cutting-edge electronics, safer automotive components, and sustainable packaging solutions. With increasing awareness of environmental regulations and consumer preferences for eco-friendly products, bonding films are positioned as critical enablers of green manufacturing. This underscores the market’s role in driving technological progress and competitive differentiation across global industrial landscapes.

Competitive Landscape

The global Bonding Films market exhibits a highly competitive environment characterized by a mix of multinational corporations and regional specialists. Market players emphasize continuous innovation, focusing on developing advanced adhesive technologies that improve bonding strength, environmental resistance, and application versatility. Competitive strategies include investing in R&D, forging strategic partnerships, and expanding production capacities to cater to diverse industry needs. Companies differentiate through product customization, sustainability initiatives, and enhanced service offerings, fostering customer loyalty and market penetration. Mergers and acquisitions are prevalent, facilitating technology consolidation and geographic expansion. Pricing strategies balance cost competitiveness with quality assurance, while distribution networks are optimized for global reach. Additionally, players actively monitor regulatory changes to ensure compliance and mitigate market risks. The rivalry among market participants drives rapid technological evolution, positioning the sector for sustained growth and dynamic market shifts over the coming decade.

Leading Companies in Bonding Films Market

- •3M Company (United States)

- •Avery Dennison Corporation (United States)

- •DuPont de Nemours, Inc. (United States)

- •Henkel AG & Co. KGaA (Germany)

- •Nitto Denko Corporation (Japan)

- •Tesa SE (Germany)

- •LINTEC Corporation (Japan)

- •Scapa Group plc (United Kingdom)

- •Sekisui Chemical Co., Ltd. (Japan)

- •Berry Global, Inc. (United States)

- •Sika AG (Switzerland)

- •Wacker Chemie AG (Germany)

- •Constantia Flexibles Group GmbH (Austria)

- •Toray Industries, Inc. (Japan)

- •Jindal Poly Films Limited (India)

- •Mactac (United States)

- •BASF SE (Germany)

- •Kolon Industries, Inc. (South Korea)

- •Bemis Company, Inc. (United States)

- •Eastman Chemical Company (United States)

- •Bridgestone Corporation (Japan)

- •Kuraray Co., Ltd. (Japan)

- •Mitsubishi Chemical Corporation (Japan)

- •Sealed Air Corporation (United States)

- •Arkema S.A. (France)

Global Bonding Films Market Segmentation

- •By Type

- ◦Adhesive Films

- ◦Heat Seal Films

- ◦Pressure Sensitive Films

- ◦UV Cure Films

- ◦Others

- •By Application

- ◦Electronics

- ◦Automotive

- ◦Construction

- ◦Packaging

- ◦Medical

- •By End-Use Industry

- ◦Consumer Electronics

- ◦Industrial Manufacturing

- ◦Healthcare Products

- ◦Automotive Assembly

- ◦Food & Beverage Packaging

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Retail

- ◦Third-Party Resellers

Growth Dynamics of Global Bonding Films Market

- •The global bonding films market is propelled by rapid advancements in electronics and automotive sectors, where the demand for lightweight, durable, and high-performance bonding solutions is increasing. Innovations in adhesive chemistry and film technology enable manufacturers to meet stringent industry standards for strength and environmental resistance. Growing adoption of electric vehicles and miniaturized electronic devices further stimulates market growth, as bonding films contribute to improved energy efficiency and device compactness. Additionally, rising awareness of sustainability and eco-friendly manufacturing practices drives the shift towards solvent-free and UV-curable bonding films. The expanding construction and packaging industries also contribute significantly, leveraging bonding films for enhanced durability and product protection. Overall, technological progress, coupled with rising industrial investments, forms a robust growth foundation for the market.

- •Emerging trends include the integration of smart bonding films embedded with sensing capabilities for real-time monitoring in electronics and automotive applications. Manufacturers are increasingly adopting digital printing and customization to meet specific client needs, enabling tailored bonding solutions. The trend toward sustainable raw materials and recyclable films is gaining momentum, driven by regulatory pressures and consumer preferences. Furthermore, there is a growing focus on multi-functional films combining bonding with insulation or barrier properties, expanding application potential. Collaborative innovation between chemical companies and end-users fosters rapid technology adoption and market expansion. These trends collectively accelerate product diversification and competitive differentiation in the bonding films market.

- •Despite promising growth, the market faces restraints including volatility in raw material prices such as polymers and additives, which impacts production costs and profitability. Regulatory compliance related to volatile organic compounds (VOCs) and environmental safety imposes additional challenges for manufacturers. Technical limitations in bonding films, such as temperature sensitivity and limited adhesion on certain substrates, restrict application scope. Moreover, intense competition leads to pricing pressures and margin erosion. Supply chain disruptions and fluctuating demand in end-use industries also create uncertainties. Addressing these restraints requires continuous innovation in materials science and strategic supply chain management.

- •Opportunities abound in expanding into emerging markets with growing industrialization and automotive production, particularly in Asia-Pacific and Latin America. Development of bio-based and biodegradable bonding films offers avenues for differentiation and regulatory compliance. Integration of bonding films into new applications such as flexible electronics, wearable devices, and medical implants presents untapped market potential. Strategic collaborations between chemical producers and end-users can accelerate product development and market penetration. Additionally, advancements in digital manufacturing and automation create efficiencies in bonding film production, reducing costs and improving quality. Capitalizing on these opportunities will be key to sustaining competitive advantage and market growth.

- •Key challenges include navigating complex regulatory landscapes across different regions, which require adaptation of products and processes to meet diverse standards. High initial investment costs for developing advanced bonding films and scaling production limit entry for new players. The need for continuous innovation to overcome technical barriers demands substantial R&D expenditure. Market fragmentation with numerous small and medium enterprises intensifies competition, complicating market consolidation. Furthermore, customer education and convincing traditional industries to adopt bonding films over conventional adhesives remain ongoing challenges. Effective risk management and strategic planning are essential to overcome these obstacles and leverage market potential.

Market Trends in Bonding Films

- •Increasing demand for eco-friendly and solvent-free bonding films is driving innovation toward sustainable materials and manufacturing processes, aligning with global environmental objectives and consumer preferences. Companies are actively developing bio-based adhesives and recyclable film solutions to reduce carbon footprint and comply with stringent regulations.

- •The adoption of UV-curable bonding films is gaining traction due to their rapid curing times, strong adhesion, and lower environmental impact compared to solvent-based adhesives. This trend is particularly pronounced in electronics and automotive manufacturing, where production efficiency and durability are critical.

- •Customization and digital printing technologies enable manufacturers to offer tailored bonding films that meet specific application needs, such as varying thickness, adhesive strength, and functional properties. This personalization trend enhances product differentiation and customer satisfaction.

- •Integration of multi-functional properties into bonding films, such as thermal insulation, electrical conductivity, and barrier protection, is expanding application areas and creating value-added products. This trend supports the development of advanced electronics and packaging solutions.

- •Strategic collaborations among raw material suppliers, bonding film manufacturers, and end-users are fostering innovation ecosystems that accelerate technology adoption and market expansion. Such partnerships facilitate co-development and faster time-to-market for new products.

- •Rising automation and digitalization in bonding film production processes enhance manufacturing precision, reduce waste, and improve scalability. Industry 4.0 technologies are increasingly integrated to optimize quality control and supply chain efficiency.

- •Growing emphasis on lightweight and flexible bonding solutions in automotive and electronics industries is driving research into novel polymers and adhesive systems. This focus supports the trend toward miniaturization and energy-efficient product designs.

Emerging Opportunities in Bonding Films Market

- •Expanding presence in emerging economies with rapid industrialization offers significant growth potential due to increasing automotive production and electronics manufacturing, creating new demand for bonding films. Market entry strategies tailored to local requirements can unlock these opportunities.

- •Development of bio-based and biodegradable bonding films addresses growing regulatory pressures and consumer demand for sustainable products, offering differentiation and compliance advantages in competitive markets.

- •Innovations in flexible electronics and wearable devices open new application areas where bonding films play a crucial role in assembly and durability, providing avenues for product diversification and premium pricing.

- •Collaborations between chemical companies and technology firms enable co-creation of advanced bonding solutions tailored to emerging industry needs, accelerating innovation and market penetration.

- •Integration of bonding films with digital manufacturing and automation technologies enhances production efficiency and customization capabilities, reducing costs and improving market responsiveness.

- •Expansion into the healthcare sector, including medical device assembly and packaging, leverages the biocompatibility and precision bonding attributes of advanced films, offering high-margin growth prospects.

- •Increasing demand for lightweight automotive components driven by electric vehicle adoption creates opportunities for bonding films that contribute to weight reduction and enhanced safety standards.

Key Challenges Constraining Bonding Films Market Growth

- •Volatility in raw material prices, particularly polymers and specialty additives, raises production costs and impacts profit margins, necessitating effective supply chain management and cost control strategies by manufacturers.

- •Stringent environmental regulations concerning VOC emissions and chemical safety impose compliance burdens and require continuous reformulation of bonding films, increasing R&D expenditures and time-to-market.

- •Technical limitations such as adhesion difficulties with certain substrates and sensitivity to environmental factors restrict the use of bonding films in some applications, driving the need for material innovation and testing.

- •Intense competition and price pressures in mature markets challenge profitability, compelling companies to innovate and differentiate products while maintaining cost efficiency.

- •Supply chain disruptions, including raw material shortages and logistics constraints, create uncertainties in production schedules and inventory management, affecting market stability and customer satisfaction.

- •Customer hesitation in replacing traditional adhesives with bonding films, often due to lack of awareness or perceived risks, limits market penetration in certain industry segments.

- •High capital investment requirements for advanced bonding film production technologies act as barriers to entry for smaller players, limiting market diversity and innovation pace.

Regulatory Framework Impacting Global Bonding Films Market

- •From 2020 to 2024, global regulatory bodies have increasingly enforced limits on volatile organic compound (VOC) emissions associated with adhesive products, prompting manufacturers to develop low-VOC and solvent-free bonding films. These regulations impact product formulations and manufacturing processes, requiring compliance certifications and environmental audits.

- •The introduction of chemical safety standards such as REACH in Europe and TSCA in the United States mandates thorough evaluation of raw materials used in bonding films, ensuring consumer and environmental safety. Non-compliance leads to market access restrictions and financial penalties.

- •Emerging regulations on recyclability and eco-design promote the adoption of bio-based and recyclable bonding films, encouraging manufacturers to innovate sustainable product lines aligned with circular economy principles.

- •Regional mandates on workplace safety and chemical handling influence operational guidelines for bonding film production facilities, enhancing worker protection and process standardization across markets.

- •Government incentives and support programs in key regions foster R&D investments in advanced bonding technologies, supporting market growth while ensuring alignment with environmental and safety objectives.

Market Intelligence

- •15th January 2024, 3M Company launched a new range of UV-curable bonding films designed for flexible electronics applications, featuring rapid curing times and enhanced adhesion properties. This product aims to meet the increasing demand for lightweight and durable bonding solutions in wearable devices and next-generation electronics. The launch positions 3M as a key innovator in the bonding films sector, targeting growth in Asia-Pacific and North American markets with scalable manufacturing capabilities. Strategic marketing efforts emphasize sustainability credentials and customization options, responding to evolving customer needs. Source: 3M Official Press Release

- •10th October 2023, Avery Dennison Corporation introduced advanced adhesive films with bio-based components, aligning with global sustainability goals and regulatory requirements. These films offer equivalent bonding strength while reducing environmental impact, targeting packaging and automotive industries. The innovation strengthens Avery Dennison’s product portfolio and supports expanding demand in Europe and North America. Collaborative efforts with raw material suppliers ensured rapid commercialization and compliance with international standards. Source: Avery Dennison Company Webpage

- •5th May 2024, Henkel AG & Co. KGaA announced a strategic partnership with a leading electronics manufacturer to co-develop customized bonding films for electric vehicle battery assembly. This initiative aims to enhance battery safety and performance through advanced adhesive technologies, leveraging Henkel’s R&D expertise and the partner’s industry insight. The collaboration is expected to accelerate market penetration in the automotive sector and strengthen Henkel’s competitive position globally. Source: Henkel Corporate Announcement

- •20th November 2023, Nitto Denko Corporation expanded its production facility in Japan to increase capacity for pressure-sensitive bonding films used in medical device applications. The investment supports growing demand driven by healthcare innovation and regulatory approvals for advanced medical adhesives. Enhanced manufacturing efficiency and quality control measures enable faster delivery and product customization, positioning Nitto Denko as a preferred supplier in the medical bonding films segment. Source: Nitto Denko News

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 32.8 Billion |

| CAGR | 10.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.8% |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | 3M Company (United States), Avery Dennison Corporation (United States), DuPont de Nemours, Inc. (United States), Henkel AG & Co. KGaA (Germany), Nitto Denko Corporation (Japan), Tesa SE (Germany), LINTEC Corporation (Japan), Scapa Group plc (United Kingdom), Sekisui Chemical Co., Ltd. (Japan), Berry Global, Inc. (United States), Sika AG (Switzerland), Wacker Chemie AG (Germany), Constantia Flexibles Group GmbH (Austria), Toray Industries, Inc. (Japan), Jindal Poly Films Limited (India), Mactac (United States), BASF SE (Germany), Kolon Industries, Inc. (South Korea), Bemis Company, Inc. (United States), Eastman Chemical Company (United States), Bridgestone Corporation (Japan), Kuraray Co., Ltd. (Japan), Mitsubishi Chemical Corporation (Japan), Sealed Air Corporation (United States), Arkema S.A. (France) |

Global Bonding Films Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.