Global Adhesive Resin Market - Outlook 2020-2034

Global Adhesive Resin Market is segmented by Adhesive Resin Type (Epoxy Resins, Acrylic Resins, Polyurethane Adhesives, Silicone Resins, Polyester Resins), Application Segment (Construction Adhesives, Automotive Adhesives, Packaging Adhesives, Electronics Adhesives, Woodworking Adhesives), Service Type (Custom Resin Formulation, Standard Resin Supply, Technical Support Services, After-Sales Service), Deployment Model (Bulk Resin Supply, Pre-Formulated Adhesive Products, On-Site Mixing Services), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global adhesive resin market is a critical sector within the chemicals industry, supplying essential components for manufacturing adhesives that facilitate bonding across multiple industries. These resins, including epoxy, acrylic, polyurethane, silicone, and polyester types, serve pivotal roles in applications ranging from construction and automotive to packaging and electronics. The market's scope covers the entire value chain from raw material extraction and resin synthesis to adhesive formulation and end-user consumption. Adhesive resins provide key attributes such as enhanced mechanical strength, chemical resistance, and environmental durability, enabling manufacturers to meet the evolving demands of modern industries. The increasing focus on lightweight materials, sustainability, and performance optimization drives the development of advanced resin technologies. Market growth is supported by expanding infrastructure projects, automotive production, and packaging innovation globally. Furthermore, regional market dynamics vary, with North America leading in market size due to established industrial bases and stringent quality standards, while Asia-Pacific exhibits rapid growth owing to burgeoning manufacturing activities and urbanization. The strategic importance of adhesive resins lies in their ability to improve product longevity and reduce environmental impact, positioning this market as a vital contributor to global industrial advancement.

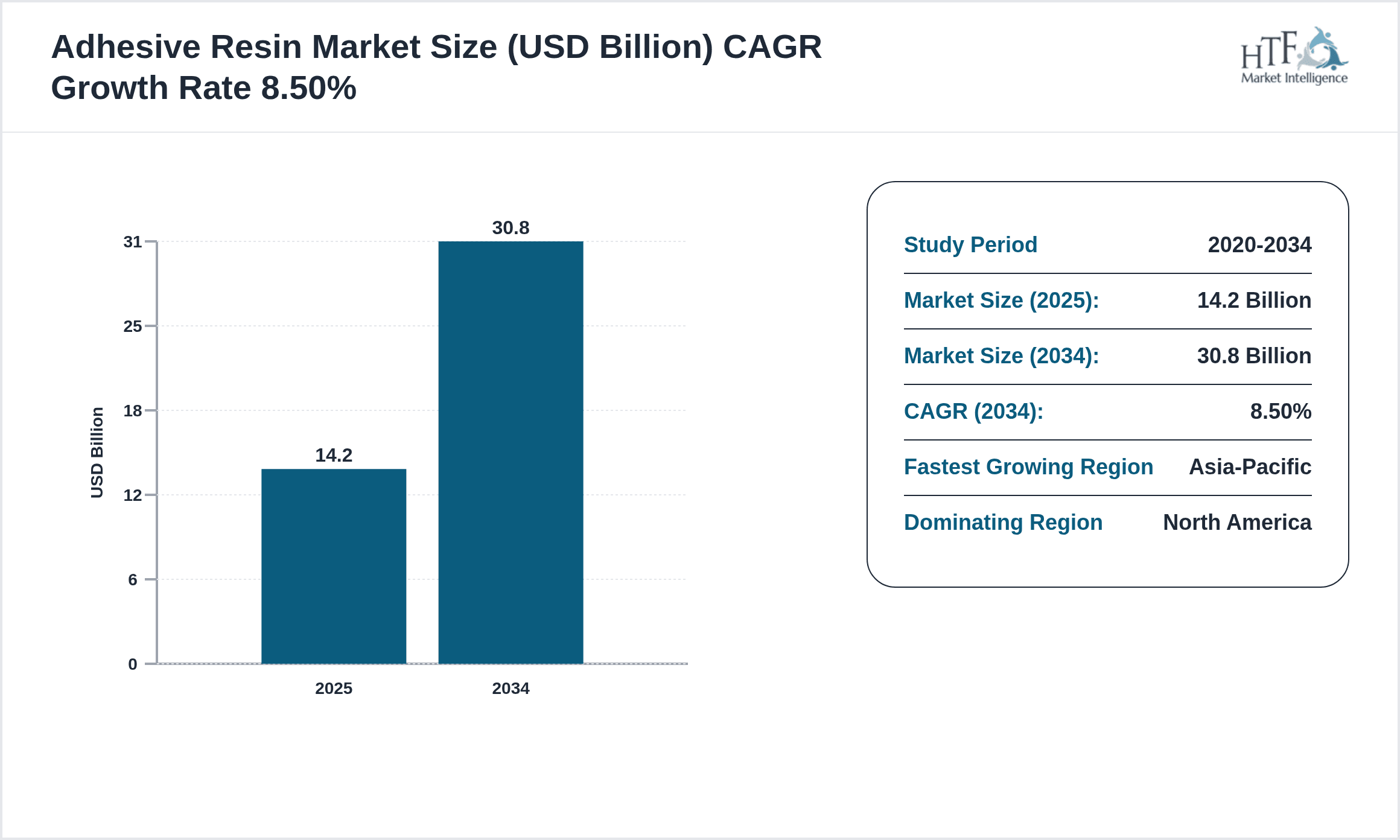

- •Key market highlights include a base market size of USD 14.2 Billion in 2025, with a projected growth to USD 30.8 Billion by 2034 at a compound annual growth rate (CAGR) of 8.5%. Year-on-year growth averages 8.2%, reflecting robust adoption across various end-use sectors. Epoxy resins dominate the product segment due to their superior bonding properties and versatility, while polyurethane adhesives are the fastest-growing type, driven by demand in automotive and electronics applications. North America currently dominates the market, attributed to technological advancements and a mature industrial ecosystem, whereas Asia-Pacific is the fastest-growing region, propelled by rapid industrialization and infrastructure expansion.

- •The adhesive resin market offers significant value proposition to stakeholders including resin manufacturers, adhesive formulators, and end users by enabling innovation in product design and assembly processes. Its strategic importance is underscored by applications that enhance product performance, reduce manufacturing costs, and contribute to environmental sustainability through development of bio-based and low-VOC resins. As industries increasingly prioritize durability and eco-friendliness, adhesive resins stand at the forefront of materials technology, fostering competitive advantage and facilitating market expansion across geographies.

Competitive Landscape

The competitive environment in the global adhesive resin market is characterized by intense rivalry among key players leveraging technological innovation, strategic partnerships, and geographic expansion to secure market share. Leading manufacturers invest heavily in research and development to enhance resin properties such as adhesion strength, chemical resistance, and environmental compliance, thereby differentiating their product portfolios. Market participants adopt diverse strategies including mergers and acquisitions, collaborations with end-use industries, and capacity expansions to enhance production capabilities and distribution networks. Pricing strategies are influenced by raw material costs and regulatory compliance expenses, while companies emphasize sustainability by developing bio-based and low-emission resin solutions to align with global environmental standards. Distribution channels are optimized through direct sales, distributors, and e-commerce platforms to reach diverse customer segments. Furthermore, regional competition is shaped by localized manufacturing hubs in Asia-Pacific and Europe, with emerging market entrants focusing on niche applications and customized solutions. Future trends point toward increased adoption of digitalization in supply chain management and the integration of smart materials to meet evolving industry requirements, underscoring a dynamic and innovation-driven competitive landscape.

Leading Companies in Adhesive Resin Market

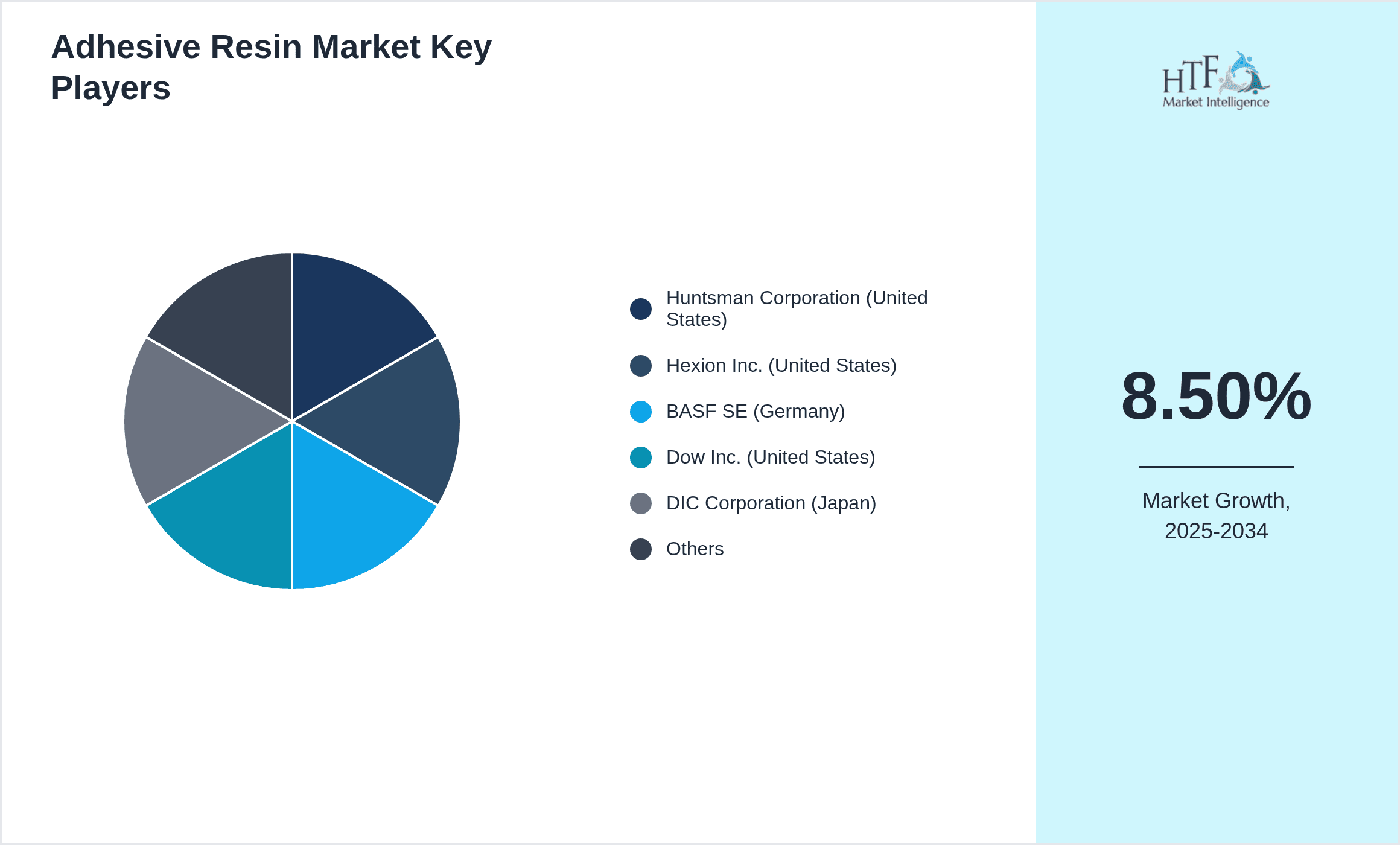

- •Huntsman Corporation (United States)

- •Hexion Inc. (United States)

- •BASF SE (Germany)

- •Dow Inc. (United States)

- •DIC Corporation (Japan)

- •Sika AG (Switzerland)

- •Henkel AG & Co. KGaA (Germany)

- •MITSUI Chemicals Inc. (Japan)

- •Kumho P&B Chemicals Inc. (South Korea)

- •Arkema S.A. (France)

- •Wanhua Chemical Group Co. Ltd. (China)

- •Kuraray Co. Ltd. (Japan)

- •Eastman Chemical Company (United States)

- •Synthomer plc (United Kingdom)

- •Evonik Industries AG (Germany)

- •Jowat SE (Germany)

- •3M Company (United States)

- •Momentive Performance Materials Inc. (United States)

- •Celanese Corporation (United States)

- •LG Chem Ltd. (South Korea)

- •Shin-Etsu Chemical Co. Ltd. (Japan)

- •Allnex (Germany)

- •Nippon Paint Holdings Co. Ltd. (Japan)

- •H.B. Fuller Company (United States)

- •Sasol Limited (South Africa)

Market Breakdown

- •By Adhesive Resin Type

- ◦Epoxy Resins

- ◦Acrylic Resins

- ◦Polyurethane Adhesives

- ◦Silicone Resins

- ◦Polyester Resins

- •By Application Segment

- ◦Construction Adhesives

- ◦Automotive Adhesives

- ◦Packaging Adhesives

- ◦Electronics Adhesives

- ◦Woodworking Adhesives

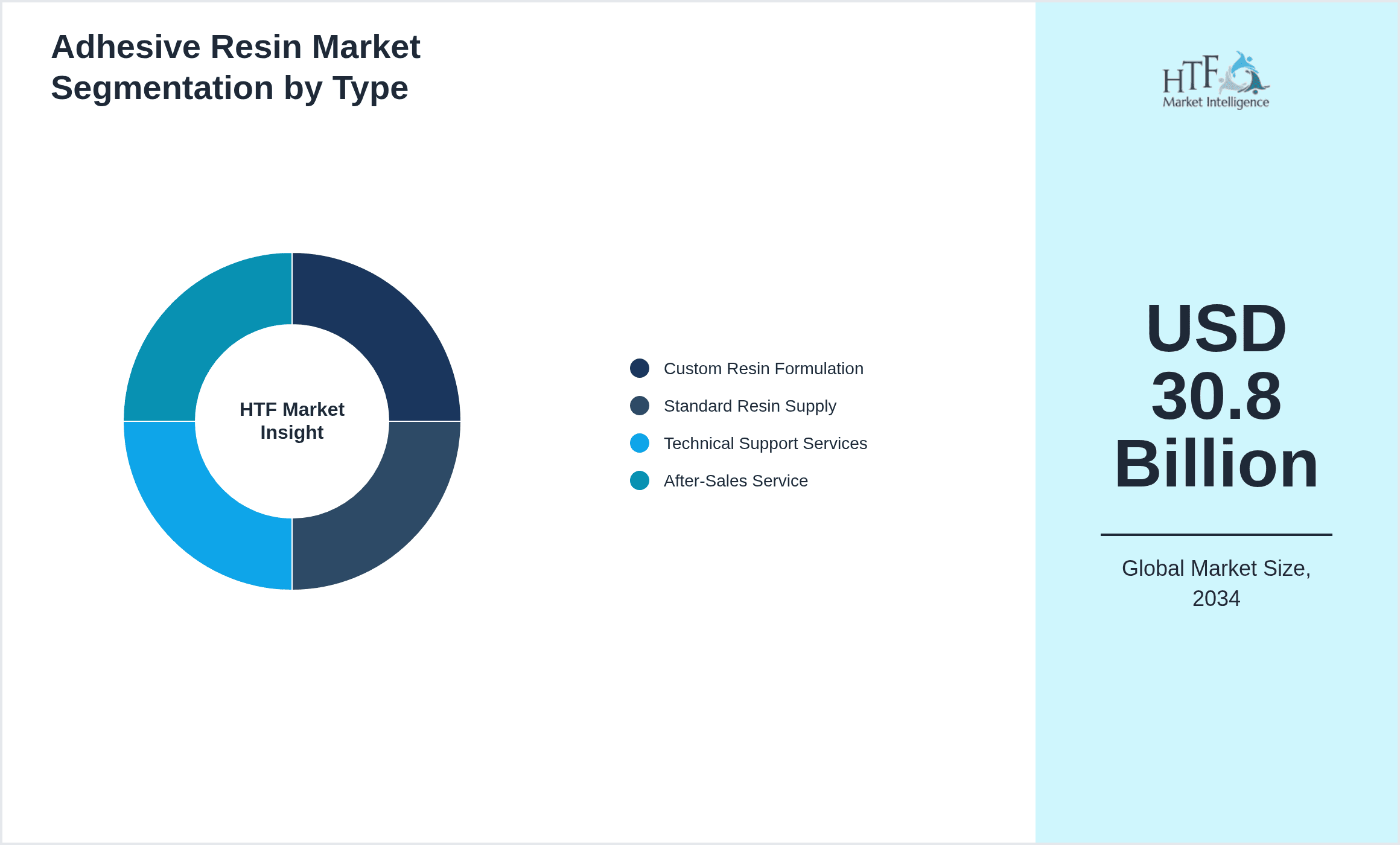

- •By Service Type

- ◦Custom Resin Formulation

- ◦Standard Resin Supply

- ◦Technical Support Services

- ◦After-Sales Service

- •By Deployment Model

- ◦Bulk Resin Supply

- ◦Pre-Formulated Adhesive Products

- ◦On-Site Mixing Services

Growth Dynamics

- •Rising demand for lightweight and high-strength materials in automotive manufacturing drives growth in adhesive resin consumption, as these resins enable weight reduction and fuel efficiency without compromising safety. Manufacturers are increasingly adopting epoxy and polyurethane adhesives to meet stringent performance criteria.

- •Expansion of construction and infrastructure projects globally fuels the demand for durable and weather-resistant adhesives, with acrylic and polyester resins widely used for bonding and sealing applications, supporting robust market growth across regions.

- •Technological advancements in resin chemistry, including development of bio-based and low-VOC (volatile organic compound) resins, align with environmental regulations and consumer preferences, promoting sustainable adhesive solutions and expanding market opportunities.

- •Growth in the packaging industry, particularly flexible packaging, increases demand for specialized adhesive resins that provide excellent bonding with diverse substrates, enhancing product protection and shelf life.

- •Increasing electronics miniaturization and complexity require high-performance silicone and epoxy resins for encapsulation and insulation, driving innovation and market expansion in the electronics adhesives segment.

- •Emerging markets in Asia-Pacific and Latin America experience industrialization and urbanization, leading to rising consumption of adhesive resins in automotive, construction, and packaging sectors, making them fastest-growing regions.

- •Investment in R&D by key players to develop customized adhesive resin formulations for niche applications enhances product differentiation and supports market growth through tailored solutions.

Market Trends

- •The trend toward environmentally friendly adhesive resins is gaining momentum, with manufacturers focusing on bio-based and waterborne resins that reduce environmental impact without sacrificing performance.

- •Integration of digital technologies such as AI and IoT in resin formulation and production processes improves quality control, efficiency, and customization capabilities, setting new industry standards.

- •Collaborations between resin manufacturers and end-use industries facilitate co-development of adhesives tailored for specific applications, accelerating innovation and market penetration.

- •Increasing adoption of multi-functional adhesive resins that offer combined properties such as adhesion, sealing, and corrosion resistance enhances product versatility and market appeal.

- •Shift towards lightweight and flexible packaging solutions drives demand for advanced acrylic and polyurethane adhesive resins with superior bonding and durability.

- •Sustainability regulations and consumer awareness push for low-VOC and solvent-free adhesive resins, influencing product development and market dynamics globally.

- •Advanced silicone resins are increasingly used in electronics for thermal management and electrical insulation, reflecting growing demand in consumer electronics and automotive electronics sectors.

Market Opportunities

- •Emerging applications in renewable energy sectors such as wind and solar power present growth potential for adhesive resins with enhanced durability and environmental resistance, creating new market segments.

- •Untapped potential in emerging economies offers opportunity for market expansion through localized production and supply chain optimization catering to rapidly growing industrial sectors.

- •Development of bio-based and biodegradable adhesive resins can capture demand from environmentally conscious consumers and regulatory bodies, fostering sustainable growth and competitive advantage.

- •Increasing use of adhesive resins in electric vehicle manufacturing, particularly for battery assembly and lightweight components, opens avenues for product innovation and revenue growth.

- •Partnerships and strategic alliances between resin manufacturers and technology providers enable accelerated development of smart adhesives, responsive to environmental stimuli, enhancing product functionality.

- •Expansion in packaging industry demand for flexible and recyclable materials drives the need for advanced adhesive resins capable of maintaining bond integrity while supporting sustainability goals.

- •Growing electronics market adoption of high-performance adhesive resins for miniaturized and wearable devices offers niche opportunities for specialized resin formulations.

Market Challenges

- •Volatility in raw material prices, particularly petrochemical derivatives, leads to fluctuating production costs, impacting pricing strategies and profit margins for adhesive resin manufacturers.

- •Stringent environmental and safety regulations require costly compliance measures and reformulation of products to meet evolving standards, posing operational challenges.

- •High competition from regional players offering low-cost alternatives pressures established manufacturers to innovate while maintaining competitive pricing.

- •Technical limitations in developing bio-based resins with comparable performance to traditional petrochemical-based resins restrict rapid adoption in certain applications.

- •Supply chain disruptions, including logistics challenges and raw material shortages, affect timely delivery and production continuity, especially in emerging markets.

- •Complexity in formulating adhesive resins that meet diverse end-use requirements across industries necessitates significant R&D investment and technical expertise.

- •Market fragmentation and lack of standardized testing methods for adhesive performance complicate product validation and customer acceptance.

Regulatory Framework

- •REACH Regulation (Registration, Evaluation, Authorization and Restriction of Chemicals) implemented between 2018 and 2025 imposes stringent requirements on chemical substances used in adhesive resins, mandating registration and safety evaluation to protect human health and the environment.

- •The U.S. EPA's Toxic Substances Control Act (TSCA) amendments enacted in 2016 with ongoing enforcement through 2025 require manufacturers to comply with chemical safety assessments and reporting for adhesive resin components, impacting product formulations.

- •VOC (Volatile Organic Compound) emission limits set by the California Air Resources Board (CARB) and the European Union's Solvent Emissions Directive between 2019 and 2025 necessitate development of low-VOC adhesive resins to reduce environmental pollution.

- •Occupational Safety and Health Administration (OSHA) standards updated between 2020 and 2025 mandate safe handling, storage, and exposure control of adhesive resin chemicals in workplace environments, influencing manufacturing practices.

- •China's Ministry of Ecology and Environment introduced regulations from 2018 to 2025 focusing on chemical management and environmental protection, requiring adhesive resin producers to adhere to strict emission and waste disposal norms.

Market Intelligence

- •15th February 2025, Huntsman Corporation launched a new line of bio-based epoxy resins designed for automotive and electronics applications, offering enhanced environmental sustainability without compromising performance. This innovation targets the growing demand for eco-friendly adhesives with reduced carbon footprint, aligning with global regulatory trends. The product features improved thermal stability and bonding strength, supporting lightweight component assembly. Huntsman aims to strengthen its market position in North America and Asia-Pacific through this launch, anticipating significant adoption in electric vehicle manufacturing and consumer electronics. Source: Huntsman Corporation Official Press Release

- •3rd March 2025, BASF SE introduced an advanced waterborne acrylic adhesive resin platform aimed at the packaging industry, emphasizing low VOC emissions and recyclability. The new resins enable flexible packaging solutions with superior adhesion to diverse substrates, enhancing product protection and shelf life. BASF's strategic focus on sustainability and regulatory compliance positions it competitively in Europe and Asia-Pacific markets. The innovation supports brand differentiation and meets increasing consumer demand for environmentally responsible packaging materials. Source: BASF SE Corporate Announcement

- •20th May 2024, Dow Inc. announced a strategic partnership with a leading electronics manufacturer to co-develop high-performance silicone adhesive resins for wearable devices. The collaboration aims to deliver adhesives with improved flexibility, thermal management, and biocompatibility, addressing the rapidly growing wearable technology segment. This initiative enhances Dow's product portfolio and accelerates market penetration in North America and Asia-Pacific regions. The partnership exemplifies industry trends towards customized adhesive solutions tailored to emerging applications. Source: Dow Inc. Press Release

- •10th January 2025, Wanhua Chemical Group completed the acquisition of a specialty resin producer to expand its adhesive resin offerings, particularly in polyurethane adhesives. The acquisition enhances Wanhua's manufacturing capacity and technical capabilities, supporting growth in automotive and construction sectors across Asia-Pacific. This move strengthens the company's competitive position through product portfolio diversification and regional market expansion. The consolidation reflects ongoing industry trends of mergers and acquisitions aimed at achieving economies of scale and innovation leadership. Source: Wanhua Chemical Group Corporate Statement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 14.2 Billion |

| Forecast Year Market Size | USD 30.8 Billion |

| CAGR | 8.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.2% |

| Scope of Report | Market is segmented by Adhesive Resin Type (Epoxy Resins, Acrylic Resins, Polyurethane Adhesives, Silicone Resins, Polyester Resins), Application Segment (Construction Adhesives, Automotive Adhesives, Packaging Adhesives, Electronics Adhesives, Woodworking Adhesives), Service Type (Custom Resin Formulation, Standard Resin Supply, Technical Support Services, After-Sales Service), Deployment Model (Bulk Resin Supply, Pre-Formulated Adhesive Products, On-Site Mixing Services) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Huntsman Corporation (United States), Hexion Inc. (United States), BASF SE (Germany), Dow Inc. (United States), DIC Corporation (Japan), Sika AG (Switzerland), Henkel AG & Co. KGaA (Germany), MITSUI Chemicals Inc. (Japan), Kumho P&B Chemicals Inc. (South Korea), Arkema S.A. (France), Wanhua Chemical Group Co. Ltd. (China), Kuraray Co. Ltd. (Japan), Eastman Chemical Company (United States), Synthomer plc (United Kingdom), Evonik Industries AG (Germany), Jowat SE (Germany), 3M Company (United States), Momentive Performance Materials Inc. (United States), Celanese Corporation (United States), LG Chem Ltd. (South Korea), Shin-Etsu Chemical Co. Ltd. (Japan), Allnex (Germany), Nippon Paint Holdings Co. Ltd. (Japan), H.B. Fuller Company (United States), Sasol Limited (South Africa) |

Global Adhesive Resin Market - Outlook 2020-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.