Global Broadcasting Equipment Market - Outlook 2024-2034

Global Broadcasting Equipment Market is segmented by Type (Transmitters, Receivers, Antennas, Mixers & Switchers, Encoders & Decoders), Application (Television Broadcasting, Radio Broadcasting, Online Streaming, Satellite Communication, Cable Broadcasting), End User Segment (Broadcasting Stations, Cable Operators, Satellite Providers, Online Media Platforms, Government Agencies), Technology Type (Analog Broadcasting Equipment, Digital Broadcasting Equipment, IP-based Broadcasting Equipment), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Broadcasting Equipment market comprises a wide range of hardware and systems that enable the transmission and reception of audio and video content via multiple platforms such as television, radio, satellite, cable, and online streaming. This market includes vital components like transmitters, receivers, antennas, mixers, switchers, and encoders, supporting the entire content delivery chain from production to consumer. It serves diverse stakeholders including broadcasters, cable operators, satellite companies, and digital streaming platforms. Technological advancements such as IP-based broadcasting and digital signal processing have broadened the market scope, incorporating both traditional and emerging digital platforms. The industry's evolution is shaped by increasing demand for high-quality content delivery, expanding internet penetration, and the shift towards OTT and streaming services. Regulatory frameworks and standardization efforts also influence market dynamics, ensuring compliance and interoperability across regions. Overall, the market is pivotal for media dissemination worldwide, addressing the growing consumer demand for seamless and versatile broadcasting solutions.

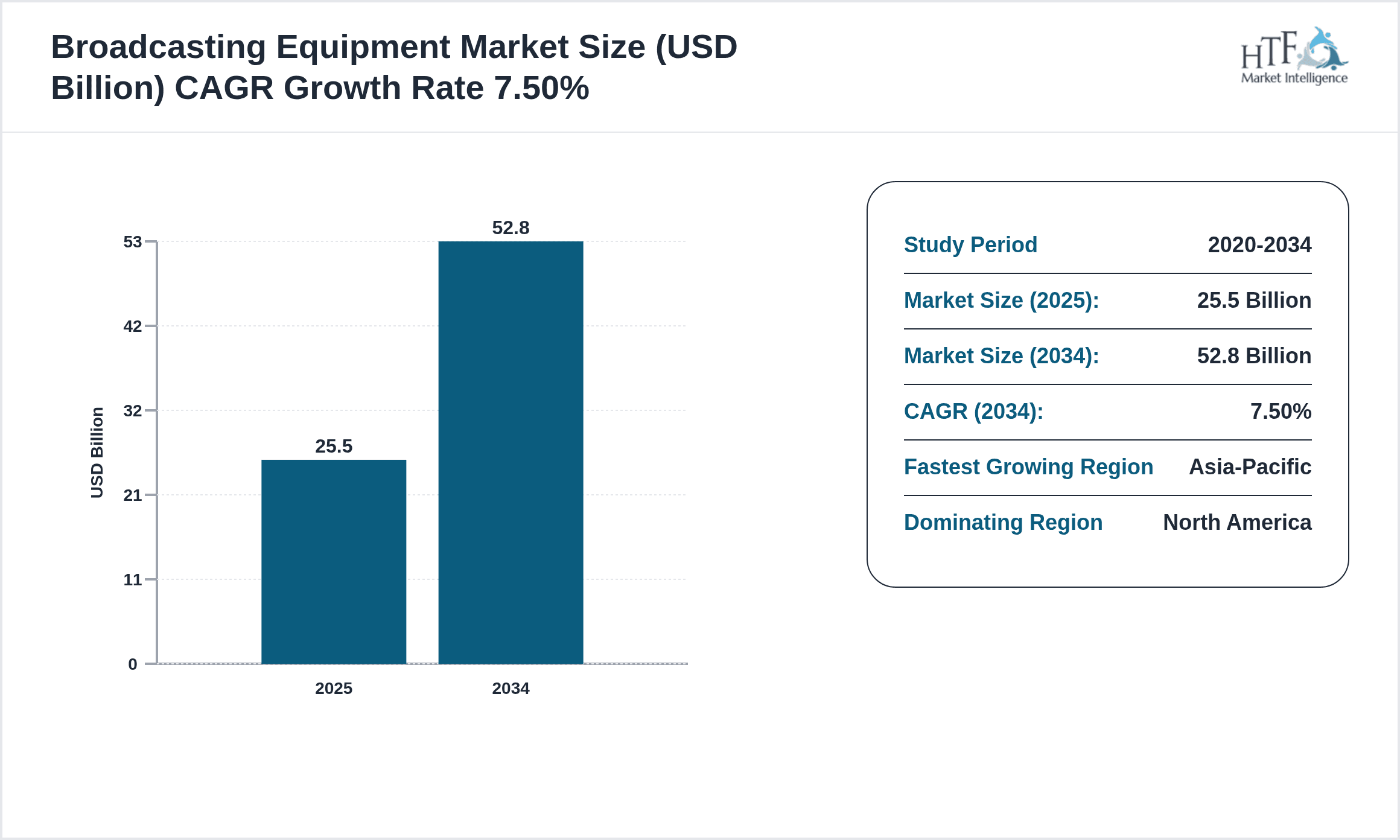

- •The Broadcasting Equipment market is projected to grow robustly, with a forecasted CAGR of 7.5% from 2024 to 2034, expanding from USD 25.5 billion in 2024 to an estimated USD 52.8 billion by 2034. North America currently dominates the market due to its advanced broadcasting infrastructure and high technology adoption rates, while the Asia-Pacific region is emerging as the fastest-growing market, driven by rising digitalization and increasing investments in broadcasting networks. Transmitters lead the product type segment, but encoders and decoders are gaining momentum owing to the rise of IP-based and digital broadcasting. Television broadcasting remains the largest application segment, closely followed by online streaming services which are rapidly expanding. These trends underscore a strategic shift towards digital and internet-based broadcasting solutions, signaling opportunities for innovation and market expansion globally.

- •The global Broadcasting Equipment market offers significant value propositions to broadcasters, content providers, and technology manufacturers by enabling reliable and efficient content transmission across multiple channels. Its strategic importance is amplified by the growing consumer demand for high-definition content and real-time streaming, necessitating advanced equipment with enhanced capabilities. The market supports various industries including media, entertainment, telecommunications, and information technology, facilitating business growth and customer engagement. Innovations in broadcasting technology such as cloud-based solutions, AI-driven content management, and 5G integration are creating new revenue streams and operational efficiencies. Consequently, stakeholders benefit from improved service quality, expanded reach, and competitive advantages in an increasingly digital and connected ecosystem.

Competitive Landscape

The global Broadcasting Equipment market features a competitive environment characterized by a mix of established multinational corporations and emerging technology innovators. Market players compete primarily through technological innovation, product differentiation, and strategic collaborations. Companies focus on developing cutting-edge equipment that supports digital broadcasting, IP-based transmission, and integration with OTT platforms to maintain competitive positioning. Strategic partnerships, mergers and acquisitions, and expansion into emerging markets are common tactics to enhance market share and geographic presence. Pricing strategies balance between premium advanced solutions and cost-effective options tailored for developing regions. The competitive rivalry drives continuous investment in R&D, fostering innovation in signal processing, compression technologies, and software-defined broadcasting systems. Market entry barriers include high capital requirements, need for technical expertise, and regulatory compliance, which protect incumbents while challenging new entrants. Future competition will likely intensify with the convergence of broadcasting and telecommunications technologies shaping new business models and ecosystem partnerships.

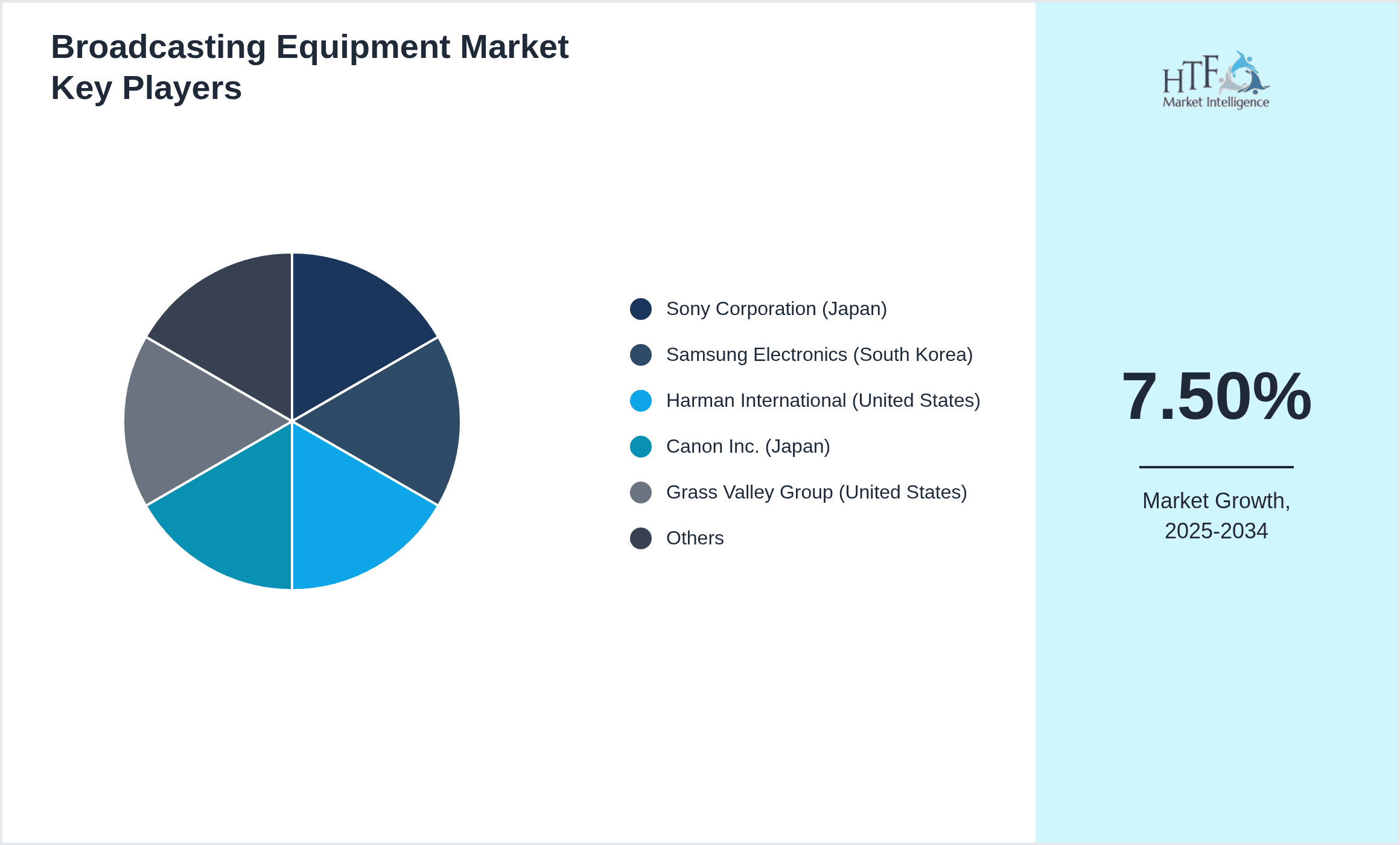

Prominent Players in Broadcasting Equipment Market

- •Sony Corporation (Japan)

- •Samsung Electronics (South Korea)

- •Harman International (United States)

- •Canon Inc. (Japan)

- •Grass Valley Group (United States)

- •Blackmagic Design (Australia)

- •NEC Corporation (Japan)

- •Panasonic Corporation (Japan)

- •ARRIS International (United States)

- •Rohde & Schwarz (Germany)

- •Avid Technology (United States)

- •Imagine Communications (United States)

- •Evertz Microsystems (Canada)

- •Calrec Audio (United Kingdom)

- •Barco NV (Belgium)

- •Lawo AG (Germany)

- •Matrox Graphics (Canada)

- •Tektronix Inc. (United States)

- •JVC Kenwood Corporation (Japan)

- •Tata Elxsi (India)

- •Hitachi Kokusai Electric (Japan)

- •For-A Company Limited (Japan)

- •Sony Professional Solutions (Japan)

- •Telestream, Inc. (United States)

- •Grass Valley USA LLC (United States)

Market Breakdown

- •By Type

- ◦Transmitters

- ◦Receivers

- ◦Antennas

- ◦Mixers & Switchers

- ◦Encoders & Decoders

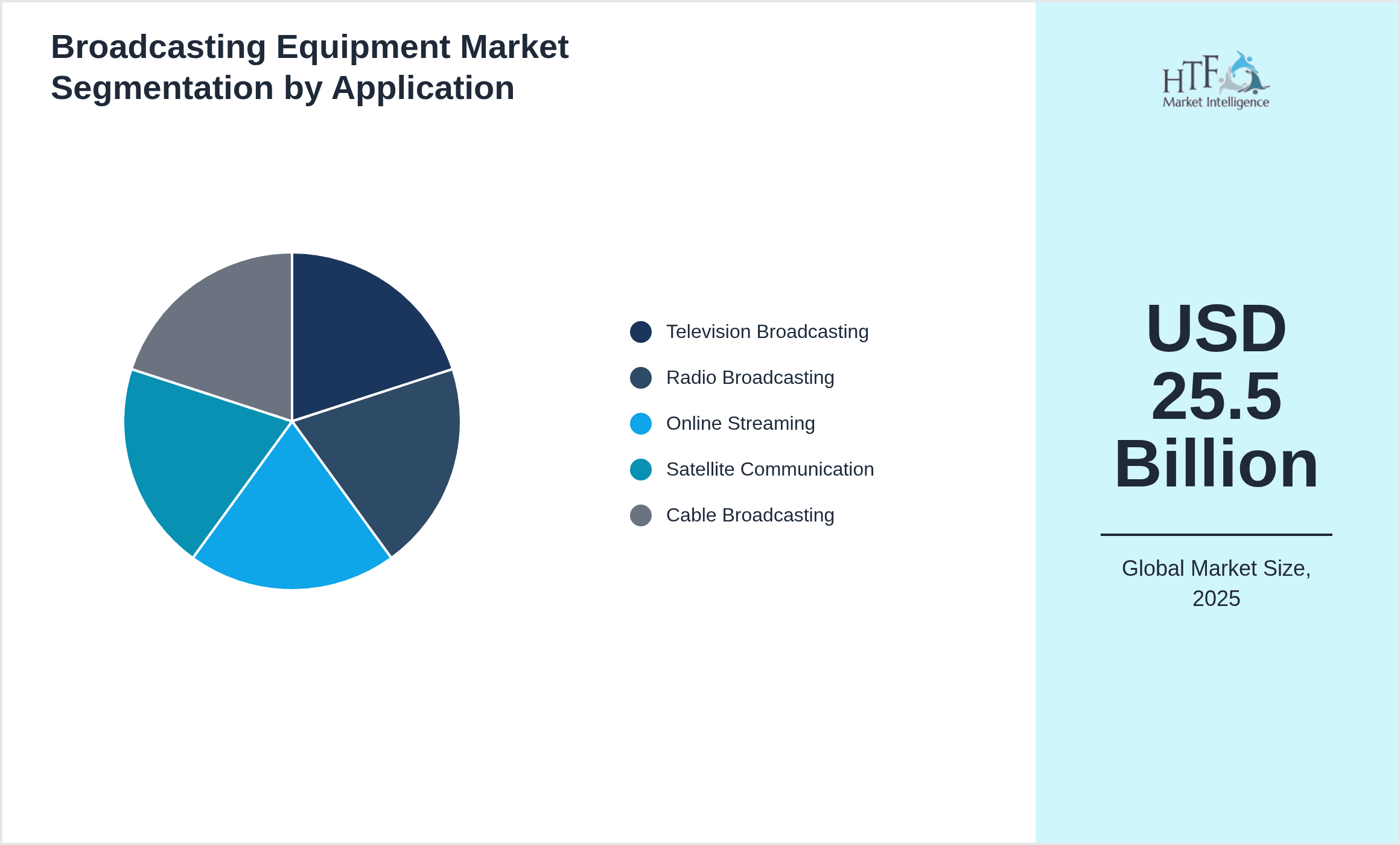

- •By Application

- ◦Television Broadcasting

- ◦Radio Broadcasting

- ◦Online Streaming

- ◦Satellite Communication

- ◦Cable Broadcasting

- •By End User Segment

- ◦Broadcasting Stations

- ◦Cable Operators

- ◦Satellite Providers

- ◦Online Media Platforms

- ◦Government Agencies

- •By Technology Type

- ◦Analog Broadcasting Equipment

- ◦Digital Broadcasting Equipment

- ◦IP-based Broadcasting Equipment

Growth Dynamics

The global Broadcasting Equipment market's growth is primarily driven by the increasing demand for high-quality, real-time content delivery across multiple platforms. The proliferation of digital media and the shift towards IP-based broadcasting have fostered the adoption of advanced equipment such as encoders and decoders. Moreover, rising internet penetration and smartphone usage in emerging economies are expanding market reach, particularly in Asia-Pacific, fueling investment in modern broadcasting infrastructure. Technological innovations like 4K/8K broadcasting and cloud-based content distribution further accelerate growth by enhancing user experience and operational efficiency. Additionally, regulatory mandates for digital migration in various regions compel broadcasters to upgrade their equipment, boosting market expansion. The convergence of traditional and OTT platforms is also creating new revenue streams and driving demand for versatile, interoperable broadcasting solutions that support multi-format content delivery.

Market Trends

A significant trend shaping the Broadcasting Equipment market is the rapid adoption of IP-based broadcasting technologies, enabling broadcasters to transmit content over internet protocols rather than traditional satellite or terrestrial methods. This shift facilitates greater flexibility, scalability, and cost-efficiency, supporting the rise of OTT services and multi-platform content consumption. Additionally, there is an increasing integration of AI and machine learning in broadcasting workflows for automated content management, quality enhancement, and targeted advertising. The emergence of cloud-based broadcasting solutions allows for remote production and distribution, further transforming operational models. Sustainability is gaining importance, with companies focusing on energy-efficient equipment and green broadcasting practices. The ongoing transition to ultra-high-definition (UHD) formats such as 4K and 8K is also driving equipment upgrades. Collaborative partnerships between technology providers and broadcasters to develop innovative solutions remain a key market dynamic.

Market Opportunities

Growing demand for online streaming and OTT platforms opens substantial opportunities for broadcasting equipment providers to innovate and supply specialized encoders, decoders, and IP-based transmission systems tailored for internet delivery. The expansion of 5G networks globally offers enhanced bandwidth and low latency, enabling broadcasters to deliver high-quality live content to mobile users, creating new market segments. Emerging economies investing in digital infrastructure present untapped markets requiring cost-effective and scalable broadcasting solutions. Furthermore, integration of AI-driven analytics and automation tools in broadcasting workflows is a lucrative area for product development, improving operational efficiency and viewer engagement. Collaborations with content creators and telecom operators can unlock bundled service offerings, expanding revenue streams. The rising trend toward green broadcasting equipment aligned with sustainability goals also provides opportunities to differentiate products and meet regulatory requirements.

Market Challenges

The Broadcasting Equipment market faces challenges including high capital expenditure required for upgrading legacy infrastructure to digital and IP-based systems, which can be prohibitive for smaller broadcasters and emerging markets. Complex regulatory environments across different regions create compliance burdens and delay technology adoption. Additionally, rapid technological change demands continuous R&D investment from manufacturers to maintain competitiveness, increasing operational costs. Interoperability issues among equipment from different vendors can hamper seamless content delivery and complicate system integration. Market saturation in developed regions leads to pricing pressures and margin erosion. Cybersecurity risks associated with IP-based broadcasting systems also pose significant concerns, requiring robust protective measures. Furthermore, the COVID-19 pandemic caused supply chain disruptions impacting equipment availability and project timelines, highlighting vulnerabilities in global manufacturing.

Regulatory Framework

Between 2020 and 2024, multiple regions implemented regulations mandating the transition from analog to digital broadcasting, compelling broadcasters to upgrade equipment for signal compatibility and quality standards. Notably, the International Telecommunication Union (ITU) updated guidelines on spectrum allocation and interference management to optimize broadcasting frequencies globally. The European Union introduced stricter energy efficiency requirements for broadcasting equipment, promoting sustainable production and usage. In North America, the Federal Communications Commission (FCC) enforced compliance with advanced encryption standards to secure digital transmissions, impacting equipment design. Additionally, data privacy laws affecting streaming and broadcasting services have necessitated robust content protection technologies. Government incentives in Asia-Pacific for digital infrastructure development have accelerated market growth by supporting equipment modernization. Overall, evolving regulatory landscapes across regions continue to shape product innovation, market entry, and compliance strategies within the broadcasting equipment industry.

Market Intelligence

- •15th January 2024, Sony Corporation launched its latest line of 8K broadcasting cameras and encoders designed to support next-generation ultra-high-definition content delivery across terrestrial and satellite networks. These products feature enhanced image processing capabilities, improved signal compression, and compatibility with IP-based workflows, targeting broadcasters transitioning to advanced formats. The launch aims to capture demand from markets investing in UHD infrastructure and to strengthen Sony's competitive position in professional broadcasting equipment. This innovation supports broadcasters' needs for high-resolution content production and efficient transmission, aligning with rising consumer expectations for premium viewing experiences.

- •10th October 2023, Harman International announced a strategic partnership with leading OTT platform providers to develop integrated audio broadcasting solutions featuring immersive sound technologies and AI-driven audio optimization. This collaboration focuses on enhancing streaming quality and personalized listener experiences for radio and digital broadcasters. The initiative includes co-development of hardware and software components that enable seamless integration with cloud-based streaming services. This move positions Harman as a key player in the evolving digital broadcasting ecosystem and addresses growing demand for superior audio quality in online content delivery.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 25.5 Billion |

| Forecast Year Market Size | USD 52.8 Billion |

| CAGR | 7.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.2% |

| Scope of Report | Market is segmented by Type (Transmitters, Receivers, Antennas, Mixers & Switchers, Encoders & Decoders), Application (Television Broadcasting, Radio Broadcasting, Online Streaming, Satellite Communication, Cable Broadcasting), End User Segment (Broadcasting Stations, Cable Operators, Satellite Providers, Online Media Platforms, Government Agencies), Technology Type (Analog Broadcasting Equipment, Digital Broadcasting Equipment, IP-based Broadcasting Equipment) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Sony Corporation (Japan), Samsung Electronics (South Korea), Harman International (United States), Canon Inc. (Japan), Grass Valley Group (United States), Blackmagic Design (Australia), NEC Corporation (Japan), Panasonic Corporation (Japan), ARRIS International (United States), Rohde & Schwarz (Germany), Avid Technology (United States), Imagine Communications (United States), Evertz Microsystems (Canada), Calrec Audio (United Kingdom), Barco NV (Belgium), Lawo AG (Germany), Matrox Graphics (Canada), Tektronix Inc. (United States), JVC Kenwood Corporation (Japan), Tata Elxsi (India), Hitachi Kokusai Electric (Japan), For-A Company Limited (Japan), Sony Professional Solutions (Japan), Telestream, Inc. (United States), Grass Valley USA LLC (United States) |

Global Broadcasting Equipment Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.