EMEA Packaging Robotic Arms Market - Europe Size & Outlook 2025-2034

EMEA Packaging Robotic Arms Market is segmented by Type (Articulated Robotic Arms, SCARA Robotic Arms, Delta Robotic Arms, Cartesian Robotic Arms, Cylindrical Robotic Arms), Application (Primary Packaging, Secondary Packaging, Palletizing, Sorting, Inspection), End User (Food & Beverage Industry, Pharmaceutical Industry, Consumer Goods, Logistics & Warehousing, Automotive Industry), Deployment Model (Fixed Robotic Arms, Mobile Robotic Arms, Collaborative Robotic Arms (Cobots)), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Packaging Robotic Arms Market is a dynamic sector focused on deploying robotic arms to automate packaging operations across Europe, the Middle East, and Africa. It involves a range of robotic arm types such as articulated, SCARA, delta, Cartesian, and cylindrical robots, which are employed for applications including primary packaging, secondary packaging, palletizing, sorting, and inspection. This market serves diverse industries such as food & beverage, pharmaceuticals, consumer goods, and logistics, aiming to enhance operational efficiency, reduce manual labor, and improve packaging precision. The integration of advanced technologies like machine vision and AI into robotic systems is driving innovation and adoption across the region. Increasing demand for automation due to labor cost pressures and the need for faster production cycles further expands the market scope. The market's boundaries encompass hardware, software, and services related to robotic packaging solutions, creating opportunities for manufacturers, system integrators, and end users throughout the EMEA region.

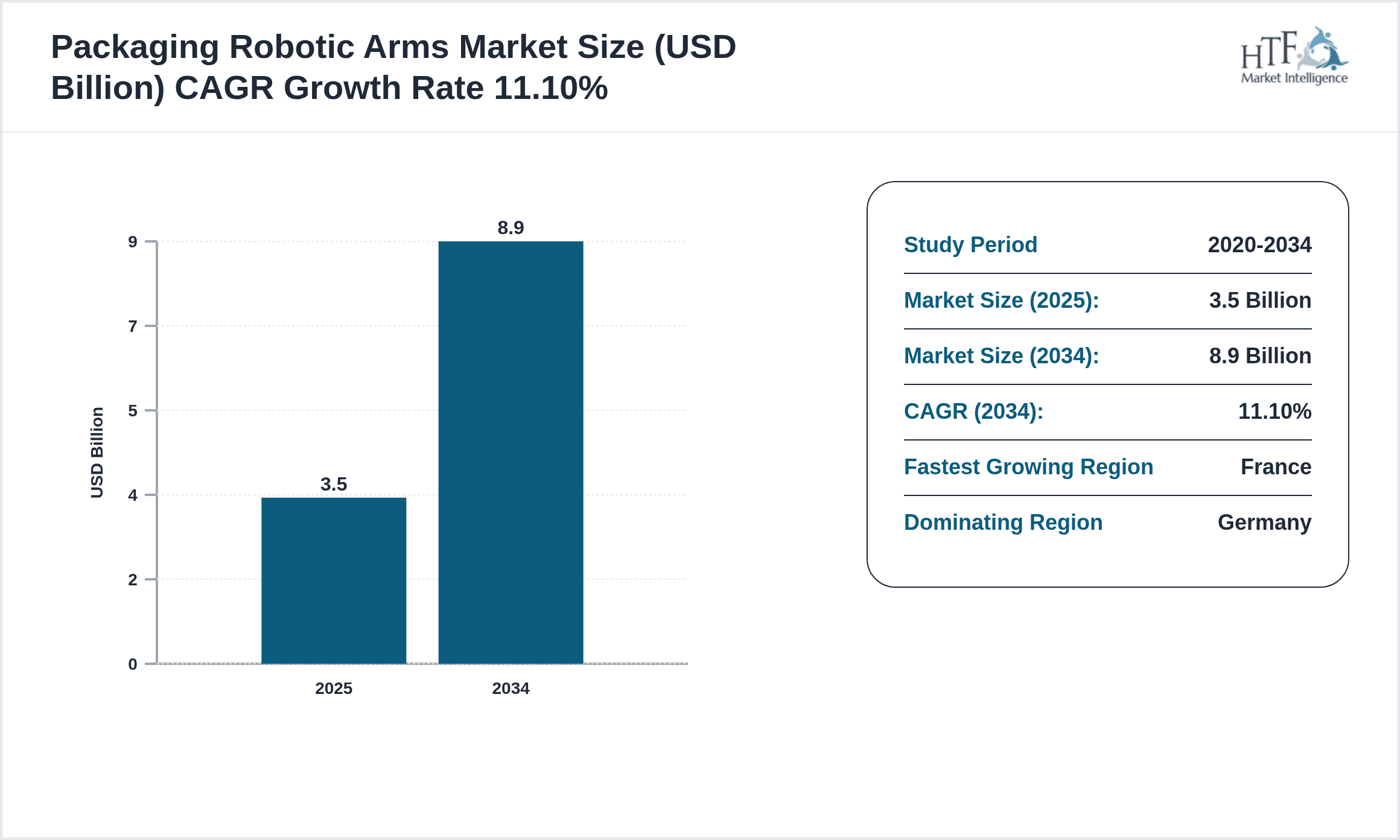

- •Key highlights include a base market size of USD 3.5 Billion in 2025 with a projected growth to USD 8.9 Billion by 2034, representing a CAGR of 11.1%. Germany leads the market in terms of size and technological adoption, while France is identified as the fastest-growing country driven by investments in industrial automation. Articulated robotic arms dominate due to their versatility, with delta robotic arms showing the fastest growth owing to their speed and precision in packaging tasks. Applications such as primary and secondary packaging hold the largest market shares because of their critical role in product protection and presentation.

- •The value proposition of the EMEA Packaging Robotic Arms Market lies in its ability to transform traditional packaging processes through automation, delivering enhanced productivity, operational consistency, and cost savings. This market is strategically important for manufacturers seeking to meet increasing consumer demands for quality and customization, while complying with stringent regulatory standards. Stakeholders including robotics manufacturers, integrators, and end users benefit from continuous technological innovation, expanding applications, and supportive government initiatives promoting Industry 4.0 adoption across EMEA nations.

Competitive Landscape

The competitive environment in the EMEA Packaging Robotic Arms Market is characterized by intense rivalry among global and regional players who focus heavily on innovation, strategic partnerships, and technological differentiation to capture market share. Market leaders deploy cutting-edge robotic technologies integrating AI, machine vision, and IoT to offer customized packaging solutions that improve accuracy and speed. The competition also hinges on expanding service portfolios, including maintenance and system integration, to provide end-to-end solutions. Pricing strategies vary with product sophistication and customer segments, influencing adoption rates in different EMEA countries. Additionally, mergers and acquisitions shape the landscape by enabling companies to consolidate technological capabilities and geographical reach. Barriers to entry include high capital investment requirements and technical expertise, which protect established players. The market is also marked by regional competition, with Western European countries leading adoption and emerging markets in the Middle East and Africa showing rapid growth potential.

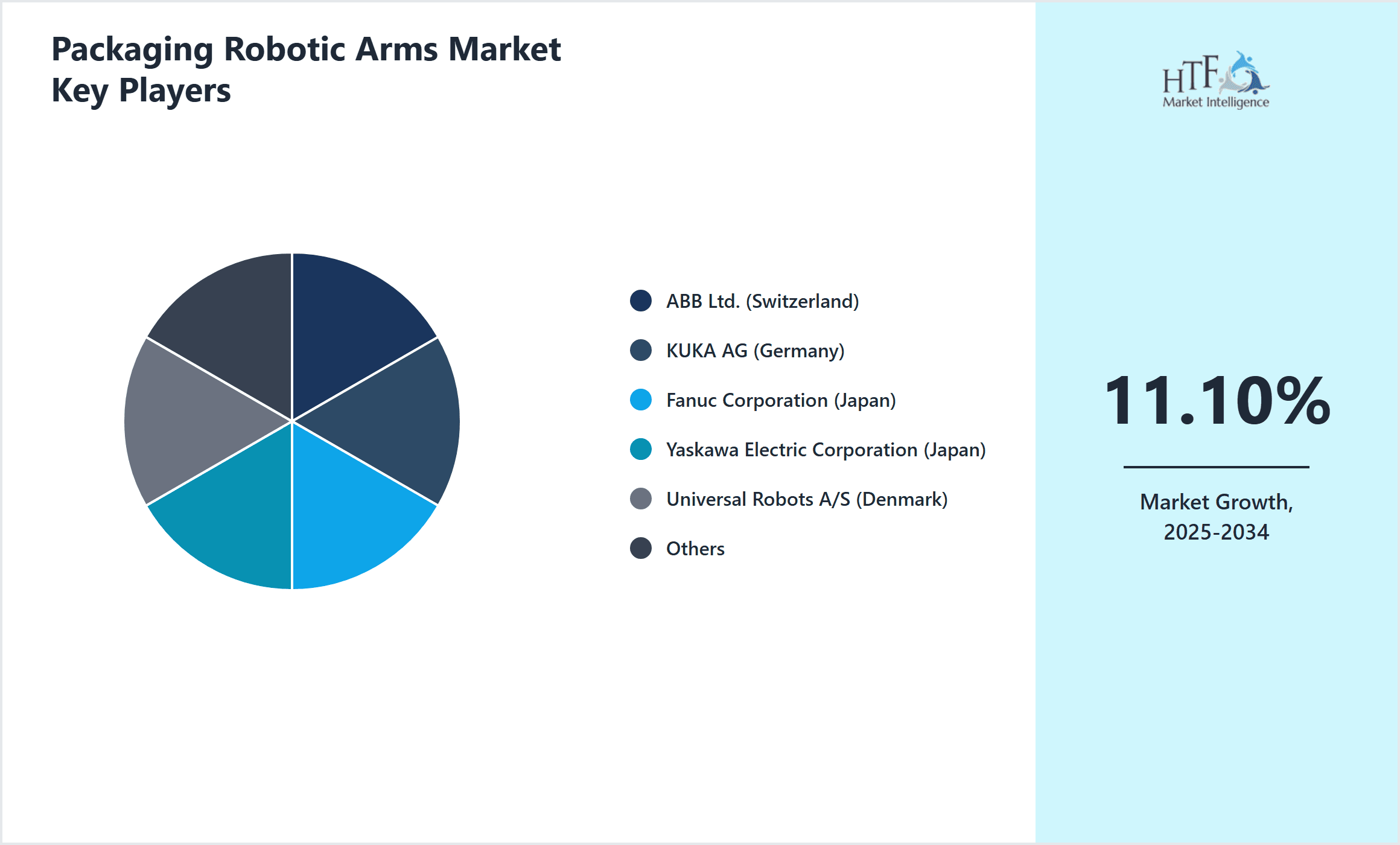

Prominent Players in EMEA Packaging Robotic Arms Market

- •ABB Ltd. (Switzerland)

- •KUKA AG (Germany)

- •Fanuc Corporation (Japan)

- •Yaskawa Electric Corporation (Japan)

- •Universal Robots A/S (Denmark)

- •Mitsubishi Electric Corporation (Japan)

- •Epson Robots (Japan)

- •Stäubli International AG (Switzerland)

- •Comau S.p.A. (Italy)

- •Omron Corporation (Japan)

- •Bosch Rexroth AG (Germany)

- •Denso Corporation (Japan)

- •Nachi-Fujikoshi Corp. (Japan)

- •Kawasaki Heavy Industries Ltd. (Japan)

- •Precise Automation, Inc. (Sweden)

- •FANUC Europe Corporation (Germany)

- •Techman Robot Inc. (Taiwan)

- •Adept Technology, Inc. (United States)

- •Toshiba Machine Co., Ltd. (Japan)

- •Aubo Robotics (China)

- •Universal Robots (Denmark)

- •Staubli Robotics (Switzerland)

- •Robotiq (Canada)

- •OnRobot ApS (Denmark)

- •Siasun Robot & Automation Co., Ltd. (China)

Market Breakdown

- •By Type

- ◦Articulated Robotic Arms

- ◦SCARA Robotic Arms

- ◦Delta Robotic Arms

- ◦Cartesian Robotic Arms

- ◦Cylindrical Robotic Arms

- •By Application

- ◦Primary Packaging

- ◦Secondary Packaging

- ◦Palletizing

- ◦Sorting

- ◦Inspection

- •By End User

- ◦Food & Beverage Industry

- ◦Pharmaceutical Industry

- ◦Consumer Goods

- ◦Logistics & Warehousing

- ◦Automotive Industry

- •By Deployment Model

- ◦Fixed Robotic Arms

- ◦Mobile Robotic Arms

- ◦Collaborative Robotic Arms (Cobots)

Growth Dynamics

- •Rising labor costs and increasing demand for automation in packaging processes across EMEA countries are significantly driving market growth. Companies are investing in robotic arms to improve efficiency and reduce human error, especially in high-volume packaging operations.

- •Technological advancements such as integration of AI, machine vision, and IoT with robotic arms are enhancing capabilities like real-time quality inspection and adaptive packaging, making these solutions more attractive to end-users.

- •Government initiatives supporting Industry 4.0 and automation, especially in European countries like Germany and France, provide subsidies and incentives that accelerate adoption of packaging robotic arms.

- •The growing e-commerce sector in the EMEA region demands faster and more precise packaging solutions, further propelling the deployment of robotic arms in logistics and warehousing applications.

- •Collaborative robots (cobots) that work alongside human operators are gaining popularity due to their flexibility and ease of deployment, expanding the market beyond traditional industrial settings.

Market Trends

- •There is a notable trend towards the adoption of delta robotic arms in packaging due to their high-speed capabilities and precision, particularly in food and pharmaceutical packaging lines.

- •Integration of cloud computing and data analytics with robotic arms enables predictive maintenance and improved operational efficiency, aligning with Industry 4.0 standards.

- •Sustainability trends drive the use of robotic arms to optimize material usage and reduce packaging waste, supporting corporate environmental goals.

- •Increasing demand for customized packaging solutions is encouraging the development of flexible robotic arms capable of handling diverse product types and sizes.

- •Robotic arms equipped with advanced sensors and vision systems enable enhanced inspection and quality control, reducing product recalls and improving brand reputation.

Market Opportunities

- •Emerging markets within the Middle East and Africa present significant growth opportunities as industries modernize and adopt automation technologies to increase competitiveness.

- •Developing collaborative robotic arms tailored for small and medium enterprises (SMEs) offers a large untapped segment to expand market penetration in EMEA.

- •Technological advancements enabling multi-functional robotic arms that can perform packaging and inspection simultaneously can create value-added solutions for end users.

- •Expansion of e-commerce and pharmaceutical sectors in the EMEA region drives demand for automated packaging, opening avenues for customized robotic solutions.

- •Strategic partnerships between robotics manufacturers and packaging companies can accelerate product innovation and market access.

Market Challenges

- •High initial investment costs and maintenance expenses of robotic arms limit adoption, especially among small and medium enterprises in the EMEA region.

- •Lack of skilled workforce capable of programming and maintaining robotic systems poses a significant barrier to market growth.

- •Regulatory complexities and compliance with safety standards across diverse EMEA countries create challenges for manufacturers and end users alike.

- •Integration issues with existing packaging lines and legacy systems can lead to operational disruptions and increased costs.

- •Cybersecurity concerns related to connected robotic systems require robust solutions to protect against data breaches and operational failures.

Regulatory Framework

- •Between 2020 and 2025, the Machinery Directive (2006/42/EC) was reinforced across EMEA countries, emphasizing stringent safety compliance and risk assessment protocols for robotic packaging arms, impacting design and deployment.

- •The EU’s General Data Protection Regulation (GDPR), effective since 2018, has influenced robotic system manufacturers to enhance data security features, especially for cloud-connected robotic packaging arms.

- •New ISO standards such as ISO 10218-2:2021 for robot safety have been adopted widely in EMEA, requiring manufacturers to meet higher operational safety benchmarks.

- •Specific country-level regulations in Germany and France focus on environmental impact, mandating energy-efficient robotic systems and promoting sustainable manufacturing practices.

- •Government-backed Industry 4.0 initiatives across EMEA provide regulatory support and financial incentives to encourage automation investments in manufacturing and packaging sectors.

Market Intelligence

- •15th March 2024, ABB Ltd. launched its new generation of collaborative robotic arms designed specifically for secondary packaging applications in the EMEA region. The robots integrate enhanced AI capabilities for real-time quality inspection and adaptive packaging, targeting food and pharmaceutical industries. This development is expected to boost operational efficiency and reduce downtime significantly. ABB aims to strengthen its market leadership by offering flexible, scalable solutions that align with Industry 4.0 standards.

- •22nd August 2024, KUKA AG introduced an innovative delta robotic arm featuring ultra-high-speed capabilities and energy-efficient operation tailored for fast-paced primary packaging lines. The product launch includes smart sensor integration for precise sorting and palletizing, enhancing throughput by up to 30%. KUKA’s strategic focus on sustainability and automation excellence is anticipated to increase adoption across EMEA manufacturing sectors.

- •10th January 2025, Universal Robots A/S announced a strategic partnership with a leading European packaging solutions provider to co-develop customized robotic arms for small and medium-sized enterprises. The collaboration aims to lower entry barriers for automation by offering affordable, easy-to-integrate robots with simplified programming interfaces. This initiative targets the rapidly growing SMEs market segment within EMEA’s packaging industry.

- •3rd April 2025, Mitsubishi Electric Corporation completed the deployment of its advanced Cartesian robotic arms in a major pharmaceutical packaging facility in France. The technology enables precise inspection and packaging of sensitive drug products, meeting stringent regulatory requirements. This strategic implementation underscores the growing importance of automation in pharmaceutical supply chains across EMEA.

- •Source: Official press releases from ABB Ltd., KUKA AG, Universal Robots A/S, Mitsubishi Electric Corporation

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.5 Billion |

| Forecast Year Market Size | USD 8.9 Billion |

| CAGR | 11.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.1% |

| Scope of Report | Market is segmented by Type (Articulated Robotic Arms, SCARA Robotic Arms, Delta Robotic Arms, Cartesian Robotic Arms, Cylindrical Robotic Arms), Application (Primary Packaging, Secondary Packaging, Palletizing, Sorting, Inspection), End User (Food & Beverage Industry, Pharmaceutical Industry, Consumer Goods, Logistics & Warehousing, Automotive Industry), Deployment Model (Fixed Robotic Arms, Mobile Robotic Arms, Collaborative Robotic Arms (Cobots)) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | ABB Ltd. (Switzerland), KUKA AG (Germany), Fanuc Corporation (Japan), Yaskawa Electric Corporation (Japan), Universal Robots A/S (Denmark), Mitsubishi Electric Corporation (Japan), Epson Robots (Japan), Stäubli International AG (Switzerland), Comau S.p.A. (Italy), Omron Corporation (Japan), Bosch Rexroth AG (Germany), Denso Corporation (Japan), Nachi-Fujikoshi Corp. (Japan), Kawasaki Heavy Industries Ltd. (Japan), Precise Automation, Inc. (Sweden), FANUC Europe Corporation (Germany), Techman Robot Inc. (Taiwan), Adept Technology, Inc. (United States), Toshiba Machine Co., Ltd. (Japan), Aubo Robotics (China), Universal Robots (Denmark), Staubli Robotics (Switzerland), Robotiq (Canada), OnRobot ApS (Denmark), Siasun Robot & Automation Co., Ltd. (China) |

EMEA Packaging Robotic Arms Market - Europe Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.